|

市場調查報告書

商品編碼

2064512

人力資本管理的智慧體人工智慧:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Agentic AI In HCM - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

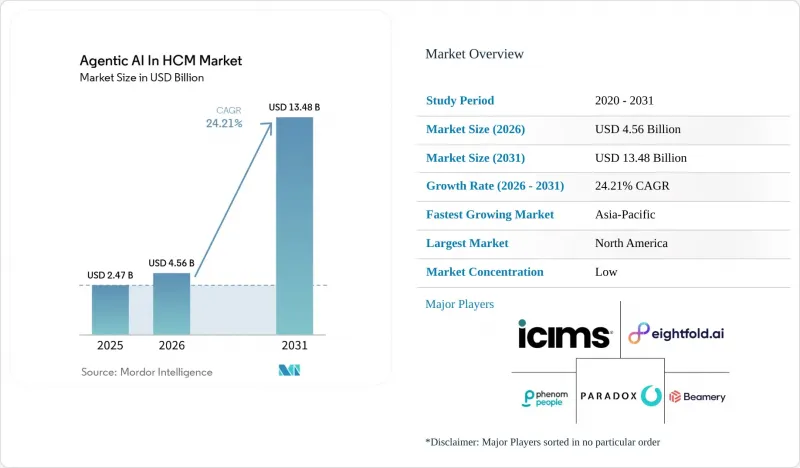

根據 Mordor Intelligence 預測,用於人力資本管理 (HCM) 的智慧體人工智慧 (AI) 市場規模預計將從 2025 年的 24.7 億美元成長到 2026 年的 45.6 億美元,然後從 2026 年到 2031 年以 24.21% 的複合年成長率達到 13.3 億美元。

本報告按組件(例如,智慧體人工智慧平台編配引擎)、功能(例如,招聘/候選人搜尋)、部署模式(例如,基於雲端)、企業規模(例如,大型企業、中小企業)、最終用戶行業(例如,銀行、金融服務和保險、醫療保健/生命科學)以及地區進行細分。市場預測以價值(美元)表示。

全球人力資本管理(HCM)智慧AI市場趨勢及洞察。

高技能工人和現場負責人。

持續的勞動力短缺正在加速人力資本管理(HCM)領域智慧人工智慧(AI)的應用。這是因為人工招募團隊無法跟上當前現場營運和專業所需的招募規模和速度。根據美國就業及勞動力市場調查(JOLTS)的數據,到2025年12月,職位空缺數量將達到740萬個,醫療保健、製造業和物流行業的職位空缺與招聘人數之比仍將高於疫情前水平,這表明招聘壓力將持續存在,而非短期中斷。此外,企業報告顯示,截至2025年2月,美國未填補的職缺佔總勞動力需求的4.5%,而招聘率在2025年12月降至3.3%,為近十年來的最低水平,這表明勞動力供應存在結構性錯配。這種壓力十分顯著,因為現場工作人員在全球勞動力中佔很大比例,即使不考慮生產力下降,每位員工的替代成本仍高達3000至5000美元。 2026年3月,iCIMS報告稱,實施Frontline AI的客戶招募時間縮短了高達75%,每位招募人員的招募人數提高了高達10倍。這凸顯了互動式招募代理商在需要大規模招募的職位類別中的業務效能。成熟經濟體勞動年齡人口的下降進一步加劇了人力資本管理(HCM)機構人工智慧市場的長期需求。這使得更快的招募能力對於確保勞動力的持續性至關重要。

