|

市場調查報告書

商品編碼

2072666

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East and Africa Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

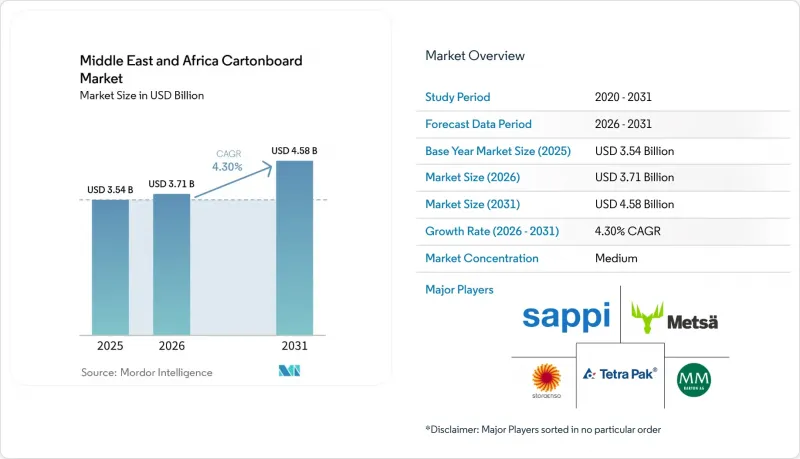

據 Mordor Intelligence 稱,2025 年中東和非洲紙板市場價值為 35.4 億美元,預計到 2031 年將從 2026 年的 37.1 億美元成長至 45.8 億美元,預測期(2026-2031 年)的複合年成長率為 4.30%。

本報告按產品等級(例如,固態漂白紙板、固態未漂白紙板)、包裝類型(例如,折疊紙盒、液體包裝)、終端用戶行業(例如,食品和飲料)以及地區(沙烏地阿拉伯、阿拉伯聯合大公國、土耳其、南非、埃及、奈及利亞以及其他中東和非洲國家)進行細分。市場預測以美元計價。

中東及非洲紙板市場趨勢及洞察

塑膠替代和包裝法規帶來的利好

阿拉伯聯合大公國2022年第380號部長令第二階段於2026年1月1日生效,禁止進口、生產及貿易塑膠飲料杯及杯蓋、刀叉餐具、食品容器及餐盤。這些產品均可直接取代紡織品。這一轉變導致許多餐飲服務和外帶企業對紙板的需求發生變化,從自願的永續性選擇轉變為受監管要求驅動的採購。這種壓力並非均勻分佈在整個供應鏈中,因為大規模加工商比小規模工廠更容易證明其產品的可追溯性、材料成分和生產一致性。這種差異增強了獲得認證的本地加工商的地位,他們無需經歷冗長的認證流程即可滿足跨國公司的採購標準。此外,在產品與食品直接接觸的情況下,對更合適的等級選擇、更清潔的表面和更穩定的加工性能的需求也日益成長。由於這項監管變化,中東和非洲的紙板市場正經歷短期需求成長。這是因為,在一些顯而易見的消費品應用中,包裝重新設計正在取得進展,而不是簡單的材料減少。

包裝食品消費量增加

包裝食品消費量的成長仍然是該地區最廣泛的需求基礎。這一點在那些因都市化、現代零售商店發展以及家庭生活節奏加快而導致日常購買行為變化的地區尤為明顯。隨著家庭規模縮小和用於準備生鮮食品的時間減少,即食、常溫保存和注重便利性的食品形式,尤其是那些在初級和二級包裝鏈中使用紙板的食品,正變得越來越受歡迎。這一趨勢意義重大,因為塑膠法規迫使多個品類的品牌所有者重新設計其包裝結構,而不僅僅是調整材料。當生產商需要食品接觸相容性、更佳的展示效果以及在大規模加工中可靠的加工性能時,折疊紙板和食品服務用紙板是最有利的選擇。土耳其作為海灣合作理事會(GCC)分銷路線上的主要紙板加工國和包裝食品供應商,在加工方面具有優勢。因此,儘管原料成本波動和進口競爭給加工商的盈利帶來壓力,但中東和非洲的紙板市場仍保持著強勁的消費動能。

