|

市場調查報告書

商品編碼

2065484

北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

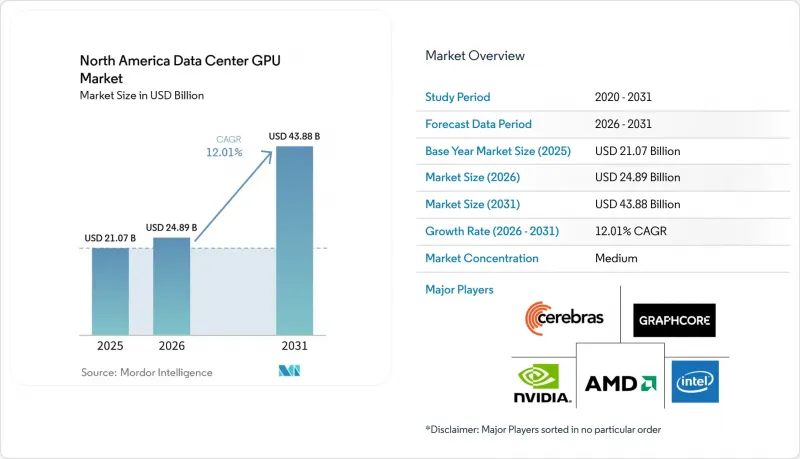

據 Mordor Intelligence 稱,北美資料中心 GPU 市場預計將從 2026 年的 248.9 億美元成長到 2031 年的 438.8 億美元,2026 年至 2031 年的複合年成長率為 12.01%。

本報告按部署類型(例如,雲端資料中心)、GPU 類型(訓練 GPU 和推理 GPU)、互連方式(基於 PCIe 的 GPU 和高頻寬互連 GPU)、工作負載類型(例如,人工智慧和機器學習、高效能運算)、最終用戶(例如,超大規模資料中心業者/雲端服務供應商、企業)以及國家/地區(例如,美國、加拿大)進行細分。市場預測以美元 (USD) 為單位。

北美資料中心GPU市場趨勢及洞察。

超大規模資料中心人工智慧與機器學習訓練工作負載激增

超大規模資料中心業者目前正利用超過 10 萬個 GPU 組成的叢集,訓練參數超過一兆的尖端模型。這種規模得益於 NVLink 架構,它將所有歸約延遲從幾分鐘縮短到幾秒鐘。主要 GPU 供應商在 2025 年的銷售數據顯示,模型預算將超過每次運行 1 億美元,從而推動了需求週期。 Solstice 和 Equinox 等公共部門專案正在使用超過 1 萬個 GPU 的叢集來運行氣候模型,這進一步增強了供應商的長期前景。營運商擴大將測試時運算資源納入容量規劃,隨著推理預算成長到與訓練預算相當的水平,GPU 的生命週期需求實際上加倍。由此產生的拉動效應使得先進節點晶圓廠運作運轉,加劇了對 HBM供給能力的競爭。

財富 500 強企業擴大採用混合雲端策略

企業正將人工智慧工作負載遷移回本地GPU集群,以便管理自身資料並避免可能超過總支出30%的雲端資料傳輸成本。配備4至64個GPU和類似SaaS管理功能的承包私有雲端人工智慧設備,正幫助製藥、汽車和媒體產業的企業在其防火牆內微調其生命週期管理(LLM)。這種混合模式得益於成熟的虛擬化技術,vGPU 19.0支援每個Blackwell GPU運行48個虛擬機,從而允許加速器進行分區並在多個業務部門之間使用。在季節性高峰期,無法處理的作業可以突發到雲端服務供應商(CSP)的容量上,在保持敏捷性的同時,避免長期鎖定公共雲端。這種工作負載的靈活性正在擴大中型資料中心的潛在市場,並增加對GPU租賃的需求。

先進節點半導體供應鏈持續面臨限制因素

由於先進封裝技術的持續供應限制,Blackwell 和 Rubin GPU 的前置作業時間現已超過 50 週。 CoWoS 的產能無法滿足需求,而 HBM3E 的供應預計要到 2026 年才能滿足訂單。供應商正透過擴建其在美國的晶圓廠來應對這項挑戰,但產能擴張計畫只能在短期內緩解供應緊張的局面,迫使超大規模超大規模資料中心業者簽訂數十億美元的預購協議和股權掛鉤交易。 Meta 的 6 GW Instinct 採購協議就包含了 AMD 的股票認股權證,這便是客戶利用資產負債表優勢來確保佔有率分配的一個例證。而缺乏類似談判能力的新創公司則面臨認證週期延長和收入延遲等挑戰。

