|

市場調查報告書

商品編碼

2064486

中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

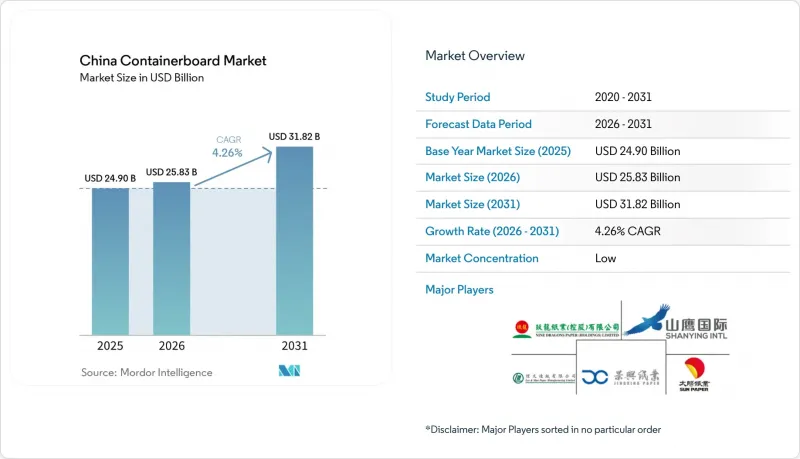

根據 Mordor Intelligence 預測,中國瓦楞紙板原紙市場規模預計到 2025 年將達到 249 億美元,到 2026 年將達到 258.3 億美元,到 2031 年將達到 318.2 億美元,2026 年至 2031 年的複合年成長率為 4.26%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業及其他)進行細分。市場預測以美元計價。

中國瓦楞紙板原紙市場趨勢及洞察。

電子商務和小包裹遞送業務的擴張

隨著小包裹遞送在中國都市區居民的日常生活中日益普及,電子商務仍然是中國瓦楞紙板市場需求的最大驅動力。 2024年,中國宅配網路處理了1,750億件小包裹,連續第11年蟬聯全球最大快遞網路。修訂後的《宅配暫行條例》於2025年6月1日生效,將服務品質和包裝耐用性納入更完善的法規結構。該政策鼓勵生產更堅固耐用的瓦楞紙板,進一步鞏固了中國箱板紙市場對紙箱的需求基礎。預計到2026年,宅配業對瓦楞紙板的需求將超過900萬噸,顯示儘管紙張生產商持續面臨價格壓力,但物流需求仍保持成長。此外,需求基礎正在向地方縣域擴展,使中國瓦楞紙板市場不再局限於傳統的沿海製造地。

食品飲料包裝需求集中

食品飲料產業仍是中國瓦楞紙板原紙市場最大的需求來源,預計到2025年將佔終端用戶佔有率的42.41%,並滿足最廣泛的包裝需求。此類別的需求不再僅僅受出貨量所驅動。生鮮食品、已調理食品、乳製品和飲料的運輸需要比標準低規格運輸包裝性能更穩定的紙箱。低溫運輸物流的普及提高了對防潮性、承載強度和表面品質的需求,從而提升了中國瓦楞紙板原紙市場所用紙板的價值。中國的食品安全標準GB 4806.8限制了在某些直接接觸食品的應用中使用再生纖維,這使得部分高階食品包裝的需求轉向原生紙漿和塗佈紙。這種轉變使得擁有認證材料和規範產品線的造紙企業在與主要食品品牌的合作中,在中國瓦楞紙板原紙市場佔據了更有利的地位。這也意味著產品組合的改進不僅是由出貨量增加所驅動的,也是由監管合規性和性能需求所驅動的。

持續的供應過剩和價格競爭

由於供應成長持續超過實際需求吸收,持續的供應過剩仍是中國瓦楞紙板市場的主要結構性限制因素。儘管2025年產能預計達3,819萬噸,但實際產量僅2,820萬噸,導致產業整體運轉率僅70%-80%。這種供需失衡使得產業平均淨利率率僅為2.3%,即使在出貨量穩定的時期,許多生產者也面臨困境。 2025年約有140條中小生產線關閉或改造,但這仍不足以解決中國箱板紙市場供應過剩的規模。北京當局關於「抑制創新」的表態表明其政策意圖是遏制破壞性的價格競爭,但緩解中國瓦楞紙板市場的價格壓力仍然取決於多個投資週期內新增產能增速的放緩。在此之前,中國瓦楞紙板市場可能會持續保持強勁的銷售量,但利潤率仍然較低。

細分市場分析

截至2025年,再生纖維在中國瓦楞紙板原紙市場佔有率中佔比高達69.14%,顯示此原料基礎仍佔主導地位。這一地位源自於中國完善的再生紙(OCC)回收體係以及圍繞再生纖維加工而建立的長期生產基礎設施。Delta和珠三角Delta的大型造紙廠在再生紙流通方面仍然享有規模經濟、接近性加工商以及運輸便利的優勢,這鞏固了該地區在中國瓦楞紙板原紙市場的成本優勢。此外,再生紙非常適合大量生產的測試襯紙和瓦楞紙的需求,在這些領域,穩定的產量比高價更為重要。正因如此,儘管通用級瓦楞紙板的利潤率持續承壓,再生纖維仍是中國瓦楞紙板原紙產業的基石。

