|

市場調查報告書

商品編碼

2063976

日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Japan HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

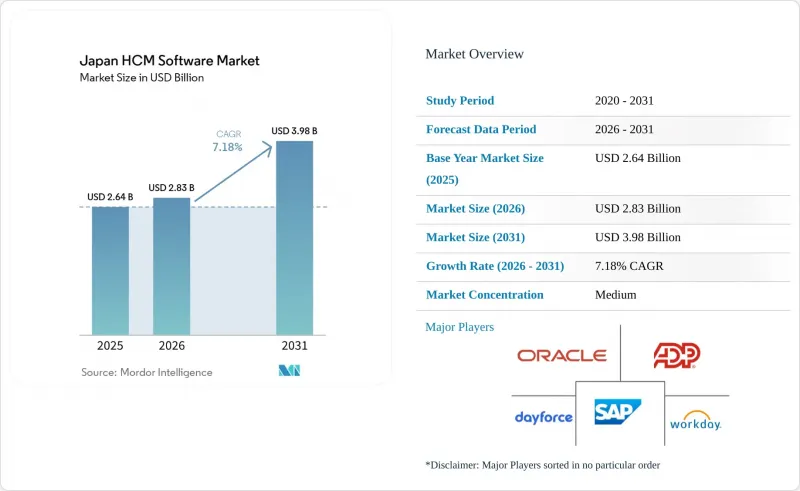

根據 Mordor Intelligence 預測,日本 HCM 軟體市場規模將從 2025 年的 26.4 億美元成長到 2026 年的 28.3 億美元,到 2031 年將達到 39.8 億美元,2026 年至 2031 年的複合年成長率為 7.18%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理、人力資源管理、薪資管理等)以及最終用戶產業(IT和電信、銀行、金融服務和保險等)進行細分。市場預測以美元計價。

日本HCM軟體市場的趨勢與洞察

日本企業的數位轉型舉措

2025年公佈的稅收優惠政策鼓勵企業將人力資源系統視為產生收入資產,而非僅僅是後勤部門工具。曾經經營數十個獨立人力資源資料庫的大型企業集團正在整合為整合套件,以實現即時分析並縮短入職週期。 2025年,三井物產為其4萬名員工部署了Oracle Fusion Cloud HCM,整合了薪資、考勤和人才管理模組,從而消除了地理分散的系統,並實現了即時勞動力分析。製造業、廣告業和化工業等大型企業集團多年來持續採用雲端技術,顯示企業正在從客製化的本地部署轉向標準化、可升級的平台。這些項目的投資回報擴大以勞動力靈活性來衡量,企業指出,快速重新部署技能型員工隊伍直接有助於獲得新業務。

中小企業擴大採用基於雲端的人力資源解決方案。

高達首年訂閱費四分之三的補助降低了以往依賴電子表格的企業的進入門檻。免費增值模式、兩週內即可部署的模板以及應用商店整合縮短了銷售週期,使供應商能夠將眾多微企業轉化為穩定的收入來源。與薪資核算和考勤管理專家的互通性協議消除了重複資料輸入,使基於雲端的人力資本管理 (HCM) 成為 IT負責人有限的企業主的低風險升級選擇。目標中小企業群體依然龐大,而那些已建立自動化入駐流程的供應商預計將在未來的成長中佔據主導市場佔有率。

傳統產業中對資料儲存位置和安全性的擔憂

日益嚴格的跨境資料監管迫使銀行、醫院和政府機構將人事記錄保存在國內。雖然主權雲端和專用區域現已存在,但基於政府安全計畫的有限供應商認證正在縮小產品選擇範圍並延長採購週期。將薪資核算和相關功能分開的混合模式是一種權宜之計,但許多現有客戶仍然預設選擇本地部署,這減緩了雲端的全面普及。

細分市場分析

到2025年,軟體將佔日本人力資本管理(HCM)市場收入的74.12%,反映出核心人力資源、薪資和考勤管理模組的授權和訂閱費用佔據市場主導地位。然而,預計2026年至2031年,服務領域的複合年成長率將達到8.26%。 Works Human Intelligence透過在其核心套件中整合季度規則更新和薪資核算管理功能,凸顯了這一轉變,從而確保了營運層面的獲利能力。

