|

市場調查報告書

商品編碼

2063849

製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)HCM Software In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

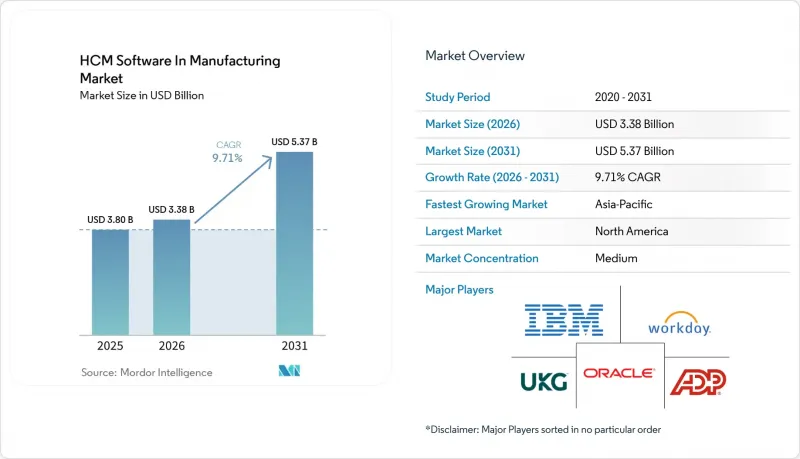

根據 Mordor Intelligence 預測,製造業 HCM 軟體市場將從 2025 年的 30.8 億美元成長到 2026 年的 33.8 億美元,到 2031 年達到 53.7 億美元,2026 年至 2031 年的複合年成長率為 9.71%。

本報告按部署方式(雲端、本地部署、混合部署)、組織規模(中小企業、大型企業)、軟體模組(核心人力資源、人力資源管理等)、製造子產業(汽車、航太與國防、電子與高科技等)以及地區進行細分。市場預測以美元計價。

全球製造業人力資本管理 (HCM) 軟體市場趨勢及洞察

製造業雲優先人力資源轉型

到2025年,雲端採用佔新契約的52%,高於兩年前的38%。製造商表示,季度功能更新(包括監管更新和機器學習增強功能)是關鍵促進因素。混合模式越來越受歡迎,因為它允許薪資核算資料保留在本地,同時將人才管理和分析工作負載遷移到供應商管理的雲端。汽車產業的一級供應商行動最快,他們利用SaaS套件來同步全球各工廠的勞動需求。由於供應商需要開設區域資料中心以符合GDPR法規,歐洲工廠的部署進度有所延遲,但這被視為維持合規性的必要權衡。

引入人工智慧驅動的預測性人才分析

到2025年,38%的主要製造商將投入生產使用預測性離職引擎,從而能夠在員工離職前90天識別出有離職風險的員工。輸入訊號涵蓋從輪班出勤到協作指標等多種因素,而將這些訊號結合起來,已使多家電子工廠的非計劃離職率降低了五分之一以上。隨著積層製造技術的日益普及,航太公司也正在使用類似的模型來檢測技能過時情況,並引導員工進行再培訓,而不是從外部招募。據報導,這些模型帶來的成果包括招募時間縮短高達28%,以及第一年員工留任率的顯著提高。

整合舊有系統面臨的挑戰

到2025年,約有三分之一的規劃系統運作被延後。這是由於客製化中間件成本超出預算高達60%所致。一家使用SAP ECC的汽車工廠在協調其S/4HANA升級與基於雲端的HCM試點實施方面遇到了困難,導致薪資核算出現差異,並面臨因違規罰款的風險。一家食品加工製造商由於受限於其專有的MES系統,不得不手動核對生產和人力資源計劃,導致效率提升的實現延遲了近兩年。目前,提供現成連接器的供應商在現有系統的實施專案中具有明顯的優勢。

細分市場分析

到2025年,本地部署將佔製造業人力資本管理(HCM)軟體市場佔有率的48.23%,成為受資料主權要求約束的工廠的首選。然而,預計到2031年,雲端合約將以10.43%的複合年成長率成長。隨著企業將分析和人才管理功能遷移到雲端,以確保功能持續交付,同時將薪資核算引擎保留在防火牆內,製造業HCM軟體市場正在成長。在汽車產業,61%的一級供應商已經依賴雲端模組來管理連網組裝的員工。航太產業由於多租戶託管通常與出口管制法規相衝突,因此發展滯後,但正在經歷選擇性的遷移。