進口紙漿和紙板價格波動

中東和非洲的紙板市場仍然嚴重依賴進口紙漿、再生纖維和成品紙板,導致加工商的利潤率與全球價格週期密切相關。歐洲和亞洲產能的增加、生產商面臨的外匯波動以及運輸瓶頸,都可能由於當地原料供應有限而立即影響區域投入成本。邁耶·梅爾霍夫公司在2026年第一季財報中指出,中東的地緣政治緊張局勢給能源、運輸和化學工業帶來了巨大的成本壓力。該公司2025年的財報也強調了其位於中東的兩家包裝廠面臨營運中斷的風險。這些衝擊發生的時機與價格水平同樣重要,因為紙板成本的調整通常會在日常消費品(FMCG)客戶接受更高的包裝價格之前就影響到加工商。這種時間滯後會擠壓利潤率,削弱現金流,並使小規模企業相比擁有穩定客戶合約的大型加工商面臨更大的風險。在這種情況下,中東和非洲的紙板市場可能會繼續成長,但收入波動性可能會進一步增加,具體取決於產品等級、加工商規模和進口路線。

細分市場分析

截至2025年,可折疊紙板將佔據38.32%的市場佔有率,在中東和非洲紙板市場中佔據主導地位。這是因為可折疊紙板適用於食品、個人護理和醫療保健行業的紙盒包裝,並符合廣泛認可的規格標準。其在剛性、印刷品質和食品接觸適用性方面的平衡使其成為大眾市場和高階零售通路的核心產品,滿足了對展示效果和合規性的需求。此外,隨著品牌所有者越來越重視衛生、材料完整性和穩定的加工性能,採用原生紙漿表面的趨勢也推動了可折疊紙板的發展。在中東和非洲紙板產業,即使原料價格上漲,可折疊紙板仍是許多二次包裝應用的首選材料。從歐洲進口仍然至關重要。 2026年4月,Metsa Board指出,中東地區的地緣政治緊張局勢正在推高物流成本和某些原物料成本,預計未來幾季將產生進一步的影響。

漂白實心紙板的複合年成長率高達7.53%,是所有產品等級中成長最快的。這主要得益於醫藥包裝、高階化妝品紙盒和高階食品服務應用對紙張亮度、潔淨度和精準印刷效果的需求。液體包裝紙板的市場趨勢相對穩定,這主要得益於與乳製品和果汁生產商簽訂的長期無菌包裝契約,而非短期現貨採購。利樂公司在阿拉伯聯合大公國投資興建梅里哈乳品廠,顯示新的加工和填充設施如何持續推動該地區對常溫乳製品和果汁紙盒的需求。白襯塑合板和未漂白實心紙板仍然用於對成本和強度要求較高的應用領域,但受目前席捲中東和非洲紙板市場的高階合規要求的影響相對較小。等級組成的多樣化表明,採購決策正從單純基於價格轉向基於功能規格,尤其是在監管日益嚴格、出口標籤標準和產品安全要求日益嚴格的地區。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 塑膠替代和包裝法規帶來的利多。

- 包裝食品消費量增加

- 乳製品和果汁業對飲料紙盒的需求

- 藥品和醫療保健包裝的在地化

- 擴大清真認證食品的出口

- 在高溫氣候下,優先選擇可在室溫下儲存的紙箱。

- 市場限制因素

- 進口紙漿和紙板價格波動

- 可回收纖維供應不足,收集基礎設施不完善。

- 紅海和長途貨運中斷

- 轉換器所面臨的電力、水和貨幣的嚴重性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 固體漂白紙板

- 固體未漂白紙板

- 折疊紙板

- 球場用球的白色底面

- 用於液體包裝的紙板

- 食品服務用紙板

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Metsa Board Corporation

- Billerud Aktiebolag(publ)

