|

市場調查報告書

商品編碼

2073276

中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)Middle East and Africa HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

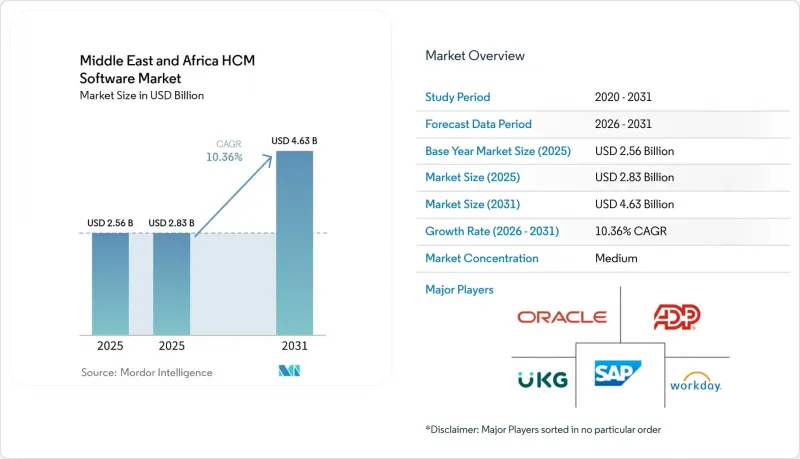

根據 Mordor Intelligence 預測,中東和非洲地區的人力資源管理 (HCM) 軟體市場規模將從 2025 年的 25.6 億美元成長到 2026 年的 28.3 億美元,到 2031 年將達到 46.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理、人力資源管理等)、最終用戶產業(IT和電信等)以及地區進行細分。市場預測以價值(美元)表示。

中東和非洲HCM軟體市場趨勢與洞察

加速海灣合作理事會地區企業採用雲端運算

海灣國家的雇主正在快速升級其傳統的人力資源資料庫,以滿足融入國家轉型計畫的即時報告標準。在沙烏地阿拉伯,政府服務的數位化率將在2024年達到95%,私部門董事會目前正在對這些標準進行基準測試,從而積極推動基於雲端的人力資本管理(HCM)的採用。阿拉伯聯合大公國(阿拉伯聯合大公國)正在將勞動力市場合規性API與私有HCM套件整合,將審計週期從季度縮短至月度,並獎勵那些保持無縫雲端連接的公司。 2025年,卡達公共服務和政府發展局與SAP SuccessFactors合作發布了配置藍圖,目前已被多家私人公司重複使用,涵蓋超過85,000名員工。在沙烏地阿拉伯和阿拉伯聯合大公國營運主權雲端節點的供應商透過消除對資料居住要求的擔憂,縮短了銷售週期。隨著超大規模資料中心業者的上運作,混合安全策略正在緩解銀行和公共產業的擔憂,使延遲的轉型得以實現。

促進工資保護和合規自動化方面的法規

工資保障框架已將薪資核算轉變為至關重要的合規流程。阿拉伯聯合大公國的「工資保障系統2.0」強制要求雇主在10個工作天內透過認可機構支付工資,重犯者將面臨巨額罰款和吊銷工作許可的處罰。沙烏地阿拉伯的「Mudad」平台旨在透過將薪資數據與社會安全和移民記錄進行匹配,到2025年將合約合規率提高到85-90%。這迫使企業用整合套件取代孤立的人力資源模組,這些套件能夠自動將資料連接到Qiwa系統。科威特現在強制要求使用生物識別考勤系統,阿曼則要求在員工入職後30天內提交電子合約。這些措施進一步擴大了人力資本管理系統(HCM)必須應對的合規範圍。

有關資料隱私和資料居住的法規增加了實施的複雜性。

各國的資料保護法要求供應商將員工記錄在地化,導致原本統一的多租戶雲端平台被分割成多個獨立實例,每個實例對應一個司法管轄區。阿拉伯聯合大公國維護一份資料匯出機制白名單,導致採購延遲長達六個月,因為買家需要等待監管部門的批准。南非的資訊監管機構已開始發出強制執行通知,引發了人們對法律責任的擔憂,這阻礙了保守型銀行的轉型。在奈及利亞,高風險人力資源流程現在必須進行資料保護影響評估,而中小企業雇主則透過要求供應商提供承包合規服務,將這一負擔轉嫁給了供應商。由此產生的拼湊式環境迫使供應商維護多個基礎設施,增加了銷貨成本並延緩了藍圖的實現。

