|

市場調查報告書

商品編碼

2072689

印度資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)India Data Center GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

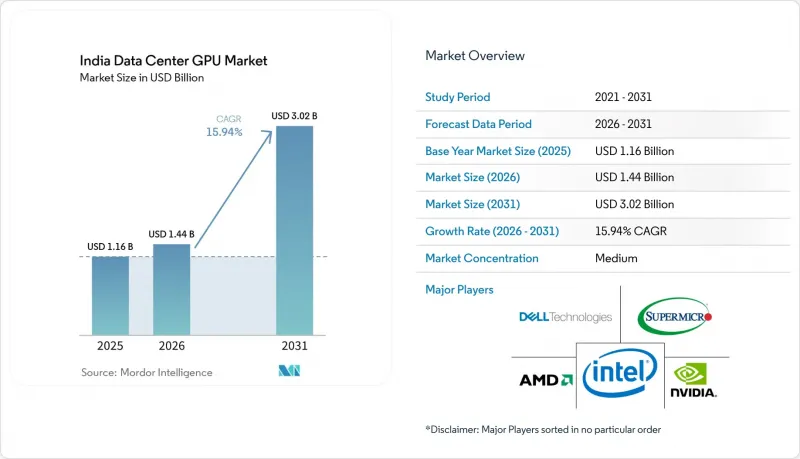

根據 Mordor Intelligence 預測,印度資料中心 GPU 市場預計將從 2025 年的 11.6 億美元成長到 2026 年的 14.4 億美元,到 2031 年達到 30.2 億美元,2026 年至 2031 年的複合年預計成長率為 15.94%。

本報告按部署類型(雲端資料中心、企業/私人資料中心等)、GPU 類型(訓練 GPU、推理 GPU)、互連方式(基於 PCIe 的 GPU、高頻寬互連 GPU)、工作負載類型(人工智慧和機器學習、高效能運算等)以及最終用戶(超大規模資料中心業者伺服器/雲端服務供應商、企業、政府機構和研究機構)進行細分。市場預測以美元 (USD) 為單位。

印度資料中心GPU市場的趨勢與洞察

印度超大規模雲端區域的快速擴張

亞馬遜雲端服務 (AWS)、Google雲端、微軟和甲骨文前所未有的資本投資,已將新的產能建置週期縮短至不到 24 個月,可以肯定的是,到 2028 年,印度資料中心 GPU 市場的總庫存量將翻倍以上。僅 AWS 一家就在海得拉巴投資了 70 億美元,而谷歌在維沙卡帕特南投資的 150 億美元區域則將海底光纜登陸點與 H100叢集相結合,以支持多語言推理工作負載。這波投資浪潮已將印度 SaaS 供應商的往返延遲從 200-300 毫秒降低到 50 毫秒以下,這項改進將直接提升建議引擎的客戶轉換率。伴隨這些投資而來的就業創造計畫旨在認證 10 萬名 AI 開發人員,從而強化一個良性循環:不斷擴大的人才庫將帶動 GPU 利用率的提高。超大規模資料中心業者資料中心的採購規模確保了英偉達和 AMD 的早期配額,保護了國內供應鏈免受全球供不應求。

政府基於「數位印度」和數據本地化標準的獎勵

價值10372印度盧比(約12.4億美元)的「印度人工智慧計畫」(IndiaAI Mission)以每小時65盧比的補貼價格分配了38,000個GPU,與典型的雲端價格相比,將原型訓練的經濟門檻降低了70%。巧合的是,數據本地化法規強制要求銀行、保險公司和醫院將受監管的數據保留在印度境內,這刺激了對專用和託管GPU叢集的新資本投資。與生產連結獎勵計畫(涵蓋增量收入的4-6%)降低了本地系統整合商的總系統成本,使其定價比品牌OEM製造商低15-20%。該計劃與印度標準局(BIS)的認證相結合,解決了傳統上與白盒硬體相關的品質問題。政府機構和銀行、金融和保險(BFSI)行業的早期採用推動了企業GPU機架租賃協議年增40%,顯示市場需求持續旺盛。

