|

市場調查報告書

商品編碼

2072780

印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)India Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

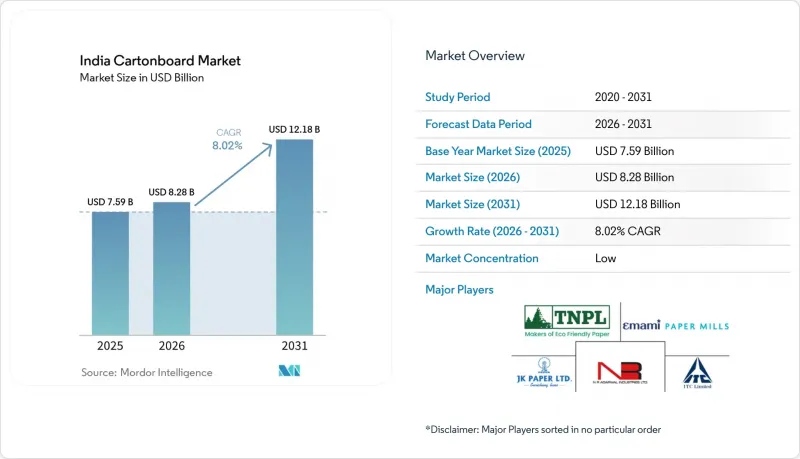

根據 Mordor Intelligence 預測,印度紙板市場規模將從 2025 年的 75.9 億美元和 2026 年的 82.8 億美元成長到 2031 年的 121.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 8.02%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草、化妝品等)進行細分。市場預測以美元計價。

印度紙板市場趨勢與洞察

自2026年起,符合EPR規定的紙包裝的合規優勢

印度紙板市場正受益於日益嚴格的塑膠法規,這些法規針對的是那些嚴重依賴硬質塑膠包裝的品牌所有者。印度一次性塑膠法規的執行力度已表明,這些法規並非徒有其表,僅德里和卡納塔克邦到2024年就已累計收取超過1.98億印度盧比(約合220萬美元)的罰款。在這樣的監管背景下,包裝團隊必須探索能夠減少合規摩擦並簡化審計追蹤的包裝形式。紙板的優點在於能夠減少二次包裝和某些餐飲服務應用中對塑膠的依賴,並且隨著環境報告成為商業採購不可或缺的一部分,其重要性也日益凸顯。因此,能夠提供供應商、材料品質和客戶特定合規要求的紙張製造商和加工商,在年度採購週期中將獲得優勢。此外,印度紙板市場也變得更加挑剔,主要買家越來越傾向於選擇那些能夠兼顧紙板性能和完善文件管理的供應商,而不僅僅是提供最低價格。

用紙板代替一次性塑膠

隨著紙質包裝在更廣泛的日常包裝應用中取代塑膠,印度紙板市場也不斷擴張。持續推進的一次性塑膠禁令加速了餐飲服務和外帶行業向牛皮紙袋、模塑纖維托盤和食品接觸紙板的轉變。這項轉變意義重大,因為它拓展了紙板的需求範圍,使其不再局限於傳統的折疊紙盒,而是佔據了以往使用低成本塑膠或發泡聚苯乙烯包裝的領域。同時,食品接觸應用對紙板的耐油性、阻隔性能和可靠性提出了更高的要求,以符合印度包裝法規中關於遷移材料的要求。這不僅增加了再生紙板的供應,也改善了食品服務紙板和其他高規格紙板的需求結構。因此,印度紙板市場同時滿足了替代需求和品質提升需求,使得這項轉變比短期政策因應措施更具永續性。

再生紙、紙漿和能源成本的波動

投入成本波動仍然是印度瓦楞紙板市場面臨的最緊迫的營運限制因素。 2026年初,受印尼造紙廠停產檢修和原物料供應中斷導致的供應短缺影響,硬木漿價格上漲至每噸615美元以上。國內造紙廠也面臨木材和再生纖維成本飆升的困境,這加劇了原料供應壓力,並使其更難維持低價等級產品的價格穩定。對於依賴進口紙漿和再生紙的造紙廠而言,這是一個特別嚴峻的問題,因為如果客戶抵制漲價,它們幾乎沒有空間來保護利潤率。另一方面,一體化生產商則處於更有利的地位,因為它們可以自行採購紙漿和纖維,即使在價格波動劇烈的時期也能提供結構性的成本緩衝。因此,印度瓦楞紙板原紙市場呈現出更為明顯的兩極化:部分供應商能夠透過一體化來吸收成本衝擊,而另一部分供應商則仍然容易受到全球纖維和能源格局快速變化的影響。

