|

市場調查報告書

商品編碼

2065495

德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Germany Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

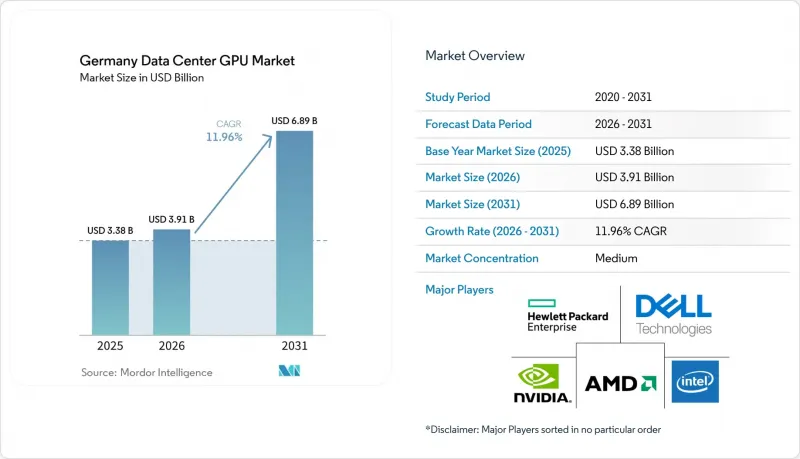

根據 Mordor Intelligence 預測,德國資料中心 GPU 市場預計將從 2025 年的 33.8 億美元成長到 2026 年的 39.1 億美元,到 2031 年達到 68.9 億美元,2026 年至 2031 年的複合年預計成長率為 11.96%。

本報告按部署類型(雲端資料中心、企業/私人資料中心等)、GPU 類型(訓練 GPU 和推理 GPU)、互連方式(基於 PCIe 的 GPU 和高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算、資料分析等)以及最終用戶(超大規模資料中心業者/雲端服務供應商、企業等)進行細分。市場預測以美元計價。

德國資料中心GPU市場的趨勢與洞察

德國企業對人工智慧工作負載的採用率不斷提高

SAP的工業人工智慧雲預計到2025年將與超過100家製造商簽訂契約,這將促使中型企業買家從資本採購轉向基於使用量的GPU合約。據Northern Data稱,到2025年第四季度,其H100和H200 GPU將透過預訂或按需合約的方式獲得保障,這標誌著企業對人工智慧的興趣已從單純的興趣轉向了切實的應用。 BMW正在利用其DGX Hopper叢集生成合成駕駛影像,從而顯著縮短感知模型的訓練時間。同時,金融服務業仍在繼續試行反詐欺模型,但由於歐盟人工智慧法的透明度要求,全面部署被推遲。

超大規模資料中心業者雲端營運商在法蘭克福和柏林擴展雲端區域

AWS 投資 88 億歐元(99 億美元)擴大其在法蘭克福的區域,但修訂後的電網法規要求新參與企業承擔變電站升級的全部費用。為此,Google斥資 55 億歐元(62 億美元)在迪岑巴赫建造了園區,以避免市中心變壓器堵塞。 AWS 投資 78 億歐元(88 億美元)在勃蘭登堡建造的主權雲端平台,旨在服務聯邦政府的工作負載,這表明營運商如何透過地理位置分離對延遲敏感的推理處理和批量訓練。

德國主要資料中心所在地電力成本高且電網受限

2024年,法蘭克福的中壓用戶將被迫繳納電網使用費。在柏林,總計2.8吉瓦的併網申請正在審核中,業者需承擔變電站全面維修的費用。這些維修將使工期延長18至36個月。

細分市場分析

預計到2031年,邊緣運算設施的複合年成長率將達到12.78%,這主要得益於汽車OEM廠商部署本地GPU叢集以將感知延遲降低到10毫秒以下的需求。 BMW慕尼黑研究中心正在使用DGX Hopper節點將合成影像生成速度提升了八倍,顯示私有邊緣機架正日益普及。

即使到了2025年,雲端資料中心仍佔總收入的58.76%,但由於法蘭克福電網容量限制和建設補貼的影響,進一步的建設速度有所放緩。 SAP的「主權人工智慧雲」結合了私有雲和公有雲模式,使製造商能夠在保持資料局部的同時,將處理工作外包出去。

到 2025 年,訓練 GPU 的支出將佔總支出的 55.72%。這是因為超大規模資料中心業者購入了 H100 和 H200 的資源,用於運行基礎模型。英特爾的「Gaudi 3」(可在 IBM 雲端的法蘭克福區域使用)據稱能夠比 H100 降低 50% 的推理成本,這也是為什麼推薦使用乙太網路架構而非 InfiniBand 的原因。

推理需求成長最快的領域是邊緣運算,在這個領域,每個插槽的能源效率和外形尺寸效率比峰值浮點運算效能更為重要。 AMD 的 MI300藍圖將每個 GPU 的 HBM 記憶體容量加倍,使其適用於主權雲端中記憶體受限的推理任務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 德國企業對人工智慧工作負載的採用率不斷提高

- 由於ESG法規的實施,對節能型GPU伺服器的需求正在擴大。

- 超大規模資料中心業者雲端營運商在法蘭克福和柏林擴展雲端區域

- 政府資助高效能運算和量子研究設施

- 自主製造領域對邊緣運算的需求日益成長

- 主權雲端舉措的興起正在推動本地GPU產能。

- 市場限制因素

- 德國主要資料中心所在地電力成本高且電網受限

- 對歐盟以外GPU製造商供應鏈的依賴

- 嚴格的資料保護和資料居住法規限制了跨境工作負載。

- 熟練的GPU程式設計師短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 透過連接方式

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Cerebras Systems Inc.

