|

市場調查報告書

商品編碼

2063973

南美洲HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)South America HCM Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

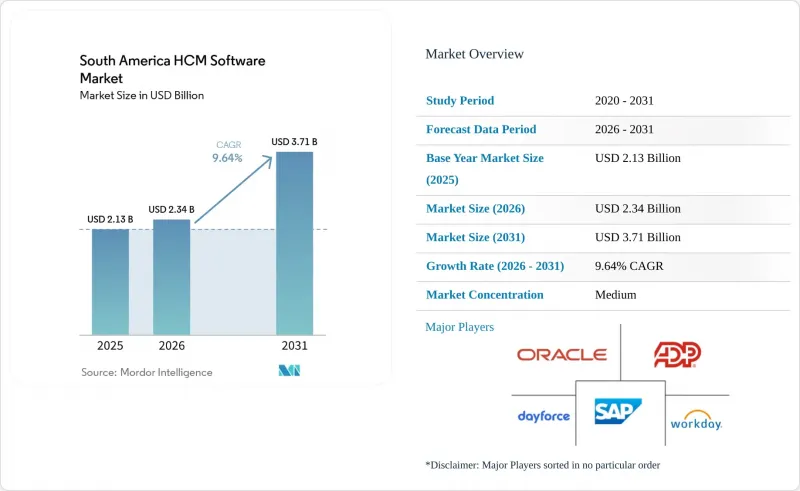

據 Mordor Intelligence 稱,2025 年南美洲人力資源管理 (HCM) 軟體市場價值為 21.3 億美元,預計到 2031 年將從 2026 年的 23.4 億美元成長至 37.1 億美元,預測期(2026-2031 年)的複合成長率為 9.64%。

本報告按元件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、應用程式(核心人力資源、人才管理、人力資源管理、薪資管理等)以及最終用戶產業(IT和電信、銀行、金融服務和保險等)進行細分。市場預測以美元計價。

南美洲HCM軟體市場趨勢與洞察

中型企業對基於雲端的HCM套件的採用率不斷提高

中型企業遷移到雲端並非僅僅為了降低成本,而是因為季度合規要求已成為本地團隊的沉重負擔。 Oracle 於 2024 年 3 月推出的 HCM Now 將員工人數在 500 至 2,000 人之間的企業的實施週期縮短至六個月。在智利,15 天的 REL 提交週期消除了批量Oracle薪資核算,即時同步也從一項便利功能轉變為必需功能。因此,雲端市場的成長率比整個南美 HCM 軟體市場的成長率高出 166 個基點。供應商現在能夠獲得以前流向本地系統整合商的經常性收入。這一趨勢正在增強供應商的定價權,預計到 2028 年將重塑中型企業市場的談判格局。

勞動法合規要求日益提高和社會數位化。

巴西強制性電子僱傭協議(DET)要求在僱用後24小時內提交電子契約,迫使企業依賴具有自動化工作流程的平台。阿根廷第27.802號法律規定,自2026年3月起,根據《阿根廷薪資改革法案》(ARCA),必須實施集中式薪資核算管理,這需要對分散式系統無法處理的現有系統進行徹底改造。智利的《公平薪酬法案》(REL)對逾期提交薪資單的行為處以罰款,使得雲端原生架構成為唯一可行的選擇。此外,巴西第14.611/2023號法律規定的平行同工同酬分析要求使用傳統資料庫不支援的儀錶板。這些法規的疊加效應,正將合規性審查從定期審計轉向持續監控,加速淘汰本地部署環境。

傳統ERP環境的初始整合成本較高

自90年代以來一直使用SAP或Oracle ERP系統的製造商,如今面臨著長達18至24個月的整合挑戰,其預算甚至可能超出授權費用高達300%。雖然中介軟體可以解決技術映射問題,但重建幾十年前的工作流程卻會大幅增加專案規模。財務長們對雲端HCM的投資回報率持懷疑態度,這為現有ERP供應商提供了以折扣價交叉銷售原生HCM的機會。除非獨立供應商投資開發現成的連接器,否則他們在南美大型企業HCM軟體市場的潛在佔有率可能會停滯不前。

細分市場分析

隨著企業加大對整合、客製化和變更管理的投入,預計到2031年,業務收益將以10.82%的複合年成長率成長。儘管軟體在2025年佔據了南美人力資本管理(HCM)軟體市場71.32%的佔有率,但實施過程中日益增多的阻力正促使總體擁有成本(TCO)轉移到服務合約。因此,擁有內部專業服務部門的供應商可以確保穩定的利潤率,而依賴合作夥伴的純軟體公司可能被迫放棄對交易的主導。

隨著中型企業日益需要支援以適應快速變化的薪資核算法規,南美洲人力資本管理 (HCM) 軟體市場的服務領域正在擴張。同時,隨著分析模組的日趨成熟,大型企業也為運作後的最佳化分配更多預算。南美 HCM 軟體市場支出模式的這些轉變,導致服務領域的成長率與整體市場的平均成長率之間持續存在差距。

