|

市場調查報告書

商品編碼

2065499

英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)United Kingdom Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

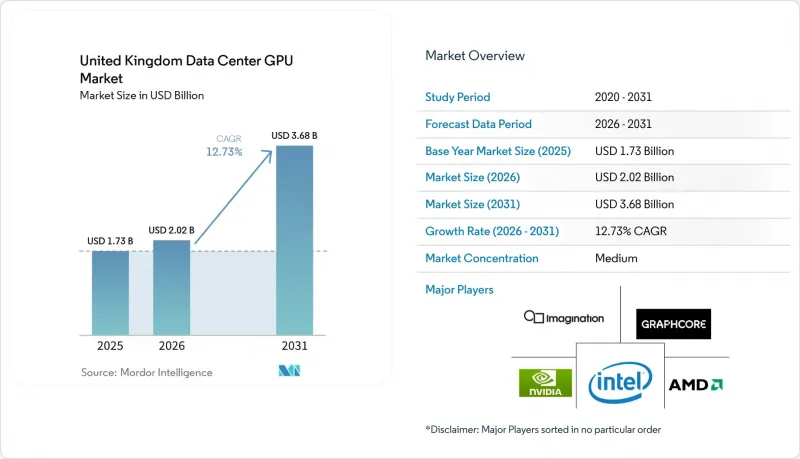

據 Mordor Intelligence 稱,2025 年英國資料中心 GPU 市值為 17.3 億美元,預計到 2031 年將從 2026 年的 20.2 億美元成長至 36.8 億美元,預測期(2026-2031 年)的複合年成長率為 12.73%。

本報告按部署類型(雲端資料中心、企業/私人資料中心等)、GPU 類型(訓練 GPU 和推理 GPU)、互連方式(基於 PCIe 的 GPU 和高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算、資料分析等)以及最終用戶(超大規模資料中心業者/雲端服務供應商、企業等)進行細分。市場預測以美元計價。

英國資料中心GPU市場的趨勢與洞察

加速英國公司採用人工智慧工作負載

企業正將面向客戶的運作中應用程式從公共雲端遷移到專用雲端平台,以確保低延遲、合規性和可預測的成本。由本地整合商提供的私有AI平台提供包含儲存、網路和託管軟體的承包叢集,將引進週期從數月縮短至數週。在銀行、醫療保健和關鍵基礎設施等高度監管的行業,這種需求尤其旺盛,因為在這些行業中,本地控制和可審計性比雲端固有的可擴展性更為重要。硬體供應商也積極回應,提供更小巧、更節能的GPU SKU,以適應現有的功率等級,從而實現分階段升級,而無需從頭開始構建。

英國可用區超大規模資料中心業者中心擴張

AWS、微軟和Google正在實施一項多年建設計劃,將新的可用區疊加到重新設計的AI成長區之上。由於分區核准流程已從先前的18個月縮短至約12個月,建設前置作業時間也隨之縮短。超大規模資料中心業者可優先連接電網,而地方政府則可在未來25年內收取全額營業稅,從而形成稅收和基礎設施擴張相互促進的良性循環。每個超大規模資料中心業者中心園區都已預留可再生能源發電用地並簽訂了專用線路電力供應契約,以確保新增發電容量不會超過國家碳預算。此外,超大規模資料中心業者資料中心營運商的土地收購也吸引了光纖骨幹網路、資料中心設施及相關供應商落腳周邊地區,進一步加劇了小規模託管業者的競爭。

高階GPU供應鏈的限制

CoWoS封裝瓶頸和HBM3e供應鏈緊張導致交付週期超過50週,使得中型企業只能在超大規模資料中心業者之後獲得次要資源。飆升的現貨價格迫使財務長仔細權衡:是選擇以每小時75至95英鎊(101.93至129.11美元)的價格租賃GPU,還是購買可能無法在整個預算週期內交付的硬體。這種短缺導致人們對ASIC的興趣迅速成長,軟體團隊正在努力壓縮模型,以最大限度地利用現有硬體。

細分市場分析

儘管邊緣運算設施在2025年僅佔英國資料中心GPU市場規模的一小部分,但隨著製造商對低於10毫秒推理處理速度的需求,其正以13.77%的複合年成長率快速成長,直至2031年。斯托克頓-蒂斯將建成40個神經邊緣運算站點中的第一個。每個網站都針對緊湊型165W RTX PRO GPU進行了最佳化,使工廠無需將幀發送到倫敦進行處理即可運作視覺檢測線。

