|

市場調查報告書

商品編碼

2065489

歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

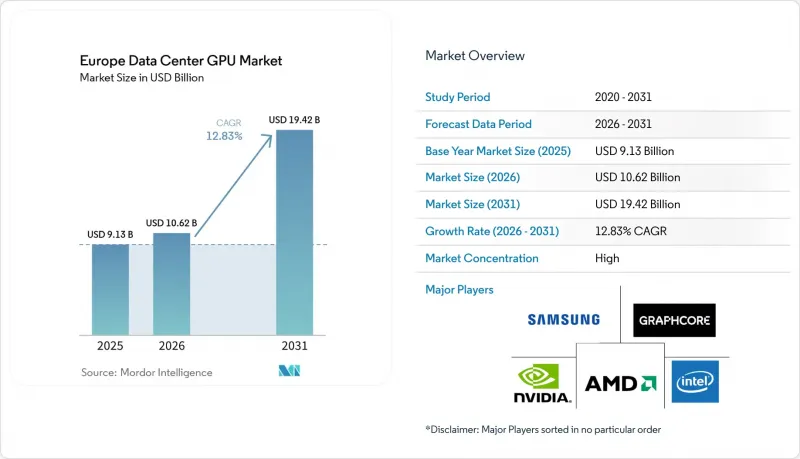

根據 Mordor Intelligence 預測,歐洲資料中心 GPU 市場規模將從 2026 年的 106.2 億美元成長到 2031 年的 194.2 億美元,2026 年至 2031 年的複合年成長率為 12.83%。

本報告按部署類型(例如,雲端資料中心)、GPU 類型(訓練 GPU 和推理 GPU)、互連方式(基於 PCIe 的 GPU 和高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算及其他)、最終用戶(超大規模資料中心業者/雲端服務供應商、企業及其他)以及國家/地區(德國、英國、法國及其他)進行分類。市場預測以美元計價。

歐洲資料中心GPU市場的趨勢與洞察

歐洲各大超大規模園區對人工智慧模型學習能力的需求正在加速成長。

超大規模營運商正在運作擁有超過 10,000 個加速器的 GPU 集群,以處理訓練基礎模型所需的高計算負載,並在慕尼黑、巴黎和北歐國家部署集群,從而推動區域百萬兆級水平的提升。靈活的電力合約和低碳電網正在吸引資本流入北歐國家,而德國和法國的主權雲端監管政策則確保了大部分運算能力仍由本國控制。高頻寬架構(例如 NVLink 6)對於這些叢集的規模至關重要,能夠降低全延遲並保持 GPU 利用率在 90% 以上。這些投資共同擴大了配套互連技術、冷卻系統和本地 AI 服務的目標市場,從而推動了歐洲資料中心 GPU 市場的發展。然而,這也增加了複雜封裝製程瓶頸帶來的風險,迫使營運商與多家供應商簽訂合約以規避供應風險。

GPU驅動的分析平台在金融服務和電信業的應用日益廣泛。

銀行和通訊業者正在將GPU整合到其詐欺偵測、風險建模和網路最佳化流程中,將推理時間從幾分鐘縮短到幾毫秒。德意志銀行、荷蘭國際集團、沃達豐和橘子在將其分析工作負載遷移到GPU叢集後,延遲均實現了兩位數的改善,這充分證明了加速器升級的投資回報。歐洲網路中交易和遙測資料的激增使得即時處理至關重要,但僅依賴CPU的平台無法經濟高效地實現這一點。因此,歐洲資料中心GPU市場正受益於定期的硬體更新周期、整合的軟體堆疊以及面向受監管行業的客製化管理服務。供應商對開放原始碼框架的支援進一步降低了採用門檻,使小規模的機構也能利用GPU加速,而無需受限於專有供應商。

台灣和韓國先進封裝供應鏈中存在集中風險

CoWoS 和 HBM3e 的產能限制導致旗艦級 GPU 的交付週期延長至 50 週以上,嚴重擾亂了歐洲雲和研究項目的部署計劃。三星和 SK 海力士優先履行北美的大型契約,迫使歐盟營運商考慮其他供應商或使用較舊的 GPU 型號。這種供不應求推高了現貨市場價格,擠壓了專案利潤率,並延遲了整個歐洲資料中心 GPU 市場的收入累計。雖然諸如雙源採購策略和庫存緩衝等緊急措施在一定程度上緩解了風險,但也增加了營運資金負擔。

細分市場分析

邊緣運算設施在2025年僅佔總收入的一小部分,但預計將以14.66%的複合年成長率成長,超過歐洲資料中心GPU市場的平均水準。這種快速普及主要得益於自動駕駛汽車遙測、工業IoT感測器融合以及擴增實境(AR)串流等應用,這些應用所需的往返延遲均低於10毫秒。雲園區在2025年將佔總營收的55.67%,主要體現在位於德國和法國的超大規模訓練叢集和多租戶推理集群。其餘部分則由企業雲端和私有雲端構成,這主要是由於合規性要求建議使用本地GPU來處理敏感的金融和醫療資料。

