|

市場調查報告書

商品編碼

2063974

印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)India HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

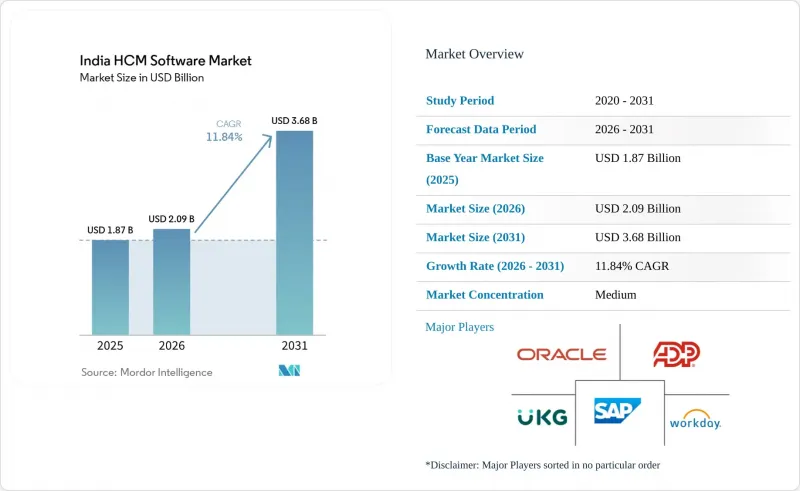

根據 Mordor Intelligence 預測,印度 HCM 軟體市場將從 2025 年的 18.7 億美元成長到 2026 年的 20.9 億美元,到 2031 年達到 36.8 億美元,2026 年至 2031 年的複合年成長率為 11.84%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理、人力資源管理、薪資管理等)以及最終用戶產業(IT和電信、銀行、金融服務和保險等)進行細分。市場預測以美元計價。

印度HCM軟體市場的趨勢與洞察

快速採用基於雲端的HCM平台

雲端運算在印度人力資本管理 (HCM) 軟體市場已佔據 62.91% 的佔有率,並以 13.54% 的複合年成長率 (CAGR) 持續成長,這主要得益於按員工收費模式消除了硬體成本。 Workday 位於清奈的 AWS 託管資料中心為跨國客戶提供獨立資料存儲,同時維護單一的全球實例。 Oracle HCM Now 將核心人力資源、薪資核算和考勤管理整合到單一雲端平台中,Wipro 在遷移後將其薪資核算週期縮短了 60%。本土挑戰者 Keka 每月處理 150 萬筆薪資核算,其地理圍籬功能和區域語言支援深受第一線員工歡迎。本地客製化預算的減少推動了與 EPFO 和 ESIC 等入口網站進行 API 整合的支出增加,進一步加速了雲端運算的發展動能。

對自動化和人工智慧主導的人力資源流程的需求日益成長

這套人才管理套件整合了履歷分析、面試安排和離職預測等功能,可將招募時間縮短30%。 2025年12月,SAP SuccessFactors整合了GP的Gia智慧代理,使客戶能夠在單一螢幕上交叉引用來自50個國家的薪資資料。根據ADP的《醫療產業趨勢報告》,84%的醫療保健機構期望人工智慧能夠減少行政工作,而65%的機構則在技能發展方面面臨挑戰。 Hunar.AI已透過WhatsApp和語音機器人與1000萬求職者建立了聯繫,有效應對了銀行業103%的離職率。目前,市場呈現兩極化:大型企業採用預測分析,而中小企業則選擇使用聊天機器人來自動化處理請假和換班申請。

對資料隱私和網路安全的擔憂

《個人資料保護法》規定,資料外洩事件必須在72小時內揭露,稽核日誌必須保留一年,違規者將面臨巨額罰款,這導致漫長的法律審查和採購週期延長。儘管Workday於2025年12月在印度開設了資料中心以滿足本地化需求,但如今,沒有ISO 27001或SOC 2認證的供應商通常會被排除在企業候選名單之外。由於員工檔案中包含財務和醫療數據,銀行、金融和保險(BFSI)以及醫療保健行業的採購人員正在進行更嚴格的滲透測試。因此,對於價格敏感的中小企業而言,不採用雙因素認證的折扣平台或許可以接受,但它們很少能進入嚴格監管的行業。

細分市場分析

業務收益正以13.12%的複合年成長率成長,預計隨著企業將法規要求映射和API整合外包,其在印度人力資本管理(HCM)軟體市場的佔有率將進一步擴大。儘管預計到2025年,軟體收入將保持70.84%的市場佔有率(主要來自許可和訂閱收入),但業務收益佔有率的成長表明,供應商正透過售後價值交付實現盈利,而不僅僅依賴基於用戶的定價。 Oracle與Wipro的案例研究表明,遷移到雲端後,薪資核算週期縮短了60%,這需要六個月的實施階段,期間需要專門的顧問來映射各州的稅收法規並整合印度僱員公積金組織(EPFO)的臉部認證API。

