|

市場調查報告書

商品編碼

2072771

德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

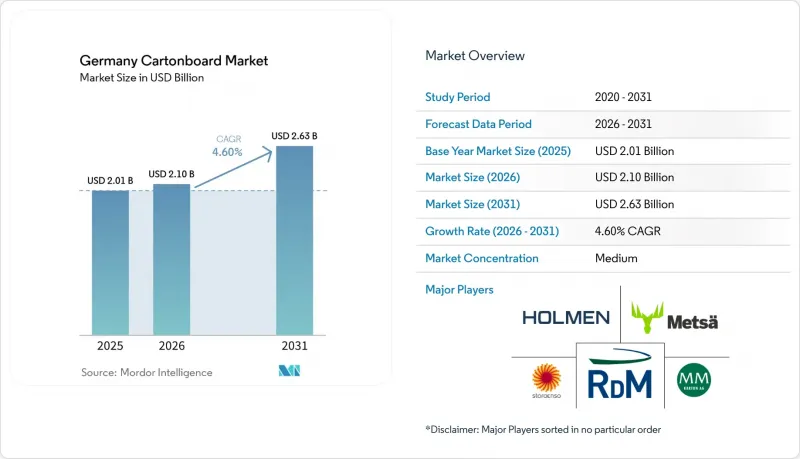

據 Mordor Intelligence 稱,2025 年德國紙板市場價值 20.1 億美元,預計到 2031 年將從 2026 年的 21 億美元成長到 26.3 億美元,預測期(2026-2031 年)的複合年成長率為 4.60%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草等)進行細分。市場預測以美元計價。

德國紙板市場趨勢及洞察

PPWR主導實施“可回收性設計”

《包裝及塑膠回收條例》(PPWR)將於2025年2月生效,並於2026年8月全面實施。這意味著推出歐盟市場的包裝必須明確符合統一的可回收性分類和合格評定要求。在德國,這項要求將添加到現有的合規系統之上,因為中央包裝註冊機構 (Zentrale Stelle Verpackungsregister) 和《包裝方法》(VerpackG) 的框架已經為製造商、加工商和品牌所有者提供了清晰的註冊、數據報告和可回收性評估途徑。在2026年8月截止日期到來之前,採購趨勢已經開始發生變化,品牌所有者正在收緊競標規範,要求包裝具有可回收性、單一材料結構,並且能夠經受更嚴格的監管審查。這種轉變正在提升紙板相對於紙-塑膠-鋁箔複合結構的優勢,因為纖維基包裝既能滿足設計和可回收性方面的要求,又能最大限度地減少材料之間的競爭。此外,造紙商將更有能力提供經認證的可回收產品系列,並確保不同等級、塗層和製作流程的可追溯性。隨著此類聲明成為常規包裝管治的一部分,德國紙板市場正從單純的數量替代轉向對更高規格的需求。

食品飲料包裝領域從塑膠轉向纖維的轉變。

隨著零售商的需求、消費者的期望以及歐盟包裝法規的推進,德國食品飲料包裝領域向塑膠替代品的轉變正加速發展,可回收纖維材料的重要性日益凸顯。食品零售業的大規模自有品牌(PB)項目正在推動這一轉變,因為只需一次設計上的改變,就能將大量的包裝材料從高度塑膠化的包裝形式轉變為可折疊紙板、餐飲用紙板和阻隔塗層紙板。其商業性影響遠不止於數量。與食品接觸的加工食品需要塗層和結構來確保產品安全,同時也要支援可回收性聲明,這提高了供應商的技術難度。因此,德國紙板市場正從單純供應低價值替代品擴展到食品包裝領域的高價值細分市場。 2025年,漢高和MM紙板公司透過一項案例研究展示了這一發展方向:他們使用TOPCOLOR® BARRIER AROMA塗層,以100%紙板解決方案取代了吸塑包裝,該包裝榮獲「2025年德國包裝獎」。 2025年,食品業佔德國紙板市場銷售額的46.21%,因此,該終端用戶領域持續進行的包裝革新活動,為德國紙板市場未來的塗層和產品開發奠定了堅實而永續的基礎。

