|

市場調查報告書

商品編碼

2063971

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

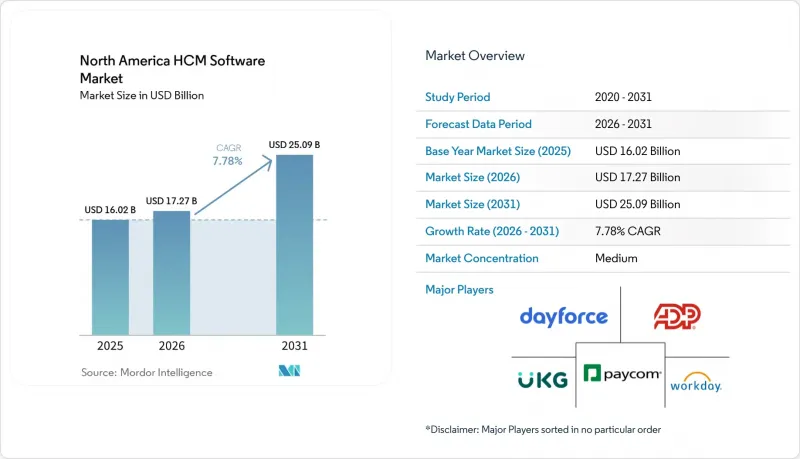

根據 Mordor Intelligence 預測,北美人力資源管理 (HCM) 軟體市場將從 2025 年的 160.2 億美元成長到 2026 年的 172.7 億美元,到 2031 年將達到 250.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 7.78%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理等)、最終用戶產業(IT和電信、銀行、金融服務和保險、製造業等)以及地區進行細分。市場預測以美元計價。

北美HCM軟體市場趨勢及洞察

人力資源系統的雲端遷移

企業持續從本地基礎設施遷移到雲端平台,以利用即時分析、行動自助服務和持續的功能發布。混合雲的採用速度超過了純雲端採用,因為銀行和醫療保健相關企業為了滿足資料居住要求,仍然在私有環境中處理薪資核算。美國的「HR 2.0」計畫正在將220萬私部門員工遷移到共用的雲端服務中心,而加拿大聯邦政府的Dayforce實施計畫則凸顯了將工會薪資規則轉化為標準化工作流程的複雜性。這些引人注目的項目展現了雲端運算的經濟效益,並鼓勵省級和地方政府機構開展類似的舉措。

人工智慧驅動的人才分析的興起

根據美國人力資源管理協會 (SHRM) 2026 年的調查,39% 的企業正在使用人工智慧進行招募和績效管理,這一比例在三年內大幅成長。預測員工離職風險的模型現在可以提前 6-9 個月識別離職風險,技能推理引擎可以突出顯示那些可能被忽略的內部候選人。然而,變革管理至關重要。由於 64% 的第一線員工擔心失業,供應商被迫提高透明度並提供再培訓途徑。 Workday 在 2025 年收購了 Paradox,後者整合了一個無需負責人干預即可安排面試的對話式助手,這表明人工智慧如何在改善候選人體驗的同時,消除低價值的任務。

對資料隱私和網路安全的擔憂

Paychex 和 Workday 近期發生的資料外洩事件,以及 Oracle 發布的 CVE-2024-21287 關鍵補丁,凸顯了集中式員工資料如何吸引網路攻擊者。各州隱私權法賦予員工廣泛的資料存取和刪除權,而墨西哥的《資料保護法》(LFPDPPPP) 則規定,違規者最高可被處以相當於企業營業額 2% 的罰款。因此,企業紛紛推遲雲端遷移,直到供應商能夠證明其具備加密、存取控制和快速事件回應能力。目前,各服務供應商正在發布 SOC 2 報告和零信任藍圖,以重建用戶信任。

細分市場分析

到2025年,軟體將佔據72.86%的市場佔有率,這反映出核心人力資源、薪資和人才管理模組的授權收入佔據主導地位。然而,隨著企業在諸如將HCM平台與傳統ERP系統整合、建立演算法審計追蹤以及培訓管理員使用人工智慧輔助決策工具等領域需要專業知識,預計到2031年,服務業將以8.94%的年均成長率成長。由於企業尋求資料遷移、建立人工智慧管治以及整合傳統ERP系統的支持,業務收益的成長速度超過了軟體收入。實施計畫通常需要12到24個月,涉及跨多個國家統一薪資核算。此外,中小企業也越來越傾向外包薪資核算和福利管理,因此託管服務也越來越受歡迎。

