|

市場調查報告書

商品編碼

2065459

馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Malaysia Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

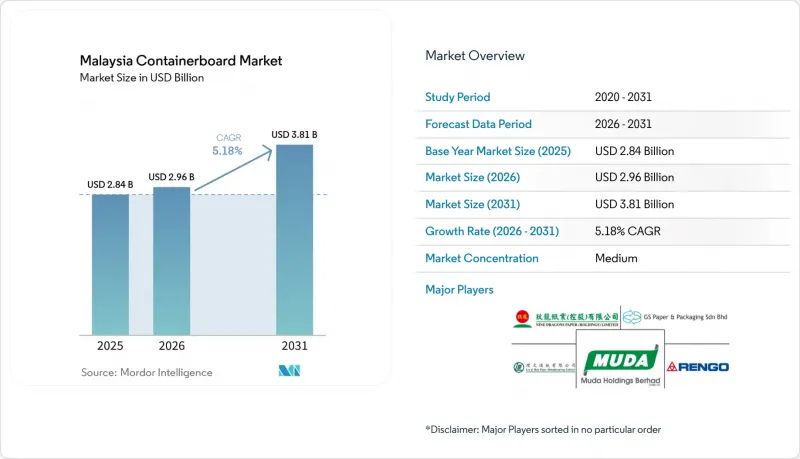

預計馬來西亞箱板市場規模將從 2025 年的 28.4 億美元和 2026 年的 29.6 億美元成長到 2031 年的 38.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.18%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業等)進行細分。市場預測以美元計價。

馬來西亞箱板市場趨勢與洞察

電子商務導致小包裹處理量增加

線上零售正在為都市區和郊區配送網路中的二級包裝和運輸包裝帶來穩定的需求,從而推動馬來西亞瓦楞紙板市場持續成長。 Ninja Van Malaysia預測,鑑於全國小包裹收件人數已超過2,000萬,2026年國內小包裹量將比2025年增加5%至10%。預計到2025年,馬來西亞宅配市場規模將達到68億至69億馬幣(約合16億至17億美元),凸顯了配送服務在本地小包裹流通中日益重要的作用。這也正在改變紙箱規格,因為許多電商經銷商要求使用單層瓦楞紙箱,並要求紙箱表面印刷精美,以提升展示效果和配送體驗。此外,電子商務的需求正在推動小批量生產和頻繁的設計變更,使紙張製造商和加工商能夠透過兼顧穩定的紙板品質和快速的配送速度而獲得競爭優勢。

食品飲料包裝的優質化

食品飲料產業仍是馬來西亞瓦楞紙板市場的主要需求方,但其產品構成正從簡單的棕色運輸包裝轉向高附加價值的紙箱。馬來西亞被評為穩定市場,在更廣泛的區域食品飲料市場機會中,其年價值成長目標為2-3%。具有印刷表面和防破損功能的零售瓦楞紙產品比標準普通槽式紙箱價格明顯更高。這意味著即使貨運量成長速度適中,單位瓦楞紙的消耗量也可能增加。冷藏產品、高階零食和品牌食品的銷售也支撐了這種需求模式,這些產品都需要在潮濕環境中擁有更佳的外觀和更穩定的性能。低溫運輸活動是另一個推動因素,因為當食品包裝需要經過更長的物流鏈時,其防潮性和表面品質就顯得特別重要。

二手紙板箱的價格和供應波動

舊瓦楞紙箱(OCC)價格波動仍然是馬來西亞瓦楞紙板原紙市場面臨的最主要短期壓力。這是因為再生紙廠極易受到進口紙漿成本波動的影響。一份2025年的產業報告指出,OCC和混合紙市場的價格波動並非暫時性的干擾,而是一種持續存在的狀況,供需失衡往往會持續數月之久。這使得那些在現貨市場大量採購紙漿,然後難以迅速將上漲的成本轉嫁給瓦楞紙箱客戶的造紙企業難以進行規劃。當能源成本也上漲時,問題會進一步加劇,因為再生瓦楞紙板的獲利能力同時受到紙漿和能源成本的雙重壓力。實際上,與那些主要依賴進口OCC的造紙企業相比,那些與國內回收網路聯繫緊密或擁有長期採購合約的造紙企業,其利潤率更為穩定。

細分市場分析

預計到2025年,再生纖維將佔馬來西亞瓦楞紙板原紙市場的66.18%,這證實了該國的瓦楞紙板體系仍依賴於長期建立的原瓦楞紙板(OCC)收集、再生紙芯生產和測試襯紙生產能力。多年來,馬來西亞瓦楞紙板原紙產業已建立起以再生原料為中心的造紙廠收入結構,即使產品要求日益複雜,再生紙的需求仍然強勁。近年來,馬來西亞廢紙貿易也反映出,與混合生活垃圾相比,分揀後的國產廢紙溢價不斷提高。馬來西亞瓦楞紙板市場的這一領域具有成本效益高、纖維生產線共用以及下游市場對標準瓦楞紙板應用的認可度高等優勢。這也與馬來西亞作為加工和消費中心的地位相符,國內對瓦楞紙板的廣泛需求支撐了對再生襯紙和中型的穩定需求。