- Huawei Technologies Co. Ltd.

- Giga Computing Technology Co. Ltd.

- AsusTek Computer Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Deutsche Telekom AG

- T-Systems International GmbH

- Hetzner Online GmbH

- SAP SE

- Atos SE

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany data center GPU market size is expected to increase from USD 3.38 billion in 2025 to USD 3.91 billion in 2026 and reach USD 6.89 billion by 2031, growing at a CAGR of 11.96% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise / Private Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and More), and End-User (Hyperscalers/CSPs, Enterprises, and More). The Market Forecasts are Provided in Value (USD).

Germany Data Center GPU Market Trends and Insights

Growing Adoption of AI Workloads in German Enterprises

SAP's Industrial AI Cloud signed over 100 manufacturers in 2025, shifting mid-market buyers from capital purchases toward consumption-based GPU contracts. By Q4 2025, Northern Data revealed that its H100 and H200 GPUs were secured under reserved or on-demand agreements, highlighting a shift from speculative interest to firm enterprise commitments. BMW harnessed DGX Hopper clusters to produce synthetic driving images, slashing the training time for perception models. While financial services continue to test fraud-detection models, the rollout is delayed by transparency requirements under the EU AI Act.

Expansion of Hyperscaler Cloud Regions in Frankfurt and Berlin

AWS spent EUR 8.8 billion (USD 9.9 billion) expanding Frankfurt zones, yet new entrants must now fund 100% of substation upgrades under revised grid rules. Google countered with a EUR 5.5 billion (USD 6.2 billion) Dietzenbach campus that bypasses inner-city transformer congestion. AWS's EUR 7.8 billion (USD 8.8 billion) Brandenburg sovereign cloud, targeting federal workloads, shows operators are geographically splitting latency-sensitive inference and batch training.

High Electricity Costs and Grid Constraints in Major German Data Center Hubs

In 2024, medium-voltage users in Frankfurt faced network fees. With pending grid requests in Berlin totaling 2.8 GW, operators are now tasked with financing comprehensive substation upgrades. These upgrades extend the construction timeline by 18 to 36 months.

Other drivers and restraints analyzed in the detailed report include:

- Emergence of Sovereign Cloud Initiatives Driving Local GPU Capacity

- Rising Demand for Energy-Efficient GPU Servers Amid ESG Regulations

- Supply Chain Dependence on Non-EU GPU Manufacturers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities are forecast to record a 12.78% CAGR through 2031, underpinned by automotive OEMs that install local GPU clusters to keep perception latency below 10 ms. BMW's Munich research hub used DGX Hopper nodes to achieve an 8-fold increase in synthetic-image generation, underscoring why private edge racks are proliferating.

Cloud data centers still accounted for 58.76% of revenue in 2025, but Frankfurt's grid caps and Baukostenzuschusse now slow further construction. SAP's sovereign AI Cloud straddles private and public models, letting manufacturers retain data locality while offloading operations.

Training GPUs accounted for 55.72% of 2025 spending, as hyperscalers snapped up H100 and H200 inventory for foundation-model runs. Intel's Gaudi 3, offered in IBM Cloud's Frankfurt region, claims 50% lower inference costs than the H100, promoting Ethernet fabrics over InfiniBand.

Inference demand is rising most sharply at the edge, where slot power and form-factor efficiency matter more than peak FLOPS. AMD's MI300 roadmap doubles HBM per GPU, appealing to memory-bound inference tasks in sovereign clouds.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Cerebras Systems Inc.

- Huawei Technologies Co. Ltd.

- Giga Computing Technology Co. Ltd.

- AsusTek Computer Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Lenovo Group Limited

- Deutsche Telekom AG

- T-Systems International GmbH

- Hetzner Online GmbH

- SAP SE

- Atos SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of AI Workloads in German Enterprises

- 4.2.2 Rising Demand for Energy-Efficient GPU Servers Amid ESG Regulations

- 4.2.3 Expansion of Hyperscaler Cloud Regions in Frankfurt and Berlin

- 4.2.4 Government Funding for HPC and Quantum Research Facilities

- 4.2.5 Increasing Edge Computing Needs for Autonomous Manufacturing

- 4.2.6 Emergence of Sovereign Cloud Initiatives Driving Local GPU Capacity

- 4.3 Market Restraints

- 4.3.1 High Electricity Costs and Grid Constraints in Major German Data Center Hubs

- 4.3.2 Supply Chain Dependence on Non-EU GPU Manufacturers

- 4.3.3 Stringent Data Protection and Residency Regulations Limiting Cross-Border Workloads

- 4.3.4 Skilled GPU Programming Talent Shortage

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Cerebras Systems Inc.

- 6.4.5 Huawei Technologies Co. Ltd.

- 6.4.6 Giga Computing Technology Co. Ltd.

- 6.4.7 AsusTek Computer Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Lenovo Group Limited

- 6.4.11 Deutsche Telekom AG

- 6.4.12 T-Systems International GmbH

- 6.4.13 Hetzner Online GmbH

- 6.4.14 SAP SE

- 6.4.15 Atos SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)