|

市場調查報告書

商品編碼

2072772

法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)France Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

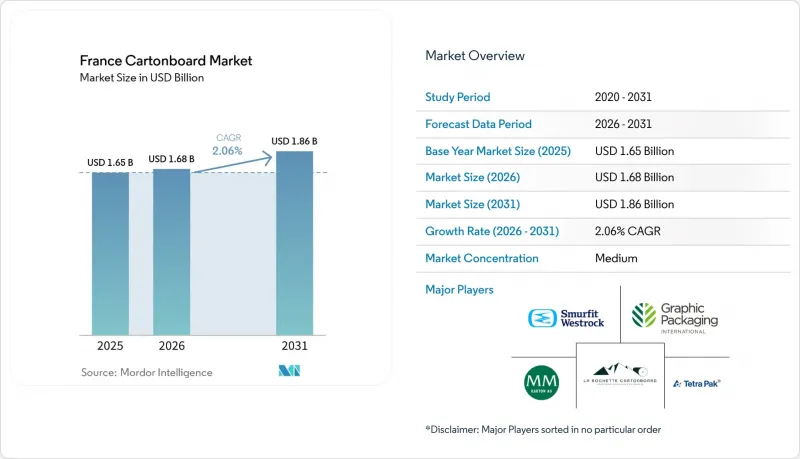

根據 Mordor Intelligence 預測,法國紙板市場規模預計在 2025 年達到 16.5 億美元,2026 年達到 16.8 億美元,到 2031 年達到 18.6 億美元,2026 年至 2031 年的複合年成長率為 2.06%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套和托盤等)以及最終用戶行業(食品、飲料、醫藥保健、煙草等)進行細分。市場預測以美元計價。

法國紙板市場的趨勢與洞察

基於AGEC和PPWR的塑膠纖維替代品

在預測期內,從塑膠轉向纖維將為法國紙板市場提供最持久的需求支撐。歐盟包裝和包裝廢棄物法規(AGEC)將於2025年2月11日生效,並於2026年8月12日起實施。這將使紙板在必須在2030年前證明其可回收性的包裝形式方面擁有更強的合規優勢。法國的AGEC法規也透過國家關於一次性塑膠包裝的法規強化了類似的方向,其中包括禁止重量低於1.5公斤的新鮮水果和蔬菜。這些協同效應為品牌所有者提供了較長的過渡期,使其能夠以纖維為主要材料重新設計包裝,而無需等待未來的合規期限。法國紙板市場受益於單一材料紙板解決方案比多層塑膠結構更容易在新法律規範內定位。此外,法國加工商在 AGEC 法案下已積累了包裝重新設計方面的早期經驗,使他們能夠快速響應客戶需求,並在更多應用轉向可回收紙板形式時提高利潤率。

即食食品和生鮮食品類別的食品包裝需求

食品仍然是法國紙板市場的主要需求來源,即食食品和生鮮食品的需求進一步增強了其穩定性。乳製品、烘焙食品、生鮮食品、冷凍食品和常溫食品的應用已構成全國紙板使用的基礎。隨著食品製造商轉向更可回收的包裝,用於折疊盒的紙板正被用於套筒、托盤和與食品直接接觸的結構中,以滿足展示和搬運的需求。這種轉變的初期階段在AGEC(法國通用電氣包裝法規)下塑膠替代相對容易的應用領域最為明顯,但在冷藏食品領域仍有進一步轉型的空間。這導致需求模式更加選擇性,消費者更傾向於選擇那些能夠在可回收紙板系統中兼具防潮性、印刷品質和可靠的食品包裝性能的供應商。因此,法國紙板市場受益於食品需求的成長,這不僅體現在包裝日益普及,也體現在朝向更專業化的等級和加工能力的逐步轉變。

紙漿、再生纖維和能源成本波動很大

原料成本波動仍然是法國紙板市場面臨的最緊迫挑戰。 Mayer Melnhof公司在2026年第一季財報中指出,當前商業環境的特徵是需求疲軟、結構性供應過剩和競爭激烈,並指出地緣政治壓力正在蔓延至能源、運輸和化學品成本。 Metsä Board公司也在2026年4月宣布,由於伊朗局勢導致原油和天然氣價格飆升,預計其2026年第二季度營業利潤將減少1000萬歐元,這表明外部衝擊對紙板行業盈利的影響之迅速。這些壓力在法國紙板市場尤為顯著,因為加工商被迫在利潤率受到擠壓的情況下,在客戶仍然期望服務可靠性和符合技術要求的環境下競爭。成本波動也會影響產品組合,因為當再生纖維和能源成本同時波動時,再生纖維等級受到的影響更為顯著。因此,擁有更優越的技術能力或更一體化結構的供應商將比缺乏定價和採購能力的小規模加工商更具優勢。