能源和再生纖維成本波動

2026年,能源價格波動仍是德國紙板市場面臨的最迫切的成本風險。這是因為造紙廠持續處於燃料、運輸和原料成本快速且不規則波動的環境中。邁耶·梅爾霍夫公司在2026年4月的獲利快報中指出,能源、運輸和化學品成本的大幅上漲是影響利潤率的主要因素,經營團隊還指出,自2026年3月以來,這些壓力變得更加明顯。再生紙漿等級尤其容易受到影響,因為其製作流程能耗更高,且對再生紙價格波動更為敏感。德國健全的回收和再利用系統有助於供應鏈的順暢運行,但其高度集中性意味著再生紙漿成本的波動會以比生產商預期更快的速度波及整個造紙廠。擁有汽電共生設施、生質能系統或購電合約的企業能夠承受劇烈的成本波動,但當銷售價格受到擠壓時,這些投資也需要資金。因此,隨著德國紙板市場經歷當前的成本週期,能夠維持利潤率的供應商與缺乏柔軟性的供應商之間的差距正在進一步擴大。

細分市場分析

到2025年,可折疊紙板將佔德國紙板市場佔有率的38.13%,繼續保持其在德國紙板產品組合中佔比最大的地位。其主導地位源自於其對眾多產業的廣泛適應性,包括食品零售、藥品二次包裝和高階消費品等,在這些產業中,紙板的剛性、印刷性和可回收性必須以實用且全面的方式發揮作用。這種營運平衡在德國至關重要,因為許多加工商運作高速生產線,需要能夠支援高效加工且不影響包裝品質或外觀的原料。白面塑合板在食品外包裝和低價消費品領域仍佔據重要地位,但其再生纖維等級更容易受到能源成本波動的影響,這將對其2026年的經濟效益構成更大的壓力。

漂白實心紙板 (SBB) 是成長最快的紙板等級,預計從 2026 年到 2031 年將以 7.53% 的複合年成長率成長。在德國紙板市場,這個細分市場主要由化妝品和非處方藥 (OTC) 應用驅動,這些應用對包裝的視覺效果和衛生性能有更高的要求。品牌擁有者要求包裝表面更亮、印刷效果更均勻、產品保護更嚴格,並且當再生紙替代品無法提供一致的表面效果時,他們正逐步將某些包裝轉向使用 SBB 和其他優質新型纖維紙板。液體包裝紙板 (LPB) 和食品服務紙板 (FSB) 雖然規模仍然相對較小,但隨著飲料和食品接觸包裝不斷轉向仍需具備阻隔性能的纖維基設計,這兩種紙板的需求都在成長。未漂白紙板 (SBB) 服務於小規模的細分市場,主要用於食品安全應用以及打造類似牛皮紙的高階定位。雖然與折疊紙盒紙板和其他 SBB 相比,其市場佔有率較為有限,但其市場地位仍然穩定。德國紙板市場在所有等級中越來越重視已驗證的可回收性和阻隔性能可靠性,從而提升了檢驗的可回收產品系列和清晰技術文件的供應商的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- PPWR主導實施“可回收性設計”

- 食品飲料包裝領域從塑膠轉向纖維的轉變。

- 藥品和非處方藥盒的需求韌性

- 選擇可折疊紙盒以達到展示效果和合規性要求。

- ZSVR費用的優惠待遇鼓勵了純光纖設計。

- 阻隔塗層板材可取代塑膠窗和含氟材料

- 市場限制因素

- 能源和再生纖維成本波動

- 歐洲紙板供應過剩和進口壓力

- 制定食品服務業可重複使用容器的相關法規,以遏制一次性包裝的擴張。

- 與屏障重組和重新認證相關的成本

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 未漂白飾面

- 折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mayr-Melnhof Karton Aktiengesellschaft