預計到2025年,雲端技術將佔南美人力資本管理(HCM)軟體市場64.18%的佔有率,複合年成長率(CAGR)為11.24%,比本地部署和混合解決方案快200多個基點。巴西的DET和阿根廷的ARCA強制要求即時提交數據,使得本地部署工具常用的批量上傳方式過時。混合解決方案仍然是確保薪資資料自主權的過渡方案,但其擴展速度緩慢,因為企業一旦管理架構成熟,最終都會遷移整個系統。

預計在2031年之前,基於雲端的人力資源管理 (HCM) 軟體的市場佔有率將顯著成長。這主要得益於供應商提供的更新服務,該服務能夠幫助企業快速適應不同地區頻繁變化的薪資、稅務和勞動法規。此外,該模式也因其初始基礎設施要求低、引進週期短以及易於隨著業務成長而擴展等優點而日益受到歡迎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中型企業對基於雲端的HCM套件的採用率不斷提高

- 勞動法合規要求日益提高和社會數位化。

- 遠距辦公和混合辦公人員的增加,對數位化人力資源工具提出了更高的要求。

- 零工經濟的擴張正在加速對彈性勞動力管理平台的需求。

- 利用人工智慧分析提高人才招聘效率

- 在南美國家推行薪資和稅務模組本地化,以吸引中小企業

- 市場限制因素

- 傳統ERP環境的初始整合成本較高

- 跨境雲端託管法規中的資料隱私問題

- 區域城市缺乏實施人力資源技術的專業知識

- 由於經濟波動,非核心項目的IT預算正在削減。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 透過使用

- 核心人力資源

- 人才管理

- 勞動力管理

- 薪資管理

- 學習與發展

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Workday, Inc.

- Dayforce, Inc.

- Automatic Data Processing, Inc.

- Oracle Corporation

- SAP SE

- Cornerstone OnDemand, Inc.

- Ultimate Kronos Group Inc.

- Paycom Software, Inc.

- YourPeople Inc.

- The Sage Group plc

- Rippling People Center Inc.

- Darwinbox Digital Solutions Private Limited

- Odoo SA

- Ramco Systems Limited

- Meta4 Spain SAU

- Cegid Group SA

- Neeyamo Enterprise Solutions Private Limited

- Deel Inc.

- HiBob Ltd.

- Factorial HR, SL

- Visma AS

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america hCM software market size was valued at USD 2.13 billion in 2025 and estimated to grow from USD 2.34 billion in 2026 to reach USD 3.71 billion by 2031, at a CAGR of 9.64% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR, Talent Management, Workforce Management, Payroll Management, and More), End-User Industry (IT and Telecommunications, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

South America HCM Software Market Trends and Insights

Rising Adoption of Cloud-Based HCM Suites Among Mid-Sized Firms

Mid-sized companies are shifting to the cloud because quarterly compliance patches overwhelm on-premise teams, not because of headline cost savings. Oracle's HCM Now rollout in March 2024 cut implementation to six months for firms with 500-2,000 workers. Chile's 15-day REL filing cycle eliminated batch payroll, converting real-time synchronization from a convenience to a requirement. As a result, cloud growth outpaces the South America HCM software market by 166 basis points. Vendors now secure recurring revenue that once drifted to local system integrators. The trend consolidates pricing power and is expected to reshape mid-market negotiations by 2028.

Increasing Regulatory Compliance Demands for Labor Laws Digitization

Brazil's DET mandate obliges electronic contract submission within 24 hours of hiring, locking enterprises into platforms with automated workflows. Argentina's Law 27.802 centralizes payroll under ARCA starting March 2026, forcing engine overhauls that decentralized systems cannot meet. Chile's REL fines for late filings make cloud-native architecture the only viable option. Parallel equal-pay analytics under Brazil's Law 14.611/2023 require dashboards that legacy databases do not support. Together, these statutes convert compliance from periodic audits to always-on monitoring and accelerate retirement of on-premise deployments.

High Initial Integration Costs for Legacy ERP Environments

Manufacturers running SAP or Oracle ERP from the 1990s face 18-24-month integrations with budgets that exceed license spend by up to 300%. Middleware solves technical mapping issues, yet re-engineering decades-old workflows strains the project's scope. CFOs view cloud HCM ROI skeptically, opening doors for incumbent ERP vendors to cross-sell native HCM at a discount. Unless standalone vendors invest in ready connectors, their addressable share of the South America HCM software market may plateau among large enterprises.

