|

市場調查報告書

商品編碼

2063972

歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

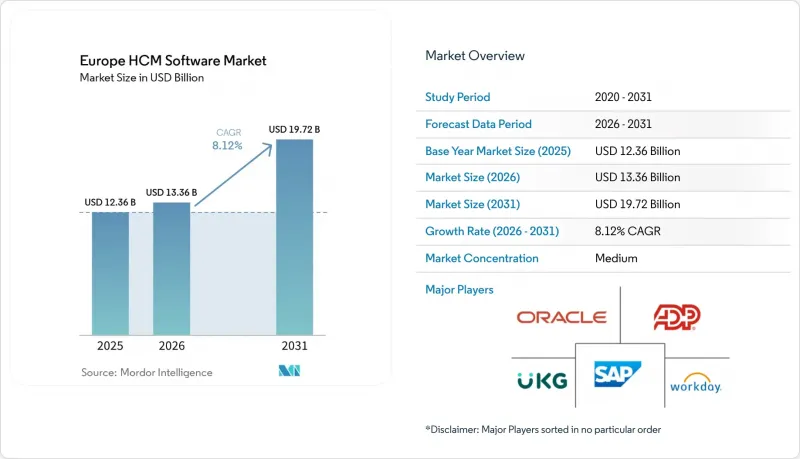

根據 Mordor Intelligence 預測,歐洲 HCM 軟體市場規模預計將在 2025 年達到 123.6 億美元,2026 年達到 133.6 億美元,到 2031 年達到 197.2 億美元,2026 年至 2031 年的複合年成長率為 8.12%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理等)、最終用戶產業(IT和電信、銀行、金融服務和保險、製造業等)以及地區進行細分。市場預測以美元計價。

歐洲HCM軟體市場的趨勢與洞察

向基於雲端的HCM平台的轉變正在加速。

到2025年,雲端將佔據歐洲人力資本管理(HCM)軟體市場67.21%的佔有率,這不僅是因為其成本效益,還因為雲端能夠提供以批次為中心的本地部署系統無法實現的監管靈活性。為此,Workday於2025年在法蘭克福和阿姆斯特丹推出了「歐盟主權雲端」。該雲端平台將完全由位於歐洲的管理員經營,使客戶能夠在滿足GDPR資料居住要求的同時利用機器學習模型。根據SAP的報告,72%的歐洲客戶已經採用了混合部署模式,即在ERP系統上維護薪資核算,同時在SuccessFactors上運作人才管理模組,這展現了分階段現代化的路徑。隨著要求近乎即時資訊揭露的指令不斷增加,雲端的採用預計將進一步加速。

對人才分析和人工智慧主導的洞察的需求日益成長

歐盟統計局2025年的一項調查顯示,歐盟只有56%的人口具備基本的數位技能,這將迫使企業從被動招募轉向主動人才規劃。 Workday位於都柏林的AI中心利用來自1Oracle客戶的匿名數據,在90天內預測員工離職風險的準確率達到了82%。 Oracle整合了技能本體圖譜,幫助丹麥銀行將資料工程職缺的招募週期縮短了40%。然而,SD Worx的一項調查顯示,員工人數少於250人的公司中,只有22%在使用預測分析,顯示面向中小企業的供應商仍存在巨大的市場潛力。為了遵守歐洲資料保護監管機構(EDPS)關於人工監督的指導方針,供應商正在其模型中添加置信度評分。

GDPR下的資料安全與隱私問題

Schrems II 裁決使跨大西洋資料流動變得更加複雜,迫使供應商除了標準合約條款外,還必須實施加密和匿名化措施。雖然 Workday 的「歐盟主權雲」將資料處理限制在歐盟境內,但 Davidson Morris 的 2025 年報告指出,58% 的英國雇主已經接受了 GDPR 審計,其中 12% 的雇主因資料保存做法不當而收到正式警告。諸如差分隱私和聯邦學習等保護隱私的分析技術正在興起,但這些技術需要許多中型市場整合商所缺乏的專業技能,而且成本高昂,實施起來也較為複雜。

細分市場分析

2025年,軟體在歐洲人力資本管理(HCM)軟體市場佔據72.04%的佔有率,而業務收益預計將在2026年至2031年間以9.21%的複合年成長率成長。實施專案越來越涵蓋資料遷移、變更管理和ERP整合,企業也正將預算從許可費用轉向諮詢費用。在人才短缺的背景下,對區域專家的需求不斷成長,外包商負責日常配置管理的託管服務合約也日益普及。