預計到2031年,原生紙漿將以4.68%的複合年成長率成長,成為中國瓦楞紙板原紙市場成長最快的材料類別。食品接觸法規、出口包裝要求以及低溫運輸配送規範的日益嚴格,都在提升原生紙漿在中國瓦楞紙板原紙市場整體地位。中國GB 4806.8標準是推動這項變革的主要因素,該標準限制了在某些關鍵食品接觸應用中使用再生紙漿。九龍紙業也計劃在重慶、天津、北海和東莞新增250萬噸化學紙漿產能,顯示主要企業正在建構上游體係以支持這種高附加價值材料組合。因此,中國箱板紙產業正呈現兩極化的趨勢,一部分企業專注於規模化生產的再生紙漿,而另一部分企業則轉向價格更高的原生紙漿牛皮紙襯紙和塗佈紙產品。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 電子商務和小包裹遞送業務的擴張

- 食品和飲料的包裝強度

- 塑膠替代品和環保包裝法規

- 高性能貨櫃板的優質化

- 生產商直接出貨需要更堅固的紙板。

- 內陸地區小批量出貨量的增加將導致造紙廠位置結構的重新平衡。

- 市場限制因素

- 光纖和能源成本波動

- 持續的供應過剩和價格競爭

- 限制乾紙漿進口將擾亂低成本纖維市場。

- 減少包裝會導致每件商品使用的纖維量減少。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 飲食

- 消費品

- 工業的

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nine Dragons Paper(Holdings)Limited

- Lee & Man Paper Manufacturing Limited

- Shanying International Holdings Co., Ltd.

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- Dongguan Jianhui Paper Co., Ltd.

- Shandong Chenming Paper Holdings Limited

- Shandong Bohui Paper Industry Co., Ltd.

- Longchen Paper & Packaging Co., Ltd.

- Liansheng Paper Industry(Longhai)Co., Ltd.

- Yuen Foong Yu Paper Manufacturing Co., Ltd.

- Jiangsu Rongsheng Pulp & Paper Co., Ltd.

- Guangzhou Paper Group Co., Ltd.

- Shandong Huatai Paper Industry Co., Ltd.

- Anhui Shanying Paper Industry Co., Ltd.

- Guangxi Jingui Pulp & Paper Co., Ltd.

- Zhejiang Yongtai Paper Co., Ltd.

- Zhejiang Zhengda Paper Co., Ltd.

- Hengfeng Paper Co., Ltd.

- Jiangsu Longchen Greentech Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china containerboard market size is projected to be USD 24.9 billion in 2025, USD 25.83 billion in 2026, and reach USD 31.82 billion by 2031, growing at a CAGR of 4.26% from 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Containerboard Market Trends and Insights

E-Commerce And Parcel Delivery Expansion

E-commerce remains the single strongest driver of demand for the China containerboard market because parcel movement is now embedded in daily consumption across urban and rural China. China's express network handled 175 billion parcels in 2024, making it the world's first for the 11th straight year. The amended Provisional Regulations on Express Delivery took effect on June 1, 2025, and pushed service quality and packaging durability into a firmer regulatory framework. That policy direction favors sturdier corrugated formats and supports a more reliable base of box demand for the China containerboard market. Corrugated demand from the express sector is on track to exceed 9 million tons in 2026, indicating that logistics demand is still rising even as mill pricing remains under pressure. The demand base is also spreading into lower-tier counties, widening the reach of the China containerboard market beyond traditional coastal manufacturing centers.

Food And Beverage Packaging Intensity

Food and beverage remains the largest demand center in the China containerboard market, accounting for 42.41% of end-user share in 2025 and still serving the broadest mix of packaging needs. The category is no longer driven only by shipment volume, because fresh produce, prepared meals, dairy, and beverage distribution all require more stable box performance than standard low-specification transport packaging. Cold-chain distribution is driving higher moisture resistance, stacking strength, and surface quality, raising the value profile of the board used in the Chinese containerboard market. China's GB 4806.8 food safety framework limits the use of recycled fiber in certain primary food-contact applications, redirecting part of premium food packaging demand toward virgin-fiber and coated grades. That shift is helping mills with certified material and compliance-ready product lines win stronger positions with major food brands in the China containerboard market. It also means that product mix improvement is being driven by compliance and performance needs, not just by higher shipment counts.

Persistent Overcapacity And Price Competition

Persistent overcapacity remains the main structural restraint on the China containerboard market because supply additions have continued to outpace real demand absorption. Capacity reached 38.19 million tons in 2025, while output stood at 28.2 million tons, which kept utilization in the 70-80% range across the sector. That mismatch left average industry net margins at 2.3% and kept many producers under pressure even when shipment volumes were stable. Around 140 small and medium production lines were shut or converted in 2025, but that still represented only a partial response to the scale of excess supply in the China containerboard market. Beijing's anti-innovation language points to a policy desire to curb destructive price competition, but pricing relief in the China containerboard market will still depend on slower new capacity additions over multiple investment cycles. Until that happens, the China containerboard market is likely to remain volume-supported but margin-constrained.