- Holmen AB

- Sappi Limited

- Graphic Packaging International, LLC

- Tetra Pak International SA

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Hotpack Holding and Investment Ltd

- Takamul Industrial Company

- United Carton Industries Company

- Arabian Packaging LLC

- Emirates Printing Press LLC

- Universal Carton Industries LLC

- Napco National

- Al Bayader International LLC

- Bony Packaging LLC

- Nampak Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and africa cartonboard market size was valued at USD 3.54 billion in 2025 and is estimated to grow from USD 3.71 billion in 2026 to reach USD 4.58 billion by 2031, at a CAGR of 4.30% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, and More), Packaging Format (Folding Cartons, Liquid Packaging, and More), End-User Industry (Food, Beverage, and More), and Geography (Saudi Arabia, United Arab Emirates, Turkey, South Africa, Egypt, Nigeria, and Rest of Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Cartonboard Market Trends and Insights

Plastic Substitution And Packaging Regulation Tailwinds

The UAE's second phase under Ministerial Decision No. 380 of 2022 became effective on January 1, 2026, and it prohibited the import, manufacture, and trade of plastic beverage cups and lids, cutlery, food containers, and plates, all of which map directly to fiber-based alternatives. That shift turns cartonboard demand into a compliance-driven purchase rather than a voluntary sustainability option for many foodservice and take-away formats. The pressure is not falling evenly across the supply base, because larger converters can document traceability, material composition, and production consistency more easily than smaller facilities. That difference improves the position of certified regional converters that can meet multinational procurement standards without long qualification cycles. It also increases the need for better grade selection, cleaner surfaces, and more stable converting performance where direct food contact is involved. The Middle East and Africa cartonboard market receives a near-term demand lift from this regulatory shift because packaging redesign is replacing simple material reduction in several visible consumer applications.

Rising Packaged Food Consumption

Rising packaged food consumption continues to provide the broadest demand base for the region, especially where urban growth, modern retail rollout, and busier household routines are changing everyday purchase behavior. Smaller households and less time for fresh meal preparation are supporting ready-to-eat, shelf-stable, and convenience-led food formats that use cartons in primary and secondary packaging chains. This trend matters because plastic restrictions are pushing brand owners in several categories to redesign packaging structures rather than make minor material changes. Folding Boxboard and food service board benefit most where producers want food-contact acceptance, stronger shelf appearance, and dependable converting performance at scale. Turkey adds a useful processing dimension because it serves as both a large converter of cartonboard and a packaged food supplier into GCC channels. The Middle East and Africa cartonboard market therefore keeps a strong consumption floor even when input cost volatility and import competition complicate converter profitability.

Imported Pulp And Board Price Volatility

The Middle East and Africa cartonboard market remains heavily exposed to imported pulp, recycled fiber, and finished board, which keeps converter margins closely tied to global price cycles. Capacity additions in Europe and Asia, producer currency moves, and shipping bottlenecks can all reach local input costs quickly because the region has limited ability to offset them with local raw material depth. Mayr-Melnhof said in its Q1 2026 trading statement that geopolitical tensions in the Middle East were creating noticeable cost pressure on energy, transportation, and chemicals, while its 2025 results also flagged interruption risk for its 2 Middle Eastern packaging plants. The timing of these shocks matters just as much as the price level, because board cost resets often reach converters before FMCG customers accept packaging price increases. That gap compresses margins, weakens cash flow, and leaves smaller operators more exposed than scale converters with stronger customer contracts. The Middle East and Africa cartonboard market can keep growing under these conditions, but returns become more uneven across product grades, converter sizes, and import corridors.