細分市場分析

2025年,北美資料中心GPU市場主要由雲端設施主導,佔58.90%的市場。然而,隨著對話式人工智慧、擴增實境和自動駕駛汽車推理處理等技術向用戶端延伸,邊緣節點預計將在2031年前以13.89%的複合年成長率成長。隨著通訊業者在其中心機房部署10到50個GPU節點,將延遲降低至兩位數毫秒級,北美資料中心邊緣部署GPU市場正在蓬勃發展。液冷微型模組有助於滿足零售和園區環境中的噪音和散熱要求,而改進的編配能力則使營運商能夠對GPU進行分區,以處理突發的多租戶流量。

邊緣運算的擴展反映了經濟和物理兩方面的因素。回程傳輸TB級Terabyte和影片資料回傳到集中式叢集的成本高於部署本地GPU容量的成本。這一趨勢在加拿大尤其明顯,因為那裡的長途頻寬價格仍然居高不下。多租戶vGPU切片支援部分利用模式,這吸引了眾多中小企業(SMB)開發者。同時,AWS本地區域和Azure邊緣區域等超大規模資料中心業者將雲端管理擴展到本地存取點(POP),將雲端工具與邊緣自主性結合。這些因素共同推動邊緣節點在預測期間內從試點規模走向生產規模。

到2025年,訓練GPU將佔總收入的57.82%,但隨著訓練後計算預算的增加,推理加速器預計將以13.45%的複合年成長率超越訓練GPU。由於Blackwell的FP4引擎、MI355X的288 GB HBM3E顯存以及Gaudi 3的成本績效,北美資料中心推理硬體GPU的市佔率正在不斷擴大。企業更傾向於選擇能夠將每個令牌的功耗降低一半,並在碳排放上限限制下降低總體擁有成本的推理GPU。

隨著架構的融合,訓練和服務之間的界線日漸模糊。整合式 GPU叢集現在可以按需重新配置,Kubernetes 會調度富含 HBM 的節點,使其在白天用於融合幀的微調,在夜間用於高吞吐量推理。測試驅動運算、思維鏈提示和 RLHF 循環正在增加每個使用者查詢的推理週期數,預計三年內需求將達到訓練水準。因此,供應商正在最佳化記憶體頻寬和調度器微代碼以實現即時服務,並基於「每焦耳令牌數」而非純粹的浮點運算次數重新定義效能指標。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模資料中心人工智慧與機器學習訓練工作負載激增

- 財富 500 強企業擴大採用混合雲端策略

- 利用 CSP 加速部署針對生成式 AI 最佳化的 GPU 執行個體。

- 擴展主權雲端區域將推動本地GPU容量的需求

- GPU 解耦和可組合基礎設施的快速發展

- 節能型水冷GPU伺服器的廣泛應用降低了整體擁有成本。

- 市場限制因素

- 先進節點半導體供應鏈持續面臨限制因素

- 資料中心電費上漲和碳排放法規

- 宏觀經濟不確定性導致中小企業凍結資本投資

- 與專有GPU軟體生態系統相關的廠商鎖定風險

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 透過連接方式

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Graphcore Ltd.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Broadcom Inc.

- Marvell Technology Inc.

- Super Micro Computer Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america data center GPU market size is expected to increase from USD 24.89 billion in 2026 to USD 43.88 billion by 2031, growing at a CAGR of 12.01% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), End-User (Hyperscalers/CSPs, Enterprises, and More), and by Country (United States, Canada, and More). The Market Forecasts are Provided in Value (USD).

North America Data Center GPU Market Trends and Insights

Surging AI and ML Training Workloads in Hyperscale Data Centers

Hyperscalers are now training trillion-parameter frontier models on clusters with more than 100,000 GPUs, a scale unlocked by NVLink fabrics that reduce all-reduce latency from minutes to seconds.Record revenue at a leading GPU vendor in 2025 underscored a demand cycle fueled by model budgets surpassing USD 100 million per run. Public-sector projects such as Solstice and Equinox are adopting 10,000-plus GPU clusters for climate models, reinforcing long-term visibility for suppliers. Operators increasingly factor test-time compute into capacity planning, effectively doubling life-cycle GPU requirements as inference budgets grow to parity with training allocations. The resulting pull-through effect keeps advanced-node fabs fully allocated and intensifies competition for HBM capacity.

Growing Adoption of Hybrid Cloud Strategies Among Fortune 500 Enterprises

Enterprises are repatriating AI workloads to on-premises GPU stacks to control proprietary data and avoid cloud egress fees that can top 30% of total spend. Turnkey private-cloud-AI appliances with 4-64 GPUs and SaaS-like management are enabling firms in pharmaceuticals, automotive, and media to fine-tune LLMs behind their firewalls. The hybrid model is underpinned by mature virtualization, with vGPU 19.0 supporting 48 virtual machines per Blackwell GPU and slicing accelerators for multiple business units. During seasonal peaks, overflow jobs burst into CSP capacity, preserving agility without long-term public-cloud lock-in. This fluidity in workload is expanding the addressable market for mid-sized data centers and fueling demand for GPU leasing.

