|

市場調查報告書

商品編碼

2073273

東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Southeast Asia HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

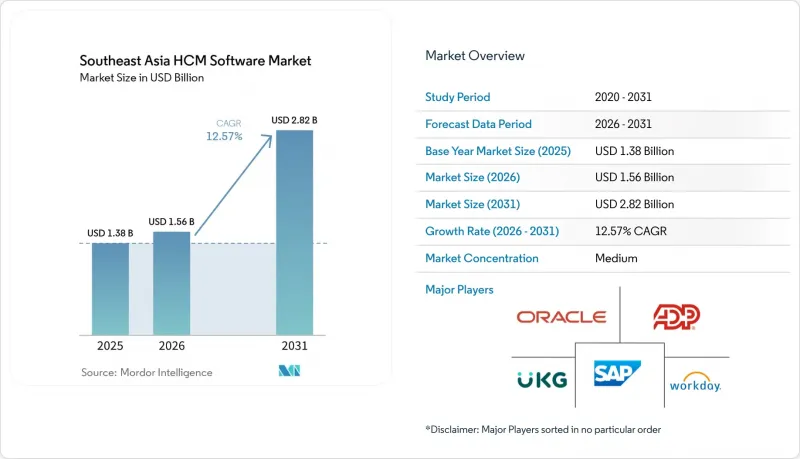

據 Mordor Intelligence 稱,東南亞 HCM 軟體市場在 2025 年的價值為 13.8 億美元,預計到 2031 年將從 2026 年的 15.6 億美元成長到 28.2 億美元,在預測期(2026-2031 年)內的複合年成長率為 12.57%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署等)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理、人力資源管理、薪資管理等)以及最終用戶產業(IT和電信、銀行、金融服務和保險等)進行細分。市場預測以美元計價。

東南亞HCM軟體市場趨勢與洞察

加速「雲端優先」人力資源轉型

印尼、泰國和菲律賓的財務總監(CFO) 正在用 Oracle Fusion Cloud HCM 取代傳統的本地部署系統,以遏制不斷飆升的人事費用通膨。他們表示,遷移到 Oracle Fusion Cloud HCM 後,IT 成本降低了 39%。這項轉變的驅動力是「行動優先」理念,85% 的第一線員工僅透過智慧型手機存取人力資源應用程式。公共部門的領先案例,例如印尼財政部,實施「Satu Kemenkeu」平台後,人力資源交易處理時間縮短了 43.7%,遠超私部門的預期。

政府主導的數位人才舉措

馬來西亞人力資源發展公司(HRDC)將於2025年提供2.25億美元的津貼用於企業培訓,其中40%的申請將涵蓋人力資本管理(HCM)軟體費用。菲律賓和新加坡簽署的《數位經濟協議》實現了電子工資記錄的互用,從而減少了跨國公司在共用服務方面的摩擦。柬埔寨已為284,484名公務員實現了薪資核算的標準化,並在世界銀行的支持下升級了人力資源管理資訊系統(HRMIS),從而在採購方面樹立了先例。

東協各國法律合規的碎片化

由於新加坡的中央公積金(CPF)、馬來西亞的僱員公積金(EPF)和印尼的印尼社會保險(BPJS)採用不同的薪資核算公式,供應商被迫維護多個運算引擎,導致產品成本增加,功能標準化進程也因此延緩。在菲律賓,不同的社會安全體系、菲律賓健康保險(PhilHealth)和住房發展互助基金(Pag-IBIG)的繳款額度因收入等級和就業類型而異,進一步加劇了問題的複雜性。同時,泰國的社會安全基金以及越南的社會保險、醫療保險和失業保險體係也提出了額外的在地化要求。資料隱私法規的差異進一步增加了跨境平台部署的難度,迫使小規模的供應商推遲多個國家/地區的計畫。

