|

市場調查報告書

商品編碼

2064384

法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)France Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

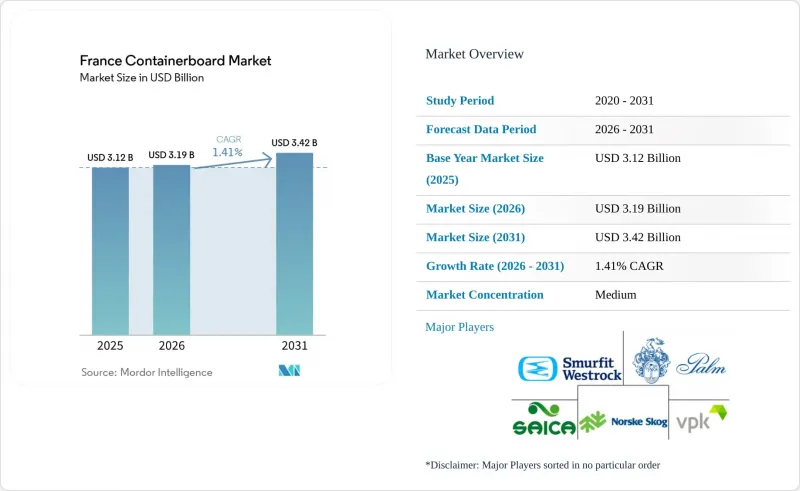

根據 Mordor Intelligence 預測,法國瓦楞紙板市場規模將從 2025 年的 31.2 億美元和 2026 年的 31.9 億美元成長到 2031 年的 34.2 億美元,2026 年至 2031 年的複合年成長率為 1.41%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業等)進行細分。市場預測以美元計價。

法國箱板紙市場趨勢與洞察

基於AGEC和PPWR的塑膠纖維替代品

法國的AGEC框架和歐盟於2025年通過的《包裝和包裝廢棄物法規》是法國箱板紙市場中期最明顯的推動因素。 2022-748號法令規定,自2025年1月1日起,超過指定閾值的生產商和進口商必須揭露包裝的可回收性特徵和再生材料含量,從而提高包裝成分對買家和監管機構的透明度。類似的政策方向正在提升可再生纖維級紙板在二次包裝和運輸包裝中的商業性吸引力,尤其是在塑膠包裝合規成本過高的領域。此外,食品、化妝品和其他對外觀要求較高的應用領域對高價值紙板(如白面測試襯紙和塗佈箱板紙)的需求也在不斷成長。因此,儘管法國箱板紙市場的短期需求仍然疲軟,但監管的支持將持續發揮作用。

最佳化電商和商店展示的包裝。

線上零售持續推動法國箱板紙市場的發展,其每次出貨使用的瓦楞紙板數量遠超傳統主導配送。 2025年,電子商務將佔法國零售總額的13%,處理超過10億小包裹,每次出貨的包裝用量將比門市需求高出60%。 VPK集團已在其位於阿利澤的工廠調整策略,以適應這一需求,引入高解析度數位印刷平台,用於生產適合特定尺寸包裹的折疊式瓦楞紙板。此外,法國食品零售業店內商店包裝的日益普及,也推動了對兼具卓越印刷性能和可回收性的高規格面紙的需求。從長遠來看,管道結構的這種轉變將推動法國箱板紙市場價值的成長,而不僅僅是噸位的增加。

歐洲再生紙板市場供應過剩

歐洲供應成長速度超過了需求復甦速度,這仍然是法國瓦楞紙板原紙市場的主要拖累因素。產業報告顯示,自2022年以來,歐洲瓦楞紙板原紙的運轉率一直低於歷史平均水平,原因是新增產能投入使用時,市場尚未從庫存調整中完全恢復。在法國,Alizée和Golbey的投產加劇了再生紙市場的國內競爭,並將持續對棕色瓦楞紙板原紙的價格構成下行壓力,這種情況將持續到2025年。挪威森林公司(Norske Skog)證實,Golbey PM1在2025年運作之初累計了EBITDA虧損,因為銷售價格的下降僅部分被再生紙(OCC)成本的降低所抵消。簡而言之,除非需求顯著改善或歐洲進一步削減產能,否則法國瓦楞紙板原紙市場價格恢復到健康水準的前景渺茫。

