|

市場調查報告書

商品編碼

2065480

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Philippines Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

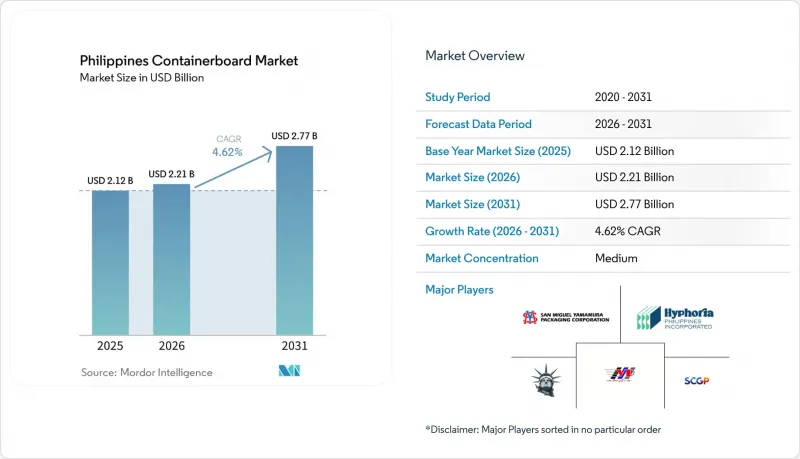

預計菲律賓箱板市場規模將從 2025 年的 21.2 億美元和 2026 年的 22.1 億美元成長到 2031 年的 27.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.62%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業等)進行細分。市場預測以價值(美元)表示。

菲律賓箱板紙市場趨勢與洞察

擴大包裝食品和飲料的生產

包裝食品和飲料的生產仍然是菲律賓箱板紙市場最強勁的需求支柱,持續帶動著都市區、鄉村和島際分銷管道的運輸需求。菲律賓統計局的報告顯示,2025年5月食品生產指數年增15.7%,2026年2月又成長3.4%,即便整體工業成長放緩。這表明食品製造業的表現優於許多其他製造業。美國農業部海外農業局也預測,2026年食品製造業將持續擴張,並指出政府為減少食品加工商的物流摩擦所做的努力是促成這一成長的因素之一。以社區主導的零售模式將進一步推高箱板紙需求,因為與以超級市場為中心的零售系統相比,更小的運輸單元和更頻繁的補貨週期將增加每單位產品的箱板消耗量。這一趨勢有助於解釋為什麼菲律賓瓦楞紙板市場在整體工業生產放緩的情況下,仍然依靠食品應用的需求來維持,以及為什麼與日常消費品相關的加工商的訂單基礎往往比主要依賴非必需消費品行業的公司更加穩定。

電子商務小包裹處理量增加

電子商務持續重塑菲律賓瓦楞紙板市場,包裝需求正轉向用於小包裹遞送和退貨處理的「一次性」瓦楞紙板。線上零售流程與傳統批發分銷截然不同。隨著訂單被拆分成更小的貨件,瓦楞紙板的規格也在不斷變化,處理量不斷增加,對輕質且品質穩定的瓦楞紙板的需求也日益成長。這帶動了對適用於小包裹遞送的再生測試襯紙和輕質瓦楞結構的需求,從而無需在所有應用場景下都使用出口級紙板。能夠處理小批量生產、多種尺寸規格以及為使用社交電商和市場平台的企業提供快速交付服務的本地加工商從中獲益最多。因此,隨著包裝需求從大型合約買家擴展到包括國內經銷商、履約服務商和宅配業者相關客戶在內的更廣泛的客戶群體,菲律賓箱板紙板市場的基本客群群正在擴大。

