|

市場調查報告書

商品編碼

2065458

越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Vietnam Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

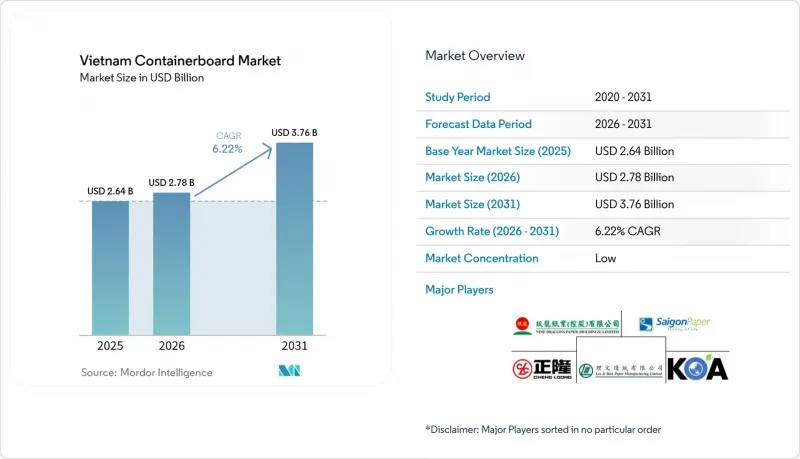

2025年越南箱板市值為26.4億美元,預計2031年將從2026年的27.8億美元成長至37.6億美元,預測期(2026-2031年)複合年成長率為6.22%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業等)進行細分。市場預測以美元計價。

越南箱板紙市場趨勢與洞察

電子商務小包裹的擴張以及最後一公里瓦楞紙箱使用密度的增加。

預計2026年第一季,越南領先的電子商務平台商品交易總額(GMV)將達到148.6兆越南盾(約57億美元),商品銷售量將達到11.4億件。與上年同期相比,分別成長47%和20%。越南國內電子商務市場預計到2025年將達到310億美元,使越南躋身全球十大線上零售市場之列,並名列東協前三名。越南瓦楞紙板市場的一個關鍵轉變是轉向採用更個性化的履約和更安全的運輸方式。儘管商品數量的成長速度低於銷售額的成長速度,但這仍然導致每筆訂單所需的瓦楞紙板數量增加。這一趨勢在胡志明市、河內和平陽省尤為明顯,這些城市是小包裹密度、倉儲和最後一公里配送活動最為集中的地區。 《2026-2030年國家電子商務發展總體規劃》的目標是實現線上零售年成長率15-20%,預計未來幾年越南瓦楞紙板市場將因出貨量的增加而迎來穩定的需求成長。

出口導向製造業的轉移正在提振對工業瓦楞紙板的需求。

預計到2025年,越南製造業將成長10.6%,創七年來工業生產成長新高。同時,電子設備和電腦出口額預計將超過1,000億美元,紡織品出口額預計將達460億美元。一項針對日本企業的調查顯示,在越南營運的受訪企業中,56.9%計劃在未來一到兩年內擴大產能,這一擴張意向率在東南亞國協中最高。這對越南瓦楞紙板原紙市場具有重大意義,因為每家新廠都會產生多層包裝需求,包括組件包裝、半成品包裝和出口主紙箱。此外,電子設備的組裝過程需要更堅固的瓦楞紙板,通常採用三層或五層紙箱結構,這增加了對高性能牛皮紙面紙和瓦楞紙的需求。隨著出口導向生產向南北工業區轉移,越南箱板紙市場正朝著更工業化、規格主導的需求方向發展。

OCC和紙漿價格的波動給加工商的利潤率帶來了壓力。

2024年下半年,越南造紙商為美國雙分揀瓦楞紙板支付的價格為每噸195-200美元,但隨後的價格下跌改變了整個東南亞地區的採購格局。中國於2025年10月實施的再生紙漿進口限制擾亂了區域內的瓦楞紙板製紙漿供應鏈,並改變了進口再生纖維的採購模式。大規模綜合造紙商由於規模更大、庫存更多、定價能力更強,因此比小規模造紙商和加工商更能應對這種壓力。據越南紙漿協會稱,到2025年,國內回收僅能滿足56%的瓦楞紙板需求,剩餘的44%將面臨全球再生紙價格和運費波動的影響。由於成本波動波及整個供應鏈的速度遠超過銷售價格的調整速度,因此這種影響仍是越南瓦楞紙板市場短期內最大的拖累因素。

細分市場分析

2025年,再生纖維在越南瓦楞紙板市場佔有穩固的領先地位,市佔率高達68.11%。這主要歸功於OCC(舊瓦楞紙板)仍然是標準瓦楞紙板中最經濟的選擇。越南本地瓦楞紙板生產歷來80%以上依賴再生紙原料,因此再生材料在造紙廠的盈利和加工商的採購模式中繼續發揮核心作用。越南國內OCC回收率從2021年的46%提高到2024年的58%,降低了(但並未完全消除)對進口再生纖維的依賴。預計到2028年,亞洲OCC加工總產能將增加450萬噸,其中越南將佔近一半。這將進一步鞏固越南作為該地區再生纖維加工大國的地位。