國內廠商也正在效法這種做法。例如,greytHR的售後團隊會事後處理勞動法的變更,而Keka則將新進員工入職支援納入其訂閱計畫。從策略角度來看,擁有強大的合作夥伴生態系統和認證顧問的廠商在中型和大型企業市場佔據了主導地位,而僅提供軟體授權的廠商則僅限於自助式中小企業市場。

預計到2025年,雲端採用率將達到62.91%,並以13.54%的複合年成長率成長至2031年。同時,混合部署模式正在興起,尤其是在敏感的薪資資料需要儲存在本地,而人才管理模組需要在雲端運作下。 Workday的本地資料中心支援全球實例和獨立儲存的共存。另一方面,Oracle HCM Now透過整合堆疊顯著減少了本地客製化。儘管本地部署的市場佔有率正在下降,但在政府和公共部門機構中仍然存在,因為在這些機構的採購規則中,資本支出優先於營運成本;此外,在那些傳統ERP系統尚無明確雲端遷移路徑的組織中,本地部署仍然佔據一席之地。

對於在多個州運作且需要集中式合規管理的中型製造商而言,一種將本地核心人力資源功能與基於雲端的人才招聘和勞動力分析相結合的混合架構正在成為一種折衷方案,而輪班排班工具又需要分散式管理。網路連接不穩定的製造商正在利用邊緣設備來追溯同步考勤數據,這表明混合架構並非一種固定的架構教條,而是一種將實際運營情況與合規法規相適應的策略。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於雲端的HCM平台快速普及

- 對自動化和人工智慧驅動的人力資源流程的需求日益成長。

- 監理合規的複雜性

- 中小企業數位化程度的提高和SaaS價格的下降。

- 人力資本管理與政府數位入口網站的整合

- 支援本地語言的行動人力資源應用程式在零工經濟從業者中的興起

- 市場限制因素

- 資料隱私和網路安全問題

- 全套人力資本管理系統總擁有成本高

- 各州勞動法規存在差異

- 人力資源分析人才短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 核心人力資源

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Oracle Corporation

- SAP SE

- Workday Inc.

- ADP, Inc.

- UKG Inc.

- Spine Technologies India Private Limited

- Cornerstone OnDemand Inc.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Darwinbox Digital Solutions Private Limited

- ZingHR Techno India Private Limited

- Greytip Software Private Limited

- Keka Technologies Private Limited

- PeopleStrong Technologies Private Limited

- Freshworks Inc.

- Paycom Software, Inc.

- The Sage Group plc

- Rippling Technologies, Inc.

- HiBob Ltd.

- Eightfold AI, Inc.

- Spine Technologies India Private Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the india hCM software market size is expected to increase from USD 1.87 billion in 2025 to USD 2.09 billion in 2026 and reach USD 3.68 billion by 2031, growing at a CAGR of 11.84% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

India HCM Software Market Trends and Insights

Rapid Adoption of Cloud-Based HCM Platforms

Cloud deployment already holds a 62.91% foothold in the India HCM software market and is on a 13.54% CAGR path because pay-per-employee pricing eliminates hardware outlays. Workday's AWS-hosted data center in Chennai gives multinational clients sovereign data storage while keeping a single global instance. Oracle HCM Now bundles core HR, payroll, and time tracking on one cloud stack, and Wipro cut payroll-cycle time by 60% after migration. Domestic challenger Keka processes 1.5 million payrolls each month with geo-fencing and regional-language screens that resonate with field workers. Falling budgets for on-premises customization push spending toward API ties with portals such as EPFO and ESIC, reinforcing cloud momentum.

Growing Demand for Automation and AI-Driven HR Processes

Talent management suites are embedding resume parsing, interview scheduling, and attrition prediction that shorten time-to-hire by 30%. SAP SuccessFactors stitched in G-P's Gia agent in December 2025 so clients can reconcile payroll across 50 countries in one view. ADP's healthcare trends report shows 84% of providers expect AI to relieve paperwork, even as 65% struggle with upskilling. Hunar.AI engaged 10 million candidates through WhatsApp and voice bots to tackle 103% attrition in frontline banking roles. The market now splits between enterprises adopting predictive analytics and SMEs opting for chatbots that automate leave requests and roster swaps.

