|

市場調查報告書

商品編碼

2063963

西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Spain Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

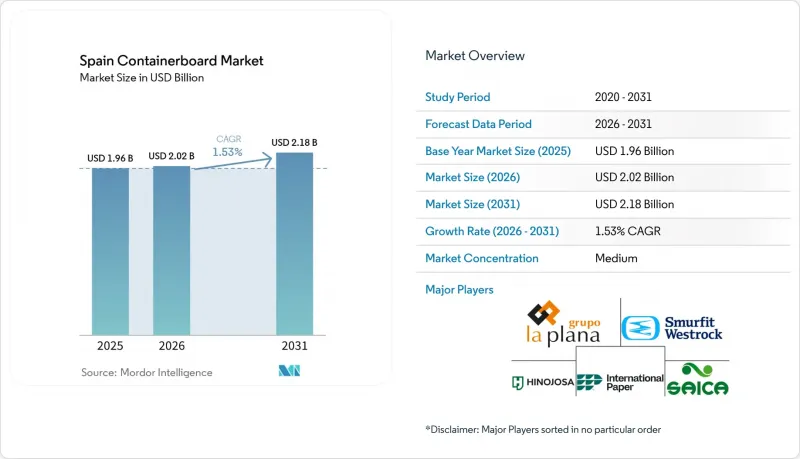

據 Mordor Intelligence 稱,2025 年西班牙瓦楞紙板市場價值 19.6 億美元,預計到 2031 年將從 2026 年的 20.2 億美元成長到 21.8 億美元,預測期(2026-2031 年)的複合年成長率為 1.53%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業及其他)進行細分。市場預測以美元計價。

西班牙箱板紙市場趨勢與洞察

食品出口和生鮮食品對瓦楞紙板的需求

由於西班牙擁有龐大的農產品和食品出口基地,其瓦楞紙板市場與生鮮食品的貿易流量密切相關。預計到2025年,西班牙新鮮蔬果出口將達186.66億歐元(202億美元)。儘管出貨量下降了4%,但仍取得了這項成就,這表明高附加價值產品正在推高單位運輸包裝的價值密度。到2025年,安達盧西亞將佔西班牙果蔬出口總量的33%,瓦倫西亞將佔28%,這兩個地區將成為瓦楞紙板需求的中心訂購樞紐。隨著出口商從低附加價值農產品轉向莓果、核果和特色蔬菜,包裝規格日益嚴格,瓦楞紙板的平均等級也不斷提高。 2024年,西班牙對華農產品和食品出口達77億美元。這導致物流運輸距離延長,並提高了出口鏈中瓦楞紙板產品的抗壓性和承載能力要求。歐盟與南方共同市場於2024年12月簽署的協議預計將使西班牙的貿易額成長0.6%至1.4%,從而進一步刺激對適用於出口和多模態的瓦楞紙板的需求。因此,西班牙的箱板紙市場不僅會受到出口量的影響,還會受到西班牙出口商品價值組成變化的影響。

電子商務小包裹的成長及合適的尺寸。

小包裹處理業務正推動西班牙箱板市場對加工紙板的需求穩定成長。 2024年,西班牙電子商務包裹處理量達到創紀錄的13.03億件,較2019年的5.38億件成長240%。同時,預計2026年,物流包裹處理量將達到每日330萬件。西班牙國際出口信貸機構(ICEX)預測,2025年電子商務成長率將達到5.4%,這將支撐小包裹處理量在此期間的持續成長。隨著物流網路轉向尺寸和形狀更適合小包裹櫃和自動化傳送帶的包裝,這種變化不僅體現在包裝箱的數量上,也體現在包裝箱形狀的精確度上。西班牙物流供應商正在快速採用路線最佳化和倉庫自動化技術,因此更傾向於選擇能夠支援自動化履約和高效利用空間的包裝材料。這種需求也蔓延至食品雜貨和快餐管道,在這些管道中,瓦楞紙二級包裝仍然是人口密集的都市區配送網路中的標準運輸方式。這一趨勢意味著西班牙箱板紙市場不僅從商品數量上獲得更多支持,而且從增值加工方法上也獲得更多支持。