細分市場分析

2025年,再生纖維佔法國瓦楞紙板市佔率的58.41%。這得歸功於法國完善的廢紙回收體係以及再生材料在正常情況下持續存在的成本優勢。再生紙板在法國瓦楞紙板行業中繼續佔據核心地位,測試襯紙和瓦楞紙板原紙仍然是食品、零售和電子商務等行業瓦楞紙板應用的主要供應來源。 Alizay和Golbey的快速投產增加了2025年法國國內再生瓦楞紙板的供應量,從而持續推高了棕色瓦楞紙板的價格。此外,Blue Paper SAS公司與法國航運公司(Voies Navigables de France)於2026年4月合作,採用水路運輸廢紙,這表明中型造紙廠正在透過改變採購和運輸方式來應對市場變化。

儘管2025年原生紙漿在法國瓦楞紙板市場中所佔佔有率仍然相對較小,但預計到2031年,其在法國瓦楞紙板市場規模中的複合年成長率將達到1.68%。這一成長主要源自於電商包裝和商店展示應用領域對優質牛皮紙襯紙需求的增加,在這些應用中,強度、印刷品質和紙張重量比最低成本的原料更為重要。斯莫菲特威洛克(Smurfit Westlock)將其位於法國的工廠定位為集團全球規模最大、成本最低的牛皮紙襯紙工廠之一,使其成為優質襯紙的重要供應樞紐。此外,與歐盟木材法規(EUDR)相關的可追溯性要求可能會使從歐盟以外地區進口原生纖維的採購和文件編制變得更加複雜。隨著買家越來越重視可追溯性和合規性,擁有認證供應鏈的法國和其他歐盟生產商將更具優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- AGEC和PPWR下的塑膠纖維替代

- 食品和飲料用紙箱需求的復甦

- 最佳化電子商務與商店展示包裝

- Alizai 和 Golbey 的產能將重建國內供應。

- 生質主導脫碳造紙廠的經濟效益

- 對永續包裝解決方案的需求日益成長

- 市場限制因素

- 歐洲再生紙板供應過剩

- 將EPR、RDUE和可追溯性成本加起來

- 能源價格波動和工業生產疲軟

- 進口棕色再生纖維會對利潤帶來壓力。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Saica Group

- VPK Group

- Smurfit Westrock plc

- Norske Skog ASA

- Palm Group

- Papeteries Palm SAS

- International Paper Company

- Blue Paper SAS

- Klingele Paper & Packaging Group

- Cartonnerie Gondardennes

- CGW Packaging Group

- Lacaux Freres

- Gemdoubs SAS

- NorPaper SAS

- Allard Emballages

- Seyfert Packaging SAS

- Papeterie de Giroux

第7章 市場機會與未來展望

According to Mordor Intelligence, the france containerboard market size is projected to expand from USD 3.12 billion in 2025 and USD 3.19 billion in 2026 to USD 3.42 billion by 2031, at a CAGR of 1.41% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Containerboard Market Trends and Insights

Plastic-To-Fiber Substitution Under AGEC And PPWR

France's AGEC framework and the EU Packaging and Packaging Waste Regulation adopted in 2025 remain the clearest medium-term support for the France containerboard market. Decree No. 2022-748 requires producers and importers above the stated thresholds to disclose recyclability characteristics and recycled-content percentages from January 1, 2025, thereby making packaging composition more visible to buyers and regulators. The same policy direction increases the commercial appeal of recyclable fiber grades in secondary and transit packaging, especially where plastic formats face weaker compliance economics. It is also expanding the addressable space for higher-value grades, such as white-top testliner and coated containerboard, in food, cosmetics, and other presentation-sensitive uses. This keeps regulatory demand support in place even while the near-term volume picture for the France containerboard market remains restrained.

E-Commerce And Shelf-Ready Packaging Optimization

Online retail continues to support the France containerboard market because corrugated use per shipment is higher than in traditional store-led distribution. E-commerce accounted for 13% of French retail sales in 2025, and parcel volumes exceeded 1 billion units, while packaging intensity per shipment was up to 60% above in-store requirements. VPK Group has already aligned part of its Alizay strategy with that demand by deploying a high-definition digital printing platform for fanfold corrugated formats used in right-sized shipping. Shelf-ready packaging is also gaining ground in French food retail, and that shift favors higher-specification liner grades that combine better print performance with recyclability. Over time, this channel mix is likely to support value growth in the France containerboard market more than simple tonnage growth.

