|

市場調查報告書

商品編碼

2072770

義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Italy Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

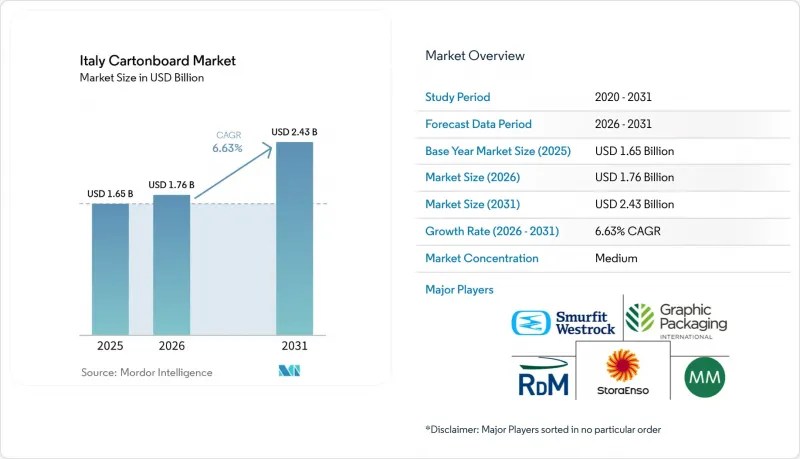

根據 Mordor Intelligence 預測,義大利紙板市場預計將從 2025 年的 16.5 億美元成長到 2026 年的 17.6 億美元,到 2031 年達到 24.3 億美元,2026 年至 2031 年的複合年成長率預計為 6.63%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草、化妝品等)進行細分。市場預測以美元計價。

義大利紙板市場趨勢與洞察

消費品包裝中以塑膠取代紙張

從塑膠包裝轉向紙包裝仍然是義大利紙板市場短期需求的最大驅動力。塑膠包裝法規(PPWR)將於2025年2月生效,並於2026年8月12日起廣泛適用。在新歐盟包裝框架下,這將使可回收纖維基包裝材料比許多塑膠替代品更具優勢。消費者的態度也正朝著類似的方向發展。根據Pro Carton發布的2025年報告,在五個歐洲國家接受調查的成年人中,89%的人更喜歡紙板包裝而非塑膠包裝,其中義大利和德國的受訪者最願意為永續包裝支付更高的價格。這種轉變意義重大,因為需求不再局限於瓦楞紙運輸包裝,而是進一步滲透到用於冷凍食品、化妝品和其他商店消費品的可折疊紙盒領域。隨著加工商擴大在以前由塑膠吸塑包裝和軟包裝主導的應用領域中使用更輕的塗佈紙,義大利紙板市場在銷售和價值方面都迎來了新的機會。當品牌擁有者要求包裝同時具備可回收性、印刷品質和高階外觀時,這種效應最為明顯。

利用PPWR重新設計封裝並減少空隙

受《包裝和廢棄物減量條例》(PPWR)的推動,義大利紙板市場正在湧現出第二個需求細分領域,其意義遠不止於簡單的材料替代方案。該條例引入了通用關於包裝設計和減少廢棄物的通用規則,敦促品牌所有者在2026年8月實施日期前減少包裝空間並重新思考面向消費者的包裝結構。對於以出口為導向的義大利食品和藥品加工商而言,這種壓力尤其顯著,因為不符合規定的設計可能會限制其進入整個歐盟單一市場。這推動了對輕質高剛性紙板的需求,這些紙板可用於製作折疊紙盒,在保持強度的同時降低紙張重量和包裝尺寸。此外,客戶越來越傾向於尋找能夠以最小營運中斷處理重新設計的包裝合作夥伴,這使得擁有強大的設計、測試和文件能力的加工商受益匪淺。事實上,義大利紙板市場不僅受益於紙板需求的成長,也受益於向更高規格等級和更複雜包裝的轉變。

原生紙漿和電力成本波動

成本波動仍然是義大利紙板市場最明顯的業務限制因素。邁耶·梅爾霍夫公司在2026年第一季獲利快報中指出,自2026年3月以來,中東局勢的惡化加劇了能源、運輸和化學原料方面的壓力。該公司在2026年4月的投資人報告中也指出,市場環境依然疲軟,結構性供應過剩問題持續存在。這意味著,生產商在不承擔銷售量下降風險的情況下,將成本上漲轉嫁給供應鏈的空間有限。這種情況給原生紙漿和再生紙漿紙板生產商都帶來了挑戰,因為造紙商需要收回成本,而加工商對價格仍然高度敏感。主要再生瓦楞紙板生產商面臨的財務壓力也令人擔憂。儘管生產和出貨量正常,但RDM公司在2026年3月簽署了債務償還延期協議。在能源、貨運和原料供應穩定之前,儘管基本需求強勁,義大利紙板市場仍將面臨利潤率壓力。