Other drivers and restraints analyzed in the detailed report include:

- Growing Remote and Hybrid Workforces Necessitating Digital HR Tools

- AI-Driven Analytics Enhancing Talent Acquisition Efficiency

- Data Privacy Concerns Amidst Cross-Border Cloud Hosting Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to rise at a 10.82% CAGR to 2031, as enterprises pay for integration, customization, and change management. In 2025, software contributed 71.32% of the South America HCM software market, yet mounting deployment friction suggests total cost of ownership is shifting toward services contracts. Vendors with in-house professional services thus gain margin resilience, whereas pure-play software firms reliant on partners may concede deal control.

The South America HCM software market for services is expanding as mid-sized buyers require guided configuration to meet rapidly changing payroll regulations. Meanwhile, larger enterprises allocate incremental budgets to post-go-live optimization as analytics modules mature. This spending evolution in the South America HCM software market underpins the sustained gap between services growth and overall market averages.

Cloud held 64.18% of the South America HCM software market in 2025 and is forecast to grow at a 11.24% CAGR, outstripping on-premises and hybrid solutions by more than 200 basis points. Brazil's DET and Argentina's ARCA compel real-time submission, invalidating batch uploads typical of on-premise tools. Hybrid remains a transitional choice for payroll data sovereignty, but its expansion lags because firms eventually migrate entire stacks once controls mature.

Cloud's share of the South America HCM software market is expected to grow substantially well before 2031, supported by vendor-managed updates that help organizations quickly adapt to frequent payroll, tax, and labor compliance changes across regional jurisdictions. The model is also gaining traction due to lower upfront infrastructure requirements, faster deployment cycles, and easier scalability for expanding enterprises.

List of Companies Covered in this Report:

- Workday, Inc.

- Dayforce, Inc.

- Automatic Data Processing, Inc.

- Oracle Corporation

- SAP SE

- Cornerstone OnDemand, Inc.

- Ultimate Kronos Group Inc.

- Paycom Software, Inc.

- YourPeople Inc.

- The Sage Group plc

- Rippling People Center Inc.

- Darwinbox Digital Solutions Private Limited

- Odoo SA

- Ramco Systems Limited

- Meta4 Spain S.A.U.

- Cegid Group SA

- Neeyamo Enterprise Solutions Private Limited

- Deel Inc.

- HiBob Ltd.

- Factorial HR, S.L.

- Visma AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Cloud-Based HCM Suites Among Mid-Sized Firms

- 4.2.2 Increasing Regulatory Compliance Demands for Labor Laws Digitization

- 4.2.3 Growing Remote and Hybrid Workforces Necessitating Digital HR Tools

- 4.2.4 Expansion of Gig Economy Accelerating Demand for Flexible Workforce Management Platforms

- 4.2.5 AI-Driven Analytics Enhancing Talent Acquisition Efficiency

- 4.2.6 Localization of Payroll and Tax Modules for South American Jurisdictions Attracting SMEs

- 4.3 Market Restraints

- 4.3.1 High Initial Integration Costs for Legacy ERP Environments

- 4.3.2 Data Privacy Concerns Amidst Cross-Border Cloud Hosting Regulations

- 4.3.3 Shortage of HR Tech Implementation Expertise in Secondary Cities

- 4.3.4 Economic Volatility Reducing IT Budgets for Non-Core Projects

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Core HR

- 5.4.2 Talent Management

- 5.4.3 Workforce Management

- 5.4.4 Payroll Management

- 5.4.5 Learning and Development

- 5.5 By End-User Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 BFSI

- 5.5.3 Industrial Manufacturing

- 5.5.4 Healthcare and Lifesciences

- 5.5.5 Retail and E-commerce

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geogrpahy

- 5.6.1 Brazil

- 5.6.2 Argentina

- 5.6.3 Colombia

- 5.6.4 Chile

- 5.6.5 Peru

- 5.6.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 Dayforce, Inc.

- 6.4.3 Automatic Data Processing, Inc.

- 6.4.4 Oracle Corporation

- 6.4.5 SAP SE

- 6.4.6 Cornerstone OnDemand, Inc.

- 6.4.7 Ultimate Kronos Group Inc.

- 6.4.8 Paycom Software, Inc.

- 6.4.9 YourPeople Inc.

- 6.4.10 The Sage Group plc

- 6.4.11 Rippling People Center Inc.

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Odoo SA

- 6.4.14 Ramco Systems Limited

- 6.4.15 Meta4 Spain S.A.U.

- 6.4.16 Cegid Group SA

- 6.4.17 Neeyamo Enterprise Solutions Private Limited

- 6.4.18 Deel Inc.

- 6.4.19 HiBob Ltd.

- 6.4.20 Factorial HR, S.L.

- 6.4.21 Visma AS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

北美HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)日本HCM軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)政府和公共部門人力資本管理軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)製造業人力資本管理軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)IT和電信行業HCM軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)零售業人力資本管理軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測

中型企業人力資本管理 (HCM) 軟體市場:按解決方案、部署類型、組織規模和產業分類 - 2026-2032 年全球預測