到2025年,原生纖維將佔越南瓦楞紙板市場佔有率的31.89%,預計到2031年,越南瓦楞紙板市場的這一細分領域將以6.74%的複合年成長率成長。太原省和北寧省等地區的電子和半導體組裝過程需要抗壓強度更穩定、抗濕性更低的包裝材料,這推動了對優質箱板紙的需求。由於範圍3報告的要求,跨國買家也要求本地供應商提高再生紙含量,儘管他們的包裝規格通常仍然要求性能標準更有利於主要由原生紙漿製成的紙板。這種矛盾持續導致優質紙板供不應求,促使企業願意進一步投資於原生紙漿相容的資產。因此,儘管再生紙板仍然是最大的基礎,但越南箱板紙產業正在轉向更混合的原料組成。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務小包裹數量的成長以及最後一公里包裹密度的增加。

- 出口製造地的轉移正在提振對工業瓦楞紙板的需求。

- 食品飲料低溫運輸和現代零售的擴張。

- 減少塑膠的使用以及遵守生產者延伸責任制 (EPR) 正在推動紡織包裝的普及。

- 範圍 3 採購規則優先考慮輕質、本地採購的再生板材。

- 透過人工智慧驅動的箱體最佳化提高小批量訂單的產量。

- 市場限制因素

- OCC(舊瓦楞紙箱)和紙漿價格的波動給造紙企業的利潤率帶來了壓力。

- 對原生纖維和優質工藝襯裡等級的進口依賴性

- 季風引起的濕度在儲存和運輸過程中會降低抗壓強度。

- 出口市場中ESG可追溯性和碳資訊揭露的負擔

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Vina Kraft Paper Co., Ltd.

- Cheng Loong Binh Duong Paper Co., Ltd.

- Vietnam Lee & Man Paper Manufacturing Limited

- Nine Dragons Paper(Holdings)Limited

- Kraft of Asia Paperboard & Packaging Co., Ltd.

- Saigon Paper Corporation

- Dong Hai Ben Tre Joint Stock Company

- Miza Corporation

- HHP Global Joint Stock Company

- Minhan Paper Joint Stock Company

- Dong Tien-Long An Paper Joint Stock Company

- Vina Corrugated Packaging Co., Ltd.

- Bien Hoa Packaging Joint Stock Company

- Settsu Carton Vietnam Corporation

- Ojitex(Vietnam)Company Limited

- Song Lam Trading & Packaging Production Co., Ltd.

- Khang Thanh Manufacturing Co., Ltd.

- HC Packaging Vietnam Company Limited

- Starprint Vietnam Joint Stock Company

- United Packaging Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the vietnam containerboard market size was valued at USD 2.64 billion in 2025 and estimated to grow from USD 2.78 billion in 2026 to reach USD 3.76 billion by 2031, at a CAGR of 6.22% during the forecast period (2026-2031).

This report is Segmented by Material (Virgin Fibers and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Containerboard Market Trends and Insights

E-Commerce Parcel Expansion And Last-Mile Box Intensity

Vietnam's leading e-commerce platforms generated VND 148.6 trillion (USD 5.7 billion) in gross merchandise value in Q1 2026, while sales volume reached 1.14 billion items, up 47% and 20% year over year, respectively. Vietnam's domestic e-commerce market reached USD 31 billion in 2025, placing the country among the world's top 10 and ASEAN's top 3 online retail markets. The important shift in the Vietnam containerboard market is that fulfillment is moving toward more individually boxed, better-protected shipments, which increases corrugated board usage per order even as item counts grow more slowly than sales value. This pattern is strongest in Ho Chi Minh City, Hanoi, and Binh Duong, where parcel density, warehousing, and last-mile activity are most concentrated. With the National E-commerce Development Master Plan for 2026-2030 targeting annual online retail growth of 15%-20%, the Vietnam containerboard market is set to receive a steady flow of shipment-driven demand over the next several years.

Export Manufacturing Relocation Boosting Industrial Carton Demand

Vietnam's manufacturing sector grew 10.6% in 2025, the strongest industrial output growth in 7 years, while electronics and computers exceeded USD 100 billion in exports, and textiles reached USD 46 billion in exports. A survey of Japanese firms showed that 56.9% of respondents in Vietnam planned capacity expansion over the next 1-2 years, the highest expansion intent rate in ASEAN. For the Vietnam containerboard market, this matters because each new factory adds several layers of packaging demand, including packaging for components, intermediate goods, and export master cartons. Electronics assembly also requires stronger corrugated formats, often using 3-layer and 5-layer box structures, which increases demand for higher-performance kraftliner and fluting grades. As more export-oriented production shifts to northern and southern industrial provinces, the Vietnam containerboard market continues to move toward a more industrial, specification-driven demand base.

