|

市場調查報告書

商品編碼

2065511

日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Japan Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

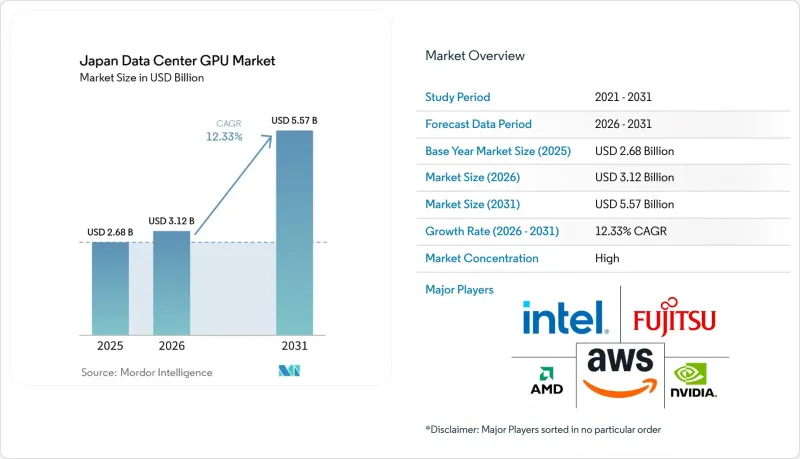

日本資料中心GPU市場預計將從2025年的26.8億美元成長到2026年的31.2億美元,到2031年達到55.7億美元,2026年至2031年的複合年成長率為12.33%。

本報告按部署類型(雲端資料中心、企業/私人資料中心、邊緣資料中心)、GPU 類型(訓練 GPU、推理 GPU)、互連方式(基於 PCIe 的 GPU、高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算等)以及最終用戶(超大規模資料中心業者伺服器/雲端服務供應商、企業、政府機構和研究機構)進行細分。市場預測以美元 (USD) 為單位。

日本資料中心GPU市場趨勢及洞察。

加速日本企業採用人工智慧和機器學習技術

日本的銀行、製造商和專業服務公司正在將生成式人工智慧融入日常運營,這顯著提升了對本地部署和混合GPU叢集的需求。櫻花網際網路(Sakura Internet)利用日本經濟產業省(METI)提供的501億日元(約合3.34億美元)補貼,將其NVIDIA HGX B200加速器集群擴展至10,800台,以滿足那些不願在多租戶雲環境中部署自有模型的企業的需求集群。微軟投資29億美元培訓100萬名人工智慧技能人才,凸顯了日本企業在營運新工作負載時必須彌補的人才缺口。 GMO Internet於2025年8月部署了200台NVIDIA B300 GPU,透過多實例分區技術,實現了每次查詢推理成本降低40%,從而加速了生產部署。隨著概念驗證(PoC)試點計畫逐步轉化為獲利服務,日本資料中心GPU市場正受惠於企業主導的持續更新周期。金融機構目前正在使用搜尋增強生成模型來實現合規自動化,而汽車零件供應商正在採用視覺變壓器以亞毫秒級的延遲來檢測缺陷。

政府的「社會5.0」舉措正在推動高效能運算基礎設施的發展。

公共部門的投資正在鞏固長期需求前景。理研的「富嶽NEXT」藍圖將把2140塊NVIDIA Blackwell GPU整合到百萬兆級計劃於2026年春季運作的百億億次級系統中,以推動國家級氣候變遷和藥物研發研究。產業技術綜合研究所(AIST)的「ABCI 3.0」自2025年1月起運作,配備了NVIDIA H200 GPU和Quantum-2 InfiniBand,透過提供比商業雲端服務低70%的補貼運算資源,使新創公司和大學能夠更便捷地獲取運算資源。這些旗艦專案透過在大規模環境中展示持續性能並培養國內人才儲備,降低了GPU部署的風險。 2024年11月,NEC簽署了一份契約,將交付一台40.4 petaflops的超級電腦結合了Intel Xeon 6900P CPU和AMD Instinct MI300A GPU,這標誌著日本科研基礎設施的多廠商異構性。因此,「社會 5.0」概念正在刺激公共和私營部門的支出,並增強人們對日本資料中心 GPU 市場的長期信心。