原生紙漿是成長最快的材料類別,預計2026年至2031年將以5.63%的複合年成長率成長。這主要得益於電子產品出口、低溫運輸食品包裝以及零售包裝對更強韌、更潔淨的紙板表面的需求不斷成長。 GS紙板包裝公司位於雪蘭莪州的PM3工廠投資12億馬來西亞馬幣(約合2.9億美元),將使用100%再生材料,每年生產高達45萬噸的輕質試驗級面紙,這表明馬來西亞國內製造商正在不斷突破再生瓦楞紙板的性能極限。同時,Nextgreen IOI Pulp和廈門建發紙漿集團宣布,將於2025年4月在彭亨州建造馬來西亞首個綜合紙漿工廠,年產能為15萬噸。第一階段的資本投資將達到9億馬來西亞馬幣(約2.02億美元),並將以棕櫚生質能為原料。如果該專案成功推進,預計將降低馬來西亞對貨櫃紙板進口的依賴,並有可能在未來改善本地牛皮紙襯紙的生產成本。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務小包裹處理量增加

- 食品飲料包裝的高階化

- 電子電氣設備的出口競爭力

- 逐步淘汰一次性塑膠製品

- 「中國+1」策略對馬來西亞製造業的連鎖反應

- 提高國內工廠輕質再生板材的質量

- 市場限制因素

- 二手瓦楞紙箱的價格和供應波動

- 與低成本塑膠包裝形式的競爭

- 來自中國的產能湧入和區域供應過載壓力

- 麵粉廠自動化和熟練人員短缺

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- GS Paperboard & Packaging Sdn Bhd

- Muda Paper Mills Sdn. Bhd.

- ND Paper(Malaysia)Sdn. Bhd.

- Lee & Man Paper Manufacturing Ltd.

- Rengo Packaging Malaysia Sdn Bhd

- Can-One Berhad

- KYM Industries(M)Sdn Bhd

- Ornapaper Industry(M)Sdn. Bhd.

- Box-Pak(Malaysia)Bhd

- Golden Corrugated Box(M)Sdn Bhd

- Avapac Sdn Bhd

- PD Pac Sdn. Bhd.

- Fibre Pak(Malaysia)Sdn. Bhd.

- YCN Carton Sdn Bhd

- Bintang Packaging Industries(M)Sdn Bhd

- Pine Packaging(M)Sdn. Bhd.

- Honwee Packaging Sdn. Bhd.

- Century Bond Bhd

第7章 市場機會與未來展望

According to Mordor Intelligence, the malaysia containerboard market size is projected to expand from USD 2.84 billion in 2025 and USD 2.96 billion in 2026 to USD 3.81 billion by 2031, registering a CAGR of 5.18% between 2026 to 2031.

This report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Containerboard Market Trends and Insights

Rising E-Commerce Parcel Volumes

Parcel demand continues to lift the Malaysian containerboard market, as online retail creates a steady flow of secondary and transit packaging across urban and suburban delivery networks. Ninja Van Malaysia projected 5% to 10% growth in domestic parcel volumes in 2026 versus 2025, after already reaching more than 20 million parcel recipients nationwide. Malaysia's courier market was valued at MYR 6.8-6.9 billion (USD 1.6-1.7 billion) in 2025, underscoring the growing role of delivery services in the local packaging flow. This is changing box specifications as well, because many marketplace sellers now want single-wall corrugated boxes with cleaner print surfaces that improve shelf appeal and the delivery experience. E-commerce demand also supports shorter production runs and more frequent design changes, giving mills and converters an edge by pairing consistent board quality with fast turnaround.

Food And Beverage Packaging Premiumization

Food and beverage remains a core volume base for the Malaysia containerboard market, but the mix is moving toward higher-value box formats rather than simple brown transit packaging. Malaysia was described as a stable market that targets 2% to 3% annual value growth within the broader regional food and beverage opportunity. Retail-ready corrugated formats with pre-printed surfaces and controlled-tear features command clear pricing premiums over standard regular slotted containers, which means board consumption per unit can rise even when shipment volume grows at a slower pace. The demand pattern is also supported by chilled products, premium snacks, and branded grocery distribution, all of which require better presentation and more consistent performance in humid conditions. Cold-chain activity adds another layer, because moisture resistance and surface quality matter more when food packaging must move through longer logistics chains.

Old Corrugated Container Price And Supply Volatility

Old corrugated container volatility remains the clearest short-term pressure point for the Malaysian containerboard market, as recycled-grade mills are exposed to swings in imported fiber costs. Industry coverage in 2025 described volatility in OCC and mixed paper markets as a persistent condition rather than a temporary disruption, with supply and demand often falling out of step for several months. This creates planning difficulties for mills that buy heavily in the spot market and then struggle to quickly pass higher costs through to box customers. The issue becomes more serious when energy costs also rise, because recycled-board economics then come under pressure from both fiber and utilities simultaneously. In practice, mills with stronger domestic collection ties or longer procurement contracts have a more durable margin position than mills that depend mainly on imported OCC cargoes.