對配備GPU的資料中心進行大量資本投資。

即使扣除房地產和電力成本,每個配備八塊H100 GPU的機架成本也高達40萬至50萬美元。這迫使中型業者將40%至50%的股本用於企劃案融資交易,而成熟經濟體通常的比例為25%至30%。液冷系統的改造對於高密度人工智慧叢集至關重要,而每個機架的改造成本又增加了5萬至8萬美元,在碳排放揭露法規日益嚴格的背景下,這進一步推高了能源消耗。貸款機構仍對專用硬體的殘值風險持謹慎態度,導致其利率差比傳統資料中心專案高出250個基點。在二線位置,電力供應運轉率不到99.99%,迫使開發商安裝大量的柴油發電機和電池組,這又使總建設成本增加了20%至25%。如果沒有針對性的綠色融資措施來獎勵提高電力使用效率 (PUE),大都會圈叢集以外的新進業者將面臨高昂的成本曲線。

細分市場分析

預計到2025年,雲端資料中心將佔據印度資料中心GPU市場佔有率的63.28%,凸顯了超大規模資料中心業者大規模資料中心透過精細化的資源利用層級整合工作負載並實現GPU貨幣化的能力。同時,邊緣資料中心被認為是成長最快的細分市場,到2031年複合年成長率將達到16.94%。在目前印度資料中心的GPU市場,AWS、微軟Azure和Google雲端正在推出符合資料居住要求的區域特定H100實例,這項轉變正獲得銀行和生命科學公司的支持。企業正在利用這種基礎設施運行短期培訓任務,而無需承擔資本支出(Capex),將資產負債表風險轉化為營運支出(OpEx)。邊緣設施(通常是連接到5G基地台的100千瓦節點)是成長最快的節點類別,能夠將自主機器人和智慧城市攝影機的推理延遲降低到10毫秒以下。

這項轉變的驅動力在於印度400個城市部署5G網路,擴大了邊緣運算的覆蓋範圍,並建立了明確的延遲保障。像Bharti Airtel這樣的通訊業者正利用與NVIDIA的合作關係,預裝推理最佳化型GPU,建構可向OTT媒體、物流和零售客戶提升銷售的資產基礎。在監管嚴格的產業中,私有資料中心的重要性仍然很高。受FDA審計追蹤約束的藥品出口商和受敏感資料處理法規約束的國防相關企業仍在採購獨立的GPU叢集。因此,印度資料中心GPU市場正呈現混合拓樸結構,分佈於雲端、託管和邊緣,而非集中於單一模式。

到2025年,推理GPU將佔印度資料中心GPU市場的58.37%。這主要得益於商業聊天機器人、產品建議引擎和即時詐欺偵測模型等應用的需求,這些應用需要高吞吐量且能效高的晶片。 NVIDIA的L4和L40S模組憑藉其卓越的每瓦查詢以及與都市區託管設施日益嚴格的供電限制相匹配的特性,在市場上佔據主導地位。同時,訓練GPU預計在整個預測期內將維持最高的成長率,到2031年複合年成長率將達到17.45%。儘管訓練GPU的出貨量較低,但由於其平均售價較高以及印度政府對印度語言和多模態內容專有模型的政策支持,其市場仍在快速成長。

Sarvam AI 部署的 4,096 個 H100 集群表明,宏觀層面的政策目標正引導資金流向高密度、專用於訓練的叢集。同時,雲端供應商也開始提供按需的 8 GPU 切片,以擴大團隊的存取權限,使他們能夠微調開放權重模型,而不是從頭開始建立模型。企業通常會將 H100叢集用於定期重新訓練,並將 L40S 集群用於日常推理,從而在資金限制和延遲目標之間取得平衡。這種混合叢集策略凸顯了需求曲線的細微差別:印度資料中心 GPU 市場既需要滿足用於訓練的高頻寬、緊密耦合架構的需求,也需要滿足用於推理的以 PCIe 為中心的低功耗顯示卡的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 印度超大規模雲端區域的快速擴張