多虧雲端架構,軟體銷售依然強勁,雲端架構支援分層模組購買。供應商透過訂閱模式實現創新獲利,但當出於合規性要求或技能框架等原因需要客製化工作流程時,服務模式則佔據更大的市場佔有率。產品收入和諮詢收入之間的相互作用,凸顯了北美人力資本管理 (HCM) 軟體市場為何能在授權成長放緩的情況下持續擴張。

預計到2025年,雲端採用將佔據63.42%的市場佔有率,這主要得益於初始投資的減少、自動化更新以及本地部署系統無法實現的行動優先員工體驗。然而,混合配置的成長率最高,達到9.21%,因為企業需要在敏捷性與資料儲存和稽核要求之間取得平衡。雖然雲端仍然是人才管理和學習模組的首選,但混合採用正在迅速成長,因為銀行和醫院將敏感的薪資資料保留在私人基礎設施上。這種分離式配置能夠在不違反資料主權規則的前提下實現快速創新。

儘管北美人力資本管理 (HCM) 軟體市場的本地部署比例正在逐漸下降,但國防相關企業和一些加拿大政府機構仍保留獨立環境。中小企業由於成本可預測性而傾向於純雲端部署,而全球企業則選擇混合雲以滿足不同的監管要求,這鞏固了混合雲作為北美 HCM 軟體市場關鍵成長引擎的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人力資源系統的雲端遷移

- 人工智慧驅動的人才分析的興起

- 關於薪資和稅收的合規要求

- 引入基於技能的招募框架

- 用於人力資源工作流程產生的AI輔助工具

- 擴展零工工作者的全面勞動力管理

- 市場限制因素

- 資料隱私和網路安全問題

- 中小企業實施成本高昂

- 算法偏見與人工智慧審計的風險

- 將傳統ERP和HCM系統整合起來的複雜性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 核心人力資源

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday, Inc.

- Ultimate Kronos Group

- Dayforce, Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Namely Inc.

- TriNet Zenefits Inc.

- Gusto, Inc.

- Rippling People Center Inc.

- HiBob Ltd.

- Deel Inc.

- Factorial HR Software SL

- Personio GmbH

- Ramco Systems Limited

- SumTotal Systems LLC

- PeopleStrategy, Inc.

- Lattice, Inc.

- ClearCompany, Inc.

- iSolved HCM LLC

- Zoho Corporation Pvt. Ltd.

- 15Five, Inc.

- TriNet Group, Inc.

- Saba Software LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america hCM software market size is projected to expand from USD 16.02 billion in 2025 to USD 17.27 billion in 2026 and USD 25.09 billion by 2031, registering a CAGR of 7.78% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, and More), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America HCM Software Market Trends and Insights

Cloud Migration of HR Systems

Enterprises continue to replace on-premises infrastructure with cloud platforms to gain real-time analytics, mobile self-service, and continuous feature releases. Hybrid adoption grows faster than pure cloud adoption because banking and healthcare firms keep payroll processing in private environments to meet data residency mandates. The U.S. HR 2.0 program is migrating 2.2 million civilian employees to shared cloud service centers, while Canada's federal rollout of Dayforce confirms the complexity of converting union pay rules to standardized workflows. These marquee projects validate the economics of the cloud and encourage state and provincial agencies to follow suit.

Rise of AI-Driven Talent Analytics

A 2026 SHRM survey showed 39% of organizations using AI for recruiting or performance management, up sharply in three years. Predictive attrition models now flag flight risks six to nine months in advance, and skills-inference engines surface internal candidates who would otherwise stay invisible. Yet change management is critical; 64% of frontline staff fear displacement, forcing vendors to supply transparency and reskilling pathways. Workday's 2025 purchase of Paradox embedded conversational assistants that book interviews without recruiter input, demonstrating how AI can remove low-value tasks while enhancing candidate experience.

