|

市場調查報告書

商品編碼

2072690

新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Singapore Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

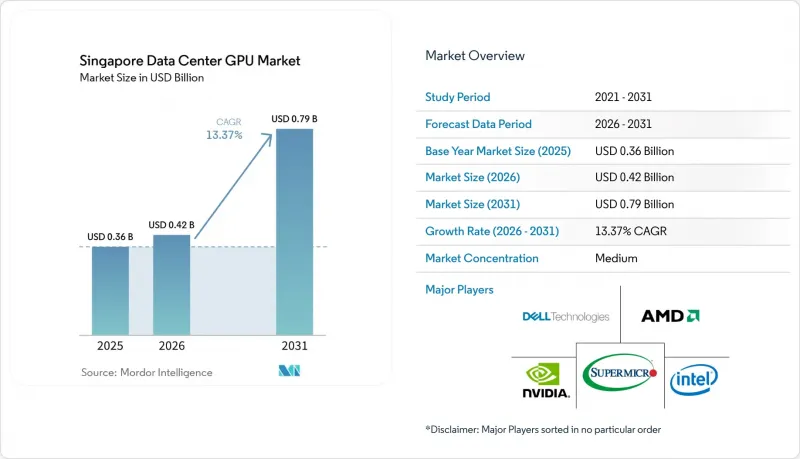

據 Mordor Intelligence 稱,新加坡資料中心 GPU 市場預計到 2026 年價值 4.2 億美元,從 2025 年的 3.6 億美元成長到 2031 年的 7.9 億美元,預計 2026 年至 2031 年的複合年成長率將達到 13.37%。

本報告按部署類型(雲端資料中心、企業/私人資料中心等)、GPU 類型(訓練 GPU、推理 GPU)、互連方式(基於 PCIe 的 GPU、高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算等)以及最終用戶(超大規模資料中心業者伺服器/雲端服務供應商、企業、政府機構、研究機構)進行細分。市場預測以美元計價。

新加坡資料中心GPU市場趨勢與洞察

對生成式人工智慧和LLM培訓的需求激增

訓練大規模語言模型 (LLM) 是推動新型 GPU叢集部署的最大動力。 ASPIRE 2A+超級電腦上的 320 個 NVIDIA H100 GPU 將 MERaLiON 模型的訓練時間從 340 天縮短到不到 6 天,充分展現了高密度加速器帶來的顯著生產力提升。自主人工智慧舉措如今需要本地處理能力來維護資料駐留,各機構正在部署 B200 DGX SuperPOD 來處理前沿工作負載。像 Firmus AI 這樣的區域模型開發公司已經預訂了數百個 H200 GPU,預訂週期長達數月,這種需求模式無法透過現貨市場滿足。大學叢集支援的應用遠不止自然語言處理,還包括影片生成人工智慧、手術輔助人工智慧和材料科學等領域。隨著模型規模的成長,互連頻寬和記憶體容量對架構選擇至關重要,這進一步加速了向 InfiniBand 架構的過渡。

新加坡超大規模資料中心業者擴張及預分配容量

微軟、亞馬遜網路服務(AWS)和Google已在2024年至2029年間總合投資超過190億美元用於新加坡的資料中心建設,其中大部分將用於建設GPU密集型可用區。吉寶資料中心房地產投資信託基金(Keppel DC REIT)2025會計年度來自超大規模資料中心業者的租金收入佔其總收入的69.3%,租金漲幅高達45%,顯示雲端巨頭願意為水冷資料中心支付租金。 DC-CFA2計畫200兆瓦的容量上限,加上2026年3月的建設截止日期,引發了土地爭奪戰,迫使超大規模資料中心業者大規模資料中心營運商簽訂多年合約。將現有機房改造為GPU機房的資產支援型專案正在加速推進,例如以14億新元收購KDC新加坡7號和8號機房。儘管鄰國馬來西亞擁有更實惠的資料中心,但這些發展鞏固了新加坡作為區域人工智慧中心的地位。