供應商推出的連接器可將中間件成本降低高達 40%,這加速了混合部署,並實現了與製造執行系統 (MES) 的整合,而此前整合難度極大。儘管食品飲料製造商仍然堅持完全本地部署環境,但 43% 的公司已獲得董事會批准,計劃在 2027 年前分階段過渡到混合部署。台灣和越南電子產業的新工廠已完全繞過傳統壁壘,行動入職使新員工的生產力提高了 22%。決策標準正從總成本轉向合規性、整合準備情況以及對供應商營運基礎設施的接受度。

到2025年,大型企業將佔總收入的63.12%,它們正利用自身規模優勢,協商整合人力資源、薪資、勞動力管理和分析功能的全公司範圍許可套餐。相較之下,由於付費使用制降低了准入門檻,預計到2031年,中小型製造商的複合年成長率將達到11.35%。隨著供應商開始銷售無需購買完整套件的“最佳組合模組”,中小企業的製造人力資本管理(HCM)軟體市場正在蓬勃發展。在印度和印度尼西亞,中型電子公司更青睞每月每位員工費用低於5美元的方案。

擁有遍佈20多個國家、員工超過5萬的大型汽車OEM廠商,優先考慮能夠確保多幣種薪資核算和多語言介面的單一解決方案。然而,即使是一些大型企業集團,也正在將七種工具整合到一到兩個核心平台中,以最大限度地減少整合成本。中小買家則更青睞那些提供本地化語言介面和自助式設定嚮導的供應商,這些嚮導可以將部署時間從九個月縮短到六週。這種日益成長的市場接受度表明,細分市場金字塔底層的市場將持續保持兩位數的成長。

區域分析

預計到2025年,北美地區的營收將佔全球總營收的34.19%,這得益於該地區對雲端運算的早期應用以及勞動力短缺的現狀,後者使得預測性排班成為經營團隊的首要任務。美國的職缺數量已超過60萬個,促使企業採用技能儲備庫,以便職位缺出現前提案橫向流動。一家加拿大汽車零件供應商統一了其遍布北美各地工廠的薪資核算,而一家位於美國中西部的食品製造商則由於其成熟的ERP核心系統而選擇保留其本地部署的系統。

亞太地區預計到2031年將維持11.41%的複合年成長率,主要得益於印度、越南和印尼為擺脫舊有系統束縛而建造的新型智慧工廠。中國的電子產業中心由於受到《個人資料保護法》(PIPL)的限制,要求居住。日本勞動力老化使得在退休高峰到來之前,迫切需要實施知識轉移機制,以收集資深員工的專業知識。

儘管歐洲的普及勢頭強勁,但由於GDPR跨境限制和平台勞動指令導致合規期限延長,轉型速度有所放緩。德國的原始設備製造商(OEM)正將人力資源管理(HCM)系統的升級與向電動車生產的轉型聯繫起來,而法國的食品工廠則在調整工作時間表,以符合《工作時間指令》的休息時間要求。南美洲由於預算限制而進展緩慢,但每人成本低於5美元的模組化SaaS解決方案正在中型出口企業中逐漸獲得認可。在中東,沙烏地阿拉伯和阿拉伯聯合大公國在政府主導的數位產業計畫的推動下加速了普及,但在非洲,普及仍處於起步階段,目前僅在南非和奈及利亞開展了少數試點計畫。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 製造業雲優先人力資源轉型

- 引入人工智慧驅動的預測性人才分析

- 勞動力短缺正在加速數位化人才計畫的實施。

- 多地點生產中合規性的複雜性

- 物聯網整合邊緣運算和HCM平台

- 輪班工作中員工體驗面臨的主要挑戰。

- 市場限制因素

- 整合舊有系統面臨的挑戰

- 資料安全和隱私限制

- 營運層面的變革阻力

- 中型製造業面臨的預算壓力

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 不同的發展

- 雲

- 現場

- 混合

- 按組織規模

- 小型企業

- 大公司

- 透過軟體模組

- 核心人力資源

- 勞動力管理

- 人力資源管理

- 薪資核算

- 分析

- 按子行業分類的製造業

- 車

- 航太/國防

- 電子與高科技

- 食品/飲料

- 其他製造業子部門

- 按地區

- 北美洲

- 南美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Automatic Data Processing Inc.

