|

市場調查報告書

商品編碼

2073278

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

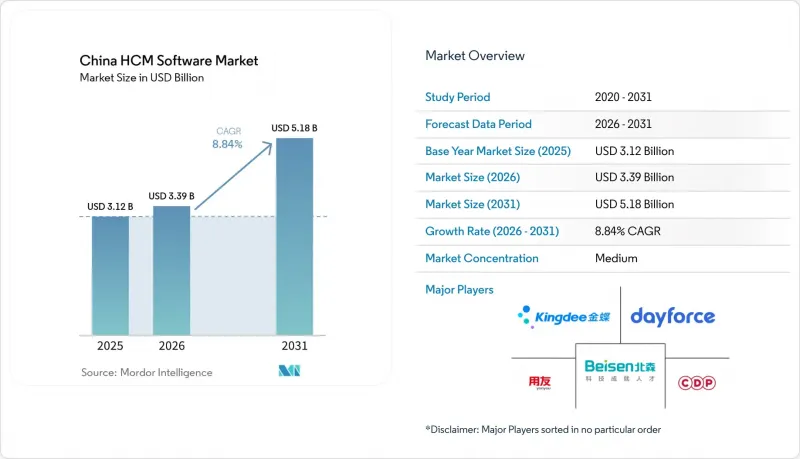

根據 Mordor Intelligence 預測,中國人力資源管理 (HCM) 軟體市場規模預計到 2025 年將達到 31.2 億美元,到 2026 年將達到 33.9 億美元,到 2031 年將達到 51.8 億美元,2026 年至 2031 年的複合年成長率為 8.84%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理、人力資源管理、薪資管理等)以及最終用戶產業(IT和電信、銀行、金融服務和保險等)進行細分。市場預測以美元計價。

中國人力資本管理軟體市場趨勢與洞察

推動企業數位轉型

由於傳統的本地部署套件無法提供即時分析,且難以適應快速變化的勞動法規,企業正在加快系統更新週期。寧波銀行等早期採用者透過部署整合招募、績效評估和繼任計畫的平台,將新員工培訓時間縮短了30%。揚州等城市實施的中小企業津貼計畫表明,公共資金可以克服預算限制,加速初期應用。零售商正在部署兼容零工人員的排班模組,以符合保護老年勞工的新法規;製造商正在將人力資本管理(HCM)整合到生產執行系統中,以應對訂單波動。雲端解決方案在靈活性和降低資本支出(CAPEX)方面都展現出優勢,從而導致供應商格局更加多元化,並加劇了中小企業用戶之間的價格競爭。這些努力共同推動了中國HCM軟體市場的復甦,擴大了目標客戶群,並提高了每位客戶的平均模組採用率。

政府針對國內軟體的「雲端優先」政策。

2026年政府工作報告明確了公共部門軟體「雲端優先」的策略,有效地引導市場需求流向能夠證明其國內託管能力的供應商。北森和用友已根據這一指南獲得了多個省級契約,兩家公司都強調獲得工信部認證,以確保數據主權,從而讓負責數據主權的機構放心。雖然混合部署在仍依賴傳統ERP薪資系統的國有企業中很常見,但即使是這些企業也在試行為新員工部署基於雲端的HCM系統,以實現政策目標。常規訂閱模式提高了供應商的知名度,而強制性資料本地化條款則增加了轉換成本,並提升了市場滲透率。在中國HCM軟體市場,這些因素將推動雲端業務在預測期間內保持兩位數的成長。

遵守嚴格的《個人資訊保護法》的成本

《個人資訊保護法》強制要求使用者明確同意、資料在地化和定期隱私審計,導致實施週期延長至多六個月。像Workday這樣的跨國公司必須營運本地資料中心或與國內雲端服務供應商合作才能通過安全審計,這增加了專案成本。小規模的本地負責人難以資金籌措合規人事費用和技術升級費用,限制了市場競爭的多樣性。生物識別考勤管理功能需要重新設計以確保獲得用戶同意,這導致新版本發布延遲。合規成本的增加正在阻礙整個中國人力資本管理(HCM)軟體市場供應商和買家的利潤成長。

細分市場分析

2025年,軟體授權收入佔總營收的75.24%,凸顯了中國人力資本管理(HCM)軟體市場歷來偏好資本化核心套件。然而,隨著企業將互動式代理培訓、隱私保護代碼審查以及雙薪資核算引擎維護等工作外包,預計到2031年,服務業將以9.62%的複合年成長率成長。供應商目前將監控31個省份社保法規變更的管理服務打包出售,將一次性部署轉化為持續的收入來源。受「AI Family 2.0」部署的推動,北森的服務業在2026年上半年實現了12%的同比成長。由於缺乏專職IT人員,中小企業依賴供應商提供的設置培訓,而國有企業則需要長期的變更管理支援來遷移數十年的人力資源資料。