延遲經濟學正在重塑網路拓撲結構。超大規模超大規模資料中心業者正透過在營運商機房內建立微區域,並建立私有傳輸迴路將邊緣節點與其主園區連接起來來應對這項挑戰。混合模式在許多中型企業中日益普及。高容量訓練任務在低成本的蘇格蘭區域運行,而面向客戶的推理任務則在毗鄰都會區域的邊緣節點上運行。這種協作模式使營運商能夠在電力價格套利和基於合規性的資料局部之間取得平衡,既能保持雲端在處理大規模批量任務方面的優勢,又能加速邊緣運算的成長。

到2025年,推理晶片將佔英國資料中心GPU市場佔有率的55.66%,超過訓練GPU。隨著即時客戶回應成為核心工作負載,預計到2031年,訓練GPU的複合年成長率將達到14.11%。

儘管訓練對於基礎模型提供者仍然至關重要,但隨著大多數公司現在更多地採用微調而非從頭開始訓練的方式,對頂級HBM記憶體的整體需求正在萎縮。供應商正在調整其產品線以適應這一趨勢。雙槽250W推理闆卡正變得越來越普及,而超高密度NVLink托架則在超大規模資料中心集群部署。這種產品分化使營運商能夠最佳化部署規模、實現晶片來源多元化並規避未來供應中斷的風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速英國公司採用人工智慧工作負載

- 超大規模資料中心業者擴大了英國的可用區。

- 政府對數位基礎設施和人工智慧研究的支持措施

- 對自主雲端 GPU 執行個體的需求不斷成長

- 邊緣運算在智慧製造走廊中的融合

- 水冷式GPU伺服器的興起滿足了永續性的要求

- 市場限制因素

- 尖端GPU供應鏈的限制因素

- 能源成本上升和碳排放減少目標

- 英國系統整合商缺乏高頻寬互連方面的專業知識。

- 在推理工作負載方面與ASIC加速器競爭

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

- 按GPU類型

- 訓練 GPU

- 用於推理的GPU

- 透過連接方式

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

- 依工作負載類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

- 最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Graphcore Ltd.

- Imagination Technologies Ltd.

- Arm Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Dell Technologies Inc.

- Lenovo Group Limited

- Super Micro Computer, Inc.

- Fujitsu Limited

- Penguin Solutions, Inc.

- OCF Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom data center GPU market size was valued at USD 1.73 billion in 2025 and is estimated to grow from USD 2.02 billion in 2026 to reach USD 3.68 billion by 2031, at a CAGR of 12.73% during the forecast period (2026-2031).

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise / Private Data Centers, and More), GPU Type (Training GPUs and Inference GPUs), Interconnect (PCIe-Based GPUs and High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, Data Analytics, and More), and End-User (Hyperscalers/CSPs, Enterprises, and More). The Market Forecasts are Provided in Value (USD).

United Kingdom Data Center GPU Market Trends and Insights

Accelerated Adoption of AI Workloads by United Kingdom Enterprises

Enterprises are migrating live customer-facing applications from the public cloud to dedicated stacks that guarantee latency, compliance, and predictable costs. Private AI platforms offered by local integrators deliver turnkey clusters bundled with storage, networking, and managed software, compressing deployment cycles from months to weeks. Demand is especially strong in regulated verticals, banking, healthcare, and critical infrastructure, where on-premises control and auditability outweigh raw cloud elasticity. Hardware vendors respond with smaller, energy-efficient GPU SKUs that fit within existing power envelopes, enabling phased upgrades rather than greenfield builds.

Hyperscaler Expansion of United Kingdom Availability Zones

AWS, Microsoft, and Google are rolling out multi-year build programs that layer new availability zones on top of AI Growth Zone planning reforms. Construction lead times are shrinking because zoning approvals now take roughly 12 months, down from 18 previously. Hyperscalers gain priority grid connections, while local authorities retain all business rates for a quarter-century, creating a self-reinforcing loop of tax revenue and infrastructure expansion. Each of these hyperscale campuses reserves parcel space for renewable generation or private-wire import agreements, ensuring that incremental megawatts do not breach national carbon budgets. The hyperscaler land grabs, in turn, pull optical fiber backbones, data center housing, and tertiary suppliers into adjacent districts, raising the competitive bar for smaller colocations.