細分市場分析

預計2026年至2031年間,業務收益將成長13.74%,反映出市場對法規映射和變更管理的需求不斷成長。儘管軟體在2025年仍佔74.92%,但許多買家現在選擇將實施和管理服務協議捆綁在一起,以確保持續更新監管要求。 Darwinbox在菲律賓推出的跨國薪資核算服務就是一個典型的例子,它顯示了供應商如何將「合規即服務」模式貨幣化。在雲端遷移專案的推動下, Oracle在亞太地區的2025會計年度業務收益成長了18%。

諮詢和管理服務的採用在跨國業務擴張的公司中最為顯著,因為跨國監管的分散使得更換供應商成本高昂。大型企業將資料遷移外包以加速雲端轉型,而中小企業通常將初始設定委託給合作夥伴。因此,隨著每一波新一輪的採用,尤其是在嚴格監管的行業中,服務在東南亞人力資本管理 (HCM) 軟體市場的佔有率正在逐步擴大。

預計到2025年,雲端市場佔有率將達到64.41%,年均成長率為14.22%。隨著供應商在雅加達、胡志明市和吉隆坡等地開設資料中心以滿足資料主權法規的要求,雲端的領先優勢預計將進一步擴大。雖然由於資料主權要求以及與舊有系統的整合,本地部署在國防和政府機構等高度監管的行業仍然佔據主導地位,但隨著雲端供應商建立國內資料中心以滿足居住要求,這一細分市場正在萎縮。

混合模式正逐漸在國防和醫療保健機構中普及,這些機構希望利用雲端人力資源模組,同時在本地處理薪資核算管理。新加坡國家醫療集團 (National Healthcare Group) 於 2024 年採用了這種混合架構。更高的運作、免維護升級和更好的行動用戶體驗正在加速中小企業 (SME) 對雲端技術的採用。同時,先前對雲端解決方案持謹慎態度的大型企業,現在也開始擁抱雲端技術,以整合人工智慧分析。因此,預計到 2031 年,雲端技術將佔據東南亞人力資本管理 (HCM) 軟體市場佔有率的三分之二以上。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章執行摘要

第3章 市場狀況

- 市場概覽

- 市場促進因素

- 加速「雲端優先」人力資源轉型

- 政府主導的數位人才發展舉措

- 千禧世代和Z世代勞動力的擴張。

- 整合了人力資源功能的社群型「超級應用」的興起。

- 引入人工智慧驅動的預測性人才分析

- 跨境自由業平台加劇了薪資核算的複雜性。

- 市場限制因素

- 東南亞國協法律遵守的差異

- 小規模人力資源技術預算的限制

- 對資料儲存位置和主權的擔憂

- 人力資源與資訊科技一體化人員短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第4章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- Core HR

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與技能發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 國家

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 菲律賓

- 其他東南亞國家

第5章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAP SE

- Oracle Corporation

- Workday Inc.

- Automatic Data Processing Inc.

- UKG Inc.

- Dayforce, Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Paycom Software Inc.

- Paylocity Holding Corporation

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Darwinbox Digital Solutions Pvt. Ltd.

- The Sage Group plc

- Intuit Inc.

- Global Groupware Solutions Limited

- PeopleStrong Technologies Pvt. Ltd.

- HiBob Ltd.

- Rippling People Center Inc.

- Gusto Inc.

- Deel Inc.

- Infor Inc.

- ServiceNow Inc.

- SumTotal Systems LLC

第6章 市場機會與未來展望

- 評估未開發的領域和未滿足的需求

According to Mordor Intelligence, the southeast asia HCM software market size was valued at USD 1.38 billion in 2025 and is estimated to grow from USD 1.56 billion in 2026 to reach USD 2.82 billion by 2031, at a CAGR of 12.57% during the forecast period (2026-2031).

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud, On-Premises, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

Southeast Asia HCM Software Market Trends and Insights

Accelerated Cloud-First HR Transformation

Chief financial officers in Indonesia, Thailand, and the Philippines are replacing legacy on-premises systems to curb rising labor-cost inflation, citing 39% information-technology savings after migrating to Oracle Fusion Cloud HCM. Mobile-first behavior underpins this pivot, with 85% of staff in frontline industries accessing HR apps solely on smartphones. Public-sector exemplars, such as Indonesia's Ministry of Finance, cut personnel-transaction processing time by 43.7% after rolling out the Satu Kemenkeu platform, raising private-sector expectations.

