|

市場調查報告書

商品編碼

2072784

新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Singapore Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

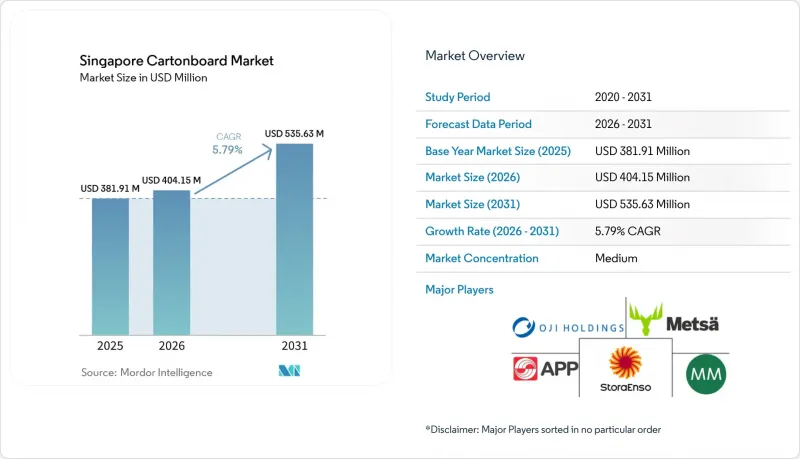

據 Mordor Intelligence 稱,新加坡紙板市場在 2025 年的價值為 3.8191 億美元,預計到 2031 年將達到 5.3563 億美元,而 2026 年為 4.0415 億美元,預測期(2026-2031 年)的複合年成長率為 5.79%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草、化妝品等)進行細分。市場預測以美元計價。

新加坡紙板市場趨勢與洞察

從塑膠包裝過渡到纖維包裝

新加坡的紙板市場直接受益於包裝法規,這些法規有助於受監管企業提高材料報告和減量計畫的透明度和實施效率。新加坡的包裝報告強制計劃要求符合資格的企業提交包裝資料和年度3R計劃,2025年的修訂版將於2025年7月1日生效。由於2025年的資料提交期間為2026年1月至3月,因此當前週期內的包裝決策必須與更嚴格的報告製度保持一致。此外,新加坡於2026年4月推出了飲料容器回收計劃,對塑膠和金屬飲料容器徵收0.10新元(0.07美元)的押金,而紙質飲料容器則免收此收費,這支持了在相關應用中使用纖維材料。 2024年,新加坡產生的塑膠只有5%被回收利用,但塑膠仍佔總廢棄物的近14%。這促使公共政策和企業報告更加關注那些使用後問題較少的替代方案。在此背景下,新加坡的紙板市場不僅受益於對塑膠替代品的需求,還受益於品牌所有者面臨的更短決策週期的需求,他們需要包裝形式具有更明確的合規性和食品接觸適用性要求。

包裝食品和飲料的需求不斷成長

新加坡的紙板市場也受益於食品飲料行業的強勁需求,該行業需要各種類型的包裝,包括印刷包裝、商店展示包裝、運輸包裝和食品接觸包裝。即使到了2025年,食品業仍將是最大的終端用戶,佔總需求的38.76%,凸顯了紙板消費與包裝食品在零售、便利商店和餐飲服務業的日常分銷之間存在著密切的關聯。折疊紙盒在這一結構中繼續發揮核心作用,作為乾貨、糖果甜點、即食產品和多件裝產品的二級包裝,透過正規的零售和分銷管道進行銷售。 「飲料容器回收計畫」將於2026年4月啟動,這也進一步顯示了政府鼓勵在飲料銷售中使用纖維基二級和補充包裝形式的政策訊號。在新加坡的紙板市場,這種需求不僅體現在銷售量的成長上;產品組合也在向對印刷品質、剛性和食品接觸性能要求更高的形式轉變。即使包裝食品種類擴張的速度比產量成長的速度慢,這些成分上的變化也能讓加工業者維持附加價值。

進口紙板及運費波動

新加坡紙板市場最大的結構性限制因素是缺乏本土紙漿和造紙基地來生產各種等級的紙板。本地加工商被迫進口用於折疊盒、固態漂白紙板、液體包裝紙板和其他等級的紙板,導致運輸成本和供應商定價直接影響採購成本。當供應管道緊張時,這種依賴性尤其嚴重,因為與大規模的區域市場不同,新加坡無法將部分需求轉向本地造紙廠。這種依賴也迫使加工商繼續依賴歐洲的高級紙板,而這些紙板對於醫藥、高階食品和化妝品等替代來源有限的行業至關重要。因此,即使終端用戶需求強勁,新加坡紙板市場的利潤率也十分脆弱,因為即使獲得訂單,紙板訂單格居高不下,加工商也難以維持盈利。在客戶可以選擇仔細比較價格並從鄰國購買預加工瓦楞紙板的情況下,這種影響更為嚴重。