Other drivers and restraints analyzed in the detailed report include:

- Beverage Carton Demand From Dairy And Juice

- Pharmaceutical And Healthcare Packaging Localization

- Limited Recovered Fiber And Collection Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 38.32% of the market in 2025, giving it the largest role in the Middle East and Africa cartonboard market because it fits food, personal care, and healthcare cartons with a broadly accepted specification base. Its balance of stiffness, print quality, and food-contact suitability keeps it central where shelf appeal and compliance need to coexist inside mass-market and premium retail channels. The grade also benefits from the shift toward virgin-fiber surfaces, since brand owners are placing more weight on hygiene, material integrity, and consistent converting performance. In the Middle East and Africa cartonboard industry, this makes Folding Boxboard the commercial default for many secondary packs even when raw material prices move higher. Imported European supply still matters heavily, and Metsa Board said in April 2026 that geopolitical tensions in the Middle East were increasing logistics and certain raw material costs, with further effects expected in later quarters.

Solid Bleached Board is expanding at a 7.53% CAGR, the fastest among product grades, because pharmaceutical packs, premium cosmetics cartons, and higher-end foodservice applications need brightness, cleanliness, and precise print results. Liquid Packaging Board remains steadier, supported by long-term aseptic relationships with dairy and juice producers rather than short-cycle spot buying. Tetra Pak's investment at the UAE's Meliha Dairy Factory shows how new processing and filling assets continue to reinforce ambient dairy and juice carton demand in the region. White-Lined Chipboard and Solid Unbleached Board still serve cost-led and strength-led applications, but they are less exposed to the premium compliance pull that now shapes the Middle East and Africa cartonboard market. The broader grade mix shows a move away from purely price-based buying and toward function-based specification, especially where regulatory scrutiny, export presentation standards, and product safety demands are rising.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Metsa Board Corporation

- Billerud Aktiebolag (publ)

- Holmen AB

- Sappi Limited

- Graphic Packaging International, LLC

- Tetra Pak International S.A.

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Hotpack Holding and Investment Ltd

- Takamul Industrial Company

- United Carton Industries Company

- Arabian Packaging LLC

- Emirates Printing Press LLC

- Universal Carton Industries LLC

- Napco National

- Al Bayader International LLC

- Bony Packaging LLC

- Nampak Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic Substitution and Packaging Regulation Tailwinds

- 4.3.2 Rising Packaged Food Consumption

- 4.3.3 Beverage Carton Demand From Dairy and Juice

- 4.3.4 Pharmaceutical and Healthcare Packaging Localization

- 4.3.5 Halal-Certified Food Export Expansion

- 4.3.6 Hot-Climate Preference for Shelf-Stable Cartons

- 4.4 Market Restraints

- 4.4.1 Imported Pulp and Board Price Volatility

- 4.4.2 Limited Recovered Fiber and Collection Infrastructure

- 4.4.3 Red Sea and Long-Haul Freight Disruptions

- 4.4.4 Power, Water, and Currency Stress on Converters

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Geography

- 5.4.1 Middle East

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Turkey

- 5.4.1.4 Rest of Middle East

- 5.4.2 Africa

- 5.4.2.1 South Africa

- 5.4.2.2 Egypt

- 5.4.2.3 Nigeria

- 5.4.2.4 Rest of Africa

- 5.4.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton AG

- 6.4.2 Stora Enso Oyj

- 6.4.3 Metsa Board Corporation

- 6.4.4 Billerud Aktiebolag (publ)

- 6.4.5 Holmen AB

- 6.4.6 Sappi Limited

- 6.4.7 Graphic Packaging International, LLC

- 6.4.8 Tetra Pak International S.A.

- 6.4.9 Nippon Paper Industries Co., Ltd.

- 6.4.10 Oji Holdings Corporation

- 6.4.11 Hotpack Holding and Investment Ltd

- 6.4.12 Takamul Industrial Company

- 6.4.13 United Carton Industries Company

- 6.4.14 Arabian Packaging LLC

- 6.4.15 Emirates Printing Press LLC

- 6.4.16 Universal Carton Industries LLC

- 6.4.17 Napco National

- 6.4.18 Al Bayader International LLC

- 6.4.19 Bony Packaging LLC

- 6.4.20 Nampak Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)