進口紙板對本地造紙公司帶來的價格壓力

進口瓦楞紙板仍然是菲律賓瓦楞紙板市場的主要限制因素。這是因為本地造紙業者被迫與規模更大、營運成本更低的區域性大規模生產體系供應商競爭。根據投資委員會(BOI)統計,菲律賓國內造紙業共有22家各自獨立的造紙企業,總合為每年165萬噸。雖然這對本地市場而言規模可觀,但與主要企業相比,仍較為分散。此外,貿易政策的支持力道也有所減弱。 2026年1月,海關委員會裁定“進口印尼瓦楞紙板並未造成嚴重損害”,隨後貿易和工業部駁回了對進口商實施最終保障措施關稅的申請,並責令其退還現金保證金。因此,進口瓦楞紙板再次為通用級瓦楞紙板市場的自由競爭創造了空間,尤其是在那些依賴老舊設備或面臨高昂營運成本的國內生產商中。這種壓力在菲律賓箱板紙市場尤其顯著,因為加工商可以利用進口產品作為與當地造紙商就價格進行談判的籌碼,從而擠壓國內利潤率,即使終端用戶需求依然強勁。

細分市場分析

到2025年,再生纖維將佔菲律賓瓦楞紙板市場佔有率的67.83%,這顯示菲律賓瓦楞紙板市場對舊新聞紙(OCC)和混合再生紙的依賴程度很高。根據菲律賓投資委員會(BOI)的PAPELS調查,菲律賓造紙業中再生纖維的含量高達95-100%,這種情況反映的是基礎設施的實際情況,而不僅僅是商業性偏好。事實上,由於菲律賓沒有商業規模的原生紙漿種植園,該國的瓦楞紙板產業以本地造紙廠使用再生紙為原料的模式為基礎。因此,再生瓦楞紙板的供應穩定,其需求不僅與終端用戶包裝材料偏好的變化密切相關,還與回收效率、市政回收系統以及國產再生紙的品質密切相關。

預計2026年至2031年間,原生纖維的複合年成長率將達到5.37%,使其成為規模最小但成長最快的材料類別。在不適合使用再生材料的領域,例如某些藥品包裝、高階消費品以及需要更清潔或經認證纖維等級的食品應用,將會出現新的機會。從成熟的原生牛皮紙供應商進口這些材料將使加工商能夠獲得這些材料。換句話說,即使沒有國內紙漿產業的整合,高附加價值需求也能成長。這正在菲律賓箱板紙產業形成「兩極化」的結構:再生材料在總噸位方面仍然佔據主導地位,而原生紙漿在更細分、更注重規格的領域中價值正在提升。 SCGP計劃在2026年投資130億泰銖(約3.54億美元)升級東南亞各地的紡織包裝設施,凸顯了將菲律賓納入其網路策略的區域公司越來越重視高附加價值定位的重要性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 擴大包裝食品和飲料的生產

- 電子商務小包裹量成長

- 電子產品和工業出口包裝的需求

- 改善家庭廢紙的收集和回收利用

- 為支持瓦楞紙板基紙的本地使用而採取的保障措施

- ISO 14001:2026 標準的採用正在推動可追溯紡織品包裝的發展。

- 市場限制因素

- 進口紙板價格對國內造紙企業施加的價格壓力

- 與東南亞國協相比,電力成本較高

- 主要都會區以外地區回收中心短缺

- 港口擁擠和貨櫃運費飆升

- 產業價值鏈分析

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- United Pulp and Paper Co., Inc.

- San Miguel Yamamura Packaging Corporation

- Valenzuela Packaging Container Corporation

- Hyphoria Philippines Inc.

- Papercon(Phils.)Inc.

- 3D Container and Packaging Phils. Corp.

- Total Packaging Solutions and Manufacturing, Inc.

- Mina Moto Packaging Corp.

- Corbox Corporation

- Liberty Corrugated Boxes Mfg. Corp.

- Davao Fibreboard Packaging Plant Inc.

- Duraboard Packaging Corp.

- Goldrich Industrial Packaging Corporation

- Malinta Corrugated Boxes Manufacturing Corporation

- Tenaga Pack Solution Inc.

- Cr8tive Boxes and Labels Corporation

- SBC Packaging OPC

- GagMax Packaging Solutions Inc.