- 政府基於「數位印度」計畫和數據本地化法規的獎勵

- 人工智慧新創企業生態系統對GPU加速運算的需求日益成長

- 影片串流、遊戲和 AR/VR 的激增增加了對基於 GPU 的轉碼和渲染的需求。

- 5G 和邊緣運算的部署將加速配備 GPU 的微型資料中心的普及。

- 資料中心GPU每TFLOPS成本的下降正在推動其應用範圍的擴大。

- 市場限制因素

- 對配備GPU的資料中心進行大量資本投資

- 由於國內生產能力不足,導致進口依賴。

- 印度二、三線城市電力與冷凍基礎設施面臨的限制因素

- 先進封裝組件(HBM、中介層)的供應鏈波動性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

第6章:依部署類型

- 雲端資料中心

- 企業/私人資料中心

- 邊緣資料中心

第7章:依GPU類型分類

- 訓練 GPU

- 用於推理的GPU

第8章 互連

- 基於 PCIe 的 GPU

- 高頻寬互連GPU

第9章 工作量類型

- 人工智慧(AI)和機器學習(ML)

- 高效能運算(HPC)(科學運算,不包括人工智慧)

- 資料分析(資料庫加速、查詢處理)

- 圖形和視覺化(VDI、渲染、數位雙胞胎)

第10章:最終用戶

- 超大規模資料中心業者雲端服務供應商/雲端服務供應商

- 公司

- 政府和研究機構

第11章 競爭格局

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介(每份簡介包括全球概覽、市場概覽、主要細分市場、現有財務資訊、策略資訊、市場排名和佔有率、產品和服務以及近期發展。)

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- ASUSTeK Computer Inc.

- Dell Technologies Inc.

- Super Micro Computer, Inc.

- Giga-Computing Technology Co., Ltd.(GIGABYTE)

- Lenovo Group Limited

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Reliance Industries Limited(Jio Platforms)

- Bharti Airtel Limited(Nxtra Data)

- Sify Technologies Limited

- CtrlS Datacenters Ltd.

- STT Global Data Centres India Pvt. Ltd.

- Yotta Infrastructure Solutions LLP

- AdaniConneX Private Limited

- NTT Global Data Centers and Cloud Infrastructure India Pvt. Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

第12章 市場機會與未來展望

- 評估閒置頻段和未滿足的需求

According to Mordor Intelligence, the india data center GPU market size is expected to increase from USD 1.16 billion in 2025 to USD 1.44 billion in 2026 and reach USD 3.02 billion by 2031, growing at a CAGR of 15.94% over 2026-2031.

This report is Segmented by Deployment Type (Cloud Data Centers, Enterprise/Private Data Centers, and More), GPU Type (Training GPUs, Inference GPUs), Interconnect (PCIe-Based GPUs, High-Bandwidth Interconnect GPUs), Workload Type (AI and ML, HPC, and More), and End-User (Hyperscalers/CSPs, Enterprises, Government and Research Institutions). Market Forecasts are Provided in Terms of Value (USD).

India Data Center GPU Market Trends and Insights

Rapid Expansion of Hyperscale Cloud Regions in India

Unprecedented capital expenditure by Amazon Web Services, Google Cloud, Microsoft, and Oracle is compressing build cycles for new capacity to under 24 months, ensuring that aggregate GPU inventory in the India data center GPU market will more than double before 2028.AWS alone earmarked USD 7 billion for Hyderabad, while Google's USD 15 billion Visakhapatnam region is pairing subsea cable landings with H100 clusters to serve multilingual inference workloads. This wave of investment shortens round-trip latency for Indian SaaS providers from 200-300 milliseconds to sub-50 milliseconds, a gain that directly raises customer conversion rates for recommendation engines. Job creation programs attached to these investments aim to certify 100,000 AI developers, reinforcing a virtuous cycle where a larger talent pool drives higher GPU utilization. Hyperscalers' purchasing scale also secures early allocations from NVIDIA and AMD, shielding the domestic supply stack from global shortages.