- Metsa Board Corporation

- Stora Enso Oyj

- RDM Group SpA

- Holmen AB

- Billerud Aktiebolag

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Moritz J. Weig GmbH & Co. KG

- Edelmann GmbH

- August Faller GmbH & Co. KG

- STI-Gustav Stabernack GmbH

- Pankakoski Mill Oy

- Sappi Germany GmbH

- Sonoco Consumer Products Europe GmbH

- Koehler Paper SE

- WEIG-Packaging GmbH & Co. KG

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany cartonboard market size was valued at USD 2.01 billion in 2025 and is estimated to grow from USD 2.10 billion in 2026 to reach USD 2.63 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, Pharmaceutical and Healthcare, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Cartonboard Market Trends and Insights

PPWR-Led Recyclability-By-Design Adoption

The PPWR entered into force in February 2025 and moves into its core operational phase in August 2026, which means packaging placed on the EU market must align more clearly with harmonized recyclability classifications and conformity requirements. In Germany, that requirement lands on top of an established compliance system, because the Zentrale Stelle Verpackungsregister and the VerpackG framework already give producers, converters, and brand owners a clear route for registration, data reporting, and recyclability assessment. Procurement behavior is already shifting ahead of the August 2026 milestone, with brand owners tightening tender specifications around recyclability, mono-material structures, and documentation that can withstand closer regulatory review. That change improves the position of cartonboard against paper-plastic-foil structures because fiber packs can meet both design and recyclability expectations with fewer material conflicts. It also improves the standing of mills that can offer certified recyclable portfolios and clearer traceability across grades, coatings, and converting steps. As those declarations become part of routine packaging governance, the Germany cartonboard market is moving toward higher-specification demand instead of simple volume replacement.

Plastic-To-Fiber Shift In Food And Beverage Packs

Plastic substitution in German food and beverage packaging is moving with more force because retailer mandates, consumer expectations, and EU-aligned packaging rules are all pointing toward recyclable fiber formats. Large own-label programs in food retail are giving that shift scale, because a single redesign decision can move substantial packaging volumes from plastic-heavy formats toward folding boxboard, foodservice board, and barrier-coated cartonboard. The commercial effect is not limited to tonnage, since food-contact conversion requires coatings and structures that can preserve product safety while still supporting recyclability claims, which raises the technology threshold for suppliers. That is why the Germany cartonboard market is gaining a larger premium layer inside food packaging, rather than only adding lower-value replacement volumes. Henkel and MM Board and Paper illustrated this direction in 2025 when they replaced a blister pack with a 100% cartonboard solution using TOPCOLOR(R) BARRIER AROMA, and that pack won the German Packaging Award 2025. Because food represented 46.21% of 2025 revenues, continued redesign activity in this end-use gives the Germany cartonboard market a large and durable platform for further coating and product development.

Energy And Recovered-Fiber Cost Volatility

Energy volatility remains the most immediate cost risk for the Germany cartonboard market in 2026, because mills are still operating in an environment where fuel, transport, and input costs can move quickly and unevenly. Mayr-Melnhof stated in its April 2026 trading update that significantly higher energy, transport, and chemical costs were the main driver of margin compression, and management said these pressures had become noticeable since March 2026. Recycled-fiber grades are especially exposed because their economics are more sensitive to energy-intensive processing and to changes in recovered paper pricing. Germany's strong collection and recovery system helps keep supply chains active, but that same concentration can make cost movements in recovered fiber pass through mills faster than producers would prefer. Operators with co-generation assets, biomass systems, or power purchase agreements are better placed to absorb sudden cost shifts, yet those investments also require capital at a time when selling prices are under pressure. The result is a sharper split between suppliers that can defend margins and those that face weaker flexibility as the Germany cartonboard market moves through the current cost cycle.

