|

市場調查報告書

商品編碼

2063856

政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)HCM Software In Government And Public Sector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

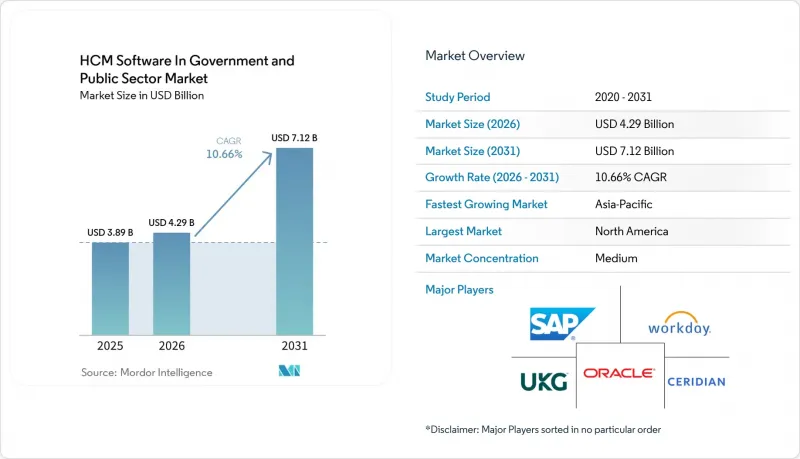

根據 Mordor Intelligence 預測,政府和公共部門的 HCM 軟體市場規模預計將從 2025 年的 38.9 億美元成長到 2026 年的 42.9 億美元,到 2031 年將達到 71.2 億美元。

預計 2026 年至 2031 年的複合年成長率為 10.66%。

本報告按組件(核心人力資源軟體、薪資和薪酬管理、人才管理、勞動力管理等)、部署模式(本地部署、雲端部署、混合部署)、政府機構規模(大型、中型、小型)、最終用戶類型(聯邦政府、州和地方政府、國防和情報機構等)以及地區進行細分。市場預測以美元計價。

政府和公共部門人力資本管理軟體的市場趨勢和洞察

加速公共部門人力資源現代化「雲端優先」模式的實施

美國、英國、澳洲和印度的資訊長(CIO) 現在不僅將雲端遷移視為節省成本的選擇,更將其視為預算義務。美國聯邦政府的「HR 2.0」指令要求各機構在 2030 年前將 190 個傳統人力資源系統整合到共用的雲端服務中,否則將面臨預算削減的風險。英國的「Matrix」、「Synergy」和「Unity」計畫中也包含類似的現代化目標,要求各機構在 2028 年前將 70% 的人力資源交易遷移到雲端。澳洲已撥款 1.8 億澳元(約 1.2 億美元),計劃在 2030 年前為 15,000 名員工提供雲端分析技能培訓,並將資金與實施里程碑掛鉤。印度的 e-HRMS 2.0 在三年內擴展到 500 萬名員工,這表明聯邦設計可以在應用中央標準的同時尊重各州的自主權。這些發展將評估週期縮短至 12 個月,有利於擁有預先已通過核准環境的供應商,並加快了政府和公共部門採用 HCM 軟體的步伐。

強制遵守 FedRAMP、GDPR 和零信任安全框架。

安全框架是至關重要的安全隔離網閘。目前僅有6%的HCM供應商獲得了FedRAMP認證,該認證耗時12-18個月,費用高達200萬美元。早期獲得認證的公司正專注於滿足美國聯邦政府的要求。歐洲的《人工智慧法案》將人力資源軟體列為高風險產品,並增加了強制性的合規性評估,這可能會使專案前置作業時間延長至多一年。美國國防部的「零信任藍圖」正在推動持續認證,這意味著基於會話的架構合格認證要求。早期獲得認證的供應商(例如2019年獲得認證的Workday、2024年獲得認證的SAP SuccessFactors以及2025年獲得認證的Oracle HCM Cloud)比競爭對手擁有18-24個月的前置作業時間,這進一步加劇了政府和公共部門HCM軟體市場的競爭格局。