細分市場分析

2025年,可折疊紙板在法國紙板市場佔據42.25%的佔有率,並持續保持其市場領先地位。這一地位反映了其在食品、醫藥、家居用品和電子商務等眾多行業的廣泛應用,在這些行業中,可印刷性、剛性和可回收性都是日常商業決策的重要考慮因素。實心漂白紙板是成長最快的等級,預計到2031年將以5.19%的複合年成長率成長。這顯示法國紙板產業的價值重心正向高階應用領域轉移。這種轉變並非主要源於銷售的簡單成長,而是由於奢侈品、醫藥和高階食品產業的客戶對其原料進行了升級。因此,即使總噸位沒有顯著變化,高階紙板在法國紙板市場中的佔有率(以以金額為準)也在不斷擴大。

斯道拉恩索(Stora Enso)於2025年9月推出的「Ensovelvet」系列產品,清晰地展現了供應商如何透過專為高階香水和個人保健產品包裝設計的SBS等級紙板來應對這一趨勢。斯莫菲特韋斯特羅克(Smurfit Westrock)於2026年2月關閉了其La Touque SBS生產線,這是其旨在供應更高規格SBS紙板而非擴大通用產品產能的投資組合策略的一部分。白襯紙板仍然與價格敏感型應用密切相關,並且在能源成本和塗層法規難以滿足時更容易受到衝擊。未漂白固態紙板在餐飲服務和工業應用中仍然發揮著重要作用,在這些應用中,強度比外觀更為重要;而液體包裝紙板和餐飲用紙板則受益於人們逐漸減少塑膠容器的使用。從實際角度來看,法國紙板市場重視那些兼具表面品質、應對力法規要求和可靠交貨的認證原生紙漿供應商,這使他們能夠滿足僅靠低成本紙板無法滿足的終端用戶需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- AGEC和PPWR下的塑膠纖維替代

- 即食食品和生鮮食品類別的食品包裝需求

- 高階美容和奢侈品對瓦楞紙板的需求。

- 醫療領域對序列化和合規包裝的需求

- EPR 生態調節獎勵計畫:設計瓦楞紙箱時考慮到回收。

- 奢侈品電商領域最佳化規模和減少空置空間的需求

- 市場限制因素

- 紙漿、再生纖維和能源成本波動很大

- 一種靈活輕便的形式,可作為特定應用的替代方案。

- 油墨、塗料和黏合劑中遷移測試的負擔

- 國內加工能力不足,依賴進口

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 實心漂白板

- 未漂白飾面

- 折疊紙板

- 白色襯裡塑合板

- 液體包裝板

- 餐飲服務業的董事會

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務業的容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International, LLC

- La Rochette Cartonboard SAS

- Tetra Pak International SA

- SIG Group AG

- Elopak ASA

- Metsa Board Corporation

- Stora Enso Oyj

- Billerud AB

- Autajon Group

- Verpack

- FP PACK

- TPG PACK

- SODEPRINT

- Cartonnages Vaillant

- Groupe Lacroix

- Huhtamaki Oyj

- Sonoco Products Company

- Holmen AB

第7章 市場機會與未來展望

According to Mordor Intelligence, the france cartonboard market size is projected to be USD 1.65 billion in 2025, USD 1.68 billion in 2026, and reach USD 1.86 billion by 2031, growing at a CAGR of 2.06% from 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, Pharmaceutical and Healthcare, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Cartonboard Market Trends and Insights

Plastic-To-Fiber Substitution Under AGEC and PPWR

Plastic-to-fiber substitution is the most durable demand support for the France cartonboard market over the forecast period. The EU Packaging and Packaging Waste Regulation entered into force on February 11, 2025, and applies from August 12, 2026, which gives cartonboard a stronger compliance position in packaging formats that must demonstrate recyclability by 2030. France's AGEC law has been reinforcing the same direction through national restrictions on single-use plastic packaging, including the ban that France implemented for fresh fruit and vegetables below 1.5 kg. This combination has created a long transition window in which brand owners can redesign packs around fiber rather than wait for a later compliance deadline. The France cartonboard market benefits because mono-material paperboard solutions are easier to position within the new regulatory framework than multilayer plastic structures. French converters also enter this phase with earlier redesign experience under AGEC, which supports faster customer response and better margin capture as more applications move toward recyclable board formats.

Food Packaging Demand From Ready-To-Eat and Fresh Categories

Food remains a core volume base for the France cartonboard market, and demand from ready-to-eat and fresh categories is adding to that stability. Dairy, bakery, fresh produce, frozen meals, and ambient food applications already anchor cartonboard use across the country. As food producers shift more packaging into recyclable formats, folding boxboard is being used in sleeves, trays, and direct-contact structures that support both shelf presentation and handling needs. The early phase of conversion has been strongest in applications where plastic replacement is easier to execute under AGEC, while chilled formats still offer room for further migration. That creates a more selective demand pattern, where value moves toward suppliers that can handle moisture resistance, print quality, and reliable food-packaging performance within recyclable board systems. The France cartonboard market therefore gains from food demand not only through broader pack adoption, but also through a gradual move toward more specialized grades and converting capability.