企業面臨壓力,需要在不增加員工的情況下提高負責人和經理的工作效率。

人力資本管理(HCM)領域智慧體人工智慧(AI)市場的發展也受到更嚴格的成本控制的推動。人力資源部門需要在不增加員工的情況下提升績效。波士頓顧問公司(BCG)在2026年2月發布的報告顯示,在特定人力資源工作流程中實施人工智慧的組織,其效率提升了20%至30%。此外,一款基於GPT的經理績效評估工具,將撰寫績效評估的時間減少了45%,評估品質提高了22%,使用者滿意度達到了90%。薪資核算管理也為企業帶來了財務壓力。研究表明,由於工資支付不足,雇主會損失2%至4%的總人事費用,而對於大型企業來說,即使1%的損失也可能高達每年1,500萬美元。 IBM的AskHR計畫證明,透過實施基於標準化工作流程的智慧體支持,人力資源團隊可以透過單一聯繫點集中提供服務。這使得個案解決率達到了94%,並在四年內將人力資源營運成本降低了40%。這種模式的重要性日益凸顯,因為麥肯錫在2025年預測,只有18%的員工人數超過1000人的組織會使用專門的人力資源共享服務中心,這意味著在軟體主導的生產力提升方面存在巨大的流程缺口。因此,用於人力資本管理(HCM)的智慧體人工智慧市場正逐漸與可衡量的勞動效率掛鉤,而非只關注實驗性的自動化預算。

資料隱私、跨境資料傳輸和人工智慧管治的負擔。

由於人力資源 (HR) 決策涉及高度敏感的數據,且通常屬於高風險監管類別,因此合規性仍然是人力資本管理 (HCM) 智慧人工智慧市場面臨的最大障礙。歐盟人工智慧法案((EU) 2024/1689 號條例)於 2024 年 8 月 1 日生效,其附件三將招募篩檢、候選人排名、績效監控和工作分配系統列為高風險類別。該框架強制要求進行適用性評估、保留使用日誌、進行影響評估以及與員工代表進行磋商,所有這些都會增加成本並減緩智慧人工智慧在人力資本管理領域的應用。在英國,資訊專員辦公室 (ICO) 於 2026 年 3 月發出警告,未經真正人工審核的人工智慧招募工具可能違反法律標準,而僅僅獲得形式上的批准並不能被視為有效的監督。 2026 年 1 月的一項調查顯示,77% 的美國高階主管認為資料隱私是其業務在 2025 年第四季面臨的最大風險,高於年初的 53%。這表明,在採購決策中,管治因素的重要性正與功能性因素不相上下。這意味著,人力資本管理(HCM)市場中的自主人工智慧將繼續擴張,但供應商需要更強大的在地化、可審計性和監督能力,才能將需求轉化為實際收入。

細分市場分析

2025年,智慧代理AI平台編配引擎在組件細分市場中佔比36.47%,成為HCM智慧代理AI市場中最大的組件類別。這一主導地位反映出,企業在擴展運作中代理數量之前,優先考慮管治、路由、策略控制和升級邏輯。這些平台為買家提供了一種方法,可以分解任務、實施人工查核點,並在招聘、人力資源服務、薪資核算和調動工作流程中管理身分。這項基礎至關重要,因為2025年和2026年的許多部署都優先考慮降低執行風險,而不是最大化代理數量。因此,組件構成比表明,在HCM智慧代理AI市場廣泛擴展用例之前,人們對基礎設施的信心已經建立起來。

預計從2026年到2031年,人工智慧代理工作流程應用將以27.39%的複合年成長率成長,成為成長最快的組件細分市場。這一階段標誌著人力資本管理(HCM)代理人工智慧市場進入下一個發展階段。在2024年和2025年建立了編配能力的公司,現在正透過專門處理面試、政策導航、薪資核算異常處理和內部調動等任務的代理來增強這些能力。 2026年2月的一項調查發現,使用人工智慧的招聘機構比同行更有可能取得更好的業績,其中55%的機構表示,透過人工智慧篩檢,關鍵績效指標(KPI)提高了25%或更多,46%的機構表示,篩檢時間縮短了50%或更多。由於大規模多系統部署仍需要實施支援、工作流程重新設計和持續調整,因此服務仍發揮著至關重要的作用。隨著越來越多的企業希望在不建構複雜的內部人工智慧營運團隊的情況下,也能從代理人工智慧中獲益,託管人工智慧服務在人力資本管理產業也越來越受歡迎。這揭示了組件結構中的一個清晰模式:平台建立控制,應用程式驅動擴展,服務支援長尾部署的複雜性。