European Recycled Containerboard Overcapacity

European supply additions have outpaced demand recovery, and this remains the main brake on the French containerboard market. Industry reporting shows that containerboard operating rates across Europe fell below historical norms after 2022 as new capacity arrived before the market had fully recovered from destocking. In France, the Alizay and Golbey start-ups intensified domestic competition in recycled grades and kept brown corrugated case material prices under pressure through 2025. Norske Skog confirmed that Golbey PM1 posted negative EBITDA during the ramp-up phase in 2025 because lower sales prices were only partly offset by lower OCC costs. This means the France containerboard market is unlikely to regain healthier pricing conditions until demand improves materially or more capacity exits the broader European system.

Other drivers and restraints analyzed in the detailed report include:

- Food And Beverage Corrugated Demand Resilience

- Alizay And Golbey Capacity Reshaping Domestic Supply

- EPR, EUDR, And Traceability Cost Stack

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 58.41% of the French containerboard market share in 2025, supported by France's established recovered-paper system and the usual cost advantage that recycled feedstock provides under normal conditions. Recycled grades remain central to the French containerboard industry because testliners and corrugating media still form the core of supply for food, retail, and e-commerce corrugated applications. The rapid start-up of Alizay and Golbey increased the domestic supply of recycled containerboard and prolonged price pressure on brown grades during 2025. Blue Paper SAS also showed how mid-sized mills are adjusting by changing procurement and transport choices, after adopting river transport for recovered paper shipments in partnership with Voies Navigables de France in April 2026.

Virgin fibers are projected to grow at a 1.68% CAGR in the France containerboard market size outlook through 2031, even though they remained the smaller material segment in 2025. That growth is tied to stronger demand for premium kraftliner in e-commerce outer boxes and shelf-facing applications where strength, print quality, and lower basis weight matter more than lowest-cost input selection. Smurfit Westrock described its Facture site in France as one of the group's largest and lowest-cost kraftliner mills globally, providing a useful platform for premium linerboard supply. EUDR-related traceability requirements can also make sourcing and documenting some non-EU virgin-fiber imports less straightforward. That could leave French and other EU producers with certified supply chains in a stronger position as buyers place more weight on traceability and compliance.

List of Companies Covered in this Report:

- Saica Group

- VPK Group

- Smurfit Westrock plc

- Norske Skog ASA

- Palm Group

- Papeteries Palm SAS

- International Paper Company

- Blue Paper SAS

- Klingele Paper & Packaging Group

- Cartonnerie Gondardennes

- CGW Packaging Group

- Lacaux Freres

- Gemdoubs SAS

- NorPaper SAS

- Allard Emballages

- Seyfert Packaging SAS

- Papeterie de Giroux

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Plastic-to-fiber substitution under AGEC and PPWR

- 4.2.2 Food and beverage corrugated demand resilience

- 4.2.3 E-commerce and shelf-ready packaging optimization

- 4.2.4 Alizay and Golbey capacity reshaping domestic supply

- 4.2.5 Biomass-led decarbonized mill economics

- 4.2.6 Rising Demand for Sustainable Packaging Solutions

- 4.3 Market Restraints

- 4.3.1 European recycled containerboard overcapacity

- 4.3.2 EPR, RDUE, and traceability cost stack

- 4.3.3 Energy-price volatility and weak industrial output

- 4.3.4 Margin Pressure From Imported Brown Recycled Fiber

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Saica Group

- 6.4.2 VPK Group

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Norske Skog ASA

- 6.4.5 Palm Group

- 6.4.6 Papeteries Palm SAS

- 6.4.7 International Paper Company

- 6.4.8 Blue Paper SAS

- 6.4.9 Klingele Paper & Packaging Group

- 6.4.10 Cartonnerie Gondardennes

- 6.4.11 CGW Packaging Group

- 6.4.12 Lacaux Freres

- 6.4.13 Gemdoubs SAS

- 6.4.14 NorPaper SAS

- 6.4.15 Allard Emballages

- 6.4.16 Seyfert Packaging SAS

- 6.4.17 Papeterie de Giroux

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)