- Oracle Corporation

- SAP SE

- Workday Inc.

- Ceridian HCM Holding Inc.

- UKG Inc.

- IBM Corporation

- Infor Inc.

- Paycom Software Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Ramco Systems Limited

- Darwinbox Digital Solutions Private Limited

- Zoho Corporation Pvt. Ltd.

- Sage Group plc

- Atoss Software AG

- WorkForce Software LLC

- Ascentis Corporation

- Namely Inc.

- Rippling Technologies Inc.

- SumTotal Systems LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the hCM software in Manufacturing Market is expected to increase from USD 3.08 billion in 2025 to USD 3.38 billion in 2026 and reach USD 5.37 billion by 2031, growing at a CAGR of 9.71% over 2026-2031.

This report is Segmented by Deployment (Cloud, On-Premises, and Hybrid), Organization Size (Small and Medium-Sized Enterprises, and Large Enterprises), Software Module (Core HR, Workforce Management, and More), Manufacturing Sub-Industry (Automotive, Aerospace and Defense, Electronics and High-Tech, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In Manufacturing Market Trends and Insights

Cloud-First Manufacturing HR Transformations

Cloud deployments represented 52% of new contracts in 2025, up from 38% two years earlier. Manufacturers cite quarterly feature drops that embed regulatory updates and machine-learning enhancements as the primary driver. Hybrid models gained favor because they keep payroll data on-site while pushing talent and analytics workloads into vendor-managed clouds. Automotive tier-1 suppliers moved fastest, synchronizing labor requirements across global plants with SaaS suites. European plants faced additional latency after providers opened regional data centers to comply with GDPR rules, yet accepted the trade-off to remain compliant.

AI-Driven Predictive Workforce Analytics Adoption

Predictive attrition engines entered production at 38% of large manufacturers in 2025, flagging at-risk employees 90 days before resignation. Input signals now range from shift attendance to collaboration metrics, which together cut unplanned turnover in several electronics factories by more than one-fifth. Aerospace firms run similar models to spot skill obsolescence as additive manufacturing scales, then trigger retraining paths rather than external hiring. Reported gains include up to 28% shorter time-to-fill and noticeable first-year retention improvements.

Legacy System Integration Challenges

Roughly one-third of scheduled go-lives slipped in 2025 because custom middleware costs outstripped budgets by up to 60%. Automotive plants running SAP ECC struggled to align S/4HANA upgrades with cloud HCM pilots, causing payroll mismatches that risked compliance penalties. Food processors tethered to proprietary MES had to manually reconcile schedules between production and HR, delaying efficiency gains for nearly two years. Vendors shipping pre-built connectors now have a clear edge in brownfield engagements.

Other drivers and restraints analyzed in the detailed report include:

- Labor Shortages Accelerating Digital Workforce Planning

- Compliance Complexity in Multisite Manufacturing

- Data Security and Privacy Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises deployments held 48.23% of the HCM software market share in manufacturing in 2025, standing as the default option for plants bound by data sovereignty mandates. Cloud contracts, however, are projected to climb at a 10.43% CAGR through 2031. The HCM software market in manufacturing is growing as organizations keep payroll engines behind the firewall while shifting analytics and talent to the cloud for continuous feature delivery. In automotive, 61% of tier-1 suppliers already rely on cloud modules to align staffing with interconnected assembly lines. Aerospace lags because multi-tenant hosting often conflicts with export-control regulations, yet selective lift-and-shift moves are underway.

Hybrid uptake accelerated where vendors introduced connectors that cut middleware spend by up to 40%, making previously rigid MES integrations feasible. Food and beverage producers still cling to full-on-premises estates, but 43% now have board approval for a phased hybrid migration by 2027. Electronics greenfield sites in Taiwan and Vietnam bypassed legacy hurdles altogether, recording 22% faster new-hire productivity thanks to mobile onboarding. Decision criteria have shifted from total cost toward regulatory posture, integration readiness, and appetite for vendor-run infrastructure.

Large enterprises captured 63.12% of 2025 revenue, wielding scale to negotiate enterprise-wide license bundles that stitch together HR, payroll, workforce management, and analytics. In contrast, small and medium-sized manufacturers are set to post an 11.35% CAGR to 2031 as pay-as-you-go pricing lowers entry barriers. The HCM software market in manufacturing is growing among SMEs as vendors now sell best-of-breed modules that eliminate the need to purchase full suites. Sub-USD 5-per-employee monthly plans resonate with mid-tier electronics firms in India and Indonesia.