細分市場分析

到2025年,可折疊瓦楞紙板將佔據義大利紙板市場34.21%的佔有率,成為以金額為準最高的紙板產品等級。其主導地位源自於其在眾多產業的廣泛應用,包括食品、非處方成藥,這些產業對紙板的剛性、印刷品質和表面光潔度要求極高,基本的保護功能也同樣重要。白襯紙板在大眾市場包裝和商店終端零售模式中仍然佔據重要地位,在這些領域,再生固態固態則繼續供應給更小眾的高階市場,這些市場對外觀、強度或特殊加工要求更為嚴格。

預計到2031年,義大利液體包裝紙板市場將以7.31%的複合年成長率成長,成長速度在所有產品等級中位居榜首。利樂公司於2026年4月推出「Sterilgarda Alimenti」產品,顯示紙基阻隔技術正正式進入商業無菌紙盒領域,不再處於研發階段。利樂公司於2026年1月決定投資6,000萬歐元(約7,120萬美元)興建紙基阻隔技術研發先導工廠,也顯示該公司將持續投資以支持此產品等級的轉型。在整個義大利紙板產業,不同等級產品之間的競爭正朝著更輕的結構、更簡單的阻隔方式以及在更低材料重量下實現更高性能的方向發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 消費品包裝中以塑膠取代紙張

- 食品、美容和非處方 (OTC) 產品包裝的優質化。

- 零售商店和商店展示用紙箱的需求

- 義大利紙張和紙板回收率很高

- 受 PPWR 的啟發,重新設計封裝並減少空隙。

- 一種結構較簡單的食品接觸屏障,不含 PFAS。

- 市場限制因素

- 原生紙漿和電力成本波動

- 與塑膠和其他液體包裝形式的競爭

- 中小企業面臨的PPWR文件編制和合規性保證的負擔。

- PFAS 和 BPA 相關法規變更後,食品接觸材料的精煉和檢測成本增加。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 未漂白木板

- 折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mayr-Melnhof Karton AG

- Reno De Medici SpA

- Stora Enso Oyj

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Fedrigoni SpA

- Seda International Packaging Group SpA

- Tetra Pak Italiana SpA

- SIG Combibloc Italia Srl

- Elopak Italia Srl

- Palladio Group SpA

- DS Smith Packaging Italia SpA

- Pozzoli SpA

- Lucaprint SpA

- BOX MARCHE SPA

- Eurpack Srl

- CM Cartotecnica Moderna Srl Benefit

- Industria Grafica Umbra srl

- Eurographic srl

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy cartonboard market size is expected to increase from USD 1.65 billion in 2025 to USD 1.76 billion in 2026 and reach USD 2.43 billion by 2031, growing at a CAGR of 6.63% over 2026-2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Cartonboard Market Trends and Insights

Plastic-To-Paper Substitution Across Consumer Packaging

Plastic-to-paper substitution remains the strongest near-term demand driver for the Italy cartonboard market. The PPWR entered into force in February 2025 and will apply broadly from August 12, 2026, which makes recyclable fiber-based formats easier to position under the new EU packaging framework than many plastic alternatives. Consumer attitudes are also moving in the same direction, with Pro Carton reporting in 2025 that 89% of surveyed adults across 5 European countries preferred cartonboard to plastic packaging, while Italian and German respondents were among the most willing to pay more for sustainable packaging. That change matters because demand is no longer limited to corrugated shipping packs and is moving deeper into folding cartons for frozen food, cosmetics, and other shelf-facing consumer products. As converters make lighter coated grades work in applications once dominated by plastic blisters or flexible formats, the Italy cartonboard market is gaining both volume and value opportunities. The effect is strongest where brand owners need recyclability, print quality, and premium presentation in the same pack.

PPWR-Driven Packaging Redesign And Void-Space Reduction

PPWR-led redesign is creating a second layer of demand for the Italy cartonboard market beyond simple material substitution. The regulation introduces common EU rules on packaging design and waste reduction, pushing brand owners to reduce space and reassess the structure of consumer-facing packs before the application date in August 2026. For Italy's export-oriented food and pharmaceutical converters, that pressure is especially relevant because non-compliant designs can restrict access across the full EU single market. This is increasing demand for lighter but stiffer folding boxboard grades that can preserve pack strength while trimming basis weight and pack dimensions. It also favors converters with deeper design, testing, and documentation capabilities, since customers increasingly want a packaging partner that can help them move through redesign work with less disruption. In practice, the Italian cartonboard market is benefiting not only from more board demand but also from a shift toward higher-specification grades and better-engineered packs.