土地和電力限制了新建設施。

新加坡的太陽能發電項目建設凍結令雖因DC-CFA2招標而部分解除,但仍將擴建規模限制在200兆瓦以內,並強制要求可再生能源佔比達到50%,導致機架密度最高僅120千瓦。空間不足造成冷卻、電力和結構方面的複雜性,從而延長了專案工期。儘管營運商透過在馬來西亞和澳洲購置產能來規避風險,但對延遲敏感的人工智慧推理技術仍集中在新加坡。跨境可再生能源進口仍存在不確定性,而屋頂空間有限也限制了太陽能發電量,預計這項限制將持續到2026年後。

細分市場分析

到2025年,雲端資料中心將佔據新加坡資料中心GPU市場佔有率的67.42%。這反映了超大規模資料中心業者資料中心的規模經濟優勢及其簽訂多年可再生能源購買協議的能力。同時,邊緣資料中心被認為是成長最快的細分市場,到2031年複合年成長率將達到16.94%。隨著微軟和AWS鎖定未來數年的GPU空間,市場集中度進一步加劇,託管費用也飆升至每千瓦每月480美元的高點。為因應金融服務業日益嚴格的資料居住要求,企業級私有雲端強勢回歸,各大銀行紛紛在Tier 4級設施內建立本地GPU區域。邊緣基礎建設成長最為迅猛,這主要得益於大士的自動駕駛汽車測試跑道以及港口對低於10毫秒延遲要求極高的即時分析應用。

預計2026年,新加坡資料中心GPU市場將出現雲端服務供應商在現有機房中加裝浸沒式冷卻槽,而邊緣運算專家則在5G基地台附近部署6千瓦預製模組。 Nxera的電纜登陸整合模式透過提供具有雲端級吞吐量的區域級推理處理,進一步模糊了核心與邊緣之間的界限。大學和政府研究實驗室繼續建造用於自主工作負載的國內叢集,這將推動絕對容量的成長,而雲端佔有率預計將略有下降。

2025年新加坡資料中心GPU市場中,推理設備佔據56.93%的市場佔有率,成為此細分市場的主要驅動力,主要得益於面向客戶的聊天機器人、詐欺偵測系統數位雙胞胎等應用程式對低延遲回應的需求。同時,訓練GPU在整個預測期內保持最高的成長率,到2031年複合年成長率將達到17.45%。銀行採用了功率上限為60瓦的H100 NVL卡,以便安裝在現有的空調管道中;而物流公司則將L40S闆卡標準化用於電腦視覺。然而,訓練加速器的成長速度最快,因為大規模語言模型的開發者搶購了H200和早期Blackwell的配額。

新加坡資料中心GPU市場佔有率已轉向訓練領域,公共部門買家訂購了用於國家安全語言模型的DGX SuperPOD。儘管多租戶限制使得私有雲端僅限於推理機架,但GB200級系統新增的隔離功能將從2027年起支援混合工作負載叢集。此外,訓練需求預計將推動統一記憶叢集的普及,從而確保這兩種類型的GPU將日益共存而非競爭。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對生成式人工智慧和LLM培訓的需求激增

- 新加坡超大規模資料中心業者業務擴張及預分配容量

- 政府對綠色資料中心的激勵措施

- 企業快速採用人工智慧工作負載

- 一個分散式GPUaaS平台,用於彌補容量缺口。

- 透過整合電纜登陸設施和資料中心來降低延遲。

- 市場限制因素

- 土地和電力限制制約了新設施的建設。

- 全球GPU供應限制與價格波動

- 液冷作業領域熟練勞動力短缺

- 對用水情況的審查可能會影響設施許可證

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 依類型互連

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧和機器學習

- 高效能運算(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Super Micro Computer, Inc.

- ASUStek Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- xFusion Digital Technologies Co., Ltd.

- Equinix, Inc.

- Digital Realty Trust, Inc.

- ST Telemedia Global Data Centres

- Keppel DC REIT

- Singtel Group(Nxera)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Aethir Pte. Ltd.