細分市場分析

2025年,折疊盒用紙板在新加坡紙板市場佔據34.45%的佔有率,在所有產品等級中佔比最高。這一地位反映了其在食品、化妝品、藥品和煙草包裝等眾多行業的廣泛應用。由於其優異的印刷性能、剛性和厚度一致性,折疊盒用紙板在對貨架外觀和紙板性能要求極高的應用中備受加工商青睞,因此其重要性依然很高。在新加坡紙板產業,折疊盒用紙板的需求也與本地市場需求趨勢高度契合。這是因為該市場以高階零售商品為主,且進口消費品佔比很高,這些商品需要美觀的二次包裝。未漂白單板、漂白單板和白襯塑合板在不同價格區間和性能水平的細分市場中仍然有需求,其中未漂白單板在藥品和高階化妝品應用領域尤為重要,因為這些領域對錶面清潔度和嚴格的認證標準要求極高。

預計到2031年,餐飲用紙板市場將以6.27%的複合年成長率成長,成為新加坡紙板市場成長最快的類別。這一成長與主導食品消費和快餐管道中盃子、托盤、烘焙包裝和服務容器的使用量不斷增加密切相關。 2026年4月,斯道拉恩索推出了“Performa Natura Aqua”,這是一款用於食品服務和烘焙包裝的塗佈折疊紙盒紙板。該產品的紙張重量為195至320克/平方米,顯示供應商正在最佳化紙板等級,以滿足諸如提高耐油性和紙張可回收性等需求。製藥業的需求也在影響產品組合。新加坡衛生科學局2025年的標籤法規強調了紙盒需要具備更高的印刷適性和整合機讀碼的能力。這推動了在受監管應用中使用更厚、更優質的紙板。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從塑膠包裝過渡到紡織包裝

- 包裝食品和飲料需求成長

- 製藥和醫療保健產業的合規需求

- 化妝品和盥洗用品包裝的優質化

- 對食品接觸材料的可追溯性和進口合規性要求更加嚴格。

- 小批量SKU的增加與數位化的需求

- 市場限制因素

- 進口板和運費波動

- 來自低成本區域轉換器的競爭

- 國內再生纖維供應短缺

- 遷移測試和食品接觸適用性評估的成本

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 未漂白飾面

- 折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- PT APP Purinusa Ekapersada

- Stora Enso Oyj

- Metsa Board Corporation

- Mayr-Melnhof Karton AG

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Graphic Packaging International, LLC

- Smurfit Westrock plc

- Tetra Pak International SA

- SIG Group AG

- Elopak ASA

- Billerud Aktiebolag(publ)

- ITC Limited

- Nine Dragons Paper(Holdings)Limited

- Sappi Limited

- Sonoco Products Company

- Huhtamaki Oyj

- OVOL Singapore Pte. Ltd.

- SCG Packaging Public Company Limited

- Singapore Cartons(Pte)Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the singapore cartonboard market size was valued at USD 381.91 million in 2025 and estimated to grow from USD 404.15 million in 2026 to reach USD 535.63 million by 2031, at a CAGR of 5.79% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Cartonboard Market Trends and Insights

Shift From Plastic to Fiber-Based Packaging

The Singapore cartonboard market is receiving direct support from packaging rules that make material reporting and reduction plans more visible and more operational for regulated companies. Singapore's Mandatory Packaging Reporting scheme requires covered businesses to submit packaging data and annual 3R plans, and the 2025 amendment regulations took effect on July 1, 2025. The 2025 data submission window ran from January to March 2026, meaning packaging decisions must already align with a tighter reporting structure in the current cycle. Singapore also activated its Beverage Container Return Scheme in April 2026, with a SGD 0.10 (USD 0.07) deposit on plastic and metal beverage containers, keeping paper-based beverage formats outside that levy structure and supporting fiber-based options in adjacent applications. Only 5% of the plastics generated in Singapore were recycled in 2024, while plastics accounted for nearly 14% of total waste generated, drawing attention to alternatives that create fewer end-of-life concerns in public policy and corporate reporting. In this setting, the Singapore cartonboard market is benefiting not only from substitution away from plastics, but also from the shorter decision window that brand owners now face when they need packaging formats with clearer compliance and food-contact credentials

Growth in Packaged Food and Beverage Demand

The Singapore cartonboard market is also supported by a food and beverage base that needs a broad mix of printed, shelf-ready, transport, and food-contact packaging. Food remained the largest end-user in 2025, accounting for 38.76% of total demand, underscoring the strong link between board consumption and daily packaged food distribution across retail, convenience, and foodservice channels. Folding cartons remained central to this structure because they serve secondary packaging in dry foods, confectionery, ready-to-eat products, and multipack applications that move through organized retail and delivery channels. The Beverage Container Return Scheme, which started in April 2026, also adds another policy signal in favor of fiber-based secondary and complementary packaging formats for beverage sales. Within the Singapore cartonboard market, this demand is not only volume-led, as the product mix is also moving toward formats that require better print finish, greater stiffness, and more reliable food-contact performance. That mix shift helps converters defend value even when tonnage growth is more measured than the expansion in packaged food offerings.