Other drivers and restraints analyzed in the detailed report include:

- Plastic-Substitution And Green Packaging Regulation

- Premiumization Toward Higher-Performance Containerboard

- Fiber And Energy Cost Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 69.14% of the China containerboard market share in 2025, which kept this material base clearly in the lead. That position came from China's deep OCC collection system and the long-established production infrastructure built around recycled fiber processing. Large mills in the Yangtze River Delta and Pearl River Delta still benefit from scale, converter proximity, and lower transport complexity for recovered paper flows, which supports the cost logic of this part of the China containerboard market. The recycled segment also fits the needs of high-volume testliner and fluting output, where consistent throughput matters more than premium pricing. This explains why recycled fiber remains the backbone of the China containerboard industry, even as margins in commodity grades stay under pressure.

Virgin fibers are projected to grow at a 4.68% CAGR through 2031, making them the fastest-growing material category in the China containerboard market. Food-contact rules, export-grade packaging requirements, and stronger specifications in cold-chain distribution are all lifting the role of virgin-based grades across the China containerboard market. China's GB 4806.8 framework supports that shift because it limits the use of recycled fiber in certain primary food-contact applications. Nine Dragons Paper is also targeting an additional 2.5 million tons of chemical pulp capacity across Chongqing, Tianjin, Beihai, and Dongguan, which shows how major players are building upstream support for this higher-value material mix. The result is a more divided China containerboard industry, where one tier focuses on scale-driven recycled grades and another moves toward virgin-fiber kraftliners and coated products with better pricing power.

List of Companies Covered in this Report:

- Nine Dragons Paper (Holdings) Limited

- Lee & Man Paper Manufacturing Limited

- Shanying International Holdings Co., Ltd.

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- Dongguan Jianhui Paper Co., Ltd.

- Shandong Chenming Paper Holdings Limited

- Shandong Bohui Paper Industry Co., Ltd.

- Longchen Paper & Packaging Co., Ltd.

- Liansheng Paper Industry (Longhai) Co., Ltd.

- Yuen Foong Yu Paper Manufacturing Co., Ltd.

- Jiangsu Rongsheng Pulp & Paper Co., Ltd.

- Guangzhou Paper Group Co., Ltd.

- Shandong Huatai Paper Industry Co., Ltd.

- Anhui Shanying Paper Industry Co., Ltd.

- Guangxi Jingui Pulp & Paper Co., Ltd.

- Zhejiang Yongtai Paper Co., Ltd.

- Zhejiang Zhengda Paper Co., Ltd.

- Hengfeng Paper Co., Ltd.

- Jiangsu Longchen Greentech Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 E-commerce and Parcel Delivery Expansion

- 4.3.2 Food and Beverage Packaging Intensity

- 4.3.3 Plastic-Substitution and Green Packaging Regulation

- 4.3.4 Premiumization Toward Higher-Performance Containerboard

- 4.3.5 Direct-From-Origin Shipping Needs Stronger Board

- 4.3.6 Inland Parcel Growth Rebalances Mill Footprints

- 4.4 Market Restraints

- 4.4.1 Fiber and Energy Cost Volatility

- 4.4.2 Persistent Overcapacity and Price Competition

- 4.4.3 Dry-Pulp Import Scrutiny Disrupts Low-Cost Fiber

- 4.4.4 Packaging Reduction Lowers Fiber Intensity per Parcel

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nine Dragons Paper (Holdings) Limited

- 6.4.2 Lee & Man Paper Manufacturing Limited

- 6.4.3 Shanying International Holdings Co., Ltd.

- 6.4.4 Shandong Sun Paper Industry Joint Stock Co., Ltd.

- 6.4.5 Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- 6.4.6 Dongguan Jianhui Paper Co., Ltd.

- 6.4.7 Shandong Chenming Paper Holdings Limited

- 6.4.8 Shandong Bohui Paper Industry Co., Ltd.

- 6.4.9 Longchen Paper & Packaging Co., Ltd.

- 6.4.10 Liansheng Paper Industry (Longhai) Co., Ltd.

- 6.4.11 Yuen Foong Yu Paper Manufacturing Co., Ltd.

- 6.4.12 Jiangsu Rongsheng Pulp & Paper Co., Ltd.

- 6.4.13 Guangzhou Paper Group Co., Ltd.

- 6.4.14 Shandong Huatai Paper Industry Co., Ltd.

- 6.4.15 Anhui Shanying Paper Industry Co., Ltd.

- 6.4.16 Guangxi Jingui Pulp & Paper Co., Ltd.

- 6.4.17 Zhejiang Yongtai Paper Co., Ltd.

- 6.4.18 Zhejiang Zhengda Paper Co., Ltd.

- 6.4.19 Hengfeng Paper Co., Ltd.

- 6.4.20 Jiangsu Longchen Greentech Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)