Large automotive OEMs manage headcounts above 50,000 across 20-plus countries and therefore prize single-stack suites that guarantee multi-currency payroll and multilingual interfaces. Yet even some conglomerates are consolidating from seven-point tools to one or two core platforms to curb integration debt. SME buyers gravitate toward providers with vernacular interfaces and self-service setup wizards that slash deployment time from nine months to six weeks. The resulting democratization suggests sustained double-digit growth at the lower end of the segment pyramid.

Geography Analysis

North America accounted for 34.19% of 2025 revenue courtesy of early cloud acceptance and tight labor markets that made predictive scheduling a board-level priority. U.S. vacancy counts crossing 600,000 spurred the adoption of skills inventories that propose lateral moves before roles open. Canadian automotive suppliers unified payroll across continental plants, while midwestern food producers kept systems on-site due to entrenched ERP cores.

Asia-Pacific is forecast to log an 11.41% CAGR through 2031, powered by greenfield smart factories in India, Vietnam, and Indonesia that sidestep legacy lock-in. Chinese electronics hubs faced PIPL constraints and therefore demanded in-country data residency. Japan's aging workforce triggered urgency around knowledge-transfer tooling that captures veteran expertise before retirements peak.

Europe saw healthy volume but slower migration due to GDPR cross-border rules and the Platform Work Directive, which stretched compliance timelines. German OEMs tie HCM upgrades to electric-vehicle production pivots, while French food plants fine-tune rosters to respect the Working Time Directive's rest-period mandates. South America lags due to budget limits, yet modular SaaS at sub-USD 5 per head is breaking through among mid-sized exporters. The Middle East accelerated adoption in Saudi Arabia and the UAE under state digital-industry programs, whereas Africa remains nascent outside South Africa and a handful of Nigerian pilots.

- Automatic Data Processing Inc.

- Oracle Corporation

- SAP SE

- Workday Inc.

- Ceridian HCM Holding Inc.

- UKG Inc.

- IBM Corporation

- Infor Inc.

- Paycom Software Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Ramco Systems Limited

- Darwinbox Digital Solutions Private Limited

- Zoho Corporation Pvt. Ltd.

- Sage Group plc

- Atoss Software AG

- WorkForce Software LLC

- Ascentis Corporation

- Namely Inc.

- Rippling Technologies Inc.

- SumTotal Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Manufacturing HR Transformations

- 4.2.2 AI-Driven Predictive Workforce Analytics Adoption

- 4.2.3 Labor Shortages Accelerating Digital Workforce Planning

- 4.2.4 Compliance Complexity in Multisite Manufacturing

- 4.2.5 Edge Computing and IoT Integration with HCM Platforms

- 4.2.6 Shift-Based Employee Experience Imperatives

- 4.3 Market Restraints

- 4.3.1 Legacy System Integration Challenges

- 4.3.2 Data Security and Privacy Constraints

- 4.3.3 Change Management Resistance on Factory Floors

- 4.3.4 Budgetary Pressures in Mid-Sized Manufacturers

- 4.4 Industry Value -Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium-Sized Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Software Module

- 5.3.1 Core HR

- 5.3.2 Workforce Management

- 5.3.3 Talent Management

- 5.3.4 Payroll

- 5.3.5 Analytics

- 5.4 By Manufacturing Sub-Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and High-Tech

- 5.4.4 Food and Beverage

- 5.4.5 Other Manufacturing Sub-Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia Pacific

- 5.5.5 Middle East

- 5.5.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 Workday Inc.

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 UKG Inc.

- 6.4.7 IBM Corporation

- 6.4.8 Infor Inc.

- 6.4.9 Paycom Software Inc.

- 6.4.10 Cornerstone OnDemand Inc.

- 6.4.11 BambooHR LLC

- 6.4.12 Ramco Systems Limited

- 6.4.13 Darwinbox Digital Solutions Private Limited

- 6.4.14 Zoho Corporation Pvt. Ltd.

- 6.4.15 Sage Group plc

- 6.4.16 Atoss Software AG

- 6.4.17 WorkForce Software LLC

- 6.4.18 Ascentis Corporation

- 6.4.19 Namely Inc.

- 6.4.20 Rippling Technologies Inc.

- 6.4.21 SumTotal Systems LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測