第7章 市場機會與未來展望

第8章 市場機會與未來展望

- 評估閒置頻段和未滿足的需求

According to Mordor Intelligence, the singapore data center GPU market size was valued at USD 0.42 billion in 2026 and is estimated to grow from USD 0.36 billion in 2025 to reach USD 0.79 billion by 2031, advancing at a 13.37% CAGR over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and More), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government, and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

Singapore Data Center GPU Market Trends and Insights

Surge in Generative AI and LLM Training Demand

Large language model training has become the single biggest catalyst for new GPU clusters. The ASPIRE 2A+ supercomputer's 320 NVIDIA H100 GPUs cut the MERaLiON model's training time from 340 days to under 6 days, proving the productivity leap enabled by dense accelerators. Sovereign AI initiatives now require on-premises capacity to maintain data residency, prompting agencies to deploy B200 DGX SuperPODs for frontier workloads. Regional model builders such as Firmus AI reserve hundreds of H200 GPUs for months, a demand pattern spot markets cannot match.University clusters support video generative AI, surgical intelligence, and materials science, broadening use cases beyond natural language processing. As model sizes swell, interconnect bandwidth and memory capacity dictate architectural choices, reinforcing the shift to InfiniBand fabrics.

Hyperscaler Expansion and Pre-Committed Capacity in Singapore

Microsoft, Amazon Web Services, and Google have collectively earmarked more than USD 19 billion for Singapore builds between 2024 and 2029, with a disproportionate share targeting GPU-dense availability zones. Keppel DC REIT's hyperscaler rent climbed to 69.3% of revenue in fiscal 2025, and rental reversions reached 45%, signaling that cloud giants will pay premiums for liquid-cooled halls. The DC-CFA2 program's 200-megawatt cap, coupled with a March 2026 build deadline, triggered a land rush that locked hyperscalers into multi-year commitments. Asset-backed conversions of legacy halls into GPU rooms accelerated, highlighted by KDC Singapore 7 and 8's SGD 1.4 billion purchase. These moves cement Singapore as the region's AI gravity center despite more affordable capacity in neighboring Malaysia.

Land and Power Caps Limiting New Facilities

Singapore's moratorium, lifted only partially through the DC-CFA2 call, restricts expansion to 200 megawatts and mandates 50% renewable energy, forcing rack densities up to 120 kilowatts. Space scarcity drives cooling, electrical, and structural complexities that lengthen project timelines. Operators hedge by securing capacity in Malaysia and Australia, but latency-sensitive AI inference still gravitates to Singapore. Cross-border renewable imports remain uncertain, and solar yield is capped by limited rooftop real estate, sustaining the constraint beyond 2026.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Green Data Centers

- Rapid Enterprise Adoption of AI Workloads

- Global GPU Supply Constraints and Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers captured 67.42% of the Singapore data center GPU market size in 2025, reflecting hyperscaler scale economics and their ability to sign multi-year renewable power purchase agreements, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031. The concentration deepened as Microsoft and AWS reserved GPU halls years in advance, pushing colocation rates toward the upper end of USD 480 per kilowatt per month. Enterprise-class private clouds mounted a comeback once data residency clauses tightened in financial services, leading banks to carve out on-premises GPU zones inside Tier 4 facilities. Edge builds recorded the sharpest growth, driven by autonomous vehicle testing tracks in Tuas and live-stream analytics at the port, where sub-10-millisecond latency is mandatory.

In 2026, the Singapore data center GPU market sees cloud operators retrofit existing halls with immersion tanks while edge specialists deploy prefabricated 6-kilowatt pods near 5G base stations. Nxera's cable-landing integration model further blurs lines between core and edge by offering regional inference at cloud-class throughput. Universities and government labs continue to build in-country clusters for sovereign workloads, ensuring that the cloud's share edges down slightly even as absolute capacity rises.