Volatile Pulp, Recovered Fiber, And Energy Costs

Input cost volatility remains the most immediate brake on the France cartonboard market. Mayr-Melnhof's Q1 2026 trading statement described the operating backdrop as subdued demand, structural overcapacity, and intense competition, with geopolitical pressure feeding through energy, transport, and chemical costs. Metsa Board also stated in April 2026 that rising oil and natural gas prices linked to the Iran conflict were expected to reduce its Q2 2026 operating result by EUR 10 million, which shows how quickly external shocks move into paperboard economics. In the France cartonboard market, these pressures are especially important because converters compete in an environment where customers still expect service reliability and technical compliance even when margins tighten. Cost volatility also affects product mix, since recycled-fiber grades are more exposed when both recovered fiber and energy costs move at the same time. This leaves technically stronger or more integrated suppliers better placed than smaller converters that lack pricing power or procurement leverage.

Other drivers and restraints analyzed in the detailed report include:

- Premium Beauty And Luxury Carton Demand

- Healthcare Serialization And Compliance Packaging Demand

- Alternative Flexible And Lightweight Formats In Selected Uses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 42.25% of France cartonboard market share in 2025, which kept it as the leading product grade in the France cartonboard market. Its position reflects broad use across food, pharmaceuticals, household goods, and e-commerce, where printability, stiffness, and recyclability all matter in everyday commercial decisions. Solid Bleached Board is the fastest-growing grade and is forecast to rise at 5.19% CAGR through 2031, which shows how much value is moving toward higher-specification applications in the France cartonboard industry. This shift is tied less to simple volume growth and more to substrate upgrading by luxury, pharmaceutical, and premium food customers. The France cartonboard market is therefore seeing premium grades gain share in value terms even when total tonnage does not change sharply.

Stora Enso's Ensovelvet launch in September 2025 is a clear example of how suppliers are targeting this movement with SBS grades designed for premium fragrance and personal care packaging. The closure of the La Tuque SBS machine in February 2026 by Smurfit Westrock was a portfolio move toward higher-specification SBS supply rather than broader commodity capacity. White-Lined Chipboard remains tied more closely to price-sensitive applications, and that leaves it more exposed when energy costs and coating compliance become harder to manage. Solid Unbleached Board still holds a role in food-service and industrial uses where strength matters more than appearance, while liquid packaging board and food-service board benefit from the ongoing replacement of plastic-based formats. In practical terms, the France cartonboard market is rewarding certified virgin-fiber suppliers that can combine surface quality, regulatory readiness, and dependable delivery across end uses that now require more than low-cost board alone.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International, LLC

- La Rochette Cartonboard SAS

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Metsa Board Corporation

- Stora Enso Oyj

- Billerud AB

- Autajon Group

- Verpack

- FP PACK

- TPG PACK

- SODEPRINT

- Cartonnages Vaillant

- Groupe Lacroix

- Huhtamaki Oyj

- Sonoco Products Company

- Holmen AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Plastic-to-Fiber Substitution Under AGEC and PPWR

- 4.3.2 Food Packaging Demand from Ready-to-Eat and Fresh Categories

- 4.3.3 Premium Beauty and Luxury Carton Demand

- 4.3.4 Healthcare Serialization and Compliance Packaging Demand

- 4.3.5 EPR Eco-Modulation Rewards Design-for-Recycling Cartons

- 4.3.6 Luxury E-Commerce Right-Sizing and Void Reduction Needs

- 4.4 Market Restraints

- 4.4.1 Volatile Pulp, Recovered Fiber, and Energy Costs

- 4.4.2 Alternative Flexible and Lightweight Formats in Selected Uses

- 4.4.3 Migration Testing Burden for Inks, Coatings, and Adhesives

- 4.4.4 Domestic Converting Capacity Gaps and Import Dependence

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International, LLC

- 6.4.4 La Rochette Cartonboard SAS

- 6.4.5 Tetra Pak International S.A.

- 6.4.6 SIG Group AG

- 6.4.7 Elopak ASA

- 6.4.8 Metsa Board Corporation

- 6.4.9 Stora Enso Oyj

- 6.4.10 Billerud AB

- 6.4.11 Autajon Group

- 6.4.12 Verpack

- 6.4.13 FP PACK

- 6.4.14 TPG PACK

- 6.4.15 SODEPRINT

- 6.4.16 Cartonnages Vaillant

- 6.4.17 Groupe Lacroix

- 6.4.18 Huhtamaki Oyj

- 6.4.19 Sonoco Products Company

- 6.4.20 Holmen AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)