高額資本投入和較長的投資報酬週期

由於日本的抗震設計標準,新建設的Tier IV級設施成本飆升至每瓦IT負載8-12美元,一個100兆瓦的園區總成本高達8億至12億美元,比全球標準高出30%-40%。平均電價為每千瓦時0.09-0.13美元,進一步擠壓了利潤空間,導致一個100兆瓦設施的年電力成本約為4470萬美元。雲端GPU每小時價格為1.50-2.50美元,比本地叢集更具競爭力,後者以每小時1.70美元的成本分攤三年,投資回收期可延長至四年。對現有設施進行改造,例如KDDI的棕地堺項目,可以節省100億美元(6700萬美元),並將部署時間縮短至不到一年,但合適的土地仍然稀缺。在東京,併網等待時間可能長達 10 年,進一步增加了投資報酬率的不確定性。

細分市場分析

預計到2025年,日本資料中心GPU市場中,雲端資料中心將佔56.13%的營收佔有率。這反映了超大規模資料中心超大規模資料中心業者能夠將價值數十億美元的園區分散並攤銷給數千家租戶,同時提供按需H100實例,從而避免長達18個月的採購週期。儘管企業正在採用雲端進行突發訓練,但邊緣資料中心才是成長最快的細分市場,因為製造商對機器視覺任務的延遲要求極高,需要達到亞毫秒。 Ubitus斥資1.13億美元部署的GPU節點位於距離生產線10-20公里的範圍內,消除了廣域往返延遲,並將品質偵測吞吐量提高了25%。

邊緣運算領域的快速成長得益於區域城市較低的電價、充足的土地資源以及相對較低的電網擁塞狀況。 HiRezo位於香川縣的資料中心利用地方政府的激勵措施,將能源成本降低了約20%;而NEC的ExpEther基礎設施實現了GPU的解耦,與固定叢集相比,資本密集度降低了30%。 KDDI大阪堺園區等現有設施棕地項目,凸顯了向適應性再利用的策略轉變,加快了產品上市速度,並將日本資料中心GPU市場的版圖擴展到東京-大阪軸線以外的地區。

在2025年的支出中,訓練GPU佔54.68%,這主要得益於國家超級運算採購,例如理研(RIKEN)用於百萬兆級模擬的2140台Blackwell超級電腦。然而,隨著企業向全面部署LLM(邏輯層級模型)邁進,推理加速器的規模正在迅速擴張。 GMO Internet透過將每塊NVIDIA B300顯示卡分割為七個推理切片,降低了40%的查詢成本,並提高了設備運轉率。

隨著許多公司採用微調取代預訓練,日本資料中心推理GPU市場正經歷更快速的成長。 NVIDIA的H200將FP8吞吐量提升了三倍,而Intel Gaudi 3在某些任務上的推理速度比H100提升了50%,吸引了注重成本的買家。這種每瓦性能的提升進一步加速了向多實例、低延遲服務的轉變。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速日本企業採用人工智慧和機器學習技術

- 政府的「社會5.0」計畫旨在促進高效能運算基礎設施的發展。

- 日本擴大超大規模雲端容量

- 對雲端遊戲和串流媒體服務的需求不斷成長

- 企業脫碳目標正在推動節能型GPU的普及。

- 製造群附近區域邊緣資料中心的興起

- 市場限制因素

- 大筆資本投入和較長的投資回收期

- 先進節點半導體供應受限

- 缺乏GPU叢集管理技能

- 更嚴格的抗震標準推高了建築成本。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 透過連接方式

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Arm Holdings plc

- Amazon Web Services Inc.

