|

市場調查報告書

商品編碼

2072688

法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)France Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

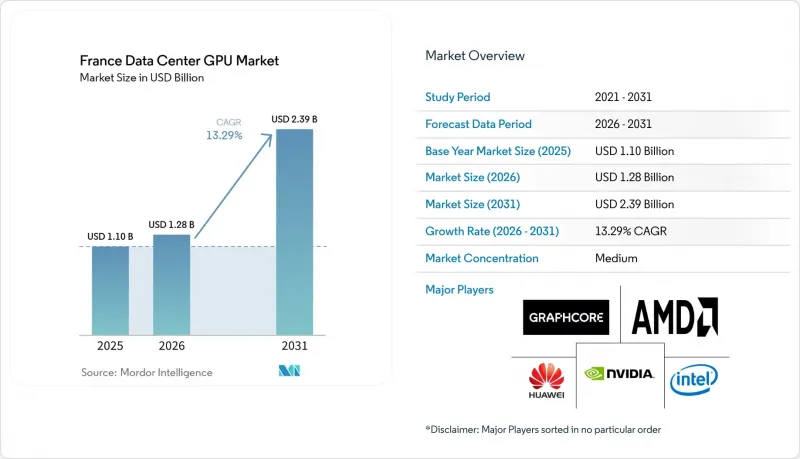

據 Mordor Intelligence 稱,法國資料中心 GPU 市場預計將從 2025 年的 11 億美元成長到 2026 年的 12.8 億美元,到 2031 年達到 23.9 億美元,預計 2026 年至 2031 年的複合年成長率為 13.29%。

本報告按部署類型(雲端資料中心、企業/私人資料中心等)、GPU 類型(訓練 GPU、推理 GPU)、互連方式(基於 PCIe 的 GPU、高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算等)以及最終用戶(超大規模資料中心業者伺服器/雲端服務供應商、企業、政府機構、研究機構)進行細分。市場預測以美元計價。

法國資料中心GPU市場的趨勢與洞察

生成式人工智慧工作負載的採用率正在激增。

生成式人工智慧的興起正推動法國的GPU採購從先導計畫計畫轉向永續的基礎設施規劃。這是因為企業和研究機構需要高密度運算能力來進行模型開發和生產服務交付。最強勁的需求來自銀行、保險、醫療保健、國防和電信等受監管的應用場景,在這些場景中,數據局部和可審計的處理與原始基準速度同等重要。這正推動法國資料中心GPU市場向「高階主權層級」發展,營運商可以透過提供本地控制、精細化服務和清晰的合規支援來設定更高的價格。隨著許多組織在生產環境中部署更多小型模型,而不是僅僅依賴少數大規模訓練運行,需求也不斷擴大。 SITEC位於科西嘉島的AI託管平台展示瞭如何在公共數位創新計劃下定位本地基礎設施,以實現區域實驗、靈活的GPU性能分析和直接的技術支援。隨著這些工作負載越來越靠近營運團隊和業務部門,法國資料中心GPU市場正受益於更穩定的正常運轉率、更高的重複購買率以及對區域推理能力日益成長的興趣。

法國超大規模設施快速擴張

大型資料中心園區的建設正在擴展法國資料中心GPU市場未來十年成長所需的實體基礎設施。 Data4已將其位於Nouzet的PAR03園區的投資計畫從10億歐元(22.6億美元)增加到20億歐元(22.6億美元),並將該園區的電力容量提升至250兆瓦,設計容量約為20萬個GPU。這顯示法國規劃的叢集規模正在不斷擴大。該公司還計劃透過將PAR03園區與其現有的Marcousis園區互聯,打造大規模的數位走廊,從而鞏固巴黎-薩克雷地區作為人工智慧能力中心的地位。在大巴黎地區以外,Iliad和OpCore與法國電力公司(EDF)合作,決定在蒙特羅投資25億歐元(28.3億美元)建造700兆瓦的資料中心。同時,其他業者也在波爾多和其他地區城市規劃大規模計畫。如此大規模的產能擴張將最佳化設備配置,縮短大型客戶的等待時間,並使法國資料中心GPU市場能夠同時支援政府主導的人工智慧專案和商業雲端需求。此外,在核心電力和網路基礎設施得到保障後,營運商不僅可以在站點接入方面,還可以在散熱設計、認證和託管人工智慧工具等領域實現差異化競爭,從而提供更多專業化服務。