公共採購週期過長和預算審核延誤

採購週期延長和預算核准流程分散持續限制公共部門機構採用人力資本管理(HCM)系統。由於涉及多個部門的資金依賴,美國國稅局(IRS)2025會計年度的人力資源管理系統競標在14個月後仍未決出結果。北卡羅來納州Workday系統的全州推廣也因災害復原預算重新分配而被推遲。雖然像NASPO ValuePoint這樣的聯合採購框架有助於加快合約簽署,但各個機構採用這些框架的比例仍然有限。這些結構性延誤對年度成長率造成了一定壓力,但並未改變政府和公共部門HCM軟體市場的長期現代化發展軌跡。

細分市場分析

到2025年,薪資和福利產業將佔總收入的28.32%,反映出該產業與財政部支付網路的深度整合,以及與薪資相關的違規風險。主要機構依賴與美國自動化標準支付應用系統(USASAP)等系統的認證介面,這使得薪酬模組在政府和公共部門人力資本管理(HCM)軟體市場中佔據核心地位。對工資扣押和退休金扣除的持續監管帶來了切實的財務課責,這也解釋了薪資核算行業佔據如此高佔有率的原因。

同時,學習與發展領域正以13.42%的複合年成長率快速成長,公共部門管理者正將重心從一次性入門培訓轉向持續技能發展。在印度,Karmayogi iGOT平台透過將微證書整合到績效評估中,使課程完成率提高了一倍以上。在澳大利亞,人工智慧推薦的奈米學位正與人才規劃相結合,以主動預防技能缺口。這顯示人力資本管理(HCM)軟體市場正在發生策略轉變,其目標客戶群正轉向政府和公共部門更廣泛的支出領域。

2025年,本地部署環境仍佔支出的56.19%。這是因為國防和情報機構必須隔離處理敏感資料的系統。國防資訊系統局(DISA)將絕密文件限制在政府所有的資料中心內,這減緩了雲端技術的普及,並增加了對安全、政府控制的基礎設施的依賴。儘管如此,私營機構仍在穩步採用雲端訂閱,以實現更快的升級和更靈活的計量型預算,而混合模式則在主權和敏捷性之間取得平衡,從而擴大了人力資本管理(HCM)軟體在兩種部署模式下的應用範圍。

然而,隨著公共機構追求更快的升級和付費使用制的預算模式,雲端訂閱正以 12.81% 的複合年成長率成長。混合模式將核心記錄保留在本地,同時將分析處理遷移到雲端,既滿足了主權要求,又不犧牲靈活性,並且正在擴大政府和公共部門的人力資本管理軟體市場。

區域分析

北美在政府和公共部門人力資本管理 (HCM) 軟體市場佔據主導地位,預計到 2025 年將佔 45.12% 的市場佔有率,但隨著較簡單的工作負載率先遷移,市場成熟度日益凸顯。僅聯邦政府的 HR 2.0 市場就價值 12 億美元,但 40% 的傳統應用程式因保密限制而無法正常使用。 Workday 在亞利桑那州、喬治亞、佛蒙特州和猶他州的全州部署表明,共用協議如何加速華盛頓特區以外的普及。加拿大各省目前正將重點從部署轉向完善分析能力。網路安全和基礎設施安全局 (CISA) 的零信任最後期限確保了不合規套件的更新換代。

歐洲的成長歸功於英國耗資8億英鎊(10.1億美元)的「Matrix」框架、德國的《數位化入職法案》以及法國全國各地的人力資源資訊系統(SIRH)現代化改造。西班牙的GEISER平台在完成核心數位化改造後展現出附加價值,透過引入聊天機器人,幫助台諮詢量減少了35%。歐盟的《人工智慧法案》延長了前置作業時間,並設置了合規壁壘,阻礙了資金有限的新進入者,從而鞏固了現有供應商在政府和公共部門人力資本管理(HCM)軟體市場的佔有率。

