|

市場調查報告書

商品編碼

2072662

北美紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)North America Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

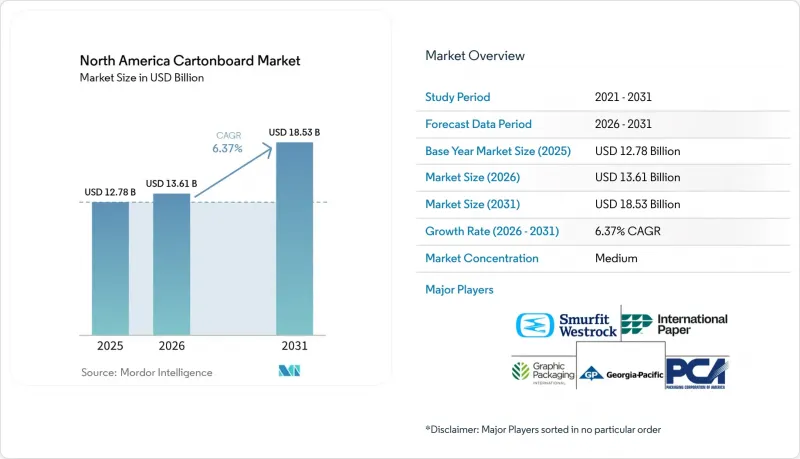

根據 Mordor Intelligence 預測,北美紙板市場規模將從 2025 年的 127.8 億美元和 2026 年的 136.1 億美元成長到 2031 年的 185.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 6.37%。

本報告按產品等級(實心漂白紙板、實心未漂白紙板、折疊盒用紙板、白襯紙板、液體包裝用紙板、食品服務用紙板)、包裝形式(折疊盒、液體包裝、紙套、托盤等)、終端用戶行業(食品、飲料等)和地區(美國等)進行細分。市場預測以美元(USD)為單位。

北美紙板市場趨勢與洞察

塑膠包裝的永續替代品

永續替代方案是北美紙板市場最顯著的長期成長動力之一。這是因為包裝的變革既受監管合規性的影響,也受品牌偏好的驅動。各州和省的包裝法規迫使品牌所有者重新評估初級包裝和二級包裝,從而擴大了紙板在餐飲服務、消費品和零售展示應用領域的應用範圍。這種變革並非簡單的包裝替換。許多轉換需要特定等級的紙板,例如SBS或塗佈未漂白牛皮紙,這提高了單位用量和紙張重量的要求。 2025年1月,美國食品藥物管理局(FDA)確認,所有35項關於紙本和紙板食品包裝中含PFAS油性拒油劑的食品接觸通知均已失效,加速了美國新規範的製定。這項變更也增加了食品接觸應用中對不含PFAS的阻隔紙板的需求。買家現在需要的是檢驗的替代方案,而不是過渡材料。此外,杯子材料從塑膠轉向紙質,也惠及了北美紙板市場,因為去除聚合物層後,需要更厚的紙板才能保持強度。這導致噸位需求增加,而不僅僅是簡單的單位替代。

包裝食品和飲料需求成長

北美紙板市場持續受益於包裝食品和飲料的強勁需求,紙板已深深融入食品雜貨、冷凍食品、冷藏食品和餐飲服務業的包裝系統中。預計到2025年,食品將佔紙板銷售額的36.19%,凸顯了紙板在品牌貨架包裝中的廣泛應用,因為視覺展示和運輸便利性都至關重要。美國餐飲協會表示,持續的需求將在2026年繼續推動餐飲業的發展趨勢,滿足品牌餐飲連鎖店的包裝試點和補貨需求。 Clearwater Paper在2026年第一季報告中指出,食品接觸紙板應用的需求將持續成長,且可折疊紙板的需求依然強勁,餐飲服務業杯盤紙板也表現良好。這項需求對北美紙板市場意義重大。這是因為外帶容器、杯子材料和複合托盤與高頻消費模式密切相關,短期內難以找到替代品。此外,一旦品牌所有者完成生產線合格,食品和飲料包裝形式通常會在漫長的生產週期內保持不變,這為紙板製造商提供了更穩定的途徑來獲得多年供應合約。