Supply Chain Constraints for Advanced GPUs

CoWoS packaging bottlenecks and tight HBM3e supply push delivery windows beyond 50 weeks, relegating mid-tier enterprises to secondary allocation after hyperscalers. Spot pricing spikes force CFOs to weigh GPU rental at GBP 75-95 (USD 101.93 - 129.11) per hour against capital purchases that may not arrive for an entire budget cycle. The shortage is accelerating interest in ASICs and pushing software teams toward model compression to stretch existing hardware.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Digital Infrastructure and AI Research

- Growing Demand for Sovereign Cloud GPU Instances

- Rising Energy Costs and Carbon Targets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Edge facilities captured a smaller share of the United Kingdom data center GPU market size in 2025, but are accelerating at a 13.77% CAGR through 2031 as manufacturers demand sub-10 millisecond inference. Stockton-on-Tees will host the first of 40 neural-edge sites, each optimized for compact 165 W RTX PRO GPUs, allowing factories to run visual inspection lines without shipping frames to London for processing.

Latency economics shape network topology. Hyperscalers respond by seeding micro-regions within carrier hotels and creating private transit rings to connect edge nodes back to their flagship campuses. For many mid-market enterprises, a hybrid approach dominates: bulk training jobs run in low-cost Scottish zones, while customer-facing inference runs on a metro-adjacent edge node. This choreography lets operators balance power-price arbitrage against compliance-driven data locality, sustaining cloud dominance for large-scale batch jobs while still rewarding edge expansion.

Inference silicon accounted for 55.66% of the United Kingdom data center GPU market share in 2025, outpacing training GPUs, which posted a 14.11% CAGR through 2031 as real-time customer interactions become the core workload.

Training remains mission-critical for foundation-model providers, but most enterprises now fine-tune rather than train from scratch, shrinking overall demand for top-bin HBM memory footprints. Vendors segment their catalog accordingly: dual-slot, 250 W inference boards proliferate, while ultra-dense NVLink trays cluster at hyperscale sites. This bifurcation allows operators to right-size deployments and diversify chip sourcing, a hedge against future supply disruptions.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Graphcore Ltd.

- Imagination Technologies Ltd.

- Arm Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

- Dell Technologies Inc.

- Lenovo Group Limited

- Super Micro Computer, Inc.

- Fujitsu Limited

- Penguin Solutions, Inc.

- OCF Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Adoption of AI Workloads by UK Enterprises

- 4.2.2 Hyperscaler Expansion of UK Availability Zones

- 4.2.3 Government Incentives for Digital Infrastructure and AI Research

- 4.2.4 Growing Demand for Sovereign Cloud GPU Instances

- 4.2.5 Convergence of Edge Computing in Smart Manufacturing Corridors

- 4.2.6 Rise of Liquid-Cooled GPU Servers to Meet Sustainability Mandates

- 4.3 Market Restraints

- 4.3.1 Supply Chain Constraints for Advanced GPUs

- 4.3.2 Rising Energy Costs and Carbon Targets

- 4.3.3 Limited High-Bandwidth Interconnect Expertise Among UK Integrators

- 4.3.4 Competition from ASIC Accelerators for Inference Workloads

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Type

- 5.1.1 Cloud Data Centers

- 5.1.2 Enterprise / Private Data Centers

- 5.1.3 Edge Data Centers

- 5.2 By GPU Type

- 5.2.1 Training GPUs

- 5.2.2 Inference GPUs

- 5.3 By Interconnect

- 5.3.1 PCIe-Based GPUs

- 5.3.2 High-Bandwidth Interconnect GPUs

- 5.4 By Workload Type

- 5.4.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 5.4.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 5.4.3 Data Analytics (database acceleration, query processing)

- 5.4.4 Graphics and Visualization (VDI, rendering, digital twins)

- 5.5 By End-User

- 5.5.1 Hyperscalers / Cloud Service Providers

- 5.5.2 Enterprises

- 5.5.3 Government and Research Institutions

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Graphcore Ltd.

- 6.4.5 Imagination Technologies Ltd.

- 6.4.6 Arm Ltd.

- 6.4.7 Amazon Web Services, Inc.

- 6.4.8 Microsoft Corporation

- 6.4.9 Dell Technologies Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Super Micro Computer, Inc.

- 6.4.12 Fujitsu Limited

- 6.4.13 Penguin Solutions, Inc.

- 6.4.14 OCF Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年) 資料中心圖形處理器 (GPU) 市場預測至 2034 年:按部署模式、功能、最終用戶和地區分類的全球分析AI資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

資料中心圖形處理器 (GPU) 市場預測至 2034 年:按部署模式、功能、最終用戶和地區分類的全球分析AI資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 資料中心GPU市場:2026年至2032年全球市場預測,依產品、記憶體容量、伺服器密度、功耗範圍、應用、部署模式及最終用戶分類

資料中心GPU市場:2026年至2032年全球市場預測,依產品、記憶體容量、伺服器密度、功耗範圍、應用、部署模式及最終用戶分類