亞太地區是成長最快的區域,預計到2031年將達到10.11%的複合年成長率。印度的國家級電子人力資源管理系統2.0(e-HRMS 2.0)和邦級Maha-AASTHA舉措每年新增數百萬用戶。澳洲正投資1.8億澳元(1.2億美元)提升勞動力分析技能,紐西蘭則透過引入共用服務,在35個機構中實現薪資核算的標準化。越南和印尼的網路主權法規雖然減緩了跨境託管的速度,但卻創造了對國內資料中心的新需求,從而提振了該地區政府和公共部門人力資本管理(HCM)軟體市場的前景。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速推動公共部門人力資源部門現代化進程中的「雲端優先」政策

- 強制遵守 FedRAMP、GDPR 和零信任安全框架。

- 人工智慧驅動的人才分析:提升任務績效與預算效率

- 利用生成式人工智慧副駕駛實現人員調動申請(PAR)的自動化。

- 整合統一的薪資系統和財務支付系統

- 傳統大型主機人力資源資訊系統退役獎勵獎勵津貼

- 市場限制因素

- 加強網路主權法規,限制跨境資料流動。

- 公共採購週期越來越長,預算執行也延誤。

- 政府資訊科技部門在實施大規模人力資本管理轉型方面存在技能缺口

- 新人工智慧法規下的演算法偏見檢驗

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 核心人力資源軟體

- 薪資/報酬

- 人才管理

- 勞動力管理

- 學習與發展

- 部署模式

- 現場

- 雲

- 混合

- 按政府機構規模分類

- 大型政府機構(擁有10,000名或以上員工)

- 中型政府機構(員工人數 1,000 至 10,000 人)

- 小規模政府機構(1000名員工)

- 最終用戶

- 聯邦和中央政府機構

- 州/地方政府

- 國防和情報機構

- 公立教育機構和大學

- 公共安全/司法部門

- 醫療和社會福利機構

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday, Inc.

- Oracle Corporation

- SAP SE

- UKG Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- Infor, Inc.

- Tyler Technologies, Inc.

- NEOGOV, Inc.

- Unit4 NV

- BambooHR LLC

- PeopleFluent(Learning Technologies Group plc)

- Ramco Systems Limited

- Paycor HCM, Inc.

- Gusto, Inc.

- The Sage Group plc

- SumTotal Systems, LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the HCM software in the Government and Public Sector Market is expected to increase from USD 3.89 billion in 2025 to USD 4.29 billion in 2026, and reach USD 7.12 billion by 2031, growing at a CAGR of 10.66% over 2026-2031.

This report is Segmented by Component (Core HR Software, Payroll and Compensation, Talent Management, Workforce Management, and More), Deployment Mode (On-Premises, Cloud, and Hybrid), Agency Size Tier (Large, Medium, and Small), End-User Type (Federal, State and Local, Defense and Intelligence, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HCM Software In Government And Public Sector Market Trends and Insights

Accelerating Cloud-First Mandates In Public Sector HR Modernization

Chief information officers across the United States, the United Kingdom, Australia, and India now treat cloud migration as a budget-binding obligation rather than a cost-saving option. The United States Federal HR 2.0 directive requires agencies to rationalize 190 legacy personnel systems onto shared cloud services by 2030, and failure to comply risks appropriation cuts. Similar modernization quotas embedded in the United Kingdom's Matrix, Synergy, and Unity programs require departments to move 70% of HR transactions to the cloud by 2028. Australia budgeted AUD 180 million (USD 120 million) to upskill 15,000 workers in cloud analytics by 2030, linking funding to adoption milestones. India's e-HRMS 2.0 scaled to five million employees within three years, proving that federated designs can respect state autonomy while enforcing central standards. These moves compress evaluation cycles to 12 months, favoring vendors with pre-authorized environments and accelerating the HCM software in the government and public sector market adoption curve.