Data-Privacy and Cyber-Security Concerns

Recent breaches at Paychex and Workday, plus Oracle's critical CVE-2024-21287 patch, highlight how centralized employee data attracts threat actors. State privacy laws grant workers broad rights to access and delete data, while Mexico's LFPDPPP levies fines up to 2% of revenue. Enterprises, therefore, delay cloud migrations until vendors demonstrate encryption, access controls, and rapid incident response. Providers now publish SOC 2 reports and zero-trust roadmaps to rebuild confidence.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Mandates on Payroll and Tax

- Skills-Based Hiring Framework Adoption

- Algorithmic Bias and AI-Audit Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held a 72.86% share in 2025, reflecting the dominance of licensing revenue from core HR, payroll, and talent management modules, yet services are expanding at 8.94% through 2031 as enterprises require specialized expertise to integrate HCM platforms with legacy ERP systems, configure algorithmic audit trails, and train managers on AI-assisted decision tools. Services revenue is rising faster than software revenue as enterprises seek support for migrating data, configuring AI governance, and integrating legacy ERP systems. Implementation projects often span 12-24 months and involve multi-country payroll harmonization. Managed services adoption is also increasing among small employers that prefer to outsource payroll and benefits administration.

Software sales remain robust because cloud architectures enable incremental module purchases. Vendors monetize innovation through subscription tiers, yet services capture greater wallet share when compliance mandates or skills frameworks require customized workflows. The interplay of product and consulting revenue underscores why the North America HCM software market size continues to expand even as license growth moderates.

Cloud deployments commanded a 63.42% share in 2025, driven by lower upfront capital expenditure, automatic updates, and mobile-first employee experiences that on-premises systems cannot match, yet hybrid configurations are growing fastest at 9.21% as enterprises balance agility with data residency and audit requirements. Cloud remains the primary choice for talent and learning modules, but hybrid deployments grow fastest as banks and hospitals keep sensitive payroll data on private infrastructure. This split configuration allows rapid innovation without breaching data sovereignty rules.

On-premises adoption in the North America HCM software market is gradually shrinking, though defense contractors and some Canadian ministries still maintain standalone environments. Small businesses gravitate toward pure cloud for cost predictability, whereas global enterprises choose hybrid to meet divergent jurisdictional mandates, reinforcing hybrid as the pivotal growth engine in the North America HCM software market.

List of Companies Covered in this Report:

- Workday, Inc.

- Ultimate Kronos Group

- Dayforce, Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Namely Inc.

- TriNet Zenefits Inc.

- Gusto, Inc.

- Rippling People Center Inc.

- HiBob Ltd.

- Deel Inc.

- Factorial HR Software SL

- Personio GmbH

- Ramco Systems Limited

- SumTotal Systems LLC

- PeopleStrategy, Inc.

- Lattice, Inc.

- ClearCompany, Inc.

- iSolved HCM LLC

- Zoho Corporation Pvt. Ltd.

- 15Five, Inc.

- TriNet Group, Inc.

- Saba Software LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud Migration of HR Systems

- 4.2.2 Rise of AI-Driven Talent Analytics

- 4.2.3 Compliance Mandates on Payroll and Tax

- 4.2.4 Skills-Based Hiring Framework Adoption

- 4.2.5 Generative AI Copilots for HR Workflows

- 4.2.6 Expansion of Total Workforce Management for Gig Labor

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cyber-Security Concerns

- 4.3.2 High Implementation Costs for SMEs

- 4.3.3 Algorithmic Bias and AI-Audit Exposure

- 4.3.4 Legacy ERP-HCM Integration Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 Ultimate Kronos Group

- 6.4.3 Dayforce, Inc.

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 BambooHR LLC

- 6.4.9 Namely Inc.

- 6.4.10 TriNet Zenefits Inc.

- 6.4.11 Gusto, Inc.

- 6.4.12 Rippling People Center Inc.

- 6.4.13 HiBob Ltd.

- 6.4.14 Deel Inc.

- 6.4.15 Factorial HR Software SL

- 6.4.16 Personio GmbH

- 6.4.17 Ramco Systems Limited

- 6.4.18 SumTotal Systems LLC

- 6.4.19 PeopleStrategy, Inc.

- 6.4.20 Lattice, Inc.

- 6.4.21 ClearCompany, Inc.

- 6.4.22 iSolved HCM LLC

- 6.4.23 Zoho Corporation Pvt. Ltd.

- 6.4.24 15Five, Inc.

- 6.4.25 TriNet Group, Inc.

- 6.4.26 Saba Software LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測