Government Incentives Under Digital India and Data Localization Norms

The INR 10,372 crore (USD 1.24 billion) IndiaAI Mission reserves 38,000 GPUs for subsidized usage at INR 65 per hour, lowering the economic barrier for prototype training runs by 70% relative to retail cloud pricing. Parallel data-localization statutes compel banks, insurers, and hospitals to retain regulated data inside India, a mandate that steers fresh capex toward both captive and colocation GPU clusters. Production-linked incentives covering 4-6% of incremental sales reduce total system costs for local integrators, letting them undercut branded OEMs by 15-20%. When combined with Bureau of Indian Standards certification, the scheme removes quality concerns traditionally associated with white-box hardware. Early adoption in government and BFSI workloads has already produced a 40% year-over-year jump in enterprise GPU rack leases, signaling durable demand.

High Capital Expenditure for GPU-Equipped Data Centers

A single rack populated with eight H100 GPUs costs USD 400,000-500,000, excluding real estate and power provisioning, which forces mid-market operators to allocate 40-50% equity in project finance deals versus the 25-30% norms observed in mature economies. Liquid cooling retrofits, now indispensable for dense AI clusters, add another USD 50,000-80,000 per rack and push energy footprints higher at a time when carbon disclosure mandates are tightening. Lenders remain wary of residual-value risk on specialized hardware, making interest spreads up to 250 basis points wider than for traditional data-center projects. In Tier-2 locations, the absence of 99.99% utility uptime obliges developers to oversize diesel gensets and battery strings, lifting all-in build costs by an additional 20-25%. Without targeted green-financing instruments that reward improved power usage effectiveness, new entrants outside the metro clusters face a prohibitive cost curve.

Other drivers and restraints analyzed in the detailed report include:

- Rising AI Startup Ecosystem Demand for GPU-Accelerated Compute

- Surge in Video Streaming, Gaming and AR/VR Requiring GPU-Based Transcoding and Rendering

- Limited Domestic Manufacturing Capacity Leading to Import Dependency

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud data centers accounted for 63.28% of the India data center GPU market share in 2025, underscoring hyperscalers' ability to aggregate workloads and monetize GPUs via granular usage tiers, while edge data centers were identified as the fastest-growing segment through at 16.94% CAGR through 2031. The India data center GPU market now sees AWS, Microsoft Azure, and Google Cloud touting region-locked H100 instances that comply with data-residency statutes, a pivot that resonates with banks and life-sciences firms. Enterprises piggyback on these footprints, spinning up short-lived training jobs without committing capex and thereby shifting balance-sheet exposure to opex. Edge facilities, often 100-kilowatt pods attached to 5G base stations, are the fastest-growing node category because they reduce inference latency to sub-10 milliseconds for autonomous mobile robots and smart-city cameras.

The shift is powered by India's 5G rollout across 400 cities, which is widening the addressable edge radius and establishing deterministic latency guarantees. Telecom operators such as Bharti Airtel leverage partnerships with NVIDIA to pre-install inference-optimized GPUs, creating an asset base that can be upsold to over-the-top media, logistics, and retail clients. Private data centers remain relevant for regulated verticals: pharmaceutical exporters subject to FDA audit trails and defense contractors bound by classified-data handling rules continue to procure isolated GPU clusters. The result is a hybrid topology in which the India data center GPU market size gets distributed across cloud, colocation, and edge rather than gravitating toward a single archetype.

Inference GPUs secured 58.37% of the India data center GPU market size in 2025, driven by commercial chatbots, product-recommendation engines, and real-time fraud-detection models that require high-throughput yet power-efficient silicon. NVIDIA's L4 and L40S modules dominate because they deliver superior queries-per-watt, an attribute that dovetails with tightening power-availability caps in urban colocation campuses, whereas training GPUs are registering the highest growth at 17.45% CAGR through 2031 momentum across the forecast window. Training GPUs, while smaller in volume, command higher average selling prices and are expanding quickly as sovereign models for Indic languages and multimodal content gain policy backing.

Sarvam AI's 4,096-H100 deployment illustrates how macro-level policy ambitions funnel capital into dense, training-only clusters. Concurrently, cloud vendors have launched on-demand eight-GPU slices that democratize access for teams looking to fine-tune open-weights models instead of building from scratch. Enterprises often pair H100 clusters for periodic retraining with L40S fleets for day-to-day inference, striking an internal equilibrium between capex constraints and latency targets. This mixed-fleet strategy underlines a nuanced demand curve: the India data center GPU market must accommodate both high-bandwidth, tightly coupled fabrics for training and PCIe-centric, power-sipping cards for inference.

