|

市場調查報告書

商品編碼

2072767

西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spain Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

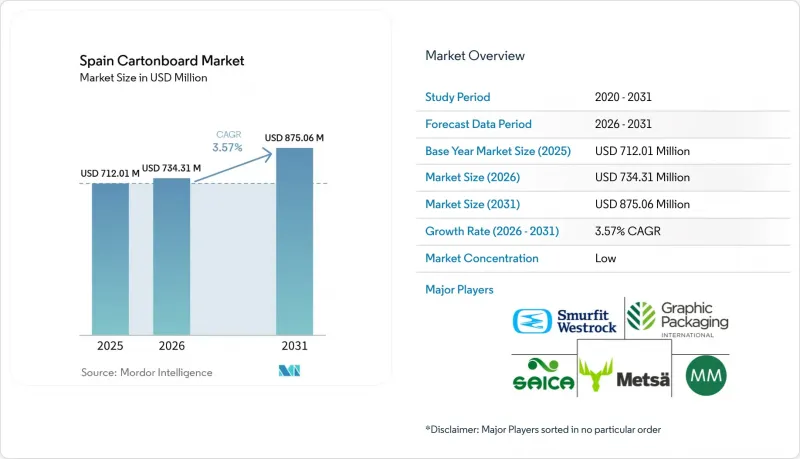

據 Mordor Intelligence 稱,2025 年西班牙紙板市場價值為 7.1201 億美元,預計到 2031 年將達到 8.7506 億美元,而 2026 年為 7.3431 億美元,預測期(2026-2031 年)的複合成長率為 3.57%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊紙盒紙板、白襯紙板、液體包裝紙板、食品服務用紙板)、包裝形式(折疊紙盒、液體包裝、套筒和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草、化妝品等)進行細分。市場預測以美元計價。

西班牙紙板市場的趨勢與洞察

食品飲料產業的永續包裝替代方案

西班牙紙板市場正受益於更嚴格的塑膠包裝法規以及製造商對非紡織包裝材料日益成長的責任成本。西班牙的包裝法律規範迫使品牌所有者轉向可回收包裝,並提供更清晰的處置方法信息,這使得紙板成為食品和飲料產品線更實用的商業性選擇。 2025年,新鮮和冷凍食品佔西班牙可折疊紙板加工商銷售額的29%,飲料佔21%。因此,這些品類的替代產品具有顯著的銷售量成長潛力。 2024年12月在西班牙推出的「PaperSeal Shape」托盤表明,加工商已在2026年8月監管合規截止日期前開始用紙板結構取代傳統的塑膠托盤。隨著越來越多的食品包裝轉向單一材料纖維包裝,西班牙紙板市場對高品質原生紙漿紙板和可回收零售包裝的需求都在不斷成長。這種轉變有利於那些能夠在一份提案中提供原料採購、加工品質和監管文件的供應商。

對電子商務和貨架即用型紙箱的需求

西班牙紙板市場也受惠於零售和線上履約中「貨架即用型」包裝的普及。零售商越來越傾向於選擇能夠保護運輸途中商品且無需額外處理即可直接擺放在貨架上的包裝形式,這使得紙板在物流中扮演著更實用的角色。這種需求推動了「折疊紙板」和「白襯紙板」等新型包裝形式的發展,這些包裝介於簡單的運輸包裝和高階零售展示之間。在西班牙紙板市場,這些需求正在拓展紙板的用途,使其從品牌二級包裝擴展到能夠降低人事費用和快速補貨的工具。此外,一些傳統上使用紙張重量紙板的品類也開始採用更輕的紙板,從而改變了多產品加工商的紙板等級組成。因此,紙板的需求基礎正在形成,這不僅與客流量的成長有關,也與全通路零售的發展密切相關。

能源和再生紙板成本波動

西班牙紙板市場仍然極易受到能源成本波動的影響,因為紙張和紙板的生產依賴連續的工業生產計劃,這限制了其營運柔軟性。電力和天然氣價格的上漲會迅速影響利潤率和營運資金,因為造紙廠短期內難以減產。再生纖維的成本也是一個重要因素。到2025年底,歐洲OCC(廢舊紙箱)價格徘徊在每噸120歐元(135美元)左右,之後穩定在每噸105歐元(118美元)左右。這個價格水準使得再生紙價格的下限高於2022年之前的市場水平,從而削弱了競爭力較弱的造紙企業在西班牙紙板市場的競爭力。關閉位於卡斯特爾維斯瓦爾的雷諾·德·梅迪奇造紙廠的協議表明,長期成本壓力會導致西班牙企業必須做出嚴格的產能決策。對於那些沒有能源熱電汽電共生設施或可再生能源契約,或者規模不足以將成本波動轉嫁給客戶的企業來說,這種壓力最為沉重。

