|

市場調查報告書

商品編碼

2072785

越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

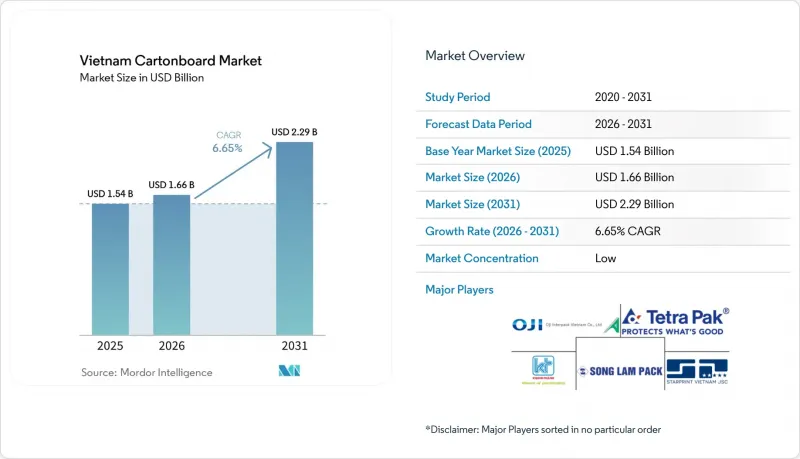

據 Mordor Intelligence 稱,越南紙板市場在 2025 年的價值為 15.4 億美元,預計到 2031 年將達到 22.9 億美元,而 2026 年為 16.6 億美元,預測期(2026-2031 年)的複合年成長率為 6.65%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草、化妝品等)進行細分。市場預測以美元計價。

越南紙板市場趨勢與洞察

加工食品和飲料消費量增加

預計到2025年,越南食品飲料產業的市場規模將達到726.5兆越南盾(約279.4億美元),到2026年將達到760兆越南盾(約292.3億美元)。這將維持對牛奶紙盒、乾貨紙盒、冷凍食品包裝和其他二次加工紙板產品的廣泛需求。這一消費趨勢對越南紙板市場意義重大,因為它同時支撐了多種瓦楞紙板等級的需求,而非僅依賴單一的終端用戶產業。隨著家庭消費越來越傾向於購買包裝品牌食品,在現代零售和餐飲通路中,標籤、運輸保護和標籤檢視展示等因素帶來的重複需求,使加工商受益匪淺。這種需求趨勢也使供應商受益,他們可以處理飲料、乳製品、冷凍食品和乾貨等不同品類的訂單,而無需等待過長的前置作業時間或擔心印刷品質的波動。因此,折疊紙盒、食品包裝和液體紙板產品的訂單變得更加穩定,即使低附加價值的通用包裝形式繼續面臨價格壓力,越南紙板市場也能夠保持成長。

擴大電子商務和零售包裝範圍

預計2025年,越南電子商務市場交易總額(GMV)將達到458.16兆越南盾(約165.8億美元),2026年第一季銷售額將達134.6兆越南盾(約51.9億美元),較去年同期成長32.74%。此外,根據越南工貿部數位經濟平台的數據,越南電子商務市場2026年的目標規模為370億美元,顯示消費者對直接配送和品牌包裝的需求將持續成長。這項轉變將推動越南紙板市場的發展,因為包裝材料不僅需要在運輸過程中保護貨物,還需要確保貨物到達買家或零售商後即可直接展示。隨著小批量生產、圖案多樣化和產品更新周期縮短等趨勢的日益普遍,擁有數位印刷和UV膠印能力的加工商的地位也因此得到鞏固。此外,價值主張已從簡單的運輸包裝轉變為可折疊的瓦楞紙箱,並採用膠印貼合加工和更高質量的表面處理,從而在越南紙板市場形成了穩健的收入結構,而這僅憑銷量成長是無法預測的。

再生纖維價格波動和對進口的依賴

由於越南已禁止進口混合紙,舊瓦楞紙板箱仍是主要的進口再生纖維原料,這使得越南國內造紙廠極易受到國際貿易波動和再生纖維價格波動的影響。美國再生紙價格已從2020年的每噸167美元上漲至2024年的每噸204美元,顯示投入成本的波動會迅速波及整個供應鏈,之後才會趨於穩定。這對越南紙板市場來說是一個直接的問題,因為白面塑合板仍然是最大的產品等級,其成本結構取決於再生纖維層。當纖維成本劇烈波動時,造紙企業和加工商並非總是能將這些波動轉嫁給簽訂固定價格或價格敏感型合約的客戶,尤其是在食品和日常消費品(FMCG)行業。因此,利潤率不斷受到擠壓,價值成長放緩,計劃的可見度降低。此外,專注於通用產品的供應商比擁有強大客戶關係的專業級供應商處境更加脆弱。