法國電價高企

電力仍是法國資料中心GPU市場的主要限制因素,因為GPU叢集的高運轉率直接轉化為高昂的經常性電力成本。法國國家電力監管局(ARENH)的監管准入機制將於2025年終止,這將降低沒有長期合約或議價能力的營運商的價格確定性,使新計畫的財務規劃變得困難。對於無法在大規模設施中分散風險的獨立託管服務供應商、私人企業資料中心和區域性設施而言,這種壓力尤其顯著。隨著營運商向最新一代加速器過渡,機架密度的增加進一步加劇了這個問題,因為冷卻需求的增加導致電力成本上升。大規模園區和政府主導的計畫擁有足夠的資源來協商有利的條款並承受暫時的價格波動,這造成了法國資料中心GPU市場中大型買家和小規模參與者之間的差距。如果電價持續波動,儘管仍會建立一些容量,但更多買家可能會傾向於混合利用模式和分階段部署,而不是大規模的即時部署。

細分市場分析

預計到2025年,雲端資料中心將佔部署類型總收入的53.47%,並將繼續作為法國資料中心GPU市場的主要商業基礎,因為多租戶模式能夠提高硬體吸收率、增強定價柔軟性並縮短更新周期。同時,邊緣資料中心預計到2031年將以14.90%的複合年成長率成長。雖然大型園區可以整合高密度電源、液冷和託管軟體層,但在企業級場以類似速度複製這些配置通常很困難。 Data4的PAR03專案清楚展現了這種規模優勢,該公司將其投資計畫加倍,達到20億歐元(22.6億美元),並將Nozay園區設計為可容納250兆瓦電力容量和約20萬個GPU。 Scaleway 的託管式 H100 服務和 OVHcloud 不斷擴展的 L4、L40S 和 H100 實例產品組合,充分展現了雲端服務供應商為何能夠滿足從新創公司到受監管企業等各類客戶不斷變化的需求。這種模式確保了即使工作負載日益多樣化,法國資料中心 GPU 市場仍將繼續以大規模共用設施為基礎。

預計到2031年,邊緣資料中心將實現最快成長。這是因為推理、工業分析和圖形密集型應用場景需要接近性,而集中式資料中心無法始終提供可接受的延遲。 UltraEdge的「數據極」(Datapoles)計畫正在投資4億歐元(約4.52億美元),在包括波爾多、里昂、斯特拉斯堡、裡爾和南特在內的九個區域地點建設51兆瓦的資料中心,旨在支持汽車、工業IoT和即時影片工作負載的10毫秒以下處理速度。標準化的模組化建設將縮短交付週期,並使區域供應更快地回應實際需求。對於那些不希望直接控制、追求穩定正常運轉率或承擔雲端服務成本的用戶而言,企業級和私有資料中心仍然至關重要。因此,戴爾和聯想等伺服器供應商現在同時支援自有和計量收費的GPU環境。因此,法國資料中心 GPU 產業正從單一部署模式轉向分層結構,其中雲端規模、邊緣應變能力和私有環境主權分別應對不同的營運挑戰。