績效定價模式的轉變日益明顯,買家將總薪酬與可量化的關鍵績效指標(KPI)掛鉤,例如更快的招募速度和更低的離職率。儘管服務預計將在中國人力資源管理(HCM)軟體市場佔據更大的佔有率,但軟體收入將轉向固定費率的雲端訂閱模式。 PIPL審計要求分階段實施,這進一步凸顯了這些服務的策略重要性。擁有內部法律和安全部門的供應商可以收取較高的日費,而小規模的競爭對手通常與專業顧問公司合作,這使得它們難以維持利潤率。因此,服務需求的激增正在擴大大型成熟企業與利基市場新進業者之間的績效差距,預計這一趨勢將在預測期內持續。

預計到2025年,雲端運算支出將占到總支出的62.82%,複合年成長率達9.18%,進一步鞏固其在中國人力資源管理(HCM)軟體市場的核心地位。 2026年政府工作報告中提出的「雲端優先」採購政策,正引導政府預算轉向提供國內託管服務的SaaS供應商。阿里雲和華為雲已獲得頂級安全認證,降低了公共部門採用雲端服務的門檻。私人企業也從中受益。多租戶更新實現了每月而非每季的AI增強,進一步提升了競爭力。雖然混合環境仍然是依賴本地ERP系統的企業的過渡方案,但雙堆疊架構帶來的成本增加正在加速企業全面遷移的藍圖。

由於地方政府補貼計劃僅涵蓋訂閱費用,而不包括本地硬體,中小企業紛紛湧向雲端以最大限度地降低資本支出。因此,使用者數量不斷成長,用於訓練人力資源人工智慧模式的廠商資料湖也日趨完善,由此形成良性循環,進一步凸顯了雲端解決方案與本地部署解決方案之間的差異。預計到2031年,在政策支援和功能增強的共同作用下,中國人力資本管理(HCM)軟體市場超過四分之三的佔有率將完全集中在雲端部署。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業推動數位轉型的需求日益成長。

- 政府針對國產軟體的「雲端優先」政策。

- 將人工智慧原生「智慧代理」引入人力資源工作流程

- 促進「新創造(國內IT堆疊)」的合規性

- 跨國業務擴張需要遵守全球薪資核算管理規定。

- 以數據分析主導的勞動力規劃,因應勞動力老化問題

- 市場限制因素

- 遵守嚴格的個人資料保護法的成本

- 與傳統ERP系統整合的複雜性

- 中小企業市場波動性大,供應商流失風險高

- 地方政府社會保險法規的差異

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- Core HR

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與技能發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Beisen Cloud Computing Co., Ltd.

- Yonyou Network Technology Co., Ltd.

- Kingdee International Software Group Company Limited

- CDP Holdings Co., Ltd.

- Dayforce, Inc.

- Cornerstone OnDemand Inc.

- Ultimate Software Group Inc.

- PeopleStrong Technologies Pvt. Ltd.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Workday Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing Inc.

- UKG Inc.

- Gaea Soft Group Co., Ltd.

- Xinren Xinshi Technology Co., Ltd.

- Ant Payslip Technology Co., Ltd.

- Honghai Cloud Computing Technology Co., Ltd.

- BenQ Guru Software Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china HCM software market size reached USD 3.12 billion in 2025 and is expected to reach USD 3.39 billion in 2026 and USD 5.18 billion by 2031, growing at a CAGR of 8.84% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

China HCM Software Market Trends and Insights

Rising Enterprise Digital Transformation Mandates

Corporations are accelerating refresh cycles because legacy on-premises suites cannot provide real-time analytics or comply with fast-shifting labor laws. Early adopters such as Ningbo Bank cut onboarding time by 30% after deploying an integrated platform that unifies recruitment, performance, and succession planning. Subsidized SME programs in cities like Yangzhou prove that public co-funding can offset budget limitations and stimulate first-time adoption. Retailers are buying gig-friendly scheduling modules to conform with new over-age worker protections, and manufacturers are embedding HCM with execution systems to cope with order volatility. Cloud alternatives win on both agility and lower capex, fragmenting the vendor roster and heightening price competition among SME buyers. Collectively, these initiatives boost the China HCM software market by widening the eligible customer pool and lifting average module penetration per customer.

Government Cloud-First Policies for Domestic Software

The 2026 Government Work Report codified a cloud-first stance for public-sector software, effectively channeling demand to vendors that can prove domestic hosting. Beisen and Yonyou secured multiple provincial contracts on the back of this directive, each emphasizing Ministry of Industry and Information Technology certification to reassure data-sovereignty watchdogs. Hybrid rollouts remain common in SOEs that still rely on legacy ERP payroll, but even those entities now pilot cloud HCM for new hires to satisfy policy targets. Recurring subscription economics improve vendor visibility, while mandatory data-localization clauses raise switching costs, reinforcing market stickiness. For the China HCM software market, this driver cements double-digit cloud growth well into the forecast window.