Virgin Pulp And Electricity Cost Volatility

Cost volatility remains the clearest operating restraint for the Italy cartonboard market. Mayr-Melnhof stated in its first-quarter 2026 trading update that recent escalations in the Middle East increased pressure on energy, transportation, and chemicals from March 2026 onward. In its April 2026 investor presentation, the company also said that weak market conditions and structural overcapacity persisted, which means producers have limited room to pass higher costs through the chain without risking volume loss. That combination creates a difficult environment for both virgin-fiber and recycled-board producers, as mills need to recover costs while converters remain highly price-sensitive. Financial stress at major recycled-board players adds to the caution, as RDM entered a forbearance agreement in March 2026 even though production and deliveries continued normally. Until energy, freight, and raw-material conditions stabilize, the Italy cartonboard market will continue to face margin pressure, even as underlying demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization In Food, Beauty, And OTC Packaging

- High Italian Paper And Board Recycling Performance

- Competition From Plastic And Alternative Liquid-Pack Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 34.21% of the Italy cartonboard market share in 2025, making it the largest product grade by value. Its lead came from broad use across food, OTC pharmaceuticals, cosmetics, and tobacco cartons, where stiffness, print quality, and surface finish matter as much as basic protection. White-lined chipboard remained important in mass-market packs and shelf-ready retail formats, where recycled fiber content and cost control are central to buying decisions. Solid bleached board and solid unbleached board continued to serve narrower premium niches, especially where appearance, strength, or specialty conversion requirements were more demanding.

The Italy cartonboard market size for liquid packaging board is projected to expand at a 7.31% CAGR through 2031, the fastest pace among product grades. Tetra Pak's April 2026 launch with Sterilgarda Alimenti showed that paper-based barrier technology has moved into commercial aseptic cartons and is no longer limited to development work. Tetra Pak's earlier January 2026 decision to invest EUR 60 million (USD 71.2 million) in a pilot plant for paper-based barrier development also points to sustained investment behind this grade transition. Across the Italy cartonboard industry, grade competition is shifting toward lighter structures, simpler barriers, and higher performance at lower material weight.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Mayr-Melnhof Karton AG

- Reno De Medici S.p.A.

- Stora Enso Oyj

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Fedrigoni S.p.A.

- Seda International Packaging Group S.p.A.

- Tetra Pak Italiana S.p.A.

- SIG Combibloc Italia S.r.l.

- Elopak Italia S.r.l.

- Palladio Group S.p.A.

- DS Smith Packaging Italia S.p.A.

- Pozzoli S.p.A.

- Lucaprint S.p.A.

- BOX MARCHE S.P.A.

- Eurpack S.r.l.

- CM Cartotecnica Moderna S.r.l. Benefit

- Industria Grafica Umbra s.r.l.

- Eurographic s.r.l.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic-to-Paper Substitution Across Consumer Packaging

- 4.3.2 Premiumization in Food, Beauty, and OTC Packaging

- 4.3.3 Retail-Ready and Shelf-Ready Carton Demand

- 4.3.4 High Italian Paper and Board Recycling Performance

- 4.3.5 PPWR-Driven Packaging Redesign and Void-Space Reduction

- 4.3.6 PFAS-Free and Simpler Food-Contact Barrier Structures

- 4.4 Market Restraints

- 4.4.1 Virgin Pulp and Electricity Cost Volatility

- 4.4.2 Competition From Plastic and Alternative Liquid-Pack Formats

- 4.4.3 PPWR Documentation and Conformity Burden for SMEs

- 4.4.4 Food-Contact Reformulation and Testing Costs After PFAS and BPA Changes

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton AG

- 6.4.2 Reno De Medici S.p.A.

- 6.4.3 Stora Enso Oyj

- 6.4.4 Smurfit Westrock plc

- 6.4.5 Graphic Packaging International, LLC

- 6.4.6 Fedrigoni S.p.A.

- 6.4.7 Seda International Packaging Group S.p.A.

- 6.4.8 Tetra Pak Italiana S.p.A.

- 6.4.9 SIG Combibloc Italia S.r.l.

- 6.4.10 Elopak Italia S.r.l.

- 6.4.11 Palladio Group S.p.A.

- 6.4.12 DS Smith Packaging Italia S.p.A.

- 6.4.13 Pozzoli S.p.A.

- 6.4.14 Lucaprint S.p.A.

- 6.4.15 BOX MARCHE S.P.A.

- 6.4.16 Eurpack S.r.l.

- 6.4.17 CM Cartotecnica Moderna S.r.l. Benefit

- 6.4.18 Industria Grafica Umbra s.r.l.

- 6.4.19 Eurographic s.r.l.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)