纖維、能源和化學原料的投入成本波動很大。

由於原料和公用事業價格的波動並未與合約價格週期同步調整,投入成本的波動仍是北美紙板市場整體獲利的主要限制因素。 Smurfit Westlock公司報告稱,2026年第一季,天氣因素對其息稅折舊攤銷前利潤(EBITDA)的影響高達6500萬美元,主要集中在北美地區。該公司還計劃進行第二輪漲價,以抵消不斷上漲的成本壓力。 Graphic Packaging公司報告稱,其2026年第一季的調整後EBITDA從去年同期的3.65億美元降至2.32億美元,並指出其中3700萬美元的降幅是由於原料和其他成本上漲所致。 Cascade在第一季財報中也指出,原物料成本持續面臨上漲壓力,這顯示無論造紙廠的結構如何,再生紙漿供應鏈都同樣面臨著廣泛的成本壓力。這些壓力對北美紙板原紙市場有重大影響,因為它們進一步凸顯了生產和加工自有紙漿的垂直整合型製造商的優勢。它們也加速了行業整合,因為小規模的造紙廠和獨立運營商吸收滯後的價格上漲以及能源、再生紙漿和特種塗料價格的急劇上漲的能力有限。

細分市場分析

到2025年,液體包裝紙板(LPB)將佔據北美紙板市場28.44%的佔有率,成為該地區最大的產品等級。其市場地位得益於高度整合的無菌包裝和山形蓋頂紙板供應鏈,這些供應鏈支撐著乳製品、植物來源飲料、果汁和湯類產品的包裝。在這些領域,灌裝線的整合往往會鞏固長期的採購週期。因此,LPB在北美紙板市場擁有穩定的需求基礎,與許多特定消費品包裝應用相比,其受包裝規格突然變化的影響較小。可折疊紙板仍用於高階消費品,其厚度均勻、白度高、印刷效果良好仍是塑造品牌形象的重要因素。未漂白紙板和白色背襯塗佈紙板繼續用於對成本敏感的飲料多包裝和一般零售包裝應用,但永續性的永續性需求正促使人們對紙板等級的選擇和纖維認證進行更嚴格的審查。

北美紙板產業正呈現出明顯的兩極化趨勢:傳統主流紙板等級與新興的成長型紙板等級(主要用於食品接觸應用)並存。受塑膠禁令、可堆肥包裝需求以及外帶和配送消費持續成長的推動,預計到2031年,食品服務紙板的複合年成長率將達到7.14%。 Clearwater Paper在其2026年第一季說明中指出,其擠出產品(包括用於杯子和聚乙烯塗層折疊紙盒的紙板)已售罄,這表明與產品重新設計和加工活動相關的食品接觸應用領域供應緊張。這種情況意義重大,因為轉向不含PFAS和PE的解決方案不僅改變了紙板的化學成分,而且通常還會改變紙板的厚度、加工速度和每噸附加價值。因此,北美紙板產業正在調整其產品組合,轉向那些能夠在單一產品中同時提供阻隔性能、符合法規要求和高產量效率的紙板等級。此外,輕型中階 SBS 替代品的出現表明了一種更有選擇性的購買模式,加工商會比較實際生產量和印刷性能,而不是僅僅依賴紙板的表面價格。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 塑膠包裝的永續替代品

- 包裝食品和飲料需求成長

- 美容和個人護理行業對高品質印刷材料和吸引人的展示品有需求。

- 電子商務和會員制零售業對二次包裝的需求

- 不含 PFAS 和 PE 的阻隔板創新

- 藥品序列化和生物製藥紙盒包裝的複雜性。

- 市場限制因素

- 纖維、能源和化學原料成本的波動

- 來自軟性包裝和替代包裝形式的競爭

- 州級 PFAS 法規合規性維修和認證週期

- 加拿大的紙板生產能力捉襟見肘,越來越依賴進口。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按產品等級

- 固體漂白紙板

- 固體未漂白紙板

- 折疊紙板

- 球場用球的白色底面

- 用於液體包裝的紙板

- 食品服務用紙板

- 按包裝類型

- 折疊紙箱

- 液體包裝

- 袖套和托盤

- 其他包裝形式(杯子、食品服務容器)

- 按最終用戶行業分類

- 食物

- 飲料

- 藥品和醫療保健

- 菸草

- 化妝品和盥洗用品

- 其他終端用戶產業(玩具、服飾、汽車、家居用品、電器、餐飲服務業)

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- International Paper Company

- Georgia-Pacific LLC

- Packaging Corporation of America

- Clearwater Paper Corporation

- Sonoco Products Company

- Cascades Inc.