細分市場分析

預計到2031年,服務市場將以11.24%的複合年成長率成長,成長速度將超過軟體市場。中東和非洲的人力資本管理(HCM)軟體市場正在擴張,這主要得益於部署、整合和託管服務的推動。這是因為所有海灣國家都在整合能夠適應其獨特退休金法規、多語言介面以及與政府入口網站連接性的薪資核算系統。 Oracle與eOracle於2025年簽署的合約包含為期三年的託管服務層級,涵蓋38個國家的合規性更新,這表明供應商如何在核心模組運作後確保持續的收入來源。像Jisr這樣的新創公司透過將沙烏地阿拉伯的「沙烏地化」標準映射到高階主管可以自行使用的自動化儀表板,從而獲得持續的諮詢費收入。在衣索比亞和塞拉利昂,公共部門津貼正在推動公務員制度改革,使當地合作夥伴有機會提供全球供應商在當地不具備的培訓和轉型管理服務。

到2025年,軟體支出仍將佔總支出的73.48%,永久授權升級和SaaS訂閱幾乎構成所有項目的基礎。然而,隨著中型買家在開放API生態系統和單體套件之間展開競價,價格競爭日益激烈。區域性新興企業將考勤管理系統、保險聚合和薪資服務捆綁成單一的員工收費模式,而大型平台則將某些微服務拆分以保持敏捷性。在預測期內,中東和非洲HCM軟體市場的整體服務佔有率預計將達到30%左右,這表明僅靠產品化無法解決該地區在地化帶來的挑戰。

預計到2025年,雲端解決方案將佔市場佔有率的68.92%,複合年成長率(CAGR)為11.56%。然而,由於監管和電網的限制,純粹的公共架構在基於SaaS的人力資源管理模組之外並不常見。銀行和政府機構擴大選擇「分離式」拓撲結構,即在本地節點上處理薪資核算,而將分析功能卸載到多區域雲端平台。隨著微軟、 Oracle和SAP現在提供將敏感表複製到本地儲存的區域特定實例,混合部署預計將在中東和非洲的人力資本管理(HCM)軟體市場獲得更大的市場佔有率。

本地部署環境依然存在,尤其是在禁止外部網路存取的政府部門中,但即使是這些場所也在採用容器化編配來實現修補程式自動化。肯亞一個暫停的資料中心計畫表明,電力短缺減緩了超大規模資料中心業者資料中心的部署,配備柴油發電機的備用機房仍在繼續使用。提供同步代理和零信任閘道器的供應商透過使客戶能夠在無需重寫程式碼的情況下在主權容量和公共容量之間切換,正在贏得市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速海灣合作理事會國家企業採用雲端運算

- 推動工資保障和自動化合規的法規制定

- 對勞動力分析和人工智慧驅動的洞察的需求日益成長

- 行動辦公和遠距辦公的增加催生了對整合式 HCM 平台的需求。

- 沙烏地阿拉伯的NEOM大型企劃正在推動勞動力管理數位化需求。

- 非洲以金融科技主導的薪資核算基礎設施正在超越傳統的人力資源系統。

- 市場限制因素

- 有關資料隱私和資料居住的法規實施起來越來越複雜。

- 非洲部分市場缺乏具備雲端運算技術技能的人員

- 阿拉伯語方言的多樣性阻礙了自然語言處理技術在人力資本管理軟體中的應用。

- 不同地區資料中心不斷上漲的電力成本正在影響 SaaS 定價。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- Core HR

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與技能發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 阿曼

- 巴林

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 肯亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Automatic Data Processing, Inc.

- BambooHR LLC

- Bayzat Technology LLC

- Dayforce, Inc.

- Cornerstone OnDemand, Inc.

- GulfHR FZ LLC

- HiBob Ltd.

- Infor, Inc.

- MenaITech for Information Technology

- Oracle Corporation

- Paycom Software, Inc.

- Paycor HCM, Inc.

- Paylocity Holding Corporation

- Ramco Systems Limited

- Rippling People Center Inc.