對業務流程外包 (BPO) 的需求進一步推動了服務的使用。 JOE 和 SmartHR 共同推出的薪資核算和考勤管理服務,將雲端軟體與經過認證的 BPO 人員結合,吸引了那些希望轉移合規風險的客戶。因此,隨著供應商將獲利模式從一次性許可轉向持續管理服務,日本人力資本管理 (HCM) 軟體市場的服務規模預計將穩步擴大。

到 2025 年,雲端採用率將佔市場佔有率的 65.38%,這主要得益於中小企業的採用以及多租戶 SaaS 的成本優勢。然而,隨著大型企業和受監管行業在不犧牲可擴展性的前提下要求數據駐留,混合模式預計將在 2031 年前以 8.74% 的複合年成長率成長,成為所有採用模式中成長最快的。 OracleOracle擴展的專用區域將使客戶能夠在自己的防火牆內運行全端 OCI 服務,同時與公共雲端模組同步,所有這些都旨在符合嚴格的資料主權規則。

儘管本地部署的市場佔有率正在下降,但在重工業和公共部門仍然保持強勁勢頭,因為這些領域優先考慮的是空氣間隙的安全性和高度客製化。然而,新的部署正在轉向混合部署,即敏感的薪資資料儲存在本地,而學習和互動工具則位於異地。就絕對收入而言,雲端仍然佔據最大佔有率,但隨著大型企業為關鍵業務工作負載採用混合配置,其佔有率正在逐漸下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 日本企業在數位轉型所做的努力

- 中小企業對雲端的人力資源解決方案的採用率不斷提高。

- 政府關於工作方式改革和遵守勞動法的指南

- 勞動力老化推動了對策略性人力資源規劃工具的需求。

- 將人工智慧和分析技術融入人力資源流程:提升價值提案

- 不斷發展的零工經濟需要一個靈活的人才管理平台。

- 市場限制因素

- 傳統產業中對資料儲存位置和安全性的擔憂

- 人力資源技術領域缺乏負責實施和維護的熟練人員。

- 大型企業本地部署客製化解決方案的初始成本較高

- 保守的企業文化中對組織變革的抵制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 核心人力資源

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday Inc.

- Oracle Corporation

- SAP SE

- ADP, Inc.

- Dayforce, Inc.

- UKG Inc.

- Cornerstone OnDemand, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- BambooHR LLC

- Zoho Corporation Private Limited

- PeopleStrong Technologies Private Limited

- Rippling People Center Inc.

- Infor, Inc.

- SmartHR, Inc.

- freee KK

- OBIC Business Consultants Co., Ltd.

- Works Human Intelligence Co., Ltd.

- NEC Corporation

- Fujitsu Limited

- CYDAS Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan hCM software market size is expected to increase from USD 2.64 billion in 2025 to USD 2.83 billion in 2026 and reach USD 3.98 billion by 2031, growing at a CAGR of 7.18% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan HCM Software Market Trends and Insights

Digital Transformation Initiatives Across Japanese Enterprises

Tax incentives unveiled in 2025 are nudging enterprises to treat HR systems as revenue-enabling assets rather than back-office utilities. Large conglomerates that once ran dozens of standalone HR databases are consolidating onto unified suites to unlock real-time analytics and reduce onboarding cycle time. Mitsui and Co. deployed Oracle Fusion Cloud HCM across 40,000 employees in 2025, integrating payroll, time, and talent modules to eliminate fragmented regional systems and enable real-time workforce analytics. Multi-year cloud rollouts by conglomerates in manufacturing, advertising, and chemicals demonstrate a shift from bespoke on-premise builds toward standardized, upgradeable platforms. The return on these projects is increasingly quantified in terms of workforce agility, with firms citing faster redeployment of skilled labor as a direct contributor to new-business wins.

Rising Adoption of Cloud-Based HR Solutions by SMEs

Subsidies covering up to three-quarters of first-year subscription fees have lowered entry barriers for firms that historically relied on spreadsheets. Freemium pricing, two-week implementation templates, and app-store connectors are shortening sales cycles and allowing vendors to convert large pools of micro-enterprises into recurring-revenue accounts. Interoperability pacts between payroll and attendance specialists eliminate duplicate data entry, positioning cloud HCM as a low-risk upgrade for owners with limited IT staff. The addressable SME base remains vast, and vendors that master automated onboarding are poised to collect outsized share of future growth.