Imported Board and Freight Cost Volatility

The biggest structural limit on the Singapore cartonboard market is the lack of a domestic pulping or papermaking base for cartonboard grades. Local converters have to import folding boxboard, solid bleached board, liquid packaging board, and other grades, which means freight costs and supplier pricing move directly into procurement economics. That dependency matters most when supply routes tighten, because Singapore cannot shift part of its requirements to local mills as larger regional markets can. The same dependence also keeps converters exposed to premium European grades, which are important in pharmaceutical, premium food, and cosmetic applications, where alternative sourcing is limited. In the Singapore cartonboard market, this leaves margins vulnerable even when end-user demand is healthy, because converters can win orders but still struggle to protect profitability when landed board costs stay high. The effect is more severe in standard jobs where customers closely compare prices and have the option to source converted cartons from neighboring countries.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical and Healthcare Compliance Needs

- Premiumization in Cosmetics and Toiletries Packaging

- Competition From Lower-Cost Regional Converters

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 34.45% of the Singapore cartonboard market share in 2025, the largest among product grades, and that position reflects its wide use across food, cosmetics, pharmaceutical, and tobacco packaging. The grade remains central because converters rely on it for strong printability, stiffness, and consistent caliper in applications where shelf appearance and carton performance both matter. Within the Singapore cartonboard industry, folding boxboard also aligns well with the local demand profile, as the market has a premium retail mix and a high share of packaged imported consumer goods that require well-finished secondary packaging. Solid bleached board, solid unbleached board, and white-lined chipboard each continue to serve distinct price and performance niches, with solid bleached board particularly important in pharmaceutical and premium cosmetic uses where cleaner surfaces and strict certification standards carry more weight.

The food service board segment is projected to grow at a 6.27% CAGR through 2031, making it the fastest-growing grade in the Singapore cartonboard market. That growth is tied to rising use of cups, trays, bakery packs, and service containers in delivery-led food consumption and quick-service channels. Stora Enso launched Performa Natura Aqua in April 2026 as a dispersion-coated folding boxboard for foodservice and bakery packaging, with grammages ranging from 195 to 320 g/m2, demonstrating how suppliers are tailoring grades to meet grease resistance and improved paper recovery needs. Pharmaceutical demand is also influencing the product mix, as the Health Sciences Authority's 2025 labeling update highlighted the need for cartons with better printability and machine-readable code integration, which supports the use of higher-caliper premium board in regulated applications.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- PT APP Purinusa Ekapersada

- Stora Enso Oyj

- Metsa Board Corporation

- Mayr-Melnhof Karton AG

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Graphic Packaging International, LLC

- Smurfit Westrock plc

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Billerud Aktiebolag (publ)

- ITC Limited

- Nine Dragons Paper (Holdings) Limited

- Sappi Limited

- Sonoco Products Company

- Huhtamaki Oyj

- OVOL Singapore Pte. Ltd.

- SCG Packaging Public Company Limited

- Singapore Cartons (Pte) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift From Plastic to Fiber-Based Packaging

- 4.2.2 Growth in Packaged Food and Beverage Demand

- 4.2.3 Pharmaceutical and Healthcare Compliance Needs

- 4.2.4 Premiumization in Cosmetics and Toiletries Packaging

- 4.2.5 Tightening Food-Contact Traceability and Import-Compliance Requirements

- 4.2.6 Short-Run SKU Proliferation and Digital Conversion Demand

- 4.3 Market Restraints

- 4.3.1 Imported Board and Freight Cost Volatility

- 4.3.2 Competition From Lower-Cost Regional Converters

- 4.3.3 Limited Domestic Recovered Fiber Availability

- 4.3.4 Migration-Testing and Food-Contact Qualification Costs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 PT APP Purinusa Ekapersada

- 6.4.2 Stora Enso Oyj

- 6.4.3 Metsa Board Corporation

- 6.4.4 Mayr-Melnhof Karton AG

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Graphic Packaging International, LLC

- 6.4.8 Smurfit Westrock plc

- 6.4.9 Tetra Pak International S.A.

- 6.4.10 SIG Group AG

- 6.4.11 Elopak ASA

- 6.4.12 Billerud Aktiebolag (publ)

- 6.4.13 ITC Limited

- 6.4.14 Nine Dragons Paper (Holdings) Limited

- 6.4.15 Sappi Limited

- 6.4.16 Sonoco Products Company

- 6.4.17 Huhtamaki Oyj

- 6.4.18 OVOL Singapore Pte. Ltd.

- 6.4.19 SCG Packaging Public Company Limited

- 6.4.20 Singapore Cartons (Pte) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)