Other drivers and restraints analyzed in the detailed report include:

- Pharma And OTC Carton Demand Resilience

- Folding Carton Preference For Shelf Impact And Compliance

- European Cartonboard Overcapacity And Import Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 38.13% of the Germany cartonboard market share in 2025, which kept it as the largest product grade across the country's cartonboard mix. Its lead comes from a broad fit across food retail, pharmaceutical secondary packaging, and premium consumer goods, where stiffness, printability, and recyclability all need to work together in a practical format. That operating balance matters in Germany because many converters run high-speed lines and need a substrate that supports efficient throughput without compromising pack quality or presentation. White-Lined Chipboard also remains important in outer food packs and lower-premium consumer goods, but its 2026 economics are under greater strain because recycled-fiber grades are more exposed to energy-linked cost volatility.

Solid Bleached Board is the fastest-growing grade, with a forecast CAGR of 7.53% from 2026 to 2031, and this part of Germany cartonboard market size is being lifted by cosmetics and OTC healthcare applications that require cleaner visual performance and stronger hygiene positioning. Brand owners moving toward brighter surfaces, more even print results, and tighter product protection are steadily shifting selected packs toward SBB and other premium fresh-fiber grades when recycled alternatives cannot deliver a consistent finish. Liquid Packaging Board and Food Service Board remain narrower in scale, but both gain when beverage and food-contact packs move further into fiber-based designs that still need barrier performance. Solid Unbleached Board serves a smaller niche centered on food-safe uses and kraft-style premium positioning, which keeps its role stable even if its share is more limited than Folding Boxboard or SBB. Across the grade landscape, the Germany cartonboard market is putting more weight on documented recyclability and barrier credibility, which improves the standing of suppliers with verified recyclable portfolios and clearer technical documentation.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Mayr-Melnhof Karton Aktiengesellschaft

- Metsa Board Corporation

- Stora Enso Oyj

- RDM Group S.p.A.

- Holmen AB

- Billerud Aktiebolag

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Moritz J. Weig GmbH & Co. KG

- Edelmann GmbH

- August Faller GmbH & Co. KG

- STI - Gustav Stabernack GmbH

- Pankakoski Mill Oy

- Sappi Germany GmbH

- Sonoco Consumer Products Europe GmbH

- Koehler Paper SE

- WEIG-Packaging GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 PPWR-Led Recyclability-by-Design Adoption

- 4.3.2 Plastic-to-Fiber Shift in Food and Beverage Packs

- 4.3.3 Pharma and OTC Carton Demand Resilience

- 4.3.4 Folding Carton Preference for Shelf Impact and Compliance

- 4.3.5 ZSVR Fee Incentives Favoring Pure-Fiber Designs

- 4.3.6 Barrier-Coated Board Replacing Plastic Windows and Fluorinated Formats

- 4.4 Market Restraints

- 4.4.1 Energy and Recovered-Fiber Cost Volatility

- 4.4.2 European Cartonboard Overcapacity and Import Pressure

- 4.4.3 Reusable Foodservice Rules Limiting One-Way Pack Growth

- 4.4.4 Barrier Reformulation and Requalification Costs

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton Aktiengesellschaft

- 6.4.2 Metsa Board Corporation

- 6.4.3 Stora Enso Oyj

- 6.4.4 RDM Group S.p.A.

- 6.4.5 Holmen AB

- 6.4.6 Billerud Aktiebolag

- 6.4.7 Smurfit Westrock plc

- 6.4.8 Graphic Packaging International, LLC

- 6.4.9 Moritz J. Weig GmbH & Co. KG

- 6.4.10 Edelmann GmbH

- 6.4.11 August Faller GmbH & Co. KG

- 6.4.12 STI - Gustav Stabernack GmbH

- 6.4.13 Pankakoski Mill Oy

- 6.4.14 Sappi Germany GmbH

- 6.4.15 Sonoco Consumer Products Europe GmbH

- 6.4.16 Koehler Paper SE

- 6.4.17 WEIG-Packaging GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)