再生纖維和能源成本波動

西班牙瓦楞紙板市場的主要風險並非終端需求的急劇下降,而是成本轉嫁。 2025年,再生纖維佔總需求的60.18%,這意味著市場很大一部分仍容易受到再生紙(OCC)價格和能源成本波動的影響。歐洲OCC基準價格從2025年秋季初的每噸120歐元(135.4美元)跌至年底的每噸105歐元(118.5美元)。這反映了下游需求疲軟、中國停止進口乾法再生紙漿以及西歐庫存過剩。儘管價格下跌,但風險並未消除,因為纖維價格的波動仍然會擾亂非一體化製造商的利潤率規劃和庫存策略。對能源的依賴是另一個令人擔憂的問題。在歐盟,再生瓦楞紙板生產過程中消耗的能源有68%來自天然氣,天然氣價格每兆瓦時上漲10歐元(11.20美元),就可能使再生包裝紙的可變生產成本每噸增加高達20歐元(22.50美元)。在西班牙瓦楞紙板原紙市場,這種壓力主要體現在那些沒有自建發電設施、生質能支持或長期能源對沖的再生紙級造紙廠。

細分市場分析

2025年,再生纖維佔西班牙瓦楞紙板原紙市場的60.18%,在原料組成中佔據主導地位。這一佔有率反映了西班牙成熟的造紙廠基礎、較高的瓦楞紙板回收率,以及在許多標準應用中,採購再生紙比進口原生牛皮紙更具成本效益。賽卡公司位於埃爾布爾戈德埃布羅的PM9型紙機每年使用100%再生纖維生產超過40萬噸輕質再生瓦楞紙板,該紙機已於2026年3月完成計劃升級,以提高效率和永續性。儘管西班牙90%的瓦楞紙板回收率保障了穩定的原料供應,但當瓦楞紙板價格在每噸105至120歐元(118至135美元)的範圍內波動時(如2025年所示),沒有自有回收網路的造紙廠仍然面臨風險。

預計到2031年,原生紙漿將以1.79%的複合年成長率成長,雖然初期規模較小,但有望成為快速成長的原料基礎。這一成長反映了高階生鮮食品出口和電子商務應用領域需求的不斷擴大,在這些領域,高性能纖維原料(如耐破強度和抗壓性)仍然備受青睞。從細分市場來看,原生纖維是西班牙瓦楞紙板市場中一個快速成長的細分市場,在該市場中,性能指標比原料成本本身更為重要。 Ense公司計劃在阿斯蓬特斯建設一座漂白再生纖維生物工廠,已獲得政府2470萬歐元(2780萬美元)的臨時資金,並於2025年8月獲得了綜合環境認證,這表明生產商正努力縮小再生纖維和原生級產品之間的性能差距。因此,儘管再生纖維仍然主導西班牙瓦楞紙板行業,但由於對更堅韌、更專業的瓦楞紙板的商業性需求不斷成長,原生紙漿解決方案正逐漸獲得成長優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品出口和生鮮食品對瓦楞紙板的需求

- 電子商務小包裹及透過最佳化實現成長

- 有關可回收性的法規對紡織品包裝是有利的。

- 健全的再生纖維和回收基礎設施

- 伊比利半島物流對自動化包裝的需求

- 由農業廢棄物衍生的奈米纖維素製成的高強度再生襯紙板

- 市場限制因素

- 再生纖維和能源成本的波動

- 強制使用可重複使用的運輸包裝材料

- 生鮮食品產業向可重複使用塑膠箱過渡

- 西班牙一家再生瓦楞紙板生產廠面臨停產風險。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- SAICA Pack, SL