- Sage Group plc

- SeamlessHR Ltd.

- SAP SE

- UKG, Inc.

- Workday, Inc.

- ZenHR Solutions LLC

- Zoho Corporation Pvt. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa HCM Software market size is projected to expand from USD 2.56 billion in 2025 to USD 2.83 billion in 2026 and USD 4.63 billion by 2031, registering a CAGR of 10.36% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, and More), End-User Industry (IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa HCM Software Market Trends and Insights

Accelerating Cloud Adoption Across GCC Enterprises

Gulf employers are rapidly modernizing legacy HR databases to meet real-time reporting standards embedded in national transformation plans. Saudi Arabia reached 95% digitization of government services in 2024, and private-sector boards now benchmark against those standards, creating a halo effect for cloud HCM rollouts. The United Arab Emirates integrated its labor-market compliance APIs with private HCM suites, cutting audit cycles from quarterly to monthly and rewarding firms that maintain seamless cloud connectivity. Qatar's Civil Service and Government Development Bureau partnered with SAP SuccessFactors in 2025 for more than 85,000 workers, publishing configuration blueprints that private companies now reuse. Vendors that operate sovereign-cloud nodes inside Saudi Arabia and the United Arab Emirates have shortened sales cycles by reducing data-residency objections. As hyperscaler regions come online, hybrid security policies are easing concerns among banks and utilities, unlocking postponed migrations.

Regulatory Push for Wage Protection and Compliance Automation

Wage-protection frameworks have turned payroll into a mission-critical compliance process. The United Arab Emirates' Wage Protection System 2.0 obliges employers to transfer salaries within 10 working days through accredited institutions, with hefty fines and work-permit suspensions for repeat breaches. Saudi Arabia's Mudad platform cross-references payroll with social-insurance and immigration records, delivering 85-90% contract compliance in 2025 and forcing companies to replace siloed HR modules with integrated suites that automatically feed Qiwa. Kuwait now mandates biometric attendance capture, while Oman requires digital contract filings within 30 days of hire, further expanding the compliance footprint that HCM must cover.

Data Privacy and Residency Regulations Increasing Deployment Complexity

Sovereign data-protection acts oblige vendors to localize employee records, fragmenting what could be a single multi-tenant cloud into jurisdiction-specific instances. The United Arab Emirates maintains a whitelist of data-export mechanisms, extending procurement by up to 6 months as buyers await regulatory clearance. South Africa's Information Regulator has begun issuing enforcement notices, raising liability concerns that are stalling migrations among conservative banks. Nigeria now requires data-protection impact assessments for high-risk HR processing, a burden that small employers pass through to vendors by demanding turnkey compliance services. The resulting patchwork forces suppliers to maintain multiple infrastructure footprints, inflating the cost of goods sold and slowing roadmap delivery.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Workforce Analytics and AI-Powered Insights

- Rising Mobile and Remote Workforce Requiring Unified HCM Platforms

- Limited Cloud-Skilled Talent Pool in Several African Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are forecast to outpace software growth, expanding at an 11.24% CAGR through 2031. The Middle East and Africa HCM Software market is expanding, driven by implementation, integration, and managed services, as every Gulf country integrates payroll with unique pension rules, multi-lingual interfaces, and government gateway connections. Oracle's 2025 deal with e and embedded a three-year managed-services layer that covers compliance updates for 38 countries, illustrating how vendors lock in annuity streams once core modules go live. Start-ups such as Jisr secure recurring consulting fees by mapping Saudization thresholds into automated dashboards that executives can self-serve. As public-sector grants fund civil-service reforms in Ethiopia and Sierra Leone, local partners gain opportunities to deliver training and change-management work that global vendors do not staff locally.

Software still accounted for 73.48% of 2025 spending, as perpetual-license upgrades and SaaS subscriptions anchor every project. Nevertheless, price pressure intensifies as mid-market buyers weigh open API ecosystems against monolithic suites. Regional challengers bundle attendance scanners, insurance aggregation, and earned-wage access inside a single per-employee fee, prompting large platforms to unbundle specific micro-services to retain agility. Over the forecast window, the share of total services in the Middle East and Africa HCM Software market is expected to reach the low-30% range, confirming that productization alone cannot absorb the region's localization load.