邊緣部署利用微模組化設計、無風扇液冷和即時編配協議棧,將推理能力更靠近用戶。通訊業者正在 5G 基地台中部署配備 GPU 的節點,以動態地頻寬;零售連鎖店則在試點店內電腦視覺系統,以增強消費者分析。雲端服務供應商也積極回應,提供分散式推理服務,建構跨越中心園區和區域聚合點的混合架構。這種分散式模式正在將歐洲資料中心 GPU 的潛在市場擴展到大都會圈區以外的地區,為專業整合商和營運商中立的交換中心創造了新的機會。

預計2025年,訓練GPU將佔總營收的59.87%。這主要得益於多機架叢集推動了基礎模型的發展,但隨著企業將預算轉向生產部署,推理加速器的複合年成長率預計將達到14.78%。 NVIDIA的L40S和L4系列產品正吸引邊緣運算和企業級市場的買家,他們需要高能源效率比來滿足聊天機器人和詐騙偵測的需求。 AMD的MI300X則為CoreWeave和Lambda Labs位於法蘭克福和巴黎的資料中心提供了更低成本的訓練和推理解決方案。

銀行目前正將大部分新增資本支出投入推理領域,配置高記憶體GPU,使其能夠每秒處理數百萬筆交易,而無需往返雲端網路流量。通訊業者則選擇整合網路功能的加速器,以優先考慮延遲和能源效率,並最大限度地減少PCIe開銷。雖然訓練對於超大規模資料中心業者和研究機構仍然至關重要,但隨著成熟模型進入以推理為中心的生命週期階段,其比例正在下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐洲各地超大規模園區對人工智慧模型學習能力的需求正在加速成長。

- GPU驅動的分析平台在金融服務和電信業的應用日益廣泛。

- 歐盟綠色交易的獎勵正在推動資料中心向節能型GPU升級。

- 擴大需要本地 GPU叢集的自主雲端概念的採用範圍。

- 水冷改造方案的出現,使得更高密度的GPU機架成為可能。

- 合成數據產生新創公司的激增正在推動對突髮型 GPU 租賃的需求。

- 市場限制因素

- 台灣和韓國先進包裝供應鏈中的風險集中

- 歐洲主要託管場所的電價飆升正在削弱總擁有成本 (TCO) 的經濟可行性。

- 歐盟正在製定的半導體主權法規使跨境共用GPU集群變得更加複雜。

- 加強乾旱地區液冷GPU群聚用水量的監測。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 透過連接方式

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

- 國家

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Samsung Electronics Co. Ltd.

- International Business Machines Corporation

- Atos SE

- Inspur Group Co. Ltd.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- Giga Computing Technology Co. Ltd.

- Graphcore Ltd.

- OVH Groupe SAS

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe data center GPU market is expected to grow from USD 10.62 billion in 2026 to USD 19.42 billion by 2031, at a 12.83% CAGR over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), End-User (Hyperscalers/CSPs, Enterprises, and More), and by Country (Germany, United Kingdom, France, Italy, and More). The Market Forecasts are Provided in Value (USD).

Europe Data Center GPU Market Trends and Insights

Accelerating Demand for AI Model Training Capacity Across European Hyperscale Campuses

Hyperscale operators are commissioning GPU clusters with more than 10,000 accelerators to meet the compute intensity of foundation-model training, with deployments in Munich, Paris, and the Nordic states pushing regional exascale thresholds. Flexible power contracts and low-carbon grids attract capital to Northern Europe, while sovereign-cloud rules in Germany and France ensure that a sizeable share of this capacity remains domestically controlled. The scale of these clusters necessitates high-bandwidth fabrics such as NVLink 6, which reduces all-reduce latency and keeps GPU utilization above 90%. Collectively, these investments expand the addressable market for complementary interconnects, cooling systems, and on-premises AI services, boosting the European data center GPU market. However, they also magnify exposure to advanced packaging bottlenecks, compelling operators to secure multi-vendor contracts to hedge supply risk.

Growing Adoption of GPU-Powered Analytics Platforms in Financial Services and Telecom Sectors

Banks and carriers are embedding GPUs into fraud-detection, risk-modeling, and network-optimization pipelines, trimming inference times from minutes to milliseconds. Deutsche Bank, ING, Vodafone, and Orange each reported double-digit latency improvements after migrating analytical workloads to GPU clusters, validating the return on investment for accelerator upgrades. The surge of transactional and telemetry data streaming through European networks necessitates real-time processing, which CPU-only platforms cannot sustain cost-effectively. As a result, the Europe data center GPU market benefits from recurring hardware refresh cycles, software stack integrations, and managed service offerings tailored to regulated industries. Vendor support for open-source frameworks further lowers adoption barriers, allowing smaller institutions to harness GPU acceleration without proprietary lock-in.