- Smurfit Westrock plc

- International Paper Company

- Hinojosa Packaging Group, SL

- Cartonajes de la Plana, SLU

- Cartonajes Santorroman, SA

- Ondupack, SAU

- Papresa, SA

- Klingele Paper & Packaging SE & Co. KG

- Cartonajes Europa, SA

- Cartondis, SA

- Vegabaja Packaging, SL

- Cartonajes International, SA

- Macopa, SA

- INECO, SA

- Avance Carton Ondulado, SL

- Cartonajes Valles Gasset, SA

- Cartonajes Arregui, SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain containerboard market size was valued at USD 1.96 billion in 2025 and estimated to grow from USD 2.02 billion in 2026 to reach USD 2.18 billion by 2031, at a CAGR of 1.53% during the forecast period (2026-2031).

This report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Containerboard Market Trends and Insights

Food Export And Fresh-Produce Corrugated Demand

Spain's agrifood export base keeps the Spain containerboard market closely linked to fresh-produce trade flows. Fresh fruit and vegetable exports generated EUR 18.666 billion in 2025 (USD 20.2 billion), even as shipped volume declined by 4%, indicating that higher-value categories lifted packaging value intensity per unit moved. Andalusia accounted for 33% of national fruit and vegetable export volume in 2025, while the Valencian Community contributed 28%, making both regions central ordering points for corrugated demand. As exporters shift from lower-value produce to berries, stone fruits, and specialty vegetables, packaging specifications become tighter and average board grades rise. Spain's agrifood exports to China reached USD 7.7 billion in 2024, which lengthens logistics distances and raises crush resistance and stacking requirements for corrugated formats serving export chains. The EU-Mercosur agreement, signed in December 2024, is expected to boost Spain's trade by 0.6%-1.4%, supporting further demand for export-ready boards suited to multi-modal handling. This keeps the Spain containerboard market tied not only to export volumes, but also to the changing value mix of what Spain ships abroad.

E-Commerce Parcel And Right-Sizing Growth

Parcel activity is providing the Spain containerboard market with a steady source of incremental demand for converted board. Spain handled a record 1.303 billion e-commerce shipments in 2024, up 240% from 538 million in 2019, while logistics package volumes are running at 3.3 million per day in 2026. ICEX projected 5.4% e-commerce growth for 2025, which supports continuing parcel throughput into the current period. The material change is not only in box count but also in format precision, as logistics networks move toward right-sized, variable-geometry packaging that better fits parcel lockers and automated handling lines. Spanish logistics operators have adopted route optimization and warehouse automation at high rates, which favors packaging inputs that can support automated fulfillment and efficient cube utilization. Demand is also broadening into grocery and quick-commerce channels, where corrugated secondary packaging remains the standard transport choice across dense urban distribution networks. That pattern gives the Spain containerboard market more support from value-added converted formats than from simple commodity volume alone.

Recovered Fiber And Energy Cost Volatility

The main risk to the Spain containerboard market remains cost transmission rather than a collapse in end demand. Recycled fibers accounted for 60.18% of demand in 2025, indicating that a large part of the market remains exposed to swings in OCC prices and energy costs. European OCC benchmark prices moved down from EUR 120 (USD 135.4) per tonne in early autumn 2025 to EUR 105 (USD 118.5) per tonne by year-end, reflecting weak downstream demand, China's suspension of dry-ground recycled pulp imports, and excess inventories in Western Europe. That price decline did not eliminate risk, as unstable fiber pricing continues to disrupt margin planning and inventory strategy for non-integrated producers. Energy exposure adds another layer, with 68% of energy consumed in EU recycled containerboard production derived from natural gas, and a EUR 10 (USD 11.2) per MWh rise in gas prices lifting variable production costs by up to EUR 20 (USD 22.5) per tonne for recycled packaging paper. For the Spain containerboard market, this pressure is strongest at recycled-grade mills that lack captive power, biomass support, or long-term energy hedging.