- Metsa Board Corporation

- Mayr-Melnhof Karton Aktiengesellschaft

- Billerud Aktiebolag(publ)

- Stora Enso Oyj

- Tetra Pak International SA

- SIG Group AG

- Huhtamaki Oyj

- CCL Industries Inc.

- Diamond Packaging

- American Carton Company

- Keystone Folding Box Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america cartonboard market size is projected to expand from USD 12.78 billion in 2025 and USD 13.61 billion in 2026 to USD 18.53 billion by 2031, registering a CAGR of 6.37% between 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, and More), and Geography (United States, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America Cartonboard Market Trends and Insights

Sustainable Substitution From Plastic Packaging

Sustainable substitution has become one of the clearest long-run supports for the North America cartonboard market because packaging changes are now being shaped by compliance as much as by brand preference. State and provincial packaging rules have pushed brand owners to reassess both primary and secondary formats, thereby widening the role of cartonboard in foodservice, consumer goods, and retail display applications. The shift is not limited to replacing one package with another, because many conversions require specific grades, such as SBS and coated unbleached kraft, which increase both carton counts and basis-weight requirements per unit. The FDA's confirmation in January 2025 that all 35 food contact notifications for PFAS-containing grease-proofing agents in paper and paperboard food packaging were no longer effective accelerated new specification work across the United States. That change also strengthened demand for PFAS-free barrier board in food-contact applications, where buyers now need validated alternatives rather than transitional materials. The North America cartonboard market also benefits when plastic-to-paper conversions in cup stock require heavier board to preserve strength after the polymer layer is removed, thereby raising tonnage demand beyond simple unit substitution.

Growth In Packaged Food And Beverage Demand

The North America cartonboard market continues to draw stable support from packaged food and beverage demand because cartonboard remains deeply embedded in grocery, frozen, chilled, and foodservice packaging systems. Food accounted for 36.19% of revenue in 2025, underscoring the material's widespread use across branded shelf-ready formats where visual presentation and transport performance matter simultaneously. The National Restaurant Association stated that enduring demand would continue to shape restaurant activity in 2026, which supports ongoing packaging trials and replenishment needs across branded foodservice chains. Clearwater Paper said in its first-quarter 2026 commentary that folding carton demand remained solid and that foodservice cup and plate grades showed strength, which points to sustained pull for food-contact paperboard applications. That demand is important for the North America cartonboard market because carry-out containers, cup stock, and laminated trays are tied to high-frequency consumption patterns that are difficult for alternatives to displace quickly. It also gives board producers a steadier path to multi-year supply agreements, since food and beverage pack formats often remain fixed for long production runs once brand owners complete their line qualification work.

Volatile Fiber, Energy, And Chemical Input Costs

Input-cost volatility remains the main earnings constraint across the North America cartonboard market because raw material and utility movements do not reset in line with contract pricing cycles. Smurfit Westrock reported a weather-related EBITDA impact of USD 65 million in the first quarter of 2026, largely in North America, while also pursuing a second wave of price increases to offset rising cost pressure. Graphic Packaging reported adjusted EBITDA of USD 232 million in the first quarter of 2026, down from USD 365 million a year earlier, and said input and other cost inflation accounted for USD 37 million of that decline. Cascades also pointed to continued upward pressure on input costs in its first-quarter 2026 results, indicating that recycled fiber networks are exposed to the same broad cost pressures even when mill structures differ. These pressures matter in the North America cartonboard market because they widen the advantage of vertically integrated producers with captive pulp and internal conversion assets. They also accelerate consolidation because smaller mills and independent operators have less room to absorb lagged pricing or sudden cost spikes in energy, recovered fiber, and specialty coatings.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce And Club Retail Secondary Packaging Demand