Data Residency and Security Concerns Among Traditional Industries

More stringent cross-border data rules are compelling banks, hospitals, and ministries to retain personnel records within national borders. Although sovereign clouds and dedicated regions now exist, limited vendor certification under government security programs constrains product choice and lengthens procurement cycles. Hybrid models that split payroll from ancillary functions offer a workaround, yet many legacy buyers still default to on-premise installations, slowing full cloud penetration.

Other drivers and restraints analyzed in the detailed report include:

- Government Mandate on Work Style Reform and Labor Law Compliance

- Aging Workforce Driving Demand for Strategic Workforce Planning Tools

- Shortage of HR Tech Skilled Professionals for Implementation and Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software commanded 74.12% of Japan's HCM market revenue in 2025, reflecting the dominance of license and subscription fees for core HR, payroll, and time-and-attendance modules. However, Services are forecast to grow at 8.26% CAGR during 2026-2031. Works Human Intelligence highlights the shift by packaging quarterly rule updates and managed payroll with its core suite, capturing margin in the operational layer.

Demand for business-process outsourcing further elevates service intake. A joint payroll-and-attendance offering from JOE and SmartHR bundles cloud software with certified BPO labor, attracting clients who prefer to transfer compliance risk. The Japan HCM Software market size captured by services is therefore expected to climb steadily as vendors monetize ongoing administration rather than one-time licenses.

Cloud deployment held 65.38% market share in 2025, driven by SME adoption and the cost advantages of multi-tenant SaaS. Yet Hybrid models are expanding at 8.74% CAGR through 2031, the fastest rate among deployment modes, as large enterprises and regulated industries demand data residency without sacrificing scalability. Oracle's dedicated-region expansion lets clients run full-stack OCI services behind their own firewalls while synchronizing with public-cloud modules, a design tailored to stringent data-sovereignty rules.

On-Premises deployments, though declining in share, persist among heavy manufacturers and public-sector entities that prioritize air-gapped security and customization depth, but new adoption tilts toward hybrid deployments that keep sensitive payroll data locally and push learning or engagement tools offsite. Cloud will remain the largest slice by absolute revenue, yet its share inches down as large enterprises retrofit hybrid blueprints for mission-critical workloads.

List of Companies Covered in this Report:

- Workday Inc.

- Oracle Corporation

- SAP SE

- ADP, Inc.

- Dayforce, Inc.

- UKG Inc.

- Cornerstone OnDemand, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- BambooHR LLC

- Zoho Corporation Private Limited

- PeopleStrong Technologies Private Limited

- Rippling People Center Inc.

- Infor, Inc.

- SmartHR, Inc.

- freee K.K.

- OBIC Business Consultants Co., Ltd.

- Works Human Intelligence Co., Ltd.

- NEC Corporation

- Fujitsu Limited

- CYDAS Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital Transformation Initiatives Across Japanese Enterprises

- 4.2.2 Rising Adoption of Cloud-Based HR Solutions by SMEs

- 4.2.3 Government Mandate on Work Style Reform and Labor Law Compliance

- 4.2.4 Aging Workforce Driving Demand for Strategic Workforce Planning Tools

- 4.2.5 Integration of AI and Analytics in HR Processes Enhancing Value Proposition

- 4.2.6 Growing Gig Economy Necessitating Flexible Talent Management Platforms

- 4.3 Market Restraints

- 4.3.1 Data Residency and Security Concerns Among Traditional Industries

- 4.3.2 Shortage of HR Tech Skilled Professionals for Implementation and Maintenance

- 4.3.3 High Upfront Costs for On-Premise Custom Solutions for Large Enterprises

- 4.3.4 Resistance to Organisational Change in Conservative Corporate Culture

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 ADP, Inc.

- 6.4.5 Dayforce, Inc.

- 6.4.6 UKG Inc.

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Paycom Software, Inc.

- 6.4.9 Paylocity Holding Corporation

- 6.4.10 BambooHR LLC

- 6.4.11 Zoho Corporation Private Limited

- 6.4.12 PeopleStrong Technologies Private Limited

- 6.4.13 Rippling People Center Inc.

- 6.4.14 Infor, Inc.

- 6.4.15 SmartHR, Inc.

- 6.4.16 freee K.K.

- 6.4.17 OBIC Business Consultants Co., Ltd.

- 6.4.18 Works Human Intelligence Co., Ltd.

- 6.4.19 NEC Corporation

- 6.4.20 Fujitsu Limited

- 6.4.21 CYDAS Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測