Mandatory Compliance With FedRAMP, GDPR And Zero-Trust Security Frameworks

Security frameworks have become decisive gatekeepers. Only 6% of HCM vendors have cleared the 12- to 18-month, USD 2 million FedRAMP authorization, concentrating on the United States federal demand among early certifiers. Europe's AI Act labels HR software as high risk, adding mandatory conformity assessments that can stretch project lead times by up to 1 year. The United States Department of Defense zero-trust roadmap pushes continuous authentication, disqualifying session-based architectures. Vendors that secured early clearances, Workday in 2019, SAP SuccessFactors in 2024, Oracle HCM Cloud in 2025, trace 18- to 24-month lead windows over challengers, tightening the HCM software in the government and public sector market competitive field.

Lengthy Public Procurement Cycles And Budget Release Delays

Lengthy procurement cycles and fragmented budget approvals continue to restrain HCM deployment across public-sector agencies. The United States Internal Revenue Service's 2025 human capital solicitation remained unresolved after 14 months due to multi-division funding dependencies, while North Carolina's statewide Workday rollout was delayed following budget reallocations toward disaster recovery. Although cooperative procurement frameworks such as NASPO ValuePoint help accelerate contracting, adoption remains limited across agencies. These structural delays modestly pressure annual growth rates but have not altered the long-term modernization trajectory of the HCM software in the government and public sector market.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Workforce Analytics Improving Mission Readiness And Budget Efficiency

- Generative AI Copilots Automating Personnel Action Requests

- Heightened Cyber-Sovereignty Rules Limiting Cross-Border Data Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Payroll and Compensation generated 28.32% of 2025 revenue, reflecting its deep integration with treasury disbursement networks and the risk of salary-related compliance breaches. Leading agencies rely on certified interfaces to systems such as the United States Automated Standard Application for Payments, positioning payroll as the anchoring module within HCM software in the government and public sector markets. Continuous controls over wage garnishments and pension deductions deliver tangible fiscal accountability, explaining payroll's durable share.

Learning and Development, however, is the fastest climber, advancing at a 13.42% CAGR as public managers pivot toward continuous capability building rather than episodic induction. India's Karmayogi iGOT platform more than doubled course-completion rates by embedding micro-credentials into performance reviews. Australia links AI-recommended nanodegrees with workforce planning, pre-empting skill gaps and signaling a strategic shift that widens the addressable spend for HCM software in the government and public sector markets.

On-Premises environments retained 56.19% of 2025 outlays because defense and intelligence units must isolate systems handling classified data. The Defense Information Systems Agency confines Top Secret files to government-owned data centers, which slows cloud penetration and reinforces reliance on secure, government-controlled infrastructure. Despite this, civilian agencies are steadily adopting cloud subscriptions to gain faster upgrades and flexible consumption-based budgets, while hybrid models balance sovereignty with mobility, expanding the HCM software footprint across both deployment camps.

Nonetheless, cloud subscriptions grow at a 12.81% CAGR as public bodies pursue faster upgrades and consumption-based budgets. Hybrid blueprints, where core records stay on-premises while analytics travel to the cloud, satisfy sovereignty requirements without sacrificing mobility, expanding the HCM software market in the government and public sectors across both camps.

Geography Analysis

North America dominates the HCM Software in the Government and Public Sector Market, accounting for 45.12% in 2025, but maturation is evident as easy workloads migrate first. Federal HR 2.0 alone represents a USD 1.2 billion pool, yet 40% of legacy apps hold classified constraints that slow conversions. Statewide Workday implementations in Arizona, Georgia, Vermont, and Utah illustrate how shared contracts accelerate adoption outside Washington, and Canadian provinces now pivot from deployment to analytics refinement. The Cybersecurity and Infrastructure Security Agency's zero-trust deadlines guarantee a replacement cycle for non-compliant suites.