- PFAS-Free And PE-Free Barrier Board Innovation

- Competition From Flexible Packaging And Alternative Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid Packaging Board held 28.44% of the North America cartonboard market share in 2025, making it the largest product grade in the regional mix. Its position rests on highly consolidated aseptic and gable-top supply chains that support dairy, plant-based beverage, juice, and broth packaging, where filling-line integration tends to lock in long procurement cycles. In the North America cartonboard market, this gives LPB a stable demand base that is less exposed to sudden format changes than many discretionary consumer packaging uses. Folding Boxboard still serves premium consumer goods where caliper consistency, high whiteness, and strong print results remain central to brand presentation. Solid Unbleached Board and White-Lined Chipboard continue to serve cost-sensitive beverage multipacks and general retail packaging, although sustainability requirements have heightened scrutiny of grade selection and fiber credentials.

The North America cartonboard industry also shows a clear split between legacy scale grades and newer growth grades tied to food-contact conversion. The Food Service Board is projected to expand at a 7.14% CAGR through 2031, driven by plastic bans, demand for compostable formats, and the steady rise in off-premise consumption. Clearwater Paper said in its first-quarter 2026 commentary that extruded products, including cup and polycoated folding carton grades, were sold out, signaling tight supply in food-contact applications linked to reformulation and conversion activity. That condition matters because the move toward PFAS-free and PE-free solutions does not just change chemistry; it often changes caliper, conversion rates, and the value captured per ton. The North America cartonboard industry is therefore seeing product architecture shift toward grades that deliver barrier performance, regulatory compliance, and stronger yield economics in a single offer. The launch of lightweight mid-market SBS alternatives also points to a more selective buying pattern, in which converters are comparing usable output and print performance rather than relying solely on headline board prices.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Country

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- International Paper Company

- Georgia-Pacific LLC

- Packaging Corporation of America

- Clearwater Paper Corporation

- Sonoco Products Company

- Cascades Inc.

- Metsa Board Corporation

- Mayr-Melnhof Karton Aktiengesellschaft

- Billerud Aktiebolag (publ)

- Stora Enso Oyj

- Tetra Pak International S.A.

- SIG Group AG

- Huhtamaki Oyj

- CCL Industries Inc.

- Diamond Packaging

- American Carton Company

- Keystone Folding Box Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable Substitution from Plastic Packaging

- 4.2.2 Growth in Packaged Food and Beverage Demand

- 4.2.3 Premium Print and Shelf Appeal Demand in Beauty and Personal Care

- 4.2.4 E-commerce and Club Retail Secondary Packaging Demand

- 4.2.5 PFAS-Free and PE-Free Barrier Board Innovation

- 4.2.6 Pharmaceutical Serialization and Biologics Carton Complexity

- 4.3 Market Restraints

- 4.3.1 Volatile Fiber, Energy, and Chemical Input Costs

- 4.3.2 Competition from Flexible Packaging and Alternative Formats

- 4.3.3 State-Level PFAS Compliance Retrofits and Qualification Cycles

- 4.3.4 Canadian Cartonboard Capacity Tightness and Import Dependence

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Graphic Packaging Holding Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 International Paper Company

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Packaging Corporation of America

- 6.4.6 Clearwater Paper Corporation

- 6.4.7 Sonoco Products Company

- 6.4.8 Cascades Inc.

- 6.4.9 Metsa Board Corporation

- 6.4.10 Mayr-Melnhof Karton Aktiengesellschaft

- 6.4.11 Billerud Aktiebolag (publ)

- 6.4.12 Stora Enso Oyj

- 6.4.13 Tetra Pak International S.A.

- 6.4.14 SIG Group AG

- 6.4.15 Huhtamaki Oyj

- 6.4.16 CCL Industries Inc.

- 6.4.17 Diamond Packaging

- 6.4.18 American Carton Company

- 6.4.19 Keystone Folding Box Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

中東和非洲紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區紙板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印度紙板市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)德國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)法國紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)美國紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)