Stringent Personal Information Protection Law Compliance Costs

The Personal Information Protection Law requires explicit consent, data-localization, and regular privacy audits, lengthening implementation timelines by up to six months. Multinationals such as Workday must run local data centers or partner with domestic clouds to pass security reviews, adding to project cost bases. Smaller local vendors struggle to fund compliance staff and technical upgrades, constraining competitive diversity. Biometric time-tracking features need redesign to secure consent, delaying new releases. Higher compliance overhead tempers margin expansion for both suppliers and buyers across the China HCM software market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Native Intelligent Agent Adoption in HR Workflows

- Xinchuang Compliance Push

- Integration Complexity with Legacy ERP Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software licenses retained 75.24% of 2025 revenue, underscoring the historical preference for capitalized core suites within the China HCM software market share. Yet services are projected to grow at a 9.62% CAGR through 2031 as enterprises commission conversational-agent training, privacy-by-design code reviews, and dual payroll-engine maintenance. Vendors now bundle managed services that monitor social-insurance rule changes across 31 provinces, converting one-time implementations into annuity revenue. Beisen's services line rose 12% year-over-year during the first half of fiscal 2026 on the back of AI Family 2.0 rollouts. SMEs lean on vendor-run configuration workshops because they lack specialist IT staff, while SOEs require prolonged change-management support to migrate decades of personnel data.

The shift toward outcome-based pricing is visible as buyers tether fee pools to quantifiable KPIs such as onboarding speed or resignation-rate reduction. Over time, services will claim a larger slice of the China HCM software market size while software revenues migrate toward ratable cloud subscriptions. The strategic importance of services is further heightened by PIPL audits that compel phased deployments. Vendors that maintain in-house legal and security practices can charge premium day-rates, whereas smaller competitors often partner with boutique consultancies, reducing margin capture. Consequently, the services surge widens the performance gap between scaled incumbents and niche newcomers, a trend likely to persist throughout the forecast period.

Cloud captured 62.82% of spending in 2025 and is on track for a 9.18% CAGR, reinforcing its centrality to the China HCM software market. Mandatory cloud-first procurement in the 2026 Government Work Report redirects agency budgets to SaaS providers that provide domestic hosting. Alibaba Cloud and Huawei Cloud achieved top-tier security certification, easing public-sector onboarding hurdles. Private enterprises see parallel benefits: multi-tenant updates deliver AI enhancements monthly rather than quarterly, sharpening competitive edge. Hybrid remains a temporary bridge for firms saddled with on-premises ERP, but dual-stack costs are accelerating full migration roadmaps.

As municipal subsidy programs reimburse only subscription fees, not on-prem hardware, SMEs flock to the cloud to minimize capex. The resulting uptick in user seats improves vendor data lakes that train HR AI models, creating a feedback loop that further differentiates cloud from on-prem alternatives. By 2031, policy pull and feature push together are set to consolidate more than three-quarters of the China HCM software market size under pure-cloud deployments.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Core HR

- Talent Management

- Workforce Management

- Payroll Management

- Learning and Development

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

List of Companies Covered in this Report:

- Beisen Cloud Computing Co., Ltd.

- Yonyou Network Technology Co., Ltd.

- Kingdee International Software Group Company Limited

- CDP Holdings Co., Ltd.

- Dayforce, Inc.

- Cornerstone OnDemand Inc.

- Ultimate Software Group Inc.

- PeopleStrong Technologies Pvt. Ltd.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Workday Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing Inc.

- UKG Inc.

- Gaea Soft Group Co., Ltd.

- Xinren Xinshi Technology Co., Ltd.

- Ant Payslip Technology Co., Ltd.

- Honghai Cloud Computing Technology Co., Ltd.

- BenQ Guru Software Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Digital Transformation Mandates

- 4.2.2 Government Cloud-First Policies for Domestic Software

- 4.2.3 AI-Native "Intelligent Agent" Adoption in HR Workflows

- 4.2.4 Xinchuang (Domestic IT Stack) Compliance Push

- 4.2.5 Cross-Border Expansion Demanding Global Payroll Compliance

- 4.2.6 Analytics-Driven Workforce Planning for Ageing Workforce

- 4.3 Market Restraints

- 4.3.1 Stringent Personal Information Protection Law Compliance Costs

- 4.3.2 Integration Complexity with Legacy ERP Systems

- 4.3.3 Vendor Churn Risk in Volatile SME Segment

- 4.3.4 Fragmented Provincial Social Insurance Rules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Beisen Cloud Computing Co., Ltd.

- 6.4.2 Yonyou Network Technology Co., Ltd.

- 6.4.3 Kingdee International Software Group Company Limited

- 6.4.4 CDP Holdings Co., Ltd.

- 6.4.5 Dayforce, Inc.

- 6.4.6 Cornerstone OnDemand Inc.

- 6.4.7 Ultimate Software Group Inc.

- 6.4.8 PeopleStrong Technologies Pvt. Ltd.

- 6.4.9 Zoho Corporation Pvt. Ltd.

- 6.4.10 Ramco Systems Limited

- 6.4.11 Workday Inc.

- 6.4.12 SAP SE

- 6.4.13 Oracle Corporation

- 6.4.14 Automatic Data Processing Inc.

- 6.4.15 UKG Inc.

- 6.4.16 Gaea Soft Group Co., Ltd.

- 6.4.17 Xinren Xinshi Technology Co., Ltd.

- 6.4.18 Ant Payslip Technology Co., Ltd.

- 6.4.19 Honghai Cloud Computing Technology Co., Ltd.

- 6.4.20 BenQ Guru Software Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)