- Google LLC

- Microsoft Corporation

- Alibaba Cloud(Alibaba Group Holding Limited)

- Oracle Corporation

- IBM Corporation

- Tencent Cloud(Tencent Holdings Limited)

- Giga Computing Technology Co. Ltd.

- Graphcore Limited

- SambaNova Systems Inc.

- Huawei Technologies Co. Ltd.

- Lenovo Group Limited

- Dell Technologies Inc.

- Super Micro Computer Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan data center GPU market size is expected to increase from USD 2.68 billion in 2025 to USD 3.12 billion in 2026 and reach USD 5.57 billion by 2031, growing at a CAGR of 12.33% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, Edge Data Centers), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

Japan Data Center GPU Market Trends and Insights

Accelerating AI and ML Adoption Across Japanese Enterprises

Japanese banks, manufacturers, and professional-services firms are embedding generative AI into daily operations, fueling outsized demand for on-premises and hybrid GPU clusters. Sakura Internet expanded its inventory to 10,800 NVIDIA HGX B200 accelerators, supported by a JPY 50.1 billion (USD 334 million) METI subsidy, to satisfy enterprises unwilling to deploy proprietary models in multi-tenant clouds. Microsoft's USD 2.9 billion commitment to train 1 million workers in AI skills underscores the talent gap that Japanese companies must bridge to operationalize new workloads.GMO Internet's August 2025 rollout of 200 NVIDIA B300 GPUs demonstrated that multi-instance partitioning can cut per-query inference costs by 40%, accelerating production deployments. As proof-of-concept pilots morph into revenue-bearing services, the Japan data center GPU market benefits from sustained enterprise-led refresh cycles. Financial institutions now run retrieval-augmented generation models for compliance automation, while automotive suppliers apply vision transformers for defect detection with sub-millisecond latency.

Government's Society 5.0 Initiatives Driving HPC Infrastructure

Public-sector investment anchors long-term demand visibility. RIKEN's FugakuNEXT roadmap integrates 2,140 NVIDIA Blackwell GPUs into exascale systems scheduled for spring 2026, advancing national climate and drug-discovery research. AIST's ABCI 3.0, live since January 2025 with NVIDIA H200 GPUs and Quantum-2 InfiniBand, offers subsidized compute at up to 70% below commercial cloud rates, democratizing access for startups and universities. These flagship programs de-risk GPU adoption by demonstrating sustained performance at scale and building a domestic talent pipeline. NEC's November 2024 contract to deliver a 40.4 petaflops supercomputer combining Intel Xeon 6900P CPUs with AMD Instinct MI300A GPUs showcases multi-vendor heterogeneity in national research infrastructure. The Society 5.0 agenda, therefore, stimulates both public and private spending and reinforces long-term confidence in the Japanese data center GPU market.

High Capital Expenditure and Long ROI Cycles

Japan's seismic engineering codes lift greenfield Tier IV cost to USD 8-12 per watt of IT load, equal to USD 800 million-1.2 billion for a 100 MW campus, 30-40% above global norms. Electricity averaging USD 0.09-0.13 per kWh further erodes margins, with a 100 MW facility incurring roughly USD 44.7 million in annual power expense. Cloud GPUs, available at USD 1.50-2.50 per hour, outcompete on-premises clusters that amortize at USD 1.70 per hour over three years, extending payback to as long as four years. Brownfield conversions like KDDI's Osaka Sakai project save JPY 10 billion (USD 67 million) and compress timelines to under one year, yet suitable sites remain scarce. Grid connection queues of up to ten years in Tokyo magnify ROI uncertainty.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Hyperscale Cloud Capacity in Japan

- Emergence of Regional Edge Data Centers Near Manufacturing Clusters

- Semiconductor Supply Constraints for Advanced Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers generated 56.13% of 2025 revenue in the Japan data center GPU market, reflecting hyperscalers' ability to amortize billion-dollar campuses across thousands of tenants while offering on-demand H100 instances that bypass 18-month procurement cycles. Enterprises embrace cloud for burst training, yet edge data centers are the fastest-growing slice as manufacturers demand sub-5 millisecond latency on machine-vision tasks. Ubitus's USD 113 million rollout places GPU nodes within 10-20 kilometers of production lines, eliminating wide-area round-trip delay and boosting quality-inspection throughput by up to 25%.