到了2025年,人才規劃與分析佔22.83%的市場佔有率,成為人力資本管理(HCM)智慧人工智慧市場中最大的功能細分領域。這一地位反映了在充滿挑戰的招募環境和不斷變化的技能需求下,即時勞動力分配、預算透明度和情境規劃的迫切需求。 HCM智慧人工智慧在這一功能領域受益於高階主管對能夠將人才決策與財務績效更直接連結的工具的需求。僅有12%的美國人力資源領導者以三年或更長的長期視角進行人才規劃,而73%的領導者仍只專注於營運規劃。人工智慧驅動的人才規劃於2026年推出,滿足了對以分析為中心的自動化日益成長的需求,並將人員配置和勞動力決策與企業資源計劃(ERP)和臨時員工數據整合起來。事實上,這項功能已經從一個簡單的報表外掛發展成為HCM智慧人工智慧的指揮中心。

預計從2026年到2031年,人才管理和內部調動將以25.41%的複合年成長率成長,成為成長最快的職能。這一成長表明,用於人力資本管理(HCM)的智慧人工智慧(AI)的應用範圍已不再局限於簡化外部招聘,而是朝著人才重新部署和保留的目標邁進。招募和候選人搜尋仍然是AI應用的主要領域,尤其是在速度和申請完成率至關重要的現場崗位。到2025年,互動式ATS的實施將使平均申請完成率達到72%,平均招募週期縮短至3.5天,候選人滿意度達到95%。員工服務和人力資源營運也透過提高個案完成率而得到改善,但由於對錯誤的接受度較低,薪資核算和考勤管理仍然受到嚴格控制。從整個HCM智慧人工智慧產業來看,其功能架構表明,買家正在將支出從以效率為中心的流程轉向在員工隊伍中創造價值。

區域分析

到2025年,北美將佔據全球人力資本管理(HCM)智慧人工智慧市場39.73%的佔有率,成為領先的區域叢集。美國憑藉著成熟的HCM軟體生態系統、企業廣泛採用雲端技術以及對大規模人工智慧專案的大力投資,確立了這一地位。截至2025年2月,美國職缺率達到總勞動力需求的4.5%,這持續對招募效率構成壓力,並推動了對人工智慧主導的候選人發現和篩選的需求。截至2026年1月,受人工智慧代理的影響,64%的美國公司改變了招募應屆畢業生的方式,高於上一季的18%,顯示人工智慧驅動的招募實踐正在迅速普及。該地區在採購標準制定方面也取得了進展,採購方不再將合規性視為次要因素,而是將管治、可解釋性和投資回報率作為一個整體進行評估。

明確的企業承諾正在推動北美主導地位。 2026年3月,Adecco SA)與銷售團隊簽署了一份名為“Agentforce 360”的多年期無限期契約,目標是在2026年底前,使其遍布60多個國家/地區的27,000名負責人中超過50%的人啟用智慧代理AI,並使AI為其超過50%的收入提供支持。在英國進行的初步試點計畫已顯示,招募時間縮短了15%。同時,隨著美國各州就業AI法規的不斷完善,北美人力資本管理(HCM)領域智慧代理AI的市場佔有率將越來越取決於供應商在通知、影響評估和反歧視措施方面的準備情況。加拿大雖然規模較小,但隨著中小企業在招募領域的應用不斷推進,也取得了穩定進展。墨西哥也擁有更廣泛的區域機遇,但其企業應用的深度仍低於美國。

歐洲仍是人力資本管理(HCM)領域智慧人工智慧的第二大市場,但其管治環境最為嚴格。儘管歐洲的採用速度通常較慢,但由於歐盟《人工智慧法案》提高了招募、績效評估和人員配置系統的最低合規標準,其管治品質更高。英國則另闢蹊徑;2026年3月,英國資訊專員辦公室(ICO)表示,人工智慧驅動的招募決策仍需真正的人工監督,而非僅憑形式批准而缺乏干預。此外,歐洲存在顯著的技能缺口,僅21%的歐洲員工接受過生成式人工智慧培訓,而美國這一比例為45%,凸顯了持續投資人力資源人工智慧工具以提高生產力的必要性。預計亞太地區在2026年至2031年間的複合年成長率將達到29.11%,成為人力資本管理領域智慧人工智慧市場成長最快的區域市場。在東南亞,人力資源人工智慧和預算規劃的日益普及推動了市場成長;而在印度、日本和中國,勞動力短缺、技術投資和企業現代化等多種因素共同驅動著市場需求,但驅動方式各有不同。南美和中東及非洲市場仍處於起步階段,但大規模。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高技能和體力勞動者的招募面臨日益嚴重的勞動力短缺問題。