Other drivers and restraints analyzed in the detailed report include:

- Recyclability Rules Favor Fiber Packaging

- Strong Recovered-Fiber And Recycling Infrastructure

- Reusable Transport Packaging Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 60.18% of the Spain containerboard market in 2025, giving this segment the leading position across the feedstock mix. That share reflects Spain's established paper mill base, high corrugated recovery rates, and the cost advantage of recovered-paper sourcing over imported virgin kraft in many standard applications. Saica's PM9 at El Burgo de Ebro produces more than 400,000 metric tons per year of lightweight recycled containerboard from 100% recovered fiber, and the machine completed a planned upgrade in March 2026 to improve efficiency and sustainability. Spain's 90% corrugated recovery rate supports stable feedstock access, although mills without captive collection remain exposed when OCC prices fluctuate within the EUR 105-120 (USD 118-135) per tonne range seen in 2025.

Virgin fibers are forecast to grow at a 1.79% CAGR through 2031, making them the faster-growing feedstock base even from a smaller starting point. That growth reflects stronger demand from premium fresh-produce exports and e-commerce applications, where burst strength and crush resistance still favor higher-performance fiber inputs. In segment terms, virgin fibers are the faster-moving part of the Spanish containerboard market size, where performance specifications matter more than raw material cost alone. Ence's planned bleached-recycled-fiber bioplant at As Pontes, backed by EUR 24.7 million (USD 27.8 million) in provisional government funding and supported by an integrated environmental authorization issued in August 2025, shows how producers are trying to narrow the performance gap between recycled and virgin-style grades. The Spain containerboard industry therefore remains led by recycled fiber, but the commercial pull toward stronger and more specialized grades is giving virgin-linked solutions a modest growth edge.

List of Companies Covered in this Report:

- SAICA Pack, S.L.

- Smurfit Westrock plc

- International Paper Company

- Hinojosa Packaging Group, S.L.

- Cartonajes de la Plana, S.L.U.

- Cartonajes Santorroman, S.A.

- Ondupack, S.A.U.

- Papresa, S.A.

- Klingele Paper & Packaging SE & Co. KG

- Cartonajes Europa, S.A.

- Cartondis, S.A.

- Vegabaja Packaging, S.L.

- Cartonajes International, S.A.

- Macopa, S.A.

- INECO, S.A.

- Avance Carton Ondulado, S.L.

- Cartonajes Valles Gasset, S.A.

- Cartonajes Arregui, S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Food Export and Fresh-Produce Corrugated Demand

- 4.2.2 E-Commerce Parcel and Right-Sizing Growth

- 4.2.3 Recyclability Rules Favor Fiber Packaging

- 4.2.4 Strong Recovered-Fiber and Recycling Infrastructure

- 4.2.5 Automation-Ready Packaging Demand in Iberian Logistics

- 4.2.6 Agricultural-Residue Nanocellulose for Stronger Recycled Linerboard

- 4.3 Market Restraints

- 4.3.1 Recovered Fiber and Energy Cost Volatility

- 4.3.2 Reusable Transport Packaging Mandates

- 4.3.3 Fresh-Produce Shift Toward Reusable Plastic Crates

- 4.3.4 Mill-Outage Risk in Spain's Recycled Containerboard Base

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAICA Pack, S.L.

- 6.4.2 Smurfit Westrock plc

- 6.4.3 International Paper Company

- 6.4.4 Hinojosa Packaging Group, S.L.

- 6.4.5 Cartonajes de la Plana, S.L.U.

- 6.4.6 Cartonajes Santorroman, S.A.

- 6.4.7 Ondupack, S.A.U.

- 6.4.8 Papresa, S.A.

- 6.4.9 Klingele Paper & Packaging SE & Co. KG

- 6.4.10 Cartonajes Europa, S.A.

- 6.4.11 Cartondis, S.A.

- 6.4.12 Vegabaja Packaging, S.L.

- 6.4.13 Cartonajes International, S.A.

- 6.4.14 Macopa, S.A.

- 6.4.15 INECO, S.A.

- 6.4.16 Avance Carton Ondulado, S.L.

- 6.4.17 Cartonajes Valles Gasset, S.A.

- 6.4.18 Cartonajes Arregui, S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)