The edge surge is underpinned by lower power tariffs in secondary cities, available land, and looser grid queues. HiRezo's Kagawa facility leverages provincial incentives to reduce energy costs by roughly 20%, while NEC's ExpEther infrastructures enable GPU disaggregation, trimming capital intensity by 30% versus fixed clusters. Brownfield conversions such as KDDI's Osaka Sakai site underscore a strategic pivot toward adaptive reuse that shortens time-to-market and spreads the Japan data center GPU market footprint beyond the Tokyo-Osaka axis.

Training GPUs held 54.68% of 2025 spending, anchored by national supercomputing procurements like RIKEN's 2,140 Blackwell units for exascale simulations. Nevertheless, inference accelerators are scaling faster as enterprises shift to production LLM deployment; GMO Internet partitions each NVIDIA B300 into seven inference slices, trimming query costs by 40% and elevating device utilization.

With fine-tuning replacing pre-training for most companies, the Japan data center GPU market size for inference is on a steeper trajectory. NVIDIA's H200 boosts FP8 throughput threefold, while Intel Gaudi 3 claims 50% higher inference/sec versus H100 on select tasks, tempting cost-sensitive buyers. The performance-per-watt gains reinforce a pivot toward multi-instance, low-latency serving.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Arm Holdings plc

- Amazon Web Services Inc.

- Google LLC

- Microsoft Corporation

- Alibaba Cloud (Alibaba Group Holding Limited)

- Oracle Corporation

- IBM Corporation

- Tencent Cloud (Tencent Holdings Limited)

- Giga Computing Technology Co. Ltd.

- Graphcore Limited

- SambaNova Systems Inc.

- Huawei Technologies Co. Ltd.

- Lenovo Group Limited

- Dell Technologies Inc.

- Super Micro Computer Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating AI and ML Adoption Across Japanese Enterprises

- 4.2.2 Government's Society 5.0 Initiatives Driving HPC Infrastructure

- 4.2.3 Expansion of Hyperscale Cloud Capacity in Japan

- 4.2.4 Growing Demand for Cloud Gaming and Streaming Services

- 4.2.5 Corporate Decarbonization Targets Catalyzing Energy-Efficient GPUs

- 4.2.6 Emergence of Regional Edge Data Centers Near Manufacturing Clusters

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure and Long ROI Cycles

- 4.3.2 Semiconductor Supply Constraints for Advanced Nodes

- 4.3.3 Skills Shortage in GPU Cluster Management

- 4.3.4 Stricter Earthquake-Resilience Standards Inflating Build Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) & Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics & Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government & Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Fujitsu Limited

- 6.4.5 NEC Corporation

- 6.4.6 Arm Holdings plc

- 6.4.7 Amazon Web Services Inc.

- 6.4.8 Google LLC

- 6.4.9 Microsoft Corporation

- 6.4.10 Alibaba Cloud (Alibaba Group Holding Limited)

- 6.4.11 Oracle Corporation

- 6.4.12 IBM Corporation

- 6.4.13 Tencent Cloud (Tencent Holdings Limited)

- 6.4.14 Giga Computing Technology Co. Ltd.

- 6.4.15 Graphcore Limited

- 6.4.16 SambaNova Systems Inc.

- 6.4.17 Huawei Technologies Co. Ltd.

- 6.4.18 Lenovo Group Limited

- 6.4.19 Dell Technologies Inc.

- 6.4.20 Super Micro Computer Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)