- 對隨時可用的員工自助服務以及不斷變化的人力資源事務的需求。

- 基於技能的人員選拔和內部調動

- 企業面臨壓力,需要在不增加員工的情況下提高負責人和經理的工作效率。

- 需要協調分散的 ATS、HRIS、服務台和協作系統之間的操作。

- 代理管治層的出現使得對多代理人力資源自動化進行稽核成為可能。

- 市場限制因素

- 資料隱私、跨境資料傳輸和人工智慧管治的負擔。

- 整合傳統 HCM、薪資核算和身分管理系統的複雜性。

- 員工代表委員會和勞資關係部反抗人力資源部的任意決定

- 流程標準化不足限制了中型企業部署中代理商的可靠性。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 按組件

- 智慧體人工智慧平台編配引擎

- AI代理工作流程應用程式

- 專業服務

- 託管人工智慧服務

- 按功能

- 招募和候選人搜尋

- 員工服務和人力資源運營

- 人力資源管理與內部調動

- 學習與發展

- 人力資源規劃與分析

- 薪資和考勤管理

- 透過部署方法

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- IT/通訊

- 零售與電子商務

- 工業/製造業

- 政府/公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Phenom People, Inc.

- Eightfold AI Inc.

- iCIMS, Inc.

- Paradox, Inc.

- Beamery Inc.

- Gloat Ltd.

- HireVue, Inc.

- Findem, Inc.

- Harver BV

- Personio SE & Co. KG

- Degree, Inc. d/b/a Lattice

- Darwinbox Digital Solutions Private Limited

- Textio, Inc.

- Peoplebox Inc.

- Peoplelogic, Inc.

- Humaans Software UK LTD

- Wisq Inc.

- Visier, Inc.

- VIVAHR, LLC d/b/a AvaHR

- Jobs and Talent, SL

第7章 市場機會與未來展望

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高技能和體力勞動者的招募面臨日益嚴重的勞動力短缺問題。

- 對隨時可用的員工自助服務以及不斷變化的人力資源事務的需求。

- 基於技能的人員選拔和內部調動

- 企業面臨壓力,需要在不增加員工的情況下提高負責人和經理的工作效率。

- 需要協調分散的 ATS、HRIS、服務台和協作系統之間的操作。

- 代理管治層的出現使得對多代理人力資源自動化進行稽核成為可能。

- 市場限制因素

- 資料隱私、跨境資料傳輸和人工智慧管治的負擔。

- 整合傳統 HCM、薪資核算和身分管理系統的複雜性。

- 員工代表委員會和勞資關係部反抗人力資源部的任意決定

- 流程標準化不足限制了中型企業部署中代理商的可靠性。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 按組件

- 智慧體人工智慧平台編配引擎

- AI代理工作流程應用程式

- 專業服務

- 託管人工智慧服務

- 按功能

- 招募和候選人搜尋

- 員工服務和人力資源運營

- 人力資源管理與內部調動

- 學習與發展

- 人力資源規劃與分析

- 薪資和考勤管理

- 透過部署方法

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- IT/通訊

- 零售與電子商務

- 工業/製造業

- 政府/公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Phenom People, Inc.

- Eightfold AI Inc.

- iCIMS, Inc.

- Paradox, Inc.

- Beamery Inc.

- Gloat Ltd.

- HireVue, Inc.

- Findem, Inc.

- Harver BV

- Personio SE & Co. KG

- Degree, Inc. d/b/a Lattice

- Darwinbox Digital Solutions Private Limited

- Textio, Inc.

- Peoplebox Inc.

- Peoplelogic, Inc.

- Humaans Software UK LTD

- Wisq Inc.

- Visier, Inc.

- VIVAHR, LLC d/b/a AvaHR

- Jobs and Talent, SL

第7章 市場機會與未來展望

According to Mordor Intelligence, the agentic AI in the HCM market size is expected to grow from USD 2.47 billion in 2025 to USD 4.56 billion in 2026 and is forecast to reach USD 13.48 billion by 2031 at 24.21% CAGR over 2026-2031.