Other drivers and restraints analyzed in the detailed report include:

- Electronics And E&E Export Strength

- Shift Away From Single-Use Plastics

- Competition From Low-Cost Plastic Packaging Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 66.18% of the Malaysian containerboard market share in 2025, confirming that the local system still relies on long-established OCC collection, recycled-medium production, and testliner capacity. The Malaysian containerboard industry has spent years building mill economics around recycled inputs, keeping recycled grades central to volume demand even as product requirements become more complex. Malaysia's recovered paper trade also reflected improving quality premiums for sorted domestic grades relative to mixed household collections in recent periods. This part of the Malaysia containerboard market benefits from cost efficiency, shared fiber lines, and established downstream acceptance across standard box applications. It also fits the country's role as a converting and consuming base, where broad domestic box demand supports a steady pull for recycled liners and mediums.

Virgin fibers are the fastest-growing material segment, with a forecast CAGR of 5.63% from 2026 to 2031, driven by increased demand from electronics exports, cold-chain food packaging, and retail-ready formats that require stronger, cleaner board surfaces. GS Paperboard and Packaging's PM3 in Selangor, built with a MYR 1.2 billion (USD 0.29 billion) investment, produces lightweight testliner grades from 100% recycled material at up to 450,000 tonnes annually, demonstrating that domestic producers are still raising the performance ceiling of recycled board. At the same time, Nextgreen IOI Pulp and Xiamen C&D Paper and Pulp Group announced Malaysia's first 150,000-tonne integrated pulp facility in Pahang in April 2025, with Phase 1 capital expenditure of MYR 900 million (USD 202 million) using palm biomass feedstock. If that project scales well, it could ease import dependence in the Malaysia containerboard market and improve the local cost base for kraftliner production over time.

List of Companies Covered in this Report:

- GS Paperboard & Packaging Sdn Bhd

- Muda Paper Mills Sdn. Bhd.

- ND Paper (Malaysia) Sdn. Bhd.

- Lee & Man Paper Manufacturing Ltd.

- Rengo Packaging Malaysia Sdn Bhd

- Can-One Berhad

- KYM Industries (M) Sdn Bhd

- Ornapaper Industry (M) Sdn. Bhd.

- Box-Pak (Malaysia) Bhd

- Golden Corrugated Box (M) Sdn Bhd

- Avapac Sdn Bhd

- PD Pac Sdn. Bhd.

- Fibre Pak (Malaysia) Sdn. Bhd.

- YCN Carton Sdn Bhd

- Bintang Packaging Industries (M) Sdn Bhd

- Pine Packaging (M) Sdn. Bhd.

- Honwee Packaging Sdn. Bhd.

- Century Bond Bhd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce Parcel Volumes

- 4.2.2 Food and Beverage Packaging Premiumization

- 4.2.3 Electronics and E&E Export Strength

- 4.2.4 Shift Away From Single-Use Plastics

- 4.2.5 China-Plus-One Manufacturing Spillover Into Malaysia

- 4.2.6 Lightweight Recycled Board Upgrades at Domestic Mills

- 4.3 Market Restraints

- 4.3.1 Old Corrugated Container Price and Supply Volatility

- 4.3.2 Competition From Low-Cost Plastic Packaging Formats

- 4.3.3 Chinese Capacity Influx and Regional Oversupply Pressure

- 4.3.4 Mill Automation and Technical Talent Gaps

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GS Paperboard & Packaging Sdn Bhd

- 6.4.2 Muda Paper Mills Sdn. Bhd.

- 6.4.3 ND Paper (Malaysia) Sdn. Bhd.

- 6.4.4 Lee & Man Paper Manufacturing Ltd.

- 6.4.5 Rengo Packaging Malaysia Sdn Bhd

- 6.4.6 Can-One Berhad

- 6.4.7 KYM Industries (M) Sdn Bhd

- 6.4.8 Ornapaper Industry (M) Sdn. Bhd.

- 6.4.9 Box-Pak (Malaysia) Bhd

- 6.4.10 Golden Corrugated Box (M) Sdn Bhd

- 6.4.11 Avapac Sdn Bhd

- 6.4.12 PD Pac Sdn. Bhd.

- 6.4.13 Fibre Pak (Malaysia) Sdn. Bhd.

- 6.4.14 YCN Carton Sdn Bhd

- 6.4.15 Bintang Packaging Industries (M) Sdn Bhd

- 6.4.16 Pine Packaging (M) Sdn. Bhd.

- 6.4.17 Honwee Packaging Sdn. Bhd.

- 6.4.18 Century Bond Bhd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)