Government-Led Digital Workforce Initiatives

Malaysia's Human Resource Development Corporation subsidized USD 225 million of enterprise training in 2025, and 40% of claims covered HCM software fees. The Philippines-Singapore Digital Economy Agreement mutualizes electronic payroll records, reducing friction in shared services for multinationals. Cambodia standardized payroll for 284,484 civil servants through a World Bank-backed HRMIS upgrade, setting procurement precedents.

Fragmented Statutory Compliance Across ASEAN

Separate payroll formulas for Singapore CPF, Malaysia EPF, and Indonesia BPJS oblige vendors to maintain multiple calculation engines, inflating product costs and stalling feature parity. The Philippines adds further complexity with Social Security System, PhilHealth, and Pag-IBIG Fund contributions that vary by income bracket and employment type, while Thailand's Social Security Fund and Vietnam's social insurance, health insurance, and unemployment insurance schemes impose additional localization requirements. Divergent data-privacy regimes further complicate cross-border platform rollouts, forcing smaller providers to defer multi-country support.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Millennial and Gen Z Workforce Demographics

- Emergence of Regional Super-Apps Integrating HR Functions

- Limited HR Tech Budgets in Micro-SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to climb at 13.74% from 2026 to 2031, reflecting rising demand for statutory-compliance mapping and change management. In 2025, software still dominated at 74.92%, but many buyers now bundle implementation and managed-services contracts to ensure continuous regulatory updates. Darwinbox's multi-country payroll launch in the Philippines exemplifies how vendors monetize compliance-as-a-service. Oracle's Asia-Pacific services revenue jumped 18% in fiscal 2025 on cloud-migration projects.

Adoption of consulting and managed services is strongest among firms expanding across borders, where fragmented rules create switching costs. Large enterprises outsource data migration to accelerate cloud cutovers, while SMEs lean on partners to handle initial configuration. As a result, services capture an incremental share of the Southeast Asia HCM Software market size for each new deployment wave, especially in regulated verticals.

Cloud captured 64.41% in 2025 and is forecast to grow 14.22% annually, extending its lead as vendors open Jakarta, Ho Chi Minh City, and Kuala Lumpur data centers to satisfy sovereignty rules. On-premises deployments persist in regulated sectors such as defense and government, where data-sovereignty mandates and legacy-system integration requirements favor locally hosted infrastructure, but this segment is contracting as cloud providers establish in-country data centers to satisfy residency rules.

Hybrid models persist for defense and healthcare entities wanting cloud talent modules but on-premises payroll. Singapore's National Healthcare Group adopted such a hybrid stack in 2024. Improved uptime, zero-maintenance upgrades, and mobile UX propel cloud uptake among SMEs, whereas large enterprises, previously hesitant, now embrace cloud to integrate AI analytics. Consequently, the cloud segment is expected to command more than two-thirds of the Southeast Asia HCM Software market share by 2031.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Core HR

- Talent Management

- Workforce Management

- Payroll Management

- Learning and Development

- By End-User Industry

- IT and Telecommunications

- BFSI

- Industrial Manufacturing

- Healthcare and Lifesciences

- Retail and E-commerce

- Government and Public Sector

- Other End-User Industries

- By Country

- Singapore

- Malaysia

- Indonesia

- Thailand

- Philippines

- Rest of Southeast Asia

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Workday Inc.

- Automatic Data Processing Inc.

- UKG Inc.

- Dayforce, Inc.

- Cornerstone OnDemand Inc.

- BambooHR LLC

- Paycom Software Inc.

- Paylocity Holding Corporation

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- Darwinbox Digital Solutions Pvt. Ltd.

- The Sage Group plc

- Intuit Inc.

- Global Groupware Solutions Limited

- PeopleStrong Technologies Pvt. Ltd.

- HiBob Ltd.

- Rippling People Center Inc.

- Gusto Inc.

- Deel Inc.