在2025年法國資料中心GPU市場中,訓練GPU佔了57.83%的佔有率。這是因為大規模模型和科學模擬的開發仍然需要部署在高密度叢集中的、具有大記憶體容量的昂貴加速器。同時,推理GPU預計將維持最高的成長率,到2031年複合年成長率將達到14.04%。自主人工智慧的雄心壯志進一步加劇了這種支出模式,因為希望在國內管理模型訓練的機構必須前期投資高性能硬體及其配套基礎設施。訓練叢集在網路和冷卻方面的支出也往往更高,因此與小規模的推理環境相比,其收入佔比更高。另一方面,隨著雲端服務供應商現在為生產環境提供各種低功耗加速器,市場需求也不斷成長。 Scaleway 針對 H100、L40S 和 L4 實例的定價,以及 OVHcloud 的按月 GPU 選項組合,表明買家現在可以更精確地客製化其加速器選擇,以服務、微調和混合企業工作負載。

隨著企業在客戶服務、詐欺偵測、建議和文件自動化等領域從孤立的實驗階段過渡到生產環境,預計到2031年,推理GPU將經歷最快的成長。法國資料中心GPU市場的這一細分領域受益於更高的能源效率、更低的每小時成本,以及許多生產模型不需要最昂貴的訓練晶片。 AMD於2025年6月發布的「Instinct MI350系列」強調了更高的成本績效(每美元的代幣數量),這將進一步加劇推理GPU的價格競爭,並擴大供應商範圍。訓練GPU對於國家級運算能力仍然至關重要,正如「Alice Recoque」和「Jean Zay」的升級所證明的那樣,它們支援主權站點的尖端研究和高階AI工作負載。因此,法國資料中心GPU產業正進入一個新階段,推理GPU將提供更廣泛、更穩定的應用曲線,而訓練GPU則維持其技術優勢和高交易量。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 生成式人工智慧工作負載的採用率正在激增。

- 法國超大規模設施的快速擴張

- 政府對綠色資料中心的稅收優惠

- 降低GPU加速伺服器的總擁有成本(TCO)

- 擴大主權雲的合規性要求

- 小規模模組化邊緣資料中心的興起

- 市場限制因素

- 法國電價高企

- 國內先進包裝供應鏈短缺

- 資料本地化法規正在減緩跨境雲端服務的成長。

- 功耗超過 700W 的 GPU 的散熱基礎設施面臨瓶頸

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 依類型互連

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nvidia Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Atos SE

- Eviden

- OVH Groupe SA

- Scaleway

- Orange Business Services

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- IBM Corporation

- Graphcore Limited

- Huawei Technologies Co., Ltd.

- Cerebras Systems Inc.

- SambaNova Systems Inc.

- Tenstorrent Inc.

- Giga Computing Technology Co., Ltd.

- Lenovo Group Limited

- Fujitsu Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the france data center GPU market size is expected to increase from USD 1.10 billion in 2025 to USD 1.28 billion in 2026 and reach USD 2.39 billion by 2031, growing at a CAGR of 13.29% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and More), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government, and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

France Data Center GPU Market Trends and Insights

Surging Adoption of Generative AI Workloads

Generative AI is moving GPU procurement in France from pilot projects into sustained infrastructure planning, because enterprises and research organizations now need dense compute for both model development and production serving. The strongest demand comes from regulated use cases in banking, insurance, healthcare, defense, and telecommunications, where data locality and auditable processing matter as much as raw benchmark speed. This is pushing the France Data Center GPU Market toward a premium sovereign tier in which operators can charge more for local control, tighter service, and clearer compliance support. The demand profile is also widening because many organizations now deploy a larger number of smaller models in production instead of relying only on a few large training runs. SITEC's AI hosting platform in Corsica shows how local infrastructure is being positioned for regional experimentation, flexible GPU profiles, and direct technical support under public digital-innovation programs. As these workloads move closer to operations teams and business units, the France Data Center GPU Market benefits from steadier utilization, more repeat buying, and stronger interest in regional inference capacity.