Data Privacy and Cybersecurity Concerns

The Personal Data Protection Act sets 72-hour breach disclosure, one-year audit logs, and hefty penalties, stretching legal reviews and lengthening procurement cycles. Workday opened an India data center in December 2025 to satisfy localization demands, but vendors lacking ISO 27001 or SOC 2 attestations are now routinely cut from enterprise shortlists. BFSI and healthcare buyers conduct more in-depth penetration tests because employee files contain financial and medical data. As a result, discount platforms that skip two-factor logins may win price-sensitive SMEs but rarely break into regulated verticals.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Regulatory Compliance Complexity

- Expanding SME Digitization and SaaS Affordability

- High Total Cost of Ownership for Full-Suite HCM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is growing at a 13.12% CAGR and will account for a growing share of the India HCM software market as enterprises outsource statutory mapping and API integration. Software retained a 70.84% share in 2025, anchored by license and subscription revenue, yet the rising share of services revenue signals that vendors are monetizing post-sale value delivery rather than relying solely on per-seat pricing. Oracle's Wipro case study, where payroll cycle time fell by 60% after cloud migration, required a 6-month implementation phase with dedicated consultants to map state-specific professional tax rules and integrate EPFO facial-authentication APIs.

Domestic vendors copy this playbook. greytHR's post-sale team retrofits labor-code updates, and Keka bundles onboarding support into subscription tiers. The strategic implication is that vendors with robust partner ecosystems and certified consultants are capturing a disproportionate share of mid-market and enterprise deals, while those offering software-only licenses are confined to self-service SME segments.

Cloud deployments commanded a 62.91% share in 2025 and are forecast to grow at a 13.54% CAGR through 2031, while hybrid rollouts are gaining ground when sensitive payroll data must reside on-prem, while talent modules run in the cloud. Workday's local data center lets global instances coexist with sovereign storage, while Oracle HCM Now removes many on-prem customizations through an integrated stack. On-premises deployments, though declining in share, persist in government and public-sector organizations where procurement rules favor capital expenditure over operating expenditure and where legacy ERP systems lack cloud-migration pathways.

Hybrid architectures, which combine on-premises core HR with cloud-based talent acquisition and workforce analytics, are emerging as a compromise for mid-market manufacturers that operate in multiple states and need centralized compliance engines but decentralized shift-scheduling tools. Manufacturers with patchy connectivity use edge devices that sync attendance data later, proving that hybrid is less about architecture dogma and more about matching site realities with compliance rules.

List of Companies Covered in this Report:

- Oracle Corporation

- SAP SE

- Workday Inc.

- ADP, Inc.

- UKG Inc.

- Spine Technologies India Private Limited

- Cornerstone OnDemand Inc.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Darwinbox Digital Solutions Private Limited

- ZingHR Techno India Private Limited

- Greytip Software Private Limited

- Keka Technologies Private Limited

- PeopleStrong Technologies Private Limited

- Freshworks Inc.

- Paycom Software, Inc.

- The Sage Group plc

- Rippling Technologies, Inc.

- HiBob Ltd.

- Eightfold AI, Inc.

- Spine Technologies India Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Cloud-Based HCM Platforms

- 4.2.2 Growing Demand for Automation and AI-Driven HR Processes

- 4.2.3 Increasing Regulatory Compliance Complexity

- 4.2.4 Expanding SME Digitization and SaaS Affordability

- 4.2.5 Integration of HCM with Government Digital Portals

- 4.2.6 Rise of Vernacular Mobile HR Apps for Gig Workforce

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Concerns

- 4.3.2 High Total Cost of Ownership for Full-Suite HCM

- 4.3.3 Fragmented State-Level Labour Regulations

- 4.3.4 Shortage of HR Analytics Talent

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE

- 6.4.3 Workday Inc.

- 6.4.4 ADP, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Spine Technologies India Private Limited

- 6.4.7 Cornerstone OnDemand Inc.

- 6.4.8 Zoho Corporation Pvt. Ltd.

- 6.4.9 Ramco Systems Limited

- 6.4.10 Darwinbox Digital Solutions Private Limited

- 6.4.11 ZingHR Techno India Private Limited

- 6.4.12 Greytip Software Private Limited

- 6.4.13 Keka Technologies Private Limited

- 6.4.14 PeopleStrong Technologies Private Limited

- 6.4.15 Freshworks Inc.

- 6.4.16 Paycom Software, Inc.

- 6.4.17 The Sage Group plc

- 6.4.18 Rippling Technologies, Inc.

- 6.4.19 HiBob Ltd.

- 6.4.20 Eightfold AI, Inc.

- 6.4.21 Spine Technologies India Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測