儘管軟體成長依然強勁,但隨著訂閱模式取代永久授權銷售以及可組合架構導致需求分散,利潤率正在下降。提供低程式碼工具和預訓練合規模板的供應商正在降低總體擁有成本並維持市場佔有率。在歐洲人力資本管理 (HCM) 軟體市場,兼具軟體和諮詢專業知識的廠商更受青睞,預計到 2031 年,服務收入將繼續超過純許可收入。

預計從2026年到2031年,混合部署將以9.74%的複合年成長率成長,成為所有部署模式中成長最快的模式。這是因為企業需要在滿足GDPR資料居住需求的同時,兼顧公共雲端分析的擴充性和創新速度。到2025年,雲端將佔據67.21%的市場佔有率,這主要得益於SaaS供應商能夠提供持續的功能更新和現成的合規模板。然而,隨著SAP和Oracle等供應商逐步停止對舊版的支持,純粹的本地部署正在減少。受監管產業正在將人才管理、學習和分析遷移到SaaS平台,同時出於資料居住的考慮,將薪資核算保留在本地。

Workday 的歐盟主權雲端和 SAP 的混合 SuccessFactors 實施方案展示了一條折衷路徑,使企業能夠在利用靈活分析的同時,保留自身的薪資核算邏輯。公共部門機構仍然傾向於資本投資,本地部署仍在繼續,但五年總擁有成本高出 30% 到 50%。混合部署浪潮將加速供應商整合,因為傳統的純本地部署供應商缺乏平台遷移所需的資金。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速向基於雲端的HCM平台轉型

- 對人才分析和人工智慧驅動的洞察的需求日益成長

- 歐盟嚴格且不斷變化的勞動合規要求

- 整合員工福祉與多元化、公平與包容性指標的數位化員工體驗平台的興起。

- 擴大歐洲投資者在ESG相關人才和資本報告的義務

- 引進隱私保護型人力資源技術以克服 GDPR 限制

- 市場限制因素

- GDPR下的資料安全與隱私問題

- 與傳統ERP和薪資系統整合的複雜性。

- 中型企業系統整合商人力資源技術實施人員短缺

- 由於通貨膨脹,公共部門機構正在削減IT預算。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 核心人力資源

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 北歐的

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Workday, Inc.

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand, Inc.

- Sage Group plc

- Personio GmbH

- HiBob Inc.

- SD Worx NV

- Cegid Group SA

- Ramco Systems Limited

- Visma AS

- Paycor HCM, Inc.

- Paycom Software, Inc.

- Zoho Corporation Pvt. Ltd.

- Rippling People Center Inc.

- SD Worx People Solutions UK Limited

- Cornerstone OnDemand Limited(UK)

- Zucchetti SpA

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe hCM software market size reached USD 12.36 billion in 2025 and is expected to reach USD 13.36 billion in 2026 and USD 19.72 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, and More), End-User Industry (IT and Telecommunications, BFSI, Industrial Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe HCM Software Market Trends and Insights

Accelerated Migration to Cloud-Based HCM Platforms

Cloud held 67.21% share of the Europe HCM Software market in 2025, but the driver extends beyond cost efficiency to regulatory agility that batch-oriented on-premises systems cannot match. Workday responded by launching an EU Sovereign Cloud in Frankfurt and Amsterdam in 2025, staffed exclusively by European-resident administrators, letting customers leverage machine-learning models while satisfying GDPR data-residency rules. SAP reported that 72% of its European base is already on hybrid deployments in which payroll remains on ERP but talent modules run on SuccessFactors, demonstrating a phased modernization path. As more directives require near-real-time disclosures, cloud penetration is set to accelerate further.

Growing Need for Workforce Analytics and AI-Driven Insights

Eurostat showed in 2025 that only 56% of the EU population held basic digital skills, forcing companies to switch from reactive hiring to predictive workforce planning. Workday's AI Center in Dublin uses anonymized data from 10 000 customers to reach 82% accuracy in predicting 90-day attrition risk. Oracle embedded skills-ontology graphs that helped Danske Bank cut time-to-fill for data-engineering roles by 40%. Yet SD Worx found that only 22% of firms under 250 employees use predictive analytics, indicating white space for SME-focused vendors. Vendors are adding model-confidence scores to comply with EDPS guidance on human oversight.