細分市場分析

2025年,可折疊紙板在西班牙紙板市場佔據33.14%的佔有率,成為銷量和價值最高的紙板等級。其在西班牙紙板市場的主導地位源於其在二級包裝中的廣泛應用,這些包裝對紙板的剛性、表面光澤和可靠的印刷品質都有很高的要求。未漂白紙板在高級化妝品和糖果甜點的包裝中繼續發揮著重要作用,其潔白的表面有助於提升產品的高階定位。未漂白紙板也用於餐飲服務和零售包裝,在這些領域,強度比高白度更為重要。白色背襯塑合板繼續用於對成本較為敏感的穀物和加工食品的包裝,在這些領域,使用回收材料已被商業性接受,並且通常是首選。

預計到2031年,液體包裝紙板的複合年成長率將達到4.63%,成為西班牙紙板市場成長最快的類別。西班牙的乳製品、果汁和植物來源飲料市場對無菌包裝的需求穩定,因為這些產品需要避光避氧。此外,自2025年1月起生效的第1055/2022號皇家法令提高了印刷品質的重要性,優先選擇能夠清晰一致地顯示分類資訊的紙板。食品服務紙板透過開發新的應用,例如用於餐飲業的杯子、托盤和載板,保持了西班牙紙板行業的類別多樣性。斯道拉恩佐位於奧盧的新消費品包裝紙板生產線預計於2025年初開始擴大產能,並從2027年開始增加對歐洲的供應。這有望部分緩解西班牙紙板市場的供應短缺,並可能促使西班牙紙板產業加工商的採購模式改變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品飲料產業轉向永續包裝

- 對電子商務和貨架即用型紙箱的需求

- 加工食品和出口包裝市場的成長

- 適用於藥品和化妝品的高級二級包裝。

- 2025年符合印刷分類標籤的要求

- 藥物聚集和可追溯性的複雜性

- 市場限制因素

- 能源和再生紙板成本波動

- 與塑膠相比,阻隔性能存在權衡

- 預印分類標籤造成的藝術作品複雜性

- 2026年8月之前有關可回收性的文件負擔

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 實心未漂白板材

- 折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mayr-Melnhof Karton AG

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- Saica Group

- Metsa Board Corporation

- Stora Enso Oyj

- Reno de Medici SpA

- SIG Group AG

- Elopak ASA

- Huhtamaki Oyj

- Lecta, SA

- Holmen AB

- Billerud Aktiebolag

- Alzamora Group

- Cartondis SAU

- Embalajes Vidal Albinana SL

- WORLD VYPMAR, SL

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain cartonboard market size was valued at USD 712.01 million in 2025 and estimated to grow from USD 734.31 million in 2026 to reach USD 875.06 million by 2031, at a CAGR of 3.57% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Cartonboard Market Trends and Insights

Sustainable Packaging Substitution In Food And Beverage

The Spain cartonboard market is gaining direct support from tighter plastic packaging rules and rising producer responsibility costs for non-fiber formats. Spain's packaging framework increased pressure on brand owners to move toward recyclable packs with clearer end-of-life communication, making cartonboard a more practical commercial choice for food and beverage lines. Fresh and frozen food represented 29% of folding carton converter turnover in Spain in 2025, while beverages accounted for 21%, so substitution in these categories carries clear volume potential for the Spain cartonboard market. The December 2024 launch of the PaperSeal Shape tray in Spain showed that converters were already replacing conventional plastic trays with paperboard structures before the August 2026 compliance deadline. As more food formats shift to mono-material fiber packs, demand is growing for both premium virgin-fiber boards and recyclable retail formats in the Spanish cartonboard market. That shift favors suppliers that can provide substrate access, conversion quality, and regulatory documentation in one offer.

E-Commerce And Shelf-Ready Carton Demand

The Spain cartonboard market is also benefiting from the spread of shelf-ready packaging in retail and online fulfillment. Retailers increasingly prefer formats that protect goods in transit and move directly onto store shelves without extra handling, giving cartonboard a more functional role in logistics. This use case supports Folding Boxboard and White-Lined Chipboard formats that sit between plain transport packaging and premium retail presentation. In the Spain cartonboard market, that requirement is broadening carton use from a branded secondary pack into a tool for labor reduction and faster replenishment. It is also pulling lighter grammage boards into categories that previously used heavier structures, changing the grade mix for converters with multi-grade portfolios. The result is a more stable demand base for cartons linked to omnichannel retail rather than to store traffic alone.