This report is Segmented by Component (Agentic AI Platforms and Orchestration Engines, and More), Function (Recruiting and Candidate Sourcing, More), Deployment Model (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In HCM Market Trends and Insights

Rising Labor Scarcity in High-Skill and Frontline Hiring

Persistent labor scarcity is pushing the agentic AI in the HCM market toward faster adoption because manual recruiting teams cannot keep pace with the volume and speed now required across frontline and specialized roles. U.S. JOLTS data showed 7.4 million job openings in December 2025, with openings-to-hire ratios in healthcare, manufacturing, and logistics still above pre-pandemic norms, signaling sustained hiring pressure rather than a short-term disruption. Companies also reported that unfilled U.S. vacancies stood at 4.5% of total labor demand in February 2025, while the hiring rate fell to a decade-low of 3.3% in December 2025, pointing to a structural mismatch in labor supply. This pressure matters because frontline employees account for a large share of the global workforce, and replacement costs per worker still range from USD 3,000 to USD 5,000 before productivity losses are counted. iCIMS reported in March 2026 that customers using Frontline AI achieved up to 75% lower time-to-fill and up to 10 times more hires per recruiter, which strengthens the business case for conversational sourcing agents in high-volume roles. The longer-term pull on the agentic AI in the HCM market is reinforced by demographic decline in working-age populations across mature economies, which makes faster hiring capacity more important to workforce continuity.

Enterprise Pressure to Lift Recruiter and Manager Productivity Without Adding Headcount

The agentic AI in the HCM market is also being driven by tighter cost discipline, since HR teams are being asked to improve output without expanding headcount. BCG reported in February 2026 that organizations applying AI in targeted HR workflows recorded 20-30% efficiency gains, and a GPT-based manager review tool cut review-writing time by 45% while improving review quality by 22% with 90% user satisfaction. Payroll administration places the same pressure on finances, with research indicating that employers lose 2-4% of total labor spend to payroll leakage, and that even a 1% loss can equal USD 15 million annually for a large employer. IBM's AskHR program showed that when agentic support is built on standardized workflows, HR teams can centralize service through a single entry point while reaching a 94% containment rate and cutting HR operating costs by 40% over 4 years. That model matters because McKinsey found in 2025 that only 18% of organizations with more than 1,000 employees used specialized HR shared services centers, leaving a significant process gap for software-led productivity gains. As a result, the agentic AI in the HCM market is increasingly tied to measurable labor efficiency rather than experimental automation budgets.

Data Privacy, Cross-Border Data Transfer, And AI Governance Burden

Compliance remains the clearest drag on the agentic AI in the HCM market because HR decisions touch highly sensitive data and often fall into higher-risk regulatory categories. The EU AI Act, Regulation (EU) 2024/1689, entered into force on August 1, 2024, and classified recruitment screening, candidate ranking, performance monitoring, and task allocation systems as high risk under Annex III. The framework requires conformity assessments, use-log retention, impact reviews, and worker-representative consultation, which increase costs and slow deployment of agentic AI in the HCM market. In the United Kingdom, the Information Commissioner's Office said in March 2026 that AI hiring tools without genuine human review can breach legal standards, and it warned that simple rubber-stamping does not qualify as meaningful oversight. Research in January 2026 showed that 77% of U.S. leaders cited data privacy as a top enterprise risk in the fourth quarter of 2025, up from 53% at the start of the year, which shows how governance concerns now shape buying criteria as much as functionality. This means the agentic AI in the HCM market will continue to expand, but vendors will need stronger localization, auditability, and oversight features to convert demand into deployed revenue.

Other drivers and restraints analyzed in the detailed report include:

- Demand for Always-on Employee Self-service and HR Case Deflection

- Shift Toward Skills-Based Talent Decisions and Internal Mobility

- Integration Complexity Across Legacy HCM, Payroll, And Identity Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agentic AI platforms and orchestration engines accounted for 36.47% of the component segment in 2025, making them the largest component category in the agentic AI in HCM market. This leadership reflected the enterprise's preference to secure governance, routing, policy control, and escalation logic before expanding the number of live agents. These platforms gave buyers a way to manage task decomposition, human checkpoints, and identity control across recruiting, HR service, payroll, and mobility workflows. That foundation mattered because many deployments in 2025 and 2026 focused first on reducing execution risk rather than maximizing agent volume. The component mix, therefore, showed that infrastructure confidence came before broader expansion of use cases in the agentic AI market in the HCM market.