Complete Report Scope:

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- ASUSTeK Computer Inc.

- Dell Technologies Inc.

- Super Micro Computer, Inc.

- Giga-Computing Technology Co., Ltd. (GIGABYTE)

- Lenovo Group Limited

- Cisco Systems, Inc.

- Hewlett Packard Enterprise Company

- Reliance Industries Limited (Jio Platforms)

- Bharti Airtel Limited (Nxtra Data)

- Sify Technologies Limited

- CtrlS Datacenters Ltd.

- STT Global Data Centres India Pvt. Ltd.

- Yotta Infrastructure Solutions LLP

- AdaniConneX Private Limited

- NTT Global Data Centers and Cloud Infrastructure India Pvt. Ltd.

- Amazon Web Services, Inc.

- Microsoft Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Hyperscale Cloud Regions in India

- 4.2.2 Government Incentives Under Digital India and Data Localization Norms

- 4.2.3 Rising AI Startup Ecosystem Demand for GPU-Accelerated Compute

- 4.2.4 Surge in Video Streaming, Gaming and AR/VR Requiring GPU-Based Transcoding and Rendering

- 4.2.5 Deployment of 5G and Edge Computing Driving Micro Data Centers With GPUs

- 4.2.6 Declining Cost per TFLOP of Data Center GPUs Enabling Broader Adoption

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for GPU-Equipped Data Centers

- 4.3.2 Limited Domestic Manufacturing Capacity Leading to Import Dependency

- 4.3.3 Power and Cooling Infrastructure Constraints in Tier-2/3 Indian Cities

- 4.3.4 Supply-Chain Volatility in Advanced Packaging Components (HBM, Interposers)

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

6 By Deployment Type

- 6.1 Cloud Data Centers

- 6.2 Enterprise / Private Data Centers

- 6.3 Edge Data Centers

7 By GPU Type

- 7.1 Training GPUs

- 7.2 Inference GPUs

8 By Interconnect

- 8.1 PCIe-Based GPUs

- 8.2 High-Bandwidth Interconnect GPUs

9 By Workload Type

- 9.1 Artificial Intelligence (AI) and Machine Learning (ML)

- 9.2 High-Performance Computing (HPC) (non-AI scientific computing)

- 9.3 Data Analytics (database acceleration, query processing)

- 9.4 Graphics and Visualization (VDI, rendering, digital twins)

10 By End-User

- 10.1 Hyperscalers / Cloud Service Providers

- 10.2 Enterprises

- 10.3 Government and Research Institutions

11 COMPETITIVE LANDSCAPE

- 11.1 Market Concentration

- 11.2 Strategic Moves

- 11.3 Market Share Analysis

- 11.4 Company Profiles (Each profile includes: Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 11.4.1 NVIDIA Corporation

- 11.4.2 Advanced Micro Devices, Inc.

- 11.4.3 Intel Corporation

- 11.4.4 ASUSTeK Computer Inc.

- 11.4.5 Dell Technologies Inc.

- 11.4.6 Super Micro Computer, Inc.

- 11.4.7 Giga-Computing Technology Co., Ltd. (GIGABYTE)

- 11.4.8 Lenovo Group Limited

- 11.4.9 Cisco Systems, Inc.

- 11.4.10 Hewlett Packard Enterprise Company

- 11.4.11 Reliance Industries Limited (Jio Platforms)

- 11.4.12 Bharti Airtel Limited (Nxtra Data)

- 11.4.13 Sify Technologies Limited

- 11.4.14 CtrlS Datacenters Ltd.

- 11.4.15 STT Global Data Centres India Pvt. Ltd.

- 11.4.16 Yotta Infrastructure Solutions LLP

- 11.4.17 AdaniConneX Private Limited

- 11.4.18 NTT Global Data Centers and Cloud Infrastructure India Pvt. Ltd.

- 11.4.19 Amazon Web Services, Inc.

- 11.4.20 Microsoft Corporation

12 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 12.1 White-Space and Unmet-Need Assessment

新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

新加坡資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)德國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本資料中心GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)英國資料中心GPU:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)