- STC Paper and Plastic Packaging Solutions

- SuperPack Enterprises

第7章 市場機會與未來展望

According to Mordor Intelligence, the philippines containerboard market size is projected to expand from USD 2.12 billion in 2025 and USD 2.21 billion in 2026 to USD 2.77 billion by 2031, registering a CAGR of 4.62% between 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Containerboard Market Trends and Insights

Packaged Food And Beverage Output Expansion

Packaged food and beverage production remains the strongest demand anchor for the Philippines containerboard market because it creates recurring shipping needs across urban, provincial, and inter-island distribution channels. The Philippine Statistics Authority reported that the volume of production index for food products rose 15.7% year over year in May 2025, then increased 3.4% in February 2026 even as wider industrial activity stayed less even, which shows that food manufacturing has been more defensive than many other factory categories. The USDA Foreign Agricultural Service also projected continued expansion in 2026 and linked part of that support to government efforts aimed at reducing logistics friction for food processors. The barangay-led retail model adds another layer of box demand because goods often move in smaller shipment formats and more frequent replenishment cycles than in supermarket-heavy systems, which raises box conversion intensity per unit of product sold. That pattern helps explain why the Philippines containerboard market draws durable support from food applications even when headline industrial production softens and why converters tied to everyday consumer staples tend to operate with a steadier order base than firms exposed mainly to discretionary categories.

E-Commerce Parcel Volume Growth

E-commerce continues to reshape the Philippines containerboard market by shifting more packaging demand toward single-trip corrugated formats used in parcel delivery and return handling. Online retail flows differ from traditional wholesale movement because orders are broken into smaller shipments, which changes box specifications, increases the number of units handled, and creates repeat demand for light but consistent corrugated grades. This has supported demand for recycled testliners and lighter fluting structures that suit parcel shipping without requiring export-grade board in every application. The benefit is strongest for local converters that can handle short production runs, varied dimensions, and quick turnaround times for merchants serving social commerce and marketplace channels. The result is a broader customer base for the Philippines containerboard market because packaging demand is spreading beyond large contract buyers and into a wider pool of domestic sellers, fulfillment operators, and courier-linked accounts.

Imported Board Price Pressure On Local Mills

Imported containerboard remains a serious constraint on the Philippines containerboard market because local mills compete against suppliers from larger regional production systems with better economies of scale and lower operating costs. The Board of Investments noted that the domestic paper sector includes 22 non-integrated mills with combined capacity of 1.65 million metric tons per year, which is sizable for the local market but still fragmented compared with regional heavyweights. Trade policy support also weakened after the Tariff Commission's January 2026 finding that Indonesian corrugating medium imports did not cause serious injury, and the Department of Trade and Industry later rejected the petition for definitive safeguard duties and ordered cash bond refunds to importers. That outcome reopened room for foreign board to compete more freely in commodity grades, especially where domestic producers rely on older machines or face higher operating costs. The pressure is especially relevant in the Philippines containerboard market because converters can use imports as a negotiating check on local mill pricing, which compresses domestic margins even when end-user demand remains healthy.

Other drivers and restraints analyzed in the detailed report include:

- Electronics And Industrial Export Packaging Demand

- Better Domestic Wastepaper Recovery And Reuse

- High Electricity Costs Versus ASEAN Peers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 67.83% of the market in 2025, which shows how deeply the Philippines containerboard market depends on OCC and mixed wastepaper as its operating base. The Board of Investments PAPELS study stated that recycled fiber content in Philippine paper production runs at 95-100%, which means this position reflects infrastructure reality more than a simple commercial preference. In practice, the Philippines containerboard industry is built around a feedstock model where local mills work with recovered paper because commercial-scale virgin pulp plantations are not available in the country. That gives recycled board a stable volume role and keeps its demand closely linked to collection efficiency, municipal recovery systems, and the quality of domestically sourced wastepaper rather than only to shifts in end-user packaging choice.