AI agents and workflow applications are projected to grow at a 27.39% CAGR from 2026 to 2031, making them the fastest-growing component segment. This phase marks the next step for agentic AI in the HCM market, where enterprises that built orchestration capacity in 2024 and 2025 are now filling it with task-specific agents for interviewing, policy navigation, payroll exception review, and internal mobility. Research in February 2026 showed that staffing firms using AI were 4 times more likely to outperform peers, while 55% said AI screening improved KPIs by more than 25%, and 46% achieved a 50% or greater reduction in screening time. Services remain relevant because large, multi-system deployments still require implementation support, workflow redesign, and ongoing tuning. Managed AI services are also gaining traction, as buyers want the benefits of agentic AI in the HCM industry without building deep internal AI operations teams. This leaves the component structure with a clear pattern where platforms establish control, applications drive scaling, and services support long-tail deployment complexity.

Workforce planning and analytics accounted for 22.83% of the market in 2025, making it the largest functional segment in the agentic AI HCM market. That position reflected the need for real-time labor allocation, budget visibility, and scenario planning amid tight hiring conditions and changing skill demand. The agentic AI in the HCM market size in this function benefited from executive demand for tools that connect workforce decisions more directly to financial outcomes. Only 12% of U.S. HR leaders engaged in workforce planning with a 3-year or longer horizon, while 73% remained focused solely on operational planning. AI-driven workforce planning launched in 2026 to link headcount and labor decisions to ERP and contingent workforce data, supporting stronger demand for analytics-centered automation. In practice, this function became the control room for the agentic AI in the HCM market rather than a reporting add-on.

Talent management and internal mobility are projected to expand at 25.41% CAGR from 2026 to 2031, making it the fastest-growing function. This rise shows that the agentic AI in the HCM market is moving closer to workforce redeployment and retention goals, rather than just external hiring efficiency. Recruiting and candidate sourcing still account for a large share of the deployment volume, especially in frontline roles where speed and application completion matter. Conversational ATS deployments delivered a 72% average application completion rate, 3.5-day average time-to-hire, and 95% candidate satisfaction rating in 2025. Employee service and HR operations are also improving through higher case containment, while payroll and time administration remain more tightly controlled due to a low tolerance for error. Across the agentic AI in the HCM industry, the function mix shows that buyers are broadening spend from efficiency-led workflows toward workforce value creation.

Geography Analysis

North America held a 39.73% share of the global agentic AI market in the HCM market in 2025, making it the leading regional cluster. The United States anchored this position through a mature HCM software ecosystem, deep enterprise cloud adoption, and a stronger willingness to fund AI programs at scale. Unfilled U.S. job vacancies stood at 4.5% of total labor demand in February 2025, which continued to put pressure on hiring efficiency and supported demand for AI-led sourcing and screening. In January 2026, 64% of U.S. organizations had changed their approach to entry-level hiring due to AI agent influence, up from 18% in the prior quarter, signaling rapid normalization of AI-assisted recruiting practices. The region is also defining procurement standards because buyers now evaluate governance, explainability, and ROI together rather than treating compliance as a later-stage issue.

Visible enterprise commitments support the North American lead. In March 2026, Adecco Group signed an unlimited, multi-year Agentforce 360 agreement with Salesforce to power more than 50% of revenues with agentic AI across 27,000 recruiters in more than 60 countries by the end of 2026. Early United Kingdom pilots had already produced 15% time savings. At the same time, state-level employment AI rules in the United States are expanding, which means the agentic AI in the HCM market share gained in North America will increasingly depend on vendor readiness for notification, impact review, and anti-discrimination controls. Canada remains smaller in scale, but it is moving steadily as SME hiring adoption improves. Mexico is also part of the broader regional opportunity, though enterprise depth remains lower than in the United States.