European growth springs from the United Kingdom's GBP 800 million (USD 1.01 billion) Matrix framework, Germany's digital onboarding law, and France's nationwide SIRH overhaul. Spain's GEISER platform reduced help-desk traffic by 35% after deploying a chatbot, demonstrating follow-on value once core digitization is complete. While the European Union AI Act elongates lead times, it simultaneously creates a compliance moat that discourages under-capitalized entrants, reinforcing the market share of established suppliers in the HCM software market for government and the public sector.

Asia-Pacific is the fastest-growing region, with a 10.11% CAGR to 2031. India's national e-HRMS 2.0 and state-level Maha-AASTHA initiatives add millions of users annually. Australia commits AUD 180 million (USD 120 million) to workforce analytics upskilling, and New Zealand's shared-service roll-out standardizes payroll across 35 agencies. Cyber-sovereignty edicts in Vietnam and Indonesia slow cross-border hosting but simultaneously create greenfield demand for domestic data centers, bolstering the regional outlook for HCM software in the government and public sector markets.

- Workday, Inc.

- Oracle Corporation

- SAP SE

- UKG Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- Infor, Inc.

- Tyler Technologies, Inc.

- NEOGOV, Inc.

- Unit4 N.V.

- BambooHR LLC

- PeopleFluent (Learning Technologies Group plc)

- Ramco Systems Limited

- Paycor HCM, Inc.

- Gusto, Inc.

- The Sage Group plc

- SumTotal Systems, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Cloud-First Mandates in Public Sector HR Modernization

- 4.2.2 Mandatory Compliance with FedRAMP, GDPR and Zero-Trust Security Frameworks

- 4.2.3 AI-Driven Workforce Analytics Improving Mission Readiness & Budget Efficiency

- 4.2.4 Generative AI Copilots Automating Personnel Action Requests (PAR)

- 4.2.5 Integration of Unified Payroll with Treasury Payment Systems

- 4.2.6 Migration Incentives from Legacy Mainframe HRIS Decommissioning Grants

- 4.3 Market Restraints

- 4.3.1 Heightened Cyber-Sovereignty Rules Limiting Cross-Border Data Flows

- 4.3.2 Lengthy Public Procurement Cycles and Budget Release Delays

- 4.3.3 Skills Gap in Government IT to Execute Large-Scale HCM Transformations

- 4.3.4 Algorithmic Bias Scrutiny under Emerging AI Regulations

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Core HR Software

- 5.1.2 Payroll & Compensation

- 5.1.3 Talent Management

- 5.1.4 Workforce Management

- 5.1.5 Learning & Development

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Agency Size Tier

- 5.3.1 Large Government Agencies (10 000 employees+)

- 5.3.2 Medium Agencies (1 000-10 000 employees)

- 5.3.3 Small Agencies (1 000 employees)

- 5.4 By End-User Type

- 5.4.1 Federal / Central Government Agencies

- 5.4.2 State & Local Government

- 5.4.3 Defense & Intelligence Agencies

- 5.4.4 Public Education & Universities

- 5.4.5 Public Safety & Justice Departments

- 5.4.6 Healthcare & Social Services Agencies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia & New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 Oracle Corporation

- 6.4.3 SAP SE

- 6.4.4 UKG Inc.

- 6.4.5 Ceridian HCM Holding Inc.

- 6.4.6 Automatic Data Processing, Inc.

- 6.4.7 Paycom Software, Inc.

- 6.4.8 Paylocity Holding Corporation

- 6.4.9 Cornerstone OnDemand, Inc.

- 6.4.10 Infor, Inc.

- 6.4.11 Tyler Technologies, Inc.

- 6.4.12 NEOGOV, Inc.

- 6.4.13 Unit4 N.V.

- 6.4.14 BambooHR LLC

- 6.4.15 PeopleFluent (Learning Technologies Group plc)

- 6.4.16 Ramco Systems Limited

- 6.4.17 Paycor HCM, Inc.

- 6.4.18 Gusto, Inc.

- 6.4.19 The Sage Group plc

- 6.4.20 SumTotal Systems, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space & Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測