Virgin fibers are projected to grow at a 5.37% CAGR from 2026 to 2031, which makes them the fastest-moving material niche even from a small base. The opportunity comes from applications where recycled content is less favored, including select pharmaceutical packaging, premium consumer goods, and food uses that require cleaner or certified fiber grades. Imports from established virgin kraft suppliers give converters access to these substrates, which means value-added demand can grow even without domestic pulp integration. This creates a two-speed structure in the Philippines containerboard industry, where recycled inputs remain dominant in tonnage while virgin-fiber applications capture incremental value in narrower, specification-driven segments. SCGP's 2026 investment plan of THB 13,000 million, or USD 354 million, for fiber packaging upgrades across Southeast Asia reinforces that higher-value positioning is becoming more important for regional players that include the Philippines in their network strategy.

List of Companies Covered in this Report:

- United Pulp and Paper Co., Inc.

- San Miguel Yamamura Packaging Corporation

- Valenzuela Packaging Container Corporation

- Hyphoria Philippines Inc.

- Papercon (Phils.) Inc.

- 3D Container and Packaging Phils. Corp.

- Total Packaging Solutions and Manufacturing, Inc.

- Mina Moto Packaging Corp.

- Corbox Corporation

- Liberty Corrugated Boxes Mfg. Corp.

- Davao Fibreboard Packaging Plant Inc.

- Duraboard Packaging Corp.

- Goldrich Industrial Packaging Corporation

- Malinta Corrugated Boxes Manufacturing Corporation

- Tenaga Pack Solution Inc.

- Cr8tive Boxes and Labels Corporation

- SBC Packaging OPC

- GagMax Packaging Solutions Inc.

- STC Paper and Plastic Packaging Solutions

- SuperPack Enterprises

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Packaged Food and Beverage Output Expansion

- 4.3.2 E-Commerce Parcel Volume Growth

- 4.3.3 Electronics and Industrial Export Packaging Demand

- 4.3.4 Better Domestic Wastepaper Recovery and Reuse

- 4.3.5 Corrugating Medium Safeguard Action Supporting Local Utilization

- 4.3.6 ISO 14001:2026 Adoption Favoring Traceable Fiber Packaging

- 4.4 Market Restraints

- 4.4.1 Imported Board Price Pressure on Local Mills

- 4.4.2 High Electricity Costs Versus ASEAN Peers

- 4.4.3 Recycling-Center Scarcity Outside Major Urban Hubs

- 4.4.4 Port Congestion and Elevated Container Freight Costs

- 4.5 Industry Value Chain Analysis

- 4.6 Supply Chain Analysis

- 4.7 Regulatory Landscape

- 4.8 Technological Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 United Pulp and Paper Co., Inc.

- 6.4.2 San Miguel Yamamura Packaging Corporation

- 6.4.3 Valenzuela Packaging Container Corporation

- 6.4.4 Hyphoria Philippines Inc.

- 6.4.5 Papercon (Phils.) Inc.

- 6.4.6 3D Container and Packaging Phils. Corp.

- 6.4.7 Total Packaging Solutions and Manufacturing, Inc.

- 6.4.8 Mina Moto Packaging Corp.

- 6.4.9 Corbox Corporation

- 6.4.10 Liberty Corrugated Boxes Mfg. Corp.

- 6.4.11 Davao Fibreboard Packaging Plant Inc.

- 6.4.12 Duraboard Packaging Corp.

- 6.4.13 Goldrich Industrial Packaging Corporation

- 6.4.14 Malinta Corrugated Boxes Manufacturing Corporation

- 6.4.15 Tenaga Pack Solution Inc.

- 6.4.16 Cr8tive Boxes and Labels Corporation

- 6.4.17 SBC Packaging OPC

- 6.4.18 GagMax Packaging Solutions Inc.

- 6.4.19 STC Paper and Plastic Packaging Solutions

- 6.4.20 SuperPack Enterprises

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Future Outlook

越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)