Rapid Expansion of France-Based Hyperscale Facilities

The build-out of large campuses is increasing the physical base on which the France Data Center GPU Market can grow over the rest of the decade. Data4 raised planned investment in its PAR03 campus in Nozay from EUR 1 billion (USD 2.26 billion) to EUR 2 billion (USD 2.26 billion), lifted the site to 250 MW, and designed it to host around 200,000 GPUs, which signals how large planned clusters are becoming in France. The company also plans to interconnect PAR03 with its existing Marcoussis campus, creating a larger digital corridor that strengthens the Paris-Saclay area as a gravity center for AI capacity. Outside the capital region, Iliad and OpCore committed EUR 2.5 billion (USD 2.83 billion) to a 700 MW site in Montereau with EDF, while other operators are planning large projects in Bordeaux and other secondary locations. More capacity at this scale improves equipment allocation, shortens wait times for large customers, and helps the France Data Center GPU Market support both sovereign AI projects and commercial cloud demand at the same time. It also creates room for more specialized services, because once core power and networking are available, operators can differentiate on cooling design, certification, and managed AI tooling rather than on land access alone.

Persistently High Electricity Prices in France

Electricity remains a real constraint for the France Data Center GPU Market because GPU clusters convert high utilization directly into large recurring energy bills. The end of the ARENH regulated-access mechanism in 2025 reduced price certainty for operators that do not have long-term contracts or strong negotiating leverage, which makes financial planning harder for new projects. This pressure is strongest for independent colocation providers, private enterprise sites, and regional facilities that cannot spread risk across very large estates. Higher rack densities also compound the issue, because power costs rise together with cooling requirements once operators move into the newest accelerator generations. Large campuses and sovereign projects are better placed to negotiate favorable terms or absorb temporary volatility, which creates a gap between very large buyers and smaller participants in the France Data Center GPU Market. If power pricing remains unstable, some capacity will still be built, but more buyers will favor hybrid use models and staged deployments rather than large immediate rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Government Tax Incentives for Green Data Centers

- Falling Total Cost of Ownership of GPU-Accelerated Servers

- Limited Domestic Supply Chain for Advanced Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers commanded 53.47% of deployment-type revenue in 2025, and they remain the main commercial base of the France Data Center GPU Market because multi-tenant utilization supports better hardware absorption, stronger pricing flexibility, and faster refresh cycles, while edge data centers are projected to expand at 14.90% CAGR through 2031. Large campuses can combine dense power, liquid cooling, and managed software layers in ways that enterprise sites often struggle to replicate at the same speed. Data4's PAR03 project shows the scale advantage clearly, because the company designed the Nozay campus for 250 MW and around 200,000 GPUs after doubling its investment plan to EUR 2 billion (USD 2.26 billion). Scaleway's managed H100 offering and OVHcloud's widening portfolio of L4, L40S, and H100 instances also show why cloud operators can serve a broad buyer base that ranges from startups to regulated enterprises with variable demand. This model keeps the France Data Center GPU Market anchored in large shared facilities even as workload diversity increases.

Edge data centers are projected to grow fastest through 2031 because inference, industrial analytics, and graphics-heavy use cases often need proximity that centralized campuses cannot always deliver at acceptable latency. UltraEdge's Datapoles program committed EUR 400 million (USD 452 million) and 51 MW across 9 regional sites, including Bordeaux, Lyon, Strasbourg, Lille, and Nantes, to support sub-10-millisecond processing for automotive, industrial IoT, and real-time video workloads. Standardized modular builds also shorten delivery times, which makes regional supply more responsive to actual demand. Enterprise and private data centers still matter where users want direct control, stable utilization, and no cloud egress costs, and server vendors such as Dell and Lenovo now support both owned and consumption-based GPU estates for that reason. The result is a France data center GPU industry that is not moving toward a single deployment model, but toward a layered structure in which cloud scale, edge responsiveness, and private sovereignty each solve a different operating problem.