細分市場分析

預計到2025年,白底塑合板將佔印度紙板市場37.19%的佔有率。這反映了再生纖維板在大眾市場二次包裝領域持續強勁的發展動能。由於其優異的印刷性能和大規模生產的成本效益,該等級的紙板在玩具、服裝和日常消費品行業中廣泛應用。此外,面漆和表面處理技術的進步部分消除了再生紙板與優質原生紙漿產品之間先前存在的表面處理差距,進一步鞏固了其市場地位。這使得品牌商能夠在眾多二次包裝應用中使用低成本的基材,同時保持強大的商店競爭力。因此,儘管消費者對外觀和品質一致性的期望日益提高,但印度紙板市場仍以再生紙漿為基礎,保持著廣泛的市場基礎。

預計2026年至2031年間,印度餐飲用紙板市場將以9.17%的複合年成長率成長,隨著連鎖餐廳、外帶平台和外帶轉向紙質食品包裝,該細分市場在印度瓦楞紙板市場中的地位將得到鞏固。這種需求的成長源自於餐飲服務應用日益嚴格的包裝標準,對耐油性、符合遷移物質法規以及優異的可塑性(這些特性是普通再生紙板所不具備的)提出了更高的要求。折疊紙盒紙板和普通漂白紙板仍然是印度瓦楞紙板行業的優質產品,用於藥品、化妝品和糖果甜點等高附加價值包裝,這些產品對白度、硬度和印刷適性要求極高。泰米爾納德邦新聞紙業公司也持續調整其產品組合,轉向盈利更高的折疊紙板,其紙板部門在2026會計年度的產量將達到200,075公噸。未漂白紙板仍然用於一些特定的工業和重型二次包裝應用,但隨著食品接觸包裝和高階印刷紙盒的需求成長速度超過實用運輸包裝的需求,其作用正在縮小。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 可替代一次性塑膠紙板

- 食品和藥品可折疊紙盒優質化進程的推進。

- 無菌乳製品和果汁市場的擴張正在推動液體包裝板的發展。

- 有組織的零售、電子商務和快速貿易中的包裝需求

- 自2026年起,符合EPR規定的紙包裝的合規優勢

- 採用符合FSSAI標準的食品接觸紙板。

- 市場限制因素

- 再生紙、紙漿和能源成本的波動

- 來自廉價進口產品和本地雙面紙廠的價格主導。

- 向不含 PFAS 的屏障過渡增加了認證成本。

- 對於需要阻隔性和低成本的應用而言,軟包裝仍然佔據主導地位。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 未漂白飾面

- 可折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ITC Limited

- NR Agarwal Industries Limited

- JK Paper Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- West Coast Paper Mills Limited

- Andhra Paper Limited

- Pakka Limited

- TCPL Packaging Limited

- Parksons Packaging Limited

- Canpac Trends Private Limited

- Borkar Packaging Private Limited

- Galaxy Offset India Pvt. Ltd.

- Pragati Pack(India)Private Limited

- Kumar Printers Pvt Ltd

- Huhtamaki India Limited

- Tetra Pak India Private Limited

- UFlex Limited

- Oji India Packaging Private Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the india cartonboard market size is projected to expand from USD 7.59 billion in 2025 and USD 8.28 billion in 2026 to USD 12.18 billion by 2031, registering a CAGR of 8.02% between 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Cartonboard Market Trends and Insights

EPR-Ready Paper Packaging Compliance Advantage From 2026

The India cartonboard market is gaining support from the growing stringency of plastic compliance obligations for brand owners that rely heavily on rigid plastic formats. India's single-use plastic enforcement has already shown that regulation is not merely symbolic, as penalties collected in Delhi and Karnataka exceeded INR 198 million (USD 2.2 million) through 2024. That enforcement backdrop is pushing packaging teams to look for formats that reduce compliance friction and simplify audit trails. Cartonboard benefits by helping lower dependence on plastic in secondary packs and selected foodservice applications, which matters more as environmental reporting becomes part of commercial procurement. Mills and converters that can document supply origin, substrate quality, and customer-specific compliance are therefore improving their position in annual sourcing cycles. The India cartonboard market is also becoming more selective, as large buyers increasingly favor suppliers that can pair board performance with documentation discipline, rather than the lowest selling price.

Substitution Of Single-Use Plastics With Paperboard

The India cartonboard market is also moving higher as paper-based formats replace plastic in a wider set of everyday packaging uses. The continued enforcement of the single-use plastic ban encouraged a shift toward kraft bags, molded-fiber trays, and food-contact cartonboard in foodservice and takeaway applications. This change matters because it widens cartonboard demand beyond traditional folding cartons and brings in categories that were once served by low-cost plastic or expanded polystyrene packs. At the same time, food-contact applications require improved grease resistance, cleaner barrier performance, and greater reliability in compliance with India's packaging rules regarding migration. That is improving the demand mix for food service board and other higher-specification grades rather than only adding more recycled board volume. The India cartonboard market is therefore capturing both substitution demand and quality upgrading simultaneously, making the shift more durable than a short-term policy response.