- Infor Inc.

- ServiceNow Inc.

- SumTotal Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 EXECUTIVE SUMMARY

3 MARKET LANDSCAPE

- 3.1 Market Overview

- 3.2 Market Drivers

- 3.2.1 Accelerated Cloud-First HR Transformation

- 3.2.2 Government-Led Digital Workforce Initiatives

- 3.2.3 Expanding Millennial and Gen Z Workforce Demographics

- 3.2.4 Emergence of Regional "Super-Apps" Integrating HR Functions

- 3.2.5 AI-Powered Predictive Workforce Analytics Adoption

- 3.2.6 Cross-Border Freelance Platforms Fueling Payroll Complexity

- 3.3 Market Restraints

- 3.3.1 Fragmented Statutory Compliance Across ASEAN

- 3.3.2 Limited HR Tech Budgets in Micro-SMEs

- 3.3.3 Data Residency and Sovereignty Concerns

- 3.3.4 Shortage of HR IT Integration Talent

- 3.4 Industry Value Chain Analysis

- 3.5 Regulatory Landscape

- 3.6 Technological Outlook

- 3.7 Impact of Macroeconomic Factors on the Market

- 3.8 Porter's Five Forces Analysis

- 3.8.1 Bargaining Power of Suppliers

- 3.8.2 Bargaining Power of Buyers

- 3.8.3 Threat of New Entrants

- 3.8.4 Threat of Substitutes

- 3.8.5 Intensity Competitive Rivalry

4 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 4.1 By Component

- 4.1.1 Software

- 4.1.2 Services

- 4.2 By Deployment Mode

- 4.2.1 Cloud

- 4.2.2 On-Premises

- 4.2.3 Hybrid

- 4.3 By Organization Size

- 4.3.1 Large Enterprises

- 4.3.2 Small and Medium Enterprises

- 4.4 By Application

- 4.4.1 Core HR

- 4.4.2 Talent Management

- 4.4.3 Workforce Management

- 4.4.4 Payroll Management

- 4.4.5 Learning and Development

- 4.5 By End-User Industry

- 4.5.1 IT and Telecommunications

- 4.5.2 BFSI

- 4.5.3 Industrial Manufacturing

- 4.5.4 Healthcare and Lifesciences

- 4.5.5 Retail and E-commerce

- 4.5.6 Government and Public Sector

- 4.5.7 Other End-User Industries

- 4.6 By Country

- 4.6.1 Singapore

- 4.6.2 Malaysia

- 4.6.3 Indonesia

- 4.6.4 Thailand

- 4.6.5 Philippines

- 4.6.6 Rest of Southeast Asia

5 COMPETITIVE LANDSCAPE

- 5.1 Market Concentration

- 5.2 Strategic Moves

- 5.3 Market Share Analysis

- 5.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 5.4.1 SAP SE

- 5.4.2 Oracle Corporation

- 5.4.3 Workday Inc.

- 5.4.4 Automatic Data Processing Inc.

- 5.4.5 UKG Inc.

- 5.4.6 Dayforce, Inc.

- 5.4.7 Cornerstone OnDemand Inc.

- 5.4.8 BambooHR LLC

- 5.4.9 Paycom Software Inc.

- 5.4.10 Paylocity Holding Corporation

- 5.4.11 Zoho Corporation Pvt. Ltd.

- 5.4.12 Ramco Systems Limited

- 5.4.13 Darwinbox Digital Solutions Pvt. Ltd.

- 5.4.14 The Sage Group plc

- 5.4.15 Intuit Inc.

- 5.4.16 Global Groupware Solutions Limited

- 5.4.17 PeopleStrong Technologies Pvt. Ltd.

- 5.4.18 HiBob Ltd.

- 5.4.19 Rippling People Center Inc.

- 5.4.20 Gusto Inc.

- 5.4.21 Deel Inc.

- 5.4.22 Infor Inc.

- 5.4.23 ServiceNow Inc.

- 5.4.24 SumTotal Systems LLC

6 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 6.1 White-Space and Unmet-Need Assessment

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)