Persistent Semiconductor Supply-Chain Constraints for Advanced Nodes

Lead times for Blackwell and Rubin GPUs now exceed 50 weeks as advanced packaging remains supply-constrained. CoWoS capacity is short of demand, and HBM3E supply is trailing orders through 2026. Vendors are responding with United States fab expansions, but ramp timelines limit near-term relief, forcing hyperscalers into multi-billion-dollar pre-purchase agreements and equity-linked deals. Meta's 6 GW Instinct commitment secured warrants for AMD shares, illustrating how customers leverage balance-sheet capacity to lock in allocation. Start-ups without similar negotiating leverage face prolonged qualification cycles and postponed revenue.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Deployment of Generative-AI-Optimized GPU Instances by CSPs

- Expansion of Sovereign Cloud Regions Demanding On-Prem GPU Capacity

- Rising Data Center Electricity Tariffs and Carbon-Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud facilities dominated the North America data center GPU market in 2025, accounting for 58.90% share, yet edge nodes will compound at a 13.89% CAGR to 2031 as conversational AI, AR, and autonomous-vehicle inference shift closer to users. The North America data center GPU market size for edge deployments is climbing as telecom carriers deploy 10-50 GPU pods in central offices, shaving latency by double-digit milliseconds. Liquid-cooled micro-modules help meet noise and heat limits in retail and campus environments, while improved orchestration lets operators partition GPUs for bursty multi-tenant traffic.

Edge expansion reflects both economics and physics. Backhauling terabytes of sensor and video data to centralized clusters costs more than placing GPU capacity on-site, especially in Canada, where long-haul bandwidth pricing remains high. Multi-tenant vGPU slicing enables fractional consumption models that attract SMB developers. Meanwhile, hyperscaler outposts such as AWS Local Zones and Azure Edge Zones extend cloud management to regional POPs, blending cloud tools with edge sovereignty. Together, these factors propel edge nodes from pilot to production scale throughout the forecast window.

Training GPUs accounted for 57.82% of 2025 revenue, but inference accelerators will outpace it at a 13.45% CAGR as post-training compute budgets rise. The North America data center GPU market share for inference hardware is widening thanks to FP4 engines in Blackwell, 288 GB HBM3E on MI355X, and Gaudi 3's price-performance profile. Enterprises favor inference GPUs that cut watt-hours per generated token by half, improving TCO under carbon caps.

Architectural convergence blurs boundaries between training and serving. Unified GPU clusters now reconfigure on demand, with Kubernetes scheduling HBM-rich nodes for few-shot fine-tuning by day and high-throughput inference overnight. Test-time compute, chain-of-thought prompting, and RLHF loops increase inference cycles per user query, driving demand parity with training within three years. Consequently, vendors are optimizing memory bandwidth and scheduler microcode for real-time serving, redefining performance metrics around tokens per joule rather than pure FLOPs.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Graphcore Ltd.

- Cerebras Systems Inc.

- Tenstorrent Inc.

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Broadcom Inc.

- Marvell Technology Inc.

- Super Micro Computer Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging AI and ML training workloads in hyperscale data centers

- 4.2.2 Growing adoption of hybrid cloud strategies among Fortune 500 enterprises

- 4.2.3 Accelerated deployment of generative AI-optimized GPU instances by CSPs

- 4.2.4 Expansion of sovereign cloud regions demanding on-prem GPU capacity

- 4.2.5 Rapid emergence of GPU disaggregation and composable infrastructure

- 4.2.6 Availability of energy-efficient liquid-cooled GPU servers lowering TCO

- 4.3 Market Restraints

- 4.3.1 Persistent semiconductor supply-chain constraints for advanced nodes

- 4.3.2 Rising data-center electricity tariffs and carbon-emission regulations

- 4.3.3 Capital-expenditure freeze among SMBs owing to macro uncertainty

- 4.3.4 Vendor lock-in risks tied to proprietary GPU software ecosystems

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Graphcore Ltd.

- 6.4.5 Cerebras Systems Inc.

- 6.4.6 Tenstorrent Inc.

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Samsung Electronics Co., Ltd.

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 Broadcom Inc.

- 6.4.11 Marvell Technology Inc.

- 6.4.12 Super Micro Computer Inc.

- 6.4.13 Dell Technologies Inc.

- 6.4.14 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

中東和非洲資料中心GPU:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)東南亞資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)