Energy And Recycled-Board Cost Volatility

The Spain cartonboard market remains exposed to energy cost swings because paper and board production runs on continuous industrial schedules with limited operating flexibility. When electricity and gas prices rise, mills cannot easily reduce output in short intervals, so pressure moves quickly into margins and working capital. The recycled-fiber cost side is also important because European OCC prices stayed near EUR 120 (USD 135) per tonne in late 2025 before stabilizing closer to EUR 105 (USD 118) per tonne. That level keeps a higher cost floor in recycled grades than the market faced before 2022, which leaves less room for weaker Spanish mills in the Spain cartonboard market. Reno de Medici's closure agreement at Castellbisbal showed how prolonged cost pressure can translate into hard capacity decisions in Spain. The burden is most severe for operators without energy co-generation assets, renewable power contracts, or enough scale to pass cost moves through to customers.

Other drivers and restraints analyzed in the detailed report include:

- Processed Food And Export Packaging Growth

- Premium Secondary Packs For Pharma And Beauty

- Barrier Performance Trade-Offs Versus Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 33.14% of the Spanish cartonboard market share in 2025, making it the leading grade by volume and value. Its lead in the Spanish cartonboard market stems from broad use across secondary packs that require stiffness, surface brightness, and reliable print quality. Solid Bleached Board remained relevant in premium cosmetics and confectionery packs where a white surface finish supports premium positioning. Solid Unbleached Board served food-service and retail-ready formats where strength mattered more than high whiteness. White-Lined Chipboard continued to serve cost-sensitive cereals and processed food packs where recycled content was commercially acceptable and often preferred.

Liquid Packaging Board is projected to grow at a 4.63% CAGR through 2031, making it the fastest-moving grade in the Spanish cartonboard market. Spain's dairy, juice, and plant-based beverage base supports steady aseptic packaging demand, as these products require protection from light and oxygen. Royal Decree 1055/2022 also raised the importance of print quality from January 2025, which favored grades that can carry sorting information clearly and consistently. Food Service Board added another outlet through cups, trays, and carrier boards for out-of-home consumption, keeping the grade mix broader in the Spanish cartonboard industry. Stora Enso's new consumer packaging board line at Oulu began ramp-up in early 2025 and will widen European supply from 2027, which may ease some board availability pressure for the Spanish cartonboard market and change converter buying patterns across the Spanish cartonboard industry.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Mayr-Melnhof Karton AG

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- Saica Group

- Metsa Board Corporation

- Stora Enso Oyj

- Reno de Medici S.p.A.

- SIG Group AG

- Elopak ASA

- Huhtamaki Oyj

- Lecta, S.A.

- Holmen AB

- Billerud Aktiebolag

- Alzamora Group

- Cartondis S.A.U.

- Embalajes Vidal Albinana S.L.

- WORLD VYPMAR, S.L.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable Packaging Substitution in Food and Beverage

- 4.2.2 E-commerce and Shelf-Ready Carton Demand

- 4.2.3 Processed Food and Export Packaging Growth

- 4.2.4 Premium Secondary Packs for Pharma and Beauty

- 4.2.5 2025 Printed Sorting-Label Compliance

- 4.2.6 Pharma Aggregation and Traceability Complexity

- 4.3 Market Restraints

- 4.3.1 Energy and Recycled-Board Cost Volatility

- 4.3.2 Barrier Performance Trade-Offs Versus Plastics

- 4.3.3 Artwork Complexity from Printed Sorting Labels

- 4.3.4 Recyclability Documentation Burden Before August 2026

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton AG

- 6.4.2 Graphic Packaging Holding Company

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Saica Group

- 6.4.5 Metsa Board Corporation

- 6.4.6 Stora Enso Oyj

- 6.4.7 Reno de Medici S.p.A.

- 6.4.8 SIG Group AG

- 6.4.9 Elopak ASA

- 6.4.10 Huhtamaki Oyj

- 6.4.11 Lecta, S.A.

- 6.4.12 Holmen AB

- 6.4.13 Billerud Aktiebolag

- 6.4.14 Alzamora Group

- 6.4.15 Cartondis S.A.U.

- 6.4.16 Embalajes Vidal Albinana S.L.

- 6.4.17 WORLD VYPMAR, S.L.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)