Supply Chain Concentration Risk Around Advanced Packaging in Taiwan and South Korea

CoWoS and HBM3e capacity constraints extend delivery lead times for flagship GPUs beyond 50 weeks, disrupting rollout schedules for European cloud and research projects. Samsung and SK hynix prioritize larger North American contracts, compelling EU operators to consider alternative vendors or older GPU SKUs. The shortage inflates spot-market pricing, narrowing project margins and delaying revenue recognition across the Europe data center GPU market. Contingency actions, such as dual-sourcing strategies and inventory buffers, partially mitigate risk but add working-capital burdens.

Other drivers and restraints analyzed in the detailed report include:

- EU Green Deal Incentives Pushing Energy-Efficient GPU Upgrades in Data Centers

- Rising Uptake of Sovereign Cloud Initiatives Requiring On-Prem GPU Clusters

- High Electricity Prices in Key European Colocation Hubs Denting TCO Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities contributed a modest slice of 2025 revenue, yet are projected to outpace the Europe data center GPU market average with a 14.66% CAGR. Rapid adoption stems from autonomous-vehicle telemetry, industrial IoT sensor fusion, and augmented-reality streaming, all of which require under 10 ms round-trip latency. Cloud campuses retained 55.67% of turnover in 2025, reflecting hyperscale training clusters and multi-tenant inference farms anchored in Germany and France. Enterprises and private clouds fill the remainder, driven by compliance mandates favoring on-prem GPUs for sensitive financial and healthcare data.

Edge deployments benefit from micro-modular designs, fanless liquid cooling, and real-time orchestration stacks that push inference closer to subscribers. Telcos deploy GPU-enabled nodes at 5G base stations to dynamically slice bandwidth, while retail chains pilot in-store computer vision systems to enhance shopper analytics. Cloud providers respond by offering distributed inference services, creating hybrid architectures that span central campuses and regional aggregation points. This decentralized pattern expands the addressable market for Europe data center GPU markets beyond metropolitan hubs, unlocking opportunities for specialized integrators and carrier-neutral exchanges.

Training GPUs accounted for 59.87% of 2025 sales because multi-rack clusters powered foundation-model development, but inference accelerators are forecast to post a 14.78% CAGR as enterprises shift budgets toward production deployment. NVIDIA's L40S and L4 attract edge and enterprise buyers seeking high performance per watt for chatbots and fraud detection. AMD's MI300X provides a lower-cost path for both training and inference at CoreWeave and Lambda Labs sites in Frankfurt and Paris.

Banks now channel most incremental capex toward inference, allocating memory-rich GPUs that handle millions of transactions per second without network round-trips to cloud campuses. Telecom operators prioritize latency and energy efficiency, selecting accelerators with on-package networking to minimize PCIe overhead. Training remains mission-critical for hyperscalers and research institutes, but its proportional share declines as mature models age into inference-heavy life-cycle phases.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Samsung Electronics Co. Ltd.

- International Business Machines Corporation

- Atos SE

- Inspur Group Co. Ltd.

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- Lenovo Group Limited

- Giga Computing Technology Co. Ltd.

- Graphcore Ltd.

- OVH Groupe SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating demand for AI model training capacity across European hyperscale campuses

- 4.2.2 Growing adoption of GPU-powered analytics platforms in financial services and telecom sectors

- 4.2.3 EU Green Deal incentives pushing energy-efficient GPU upgrades in data centers

- 4.2.4 Rising uptake of sovereign cloud initiatives requiring on-prem GPU clusters

- 4.2.5 Emergence of liquid-cooling retrofits enabling higher GPU rack densities

- 4.2.6 Proliferation of synthetic data generation startups driving burst GPU leasing

- 4.3 Market Restraints

- 4.3.1 Supply chain concentration risk around advanced packaging in Taiwan and South Korea

- 4.3.2 High electricity prices in key European colocation hubs denting TCO economics

- 4.3.3 Emerging EU chip-sovereignty rules complicating cross-border GPU fleet sharing

- 4.3.4 Growing scrutiny over water usage for liquid-cooled GPU farms in drought-prone regions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Samsung Electronics Co. Ltd.

- 6.4.5 International Business Machines Corporation

- 6.4.6 Atos SE

- 6.4.7 Inspur Group Co. Ltd.

- 6.4.8 Hewlett Packard Enterprise Company

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Giga Computing Technology Co. Ltd.

- 6.4.12 Graphcore Ltd.

- 6.4.13 OVH Groupe SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)