細分市場分析

2025年,白底瓦楞紙板在越南紙板市場佔據36.27%的佔有率,憑藉其在食品、飲料和日用快速消費品包裝應用中兼顧可接受的印刷品質和成本效益,保持著領先地位。該等級紙板仍然是越南紙板市場的核心,國內買家在批量生產二次瓦楞紙板和多包裝應用時,仍會仔細考慮原料成本。未漂白可折疊紙板繼續應用於對包裝要求更為嚴格的領域,例如藥品、化妝品和高階食品。在這些領域,更高的表面光潔度、品牌品質和更潔淨的紙板外觀支撐著更高的價格和更嚴格的採購標準。液體包裝紙板也扮演著重要的角色,因為它依賴無菌包裝形式,而無菌包裝對性能的要求與標準可折疊紙盒有所不同,尤其是在乳製品和即飲飲料(RTD)領域。

預計2026年至2031年間,餐飲服務用紙板的複合年成長率將達到7.57%,成為成長最快的紙板等級。這主要得益於速食店、外帶平台以及單份包裝消費對杯子、容器和外帶包裝的持續需求。越南的餐廳總數預計在2025年達到32.95萬家,到2026年底將達到33.36萬家,這將促進都市區一次性紙板產品的普及。在越南紙板產業,這使得白襯塑合板(需求量大)與餐飲服務和液體應用領域價值成長更快的紙板之間的界線更加清晰。這也意味著,與那些只專注於標準再生紙板的加工商相比,那些投資於阻隔性能、穩定成型性和食品接觸品管的供應商更有可能在高級產品領域獲得更大的市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 加工食品和飲料消費量增加

- 電子商務和零售包裝的擴張

- 塑膠替代及向EPR主導的紙質包裝過渡

- 對藥品在地化和合規包裝的需求

- 利樂公司產能的提升正在促進液體包裝包裝的普及。

- 出口買家的可追溯性要求和FSC要求正在改變加工商的選擇方式。

- 市場限制因素

- 再生纖維價格波動和進口依賴性

- 分散式轉換器基礎設施和持續競爭

- 聚乙烯飲料紙匣回收的瓶頸

- 進口壁壘和對液態板的依賴

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 未漂白飾面

- 折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tetra Pak International SA

- Oji Interpack Vietnam Co., Ltd.

- SONG LAM Trading & Packaging Production CO., Ltd.

- Khang Thanh Manufacturing JSC

- Starprint Vietnam Joint Stock Company

- BINH MINH PAT CO., LTD

- Ngoc Diep Joint Stock Company

- intBOX Intelligent Packaging Corporation

- New Life Packaging Printing Company

- Hoang Vuong Paper Packaging Co., Ltd.

- Viet Van Nhat CO., LTD

- Avestar Packaging Group Joint Stock Company

- Kraft of Asia Paperboard & Packaging Co., Ltd.

- My Huong Paper Manufacturing JSC

- Dong Tien Packaging and Paper Co., Ltd.

- Sai Gon Paper Corporation

- Miza Nghi Son Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the vietnam cartonboard market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.66 billion in 2026 to reach USD 2.29 billion by 2031, at a CAGR of 6.65% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Cartonboard Market Trends and Insights

Rising Processed Food And Beverage Consumption

Vietnam's food and beverage sector generated VND 726.5 trillion (USD 27.94 billion) in 2025 and is projected to reach VND 760 trillion (USD 29.23 billion) in 2026, which keeps a broad demand base in place for milk cartons, dry food cartons, frozen food packs, and other secondary paperboard formats. That spending matters to the Vietnam cartonboard market because it supports demand across multiple board grades simultaneously, rather than relying on a single end-use pocket. As household purchases move further toward packaged and branded food, converters benefit from repeat demand driven by labeling, transport protection, and visual shelf presentation in modern retail and foodservice channels. The demand profile also favors suppliers that can handle mixed jobs across beverages, dairy, frozen products, and dry grocery lines without long lead times or inconsistent print quality. The result is a steadier order book for folding cartons, foodservice packs, and liquid board applications, helping the Vietnam cartonboard market maintain growth even as lower-value commodity formats remain under pricing pressure.

E-Commerce And Retail-Ready Packaging Expansion

Vietnam's e-commerce market recorded GMV of VND 458.16 trillion (USD 16.58 billion) in 2025, and revenue in the first quarter of 2026 rose 32.74% year on year to VND 134.6 trillion (USD 5.19 billion). The Ministry of Industry and Trade's digital economy platform also stated that Vietnam's e-commerce market is targeting USD 37 billion in 2026, which points to continued expansion in direct-to-consumer shipments and branded packaging demand. This shift supports the Vietnam cartonboard market because packaging is increasingly expected to protect goods in transit and still perform as a display-ready unit when it reaches the buyer or retailer. That change improves the position of converters with digital and UV offset capabilities, since shorter runs, greater artwork variation, and faster product refresh cycles are becoming more common. It also shifts the value mix away from plain transit packs and toward litho-laminated and better-finished folding cartons, giving the Vietnam cartonboard market a stronger revenue profile than pure volume growth would suggest.