Inference devices led the segment with 56.93% share of the Singapore data center GPU market in 2025 as customer-facing chatbots, fraud detectors, and digital twins demanded low-latency responses, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window. Banks opted for H100 NVL cards configured for 60-watt power caps to fit within legacy air corridors, while logistics firms standardized on L40S boards for computer vision. Training-class accelerators, however, posted the quickest growth as large language model developers locked in H200 and early Blackwell allocations.

The Singapore data center GPU market share tilted toward training when public-sector buyers ordered DGX SuperPODs for national security language models. Multi-tenancy constraints limited private clouds to inference-only racks, but new isolation features in GB200-class systems will allow mixed-workload clusters from 2027 onward. Training demand also spurred the adoption of unified memory clusters, ensuring that the two GPU types increasingly coexist rather than compete.

Complete Report Scope:

- By Deployment Type

- Cloud Data Centers

- Enterprise / Private Data Centers

- Edge Data Centers

- By GPU Type

- Training GPUs

- Inference GPUs

- By Interconnect

- PCIe-Based GPUs

- High-Bandwidth Interconnect GPUs

- By Workload Type

- Artificial Intelligence and Machine Learning

- High-Performance Computing (non-AI scientific computing)

- Data Analytics (database acceleration, query processing)

- Graphics and Visualization (VDI, rendering, digital twins)

- By End-User

- Hyperscalers / Cloud Service Providers

- Enterprises

- Government and Research Institutions

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Super Micro Computer, Inc.

- ASUStek Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Inspur Electronic Information Industry Co., Ltd.

- Fujitsu Limited

- Huawei Technologies Co., Ltd.

- xFusion Digital Technologies Co., Ltd.

- Equinix, Inc.

- Digital Realty Trust, Inc.

- ST Telemedia Global Data Centres

- Keppel DC REIT

- Singtel Group (Nxera)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Aethir Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Generative AI and LLM Training Demand

- 4.2.2 Hyperscaler Expansion and Pre-Committed Capacity in Singapore

- 4.2.3 Government Incentives for Green Data Centers

- 4.2.4 Rapid Enterprise Adoption of AI Workloads

- 4.2.5 Decentralized GPUaaS Platforms Filling Capacity Gaps

- 4.2.6 Integrated Cable-Landing Data Centers Lowering Latency

- 4.3 Market Restraints

- 4.3.1 Land and Power Caps Limiting New Facilities

- 4.3.2 Global GPU Supply Constraints and Price Volatility

- 4.3.3 Skilled Workforce Shortage in Liquid-Cooling Operations

- 4.3.4 Water-Use Scrutiny Impacting Facility Permits

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence and Machine Learning

- 5.4.2 High-Performance Computing (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Dell Technologies Inc.

- 6.4.5 Hewlett Packard Enterprise Company

- 6.4.6 Lenovo Group Limited

- 6.4.7 Super Micro Computer, Inc.

- 6.4.8 ASUStek Computer Inc.

- 6.4.9 GIGABYTE Technology Co., Ltd.

- 6.4.10 Inspur Electronic Information Industry Co., Ltd.

- 6.4.11 Fujitsu Limited

- 6.4.12 Huawei Technologies Co., Ltd.

- 6.4.13 xFusion Digital Technologies Co., Ltd.

- 6.4.14 Equinix, Inc.

- 6.4.15 Digital Realty Trust, Inc.

- 6.4.16 ST Telemedia Global Data Centres

- 6.4.17 Keppel DC REIT

- 6.4.18 Singtel Group (Nxera)

- 6.4.19 Amazon Web Services, Inc.

- 6.4.20 Microsoft Corporation

- 6.4.21 Google LLC

- 6.4.22 Aethir Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.1.1 Fujitsu Limited

- 7.1.2 Amazon Web Services, Inc. (Annapurna Labs)

- 7.1.3 Google LLC

- 7.1.4 Samsung Electronics Co., Ltd.

- 7.1.5 EVGA Corporation

- 7.1.6 Xilinx, Inc. (AMD)

- 7.1.7 Arm Ltd.

- 7.1.8 Tyan Computer Corporation

- 7.1.9 Synopsys, Inc.

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment

印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)