Training GPUs accounted for 57.83% share of the France Data Center GPU Market size in 2025 because large model development and scientific simulation still require expensive, high-memory accelerators deployed in dense clusters, while inference GPUs are expected to record the strongest growth at 14.04% CAGR through 2031. That spending pattern is reinforced by sovereign AI ambitions, because organizations that want domestic control over model training must commit upfront capital to powerful hardware and supporting infrastructure. Training clusters also tend to pull in higher networking and cooling spend, which raises their revenue weight relative to smaller inference deployments. At the same time, the demand profile is widening because cloud providers now offer a broader set of lower-power accelerators for production use. Scaleway's pricing for H100, L40S, and L4 instances, along with OVHcloud's portfolio of monthly GPU options, shows how buyers can now match accelerator choice more closely to serving, fine-tuning, and mixed enterprise workloads.

Inference GPUs are projected to grow fastest through 2031 because enterprises are shifting from isolated experimentation toward live deployment across customer service, fraud detection, recommendation, and document automation. This part of the France Data Center GPU Market benefits from better power efficiency, lower hourly pricing, and the fact that many production models do not need the most expensive training silicon. AMD's June 2025 positioning of the Instinct MI350 Series around stronger tokens-per-dollar economics adds more pressure to inference pricing and widens the available supplier set. Training GPUs still remain essential for national compute capability, as shown by Alice Recoque and the Jean Zay upgrade, which both support advanced research and high-end AI workloads at sovereign sites. The France data center GPU industry is therefore entering a phase in which training keeps technical prestige and high ticket sizes, while inference delivers the broader and steadier deployment curve.

Complete Report Scope:

- By Deployment Type

- Cloud Data Centers

- Enterprise / Private Data Centers

- Edge Data Centers

- By GPU Type

- Training GPUs

- Inference GPUs

- By Interconnect

- PCIe-Based GPUs

- High-Bandwidth Interconnect GPUs

- By Workload Type

- Artificial Intelligence (AI) and Machine Learning (ML)

- High-Performance Computing (HPC) (non-AI scientific computing)

- Data Analytics (database acceleration, query processing)

- Graphics and Visualization (VDI, rendering, digital twins)

- By End-User

- Hyperscalers / Cloud Service Providers

- Enterprises

- Government and Research Institutions

List of Companies Covered in this Report:

- Nvidia Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Atos SE

- Eviden

- OVH Groupe SA

- Scaleway

- Orange Business Services

- Hewlett Packard Enterprise Company

- Dell Technologies Inc.

- IBM Corporation

- Graphcore Limited

- Huawei Technologies Co., Ltd.

- Cerebras Systems Inc.

- SambaNova Systems Inc.

- Tenstorrent Inc.

- Giga Computing Technology Co., Ltd.

- Lenovo Group Limited

- Fujitsu Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Generative AI Workloads

- 4.2.2 Rapid Expansion of France-Based Hyperscale Facilities

- 4.2.3 Government Tax Incentives for Green Data Centers

- 4.2.4 Falling Total Cost of Ownership of GPU-Accelerated Servers

- 4.2.5 Growth of Sovereign-Cloud Compliance Mandates

- 4.2.6 Emergence of Small-Scale Modular Edge Data Centers

- 4.3 Market Restraints

- 4.3.1 Persistently High Electricity Prices in France

- 4.3.2 Limited Domestic Supply Chain for Advanced Packaging

- 4.3.3 Data-Localization Rules Slowing Cross-Border Cloud Growth

- 4.3.4 Cooling Infrastructure Bottlenecks for >700 W GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products or Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nvidia Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Atos SE

- 6.4.5 Eviden

- 6.4.6 OVH Groupe SA

- 6.4.7 Scaleway

- 6.4.8 Orange Business Services

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Dell Technologies Inc.

- 6.4.11 IBM Corporation

- 6.4.12 Graphcore Limited

- 6.4.13 Huawei Technologies Co., Ltd.

- 6.4.14 Cerebras Systems Inc.

- 6.4.15 SambaNova Systems Inc.

- 6.4.16 Tenstorrent Inc.

- 6.4.17 Giga Computing Technology Co., Ltd.

- 6.4.18 Lenovo Group Limited

- 6.4.19 Fujitsu Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)