Data Security and Privacy Concerns Under GDPR

The Schrems II ruling continues to complicate transatlantic data flows, forcing vendors to adopt standard contractual clauses plus encryption and pseudonymization. Workday's EU Sovereign Cloud keeps processing inside EU borders, but DavidsonMorris reported in 2025 that 58% of UK employers had already faced GDPR audits, with 12% receiving formal warnings for poor data-retention practices. Privacy-preserving analytics like differential privacy and federated learning are emerging, yet they require specialized skills that many mid-market integrators lack, introducing cost and complexity.

Other drivers and restraints analyzed in the detailed report include:

- Stringent and Evolving EU Labor Compliance Requirements

- Rise of Digital Employee Experience Platforms Integrating Well-Being and DEI Metrics

- Integration Complexity With Legacy ERP and Payroll Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is forecast to expand at a 9.21% CAGR between 2026 and 2031, even though software captured 72.04% of the Europe HCM Software market share in 2025. Implementation projects increasingly span data migration, change management, and ERP integration, so enterprises are shifting budget from licenses to consulting. This shortage is spawning regional specialists and managed-services arrangements in which outsourcers administer day-to-day configuration.

Software growth remains steady, but margins are tightening as subscription models replace perpetual sales and as composable architectures fragment demand. Vendors that package low-code tools and pretrained compliance templates lower the cost of ownership and protect share. The European HCM Software market rewards players that couple software with advisory know-how, so service lines are expected to keep outpacing pure license revenue through 2031.

Hybrid deployment is forecast to grow at 9.74% CAGR from 2026 to 2031, the fastest rate among deployment modes, as organizations balance GDPR data-residency mandates with the scalability and innovation velocity of public-cloud analytics. Cloud held 67.21% market share in 2025, driven by SaaS vendors' ability to deliver continuous feature updates and pre-built compliance templates, yet pure on-premises deployments are declining as vendors such as SAP and Oracle phase out support for legacy versions. Regulated industries keep payroll on-premises for data-residency reasons while moving talent, learning, and analytics to SaaS.

Workday's EU Sovereign Cloud and SAP's hybrid SuccessFactors deployments demonstrate a middle path that lets firms preserve custom payroll logic but tap elastic analytics. On-premises deployments persist in public agencies that still favor capital expenditure, although the total cost of ownership remains 30% to 50% higher over five years. The hybrid wave will accelerate vendor consolidation because legacy on-premises specialists lack the capital to re-platform.

List of Companies Covered in this Report:

- SAP SE

- Workday, Inc.

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand, Inc.

- Sage Group plc

- Personio GmbH

- HiBob Inc.

- SD Worx NV

- Cegid Group SA

- Ramco Systems Limited

- Visma AS

- Paycor HCM, Inc.

- Paycom Software, Inc.

- Zoho Corporation Pvt. Ltd.

- Rippling People Center Inc.

- SD Worx People Solutions UK Limited

- Cornerstone OnDemand Limited (U.K.)

- Zucchetti S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Migration to Cloud-based HCM Platforms

- 4.2.2 Growing Need for Workforce Analytics and AI-driven Insights

- 4.2.3 Stringent and Evolving EU Labor Compliance Requirements

- 4.2.4 Rise of Digital Employee Experience Platforms Integrating Well-being and DEI Metrics

- 4.2.5 Expansion of ESG-linked Human Capital Reporting Mandates from European Investors

- 4.2.6 Adoption of Privacy-Preserving HR Tech to Navigate GDPR Constraints

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns under GDPR

- 4.3.2 Integration Complexity with Legacy ERP and Payroll Systems

- 4.3.3 Shortage of HR Tech Implementation Talent across Mid-Market System Integrators

- 4.3.4 Inflation-Driven IT Budget Compression in Public Sector Organizations

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Nordics

- 5.6.7 Russia

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Workday, Inc.

- 6.4.3 Oracle Corporation

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Sage Group plc

- 6.4.9 Personio GmbH

- 6.4.10 HiBob Inc.

- 6.4.11 SD Worx NV

- 6.4.12 Cegid Group SA

- 6.4.13 Ramco Systems Limited

- 6.4.14 Visma AS

- 6.4.15 Paycor HCM, Inc.

- 6.4.16 Paycom Software, Inc.

- 6.4.17 Zoho Corporation Pvt. Ltd.

- 6.4.18 Rippling People Center Inc.

- 6.4.19 SD Worx People Solutions UK Limited

- 6.4.20 Cornerstone OnDemand Limited (U.K.)

- 6.4.21 Zucchetti S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測