Wastepaper, Pulp, And Energy Cost Volatility

Input cost volatility remains the most immediate operating restraint for the India cartonboard market. Hardwood pulp prices moved above USD 615 per metric tonne in early 2026, driven by supply tightness due to mill maintenance shutdowns and raw material disruptions in Indonesia. Domestic mills also faced a sharp rise in wood and recovered fiber costs, which increased raw material pressure and made it more difficult to maintain price discipline on lower-value grades. This matters most for mills that rely on imported pulp or purchased wastepaper, because they have less room to protect margins when customers resist price increases. Integrated producers are better positioned because in-house access to pulp or fiber provides them with a structural cost buffer during volatile periods. The India cartonboard market is therefore seeing a clearer split between suppliers that can absorb cost shocks through integration and those that remain more exposed to sudden changes in global fiber and energy conditions.

Other drivers and restraints analyzed in the detailed report include:

- Rising Premiumization In Food And Pharma Folding Cartons

- Aseptic Dairy And Juice Expansion Supporting Liquid Packaging Board

- Price-Led Competition From Cheap Imports And Regional Duplex Mills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White-lined chipboard held 37.19% of the Indian cartonboard market share in 2025, which reflects the continued strength of recycled-fiber board in mass-market secondary packaging. The grade remains widely used across toys, apparel, and fast-moving consumer goods because it offers acceptable printability and cost efficiency at scale. Its position has also become more resilient because improvements in topcoats and surface treatments have narrowed part of the historical finish gap between recycled grades and premium virgin-fiber options. That allowed brand owners to maintain shelf presence while still using a lower-cost base board in many secondary applications. The India cartonboard market has therefore maintained a broad recycled-fiber foundation even as customer expectations for appearance and consistency have risen.

The food service board market is projected to expand at a 9.17% CAGR from 2026 to 2031, and this segment of the India cartonboard market is strengthening as restaurant chains, delivery platforms, and takeaway formats shift toward paper-based food packaging. Demand is rising because foodservice applications need grease resistance, migration compliance, and better forming performance than basic recycled trays can deliver under stricter packaging scrutiny. Folding boxboard and solid bleached board remain the premium end of the India cartonboard industry, serving higher-value pharmaceutical, cosmetics, and confectionery packaging where brightness, stiffness, and print performance matter more. Tamil Nadu Newsprint and Papers Limited also continued to reposition its board mix toward higher-realization folding boxboard, and its board unit reached 200,075 metric tonnes of production in FY26. Solid unbleached board still serves niche industrial and heavy-goods secondary packaging, but its role remains smaller because the strongest growth is moving toward food-contact and premium printed cartons rather than utility-heavy transport formats.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- ITC Limited

- N R Agarwal Industries Limited

- JK Paper Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- West Coast Paper Mills Limited

- Andhra Paper Limited

- Pakka Limited

- TCPL Packaging Limited

- Parksons Packaging Limited

- Canpac Trends Private Limited

- Borkar Packaging Private Limited

- Galaxy Offset India Pvt. Ltd.

- Pragati Pack (India) Private Limited

- Kumar Printers Pvt Ltd

- Huhtamaki India Limited

- Tetra Pak India Private Limited

- UFlex Limited

- Oji India Packaging Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Substitution of Single-Use Plastics With Paperboard

- 4.2.2 Rising Premiumization in Food and Pharma Folding Cartons

- 4.2.3 Aseptic Dairy and Juice Expansion Supporting Liquid Packaging Board

- 4.2.4 Organized Retail, E-Commerce, and Quick-Commerce Packaging Demand

- 4.2.5 EPR-Ready Paper Packaging Compliance Advantage From 2026

- 4.2.6 FSSAI-Compliant Food-Contact Paperboard Adoption

- 4.3 Market Restraints

- 4.3.1 Wastepaper, Pulp, and Energy Cost Volatility

- 4.3.2 Price-Led Competition From Cheap Imports and Regional Duplex Mills

- 4.3.3 PFAS-Free Barrier Transition Raises Qualification Costs

- 4.3.4 Flexible Packaging Still Wins in High-Barrier, Low-Cost Applications

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ITC Limited

- 6.4.2 N R Agarwal Industries Limited

- 6.4.3 JK Paper Limited

- 6.4.4 Tamil Nadu Newsprint and Papers Limited

- 6.4.5 Emami Paper Mills Limited

- 6.4.6 West Coast Paper Mills Limited

- 6.4.7 Andhra Paper Limited

- 6.4.8 Pakka Limited

- 6.4.9 TCPL Packaging Limited

- 6.4.10 Parksons Packaging Limited

- 6.4.11 Canpac Trends Private Limited

- 6.4.12 Borkar Packaging Private Limited

- 6.4.13 Galaxy Offset India Pvt. Ltd.

- 6.4.14 Pragati Pack (India) Private Limited

- 6.4.15 Kumar Printers Pvt Ltd

- 6.4.16 Huhtamaki India Limited

- 6.4.17 Tetra Pak India Private Limited

- 6.4.18 UFlex Limited

- 6.4.19 Oji India Packaging Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)