Recovered Fiber Price Volatility And Import Dependence

Vietnam banned imports of mixed paper and left old corrugated containers as the dominant imported recovered fiber grade, which keeps domestic mills exposed to international trade flows and pricing changes in recycled fiber. US wastepaper unit prices rose from USD 167 per tonne in 2020 to USD 204 per tonne in 2024, which shows how input cost swings can move quickly across the supply chain before easing again. This is a direct issue for the Vietnam cartonboard market because white-lined chipboard remains the largest product-grade segment and depends on recycled fiber layers in its cost structure. When fiber costs move sharply, mills and converters cannot always pass those changes through to customers on fixed or price-sensitive contracts, especially in food and FMCG work. The result is a recurring margin squeeze that slows value growth, weakens planning visibility, and keeps commodity-focused suppliers more vulnerable than specialty-grade operators with tighter customer relationships.

Other drivers and restraints analyzed in the detailed report include:

- Plastic Substitution And EPR-Led Paper Packaging Shift

- Pharmaceutical Localization And Compliance Packaging Demand

- Fragmented Converter Base And Persistent Price Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White-lined chipboard held 36.27% of the Vietnam cartonboard market share in 2025, maintaining its lead by balancing acceptable print quality with cost efficiency across food, beverage, and everyday FMCG packaging applications. The grade remains central to the Vietnam cartonboard market, where domestic buyers still closely weigh substrate cost in large-volume secondary cartons and multipack applications. Solid bleached board and folding boxboard continue to serve more demanding packaging lines in pharmaceuticals, cosmetics, and premium food, where surface finish, branding quality, and cleaner board appearance support better pricing and more controlled procurement standards. Liquid packaging board also retained an important role because dairy and ready-to-drink categories depend on aseptic formats that require a different performance profile than standard folding carton jobs.

The food service board is projected to grow at a 7.57% CAGR during 2026-2031, making it the fastest-expanding grade, as quick-service restaurants, delivery platforms, and single-serve consumption continue to drive demand for cups, containers, and takeaway packs. Vietnam's total food and beverage outlet count was estimated at 329,500 in 2025 and is projected to reach 333,600 by the end of 2026, supporting a broader adoption of disposable paperboard formats across urban centers. Within the Vietnam cartonboard industry, this creates a clearer split between large-volume white-lined chipboard demand and faster-value growth in food service and liquid applications. It also means suppliers that invest in barrier performance, consistent forming behavior, and food-contact quality control are likely to capture a larger share of the premium mix than converters that focus only on standard recycled-board grades.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Tetra Pak International S.A.

- Oji Interpack Vietnam Co., Ltd.

- SONG LAM Trading & Packaging Production CO., Ltd.

- Khang Thanh Manufacturing JSC

- Starprint Vietnam Joint Stock Company

- BINH MINH PAT CO., LTD

- Ngoc Diep Joint Stock Company

- intBOX Intelligent Packaging Corporation

- New Life Packaging Printing Company

- Hoang Vuong Paper Packaging Co., Ltd.

- Viet Van Nhat CO., LTD

- Avestar Packaging Group Joint Stock Company

- Kraft of Asia Paperboard & Packaging Co., Ltd.

- My Huong Paper Manufacturing JSC

- Dong Tien Packaging and Paper Co., Ltd.

- Sai Gon Paper Corporation

- Miza Nghi Son Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Processed Food and Beverage Consumption

- 4.3.2 E-commerce and Retail-Ready Packaging Expansion

- 4.3.3 Plastic Substitution and EPR-Led Paper Packaging Shift

- 4.3.4 Pharmaceutical Localization and Compliance Packaging Demand

- 4.3.5 Tetra Pak Capacity Expansion Supporting Liquid Carton Adoption

- 4.3.6 Export-Buyer Traceability and FSC Requirements Reshaping Converter Selection

- 4.4 Market Restraints

- 4.4.1 Recovered Fiber Price Volatility and Import Dependence

- 4.4.2 Fragmented Converter Base and Persistent Price Competition

- 4.4.3 PolyAl Beverage Carton Recycling Bottlenecks

- 4.4.4 Imported Barrier and Liquid Board Dependence

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tetra Pak International S.A.

- 6.4.2 Oji Interpack Vietnam Co., Ltd.

- 6.4.3 SONG LAM Trading & Packaging Production CO., Ltd.

- 6.4.4 Khang Thanh Manufacturing JSC

- 6.4.5 Starprint Vietnam Joint Stock Company

- 6.4.6 BINH MINH PAT CO., LTD

- 6.4.7 Ngoc Diep Joint Stock Company

- 6.4.8 intBOX Intelligent Packaging Corporation

- 6.4.9 New Life Packaging Printing Company

- 6.4.10 Hoang Vuong Paper Packaging Co., Ltd.

- 6.4.11 Viet Van Nhat CO., LTD

- 6.4.12 Avestar Packaging Group Joint Stock Company

- 6.4.13 Kraft of Asia Paperboard & Packaging Co., Ltd.

- 6.4.14 My Huong Paper Manufacturing JSC

- 6.4.15 Dong Tien Packaging and Paper Co., Ltd.

- 6.4.16 Sai Gon Paper Corporation

- 6.4.17 Miza Nghi Son Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)