Cloud solutions delivered 68.92% of the 2025 value and are set to grow at an 11.56% CAGR, yet legal and power-grid realities mean purely public architectures are uncommon beyond software-as-a-service talent modules. Buyers in banking and government increasingly opt for split-stack topologies that house payroll on sovereign nodes while pushing analytics to multiregion clouds. The Middle East and Africa HCM Software market share attributed to hybrid deployments will likely climb because Microsoft, Oracle, and SAP now offer region-specific instances that replicate sensitive tables to in-country storage.

On-premises footprints persist, particularly inside ministries that forbid external internet routes, but even these sites adopt containerized orchestration to gain patch automation. Kenya's suspended data-center project demonstrated that power scarcity can slow hyperscaler rollout, keeping standby diesel-based data rooms in play. Vendors that supply synchronization agents and zero-trust gateways capture wallet share because they let clients toggle between sovereign and public capacity without rewrites.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Core HR

- Talent Management

- Workforce Management

- Payroll Management

- Learning and Development

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Kuwait

- Oman

- Bahrain

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Kenya

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- Automatic Data Processing, Inc.

- BambooHR LLC

- Bayzat Technology LLC

- Dayforce, Inc.

- Cornerstone OnDemand, Inc.

- GulfHR FZ LLC

- HiBob Ltd.

- Infor, Inc.

- MenAITech for Information Technology

- Oracle Corporation

- Paycom Software, Inc.

- Paycor HCM, Inc.

- Paylocity Holding Corporation

- Ramco Systems Limited

- Rippling People Center Inc.

- Sage Group plc

- SeamlessHR Ltd.

- SAP SE

- UKG, Inc.

- Workday, Inc.

- ZenHR Solutions LLC

- Zoho Corporation Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Cloud Adoption Across GCC Enterprises

- 4.2.2 Regulatory Push for Wage Protection and Compliance Automation

- 4.2.3 Growing Demand for Workforce Analytics and AI-Powered Insights

- 4.2.4 Rising Mobile and Remote Workforce Requiring Unified HCM Platforms

- 4.2.5 Saudi NEOM Mega-Projects Driving Labor-Tracking Digitization Demand

- 4.2.6 Africa's Fintech-Led Payroll Infrastructure Leapfrogging Legacy HR Systems

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Residency Regulations Increasing Deployment Complexity

- 4.3.2 Limited Cloud-Skilled Talent Pool in Several African Markets

- 4.3.3 Fragmented Arabic Dialects Hindering NLP Adoption in HCM Software

- 4.3.4 High Cost of Regional Data Center Power Impacting SaaS Pricing

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 Middle East

- 5.6.1.1 Saudi Arabia

- 5.6.1.2 United Arab Emirates

- 5.6.1.3 Qatar

- 5.6.1.4 Kuwait

- 5.6.1.5 Oman

- 5.6.1.6 Bahrain

- 5.6.1.7 Rest of Middle East

- 5.6.2 Africa

- 5.6.2.1 South Africa

- 5.6.2.2 Nigeria

- 5.6.2.3 Egypt

- 5.6.2.4 Kenya

- 5.6.2.5 Rest of Africa

- 5.6.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Automatic Data Processing, Inc.

- 6.4.2 BambooHR LLC

- 6.4.3 Bayzat Technology LLC

- 6.4.4 Dayforce, Inc.

- 6.4.5 Cornerstone OnDemand, Inc.

- 6.4.6 GulfHR FZ LLC

- 6.4.7 HiBob Ltd.

- 6.4.8 Infor, Inc.

- 6.4.9 MenaITech for Information Technology

- 6.4.10 Oracle Corporation

- 6.4.11 Paycom Software, Inc.

- 6.4.12 Paycor HCM, Inc.

- 6.4.13 Paylocity Holding Corporation

- 6.4.14 Ramco Systems Limited

- 6.4.15 Rippling People Center Inc.

- 6.4.16 Sage Group plc

- 6.4.17 SeamlessHR Ltd.

- 6.4.18 SAP SE

- 6.4.19 UKG, Inc.

- 6.4.20 Workday, Inc.

- 6.4.21 ZenHR Solutions LLC

- 6.4.22 Zoho Corporation Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)