Europe remained the second-largest region in the agentic AI in the HCM market, but it operates under the most demanding governance conditions. The EU AI Act has raised the compliance floor across recruitment, performance, and workforce allocation systems, meaning deployment speed is often slower, but governance quality is higher. The United Kingdom is moving on its own track, and in March 2026, the Information Commissioner's Office said that AI-supported hiring decisions still require genuine human oversight rather than formal approval without the authority to intervene. Europe also shows a significant skills gap, with only 21% of European employees having received generative AI training, compared with 45% in the United States, underscoring the need for continued investment in productivity-oriented HR AI tools. Asia-Pacific is projected to grow at a 29.11% CAGR from 2026 to 2031, making it the fastest-growing regional segment of the agentic AI in the HCM market. Southeast Asia is strengthening through higher HR AI usage and budget intent, while India, Japan, and China each add demand through different combinations of labor pressure, technology investment, and enterprise modernization. South America, the Middle East, and Africa remain early-stage opportunities, but large enterprise bases, cloud HCM modernization, and national digital programs are gradually expanding the addressable base for agentic AI in the HCM market.

- Phenom People, Inc.

- Eightfold AI Inc.

- iCIMS, Inc.

- Paradox, Inc.

- Beamery Inc.

- Gloat Ltd.

- HireVue, Inc.

- Findem, Inc.

- Harver B.V.

- Personio SE & Co. KG

- Degree, Inc. d/b/a Lattice

- Darwinbox Digital Solutions Private Limited

- Textio, Inc.

- Peoplebox Inc.

- Peoplelogic, Inc.

- Humaans Software UK LTD

- Wisq Inc.

- Visier, Inc.

- VIVAHR, LLC d/b/a AvaHR

- Jobs and Talent, S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Labor Scarcity in High-skill and Frontline Hiring

- 4.2.2 Demand for Always-on Employee Self-service and HR Case Deflection

- 4.2.3 Shift Toward Skills-Based Talent Decisions and Internal Mobility

- 4.2.4 Enterprise Pressure to Lift Recruiter and Manager Productivity Without Adding Headcount

- 4.2.5 Need to Orchestrate Work Across Fragmented ATS, HRIS, Helpdesk, and Collaboration Stacks

- 4.2.6 Emergence of Agent Governance Layers That Make Multi-agent HR Automation Auditable

- 4.3 Market Restraints

- 4.3.1 Data Privacy, Cross-border Data Transfer, and AI Governance Burden

- 4.3.2 Integration Complexity Across Legacy HCM, Payroll, and Identity Systems

- 4.3.3 Works Council and Employee Relations Pushback Against Autonomous HR Decisions

- 4.3.4 Weak Process Standardization That Limits Agent Reliability in Mid-market Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Agentic AI Platforms and Orchestration Engines

- 5.1.2 AI Agents and Workflow Applications

- 5.1.3 Professional Services

- 5.1.4 Managed AI Services

- 5.2 By Function

- 5.2.1 Recruiting and Candidate Sourcing

- 5.2.2 Employee Service and HR Operations

- 5.2.3 Talent Management and Internal Mobility

- 5.2.4 Learning and Development

- 5.2.5 Workforce Planning and Analytics

- 5.2.6 Payroll and Time Administration

- 5.3 By Deployment Model

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By End User Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Phenom People, Inc.

- 6.4.2 Eightfold AI Inc.

- 6.4.3 iCIMS, Inc.

- 6.4.4 Paradox, Inc.

- 6.4.5 Beamery Inc.

- 6.4.6 Gloat Ltd.

- 6.4.7 HireVue, Inc.

- 6.4.8 Findem, Inc.

- 6.4.9 Harver B.V.

- 6.4.10 Personio SE & Co. KG

- 6.4.11 Degree, Inc. d/b/a Lattice

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Textio, Inc.

- 6.4.14 Peoplebox Inc.

- 6.4.15 Peoplelogic, Inc.

- 6.4.16 Humaans Software UK LTD

- 6.4.17 Wisq Inc.

- 6.4.18 Visier, Inc.

- 6.4.19 VIVAHR, LLC d/b/a AvaHR

- 6.4.20 Jobs and Talent, S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中國人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)