OCC And Pulp Cost Volatility Squeezing Converter Margins

Vietnam-bound mills were paying USD 195-200 per ton for US double-sorted OCC in late 2024 before later price declines changed procurement economics across Southeast Asia. China's recycled pulp import restrictions, introduced in October 2025, disrupted the regional OCC-to-pulp chain and altered buying patterns for imported recovered fiber. Large integrated mills can handle this pressure better because they have scale, broader inventories, and stronger pricing leverage than smaller mills and converters. Vietnam's Pulp and Paper Association said domestic collection met only 56% of OCC demand in 2025, leaving the remaining 44% exposed to global recovered paper and freight swings. That exposure remains the biggest near-term brake on the Vietnam containerboard market because cost movements can pass through the supply chain faster than selling prices can be reset.

Other drivers and restraints analyzed in the detailed report include:

- Food And Beverage Cold-Chain And Modern Retail Expansion

- Plastic Substitution And EPR Compliance Favoring Fiber Packaging

- Import Dependence For Virgin Fiber And Premium Kraftliner Grades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 68.11% of the Vietnam containerboard market share in 2025, keeping them firmly in the leading position, as OCC-based board remained the most economical option for standard corrugated grades. Over 80% of local production historically relied on recovered paper feedstock, so recycled furnish stayed central to mill economics and converter sourcing patterns. Vietnam's domestic OCC recovery rate improved from 46% in 2021 to 58% in 2024, reducing but not eliminating import dependence for recycled fiber supply. Asia's total OCC capacity is expected to grow by 4.5 million tons by 2028, with Vietnam contributing close to half of that expansion, strengthening the country's role as a regional secondary fiber processor.

Virgin fibers accounted for 31.89% in 2025, and this segment of the Vietnam containerboard market is projected to grow at a 6.74% CAGR through 2031. Electronics and semiconductor assembly in provinces such as Thai Nguyen and Bac Ninh require packaging with more stable compression strength and lower moisture sensitivity, which supports demand for premium linerboard grades. Multinational buyers are also pushing local suppliers to increase recycled content because of Scope 3 reporting, but their packaging specifications still require performance standards that often favor virgin-furnish board. That conflict keeps a premium-grade supply gap in place and supports further investment interest in virgin-capable assets. The Vietnam containerboard industry is therefore moving toward a more mixed furnish structure, even though recycled board remains the largest base.

List of Companies Covered in this Report:

- Vina Kraft Paper Co., Ltd.

- Cheng Loong Binh Duong Paper Co., Ltd.

- Vietnam Lee & Man Paper Manufacturing Limited

- Nine Dragons Paper (Holdings) Limited

- Kraft of Asia Paperboard & Packaging Co., Ltd.

- Saigon Paper Corporation

- Dong Hai Ben Tre Joint Stock Company

- Miza Corporation

- HHP Global Joint Stock Company

- Minhan Paper Joint Stock Company

- Dong Tien-Long An Paper Joint Stock Company

- Vina Corrugated Packaging Co., Ltd.

- Bien Hoa Packaging Joint Stock Company

- Settsu Carton Vietnam Corporation

- Ojitex (Vietnam) Company Limited

- Song Lam Trading & Packaging Production Co., Ltd.

- Khang Thanh Manufacturing Co., Ltd.

- HC Packaging Vietnam Company Limited

- Starprint Vietnam Joint Stock Company

- United Packaging Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Parcel Expansion and Last-Mile Box Intensity

- 4.2.2 Export Manufacturing Relocation Boosting Industrial Carton Demand

- 4.2.3 Food and Beverage Cold-Chain and Modern Retail Expansion

- 4.2.4 Plastic Substitution and EPR Compliance Favoring Fiber Packaging

- 4.2.5 Scope 3 Procurement Rules Favoring Lightweight Local Recycled Board

- 4.2.6 AI-Led Box Optimization Improving Yield for Short-Run Orders

- 4.3 Market Restraints

- 4.3.1 OCC and Pulp Cost Volatility Squeezing Converter Margins

- 4.3.2 Import Dependence for Virgin Fiber and Premium Kraftliner Grades

- 4.3.3 Monsoon Humidity Weakening Compression Strength in Storage and Transit

- 4.3.4 Export-Market ESG Traceability and Carbon Disclosure Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Vina Kraft Paper Co., Ltd.

- 6.4.2 Cheng Loong Binh Duong Paper Co., Ltd.

- 6.4.3 Vietnam Lee & Man Paper Manufacturing Limited

- 6.4.4 Nine Dragons Paper (Holdings) Limited

- 6.4.5 Kraft of Asia Paperboard & Packaging Co., Ltd.

- 6.4.6 Saigon Paper Corporation

- 6.4.7 Dong Hai Ben Tre Joint Stock Company

- 6.4.8 Miza Corporation

- 6.4.9 HHP Global Joint Stock Company

- 6.4.10 Minhan Paper Joint Stock Company

- 6.4.11 Dong Tien-Long An Paper Joint Stock Company

- 6.4.12 Vina Corrugated Packaging Co., Ltd.

- 6.4.13 Bien Hoa Packaging Joint Stock Company

- 6.4.14 Settsu Carton Vietnam Corporation

- 6.4.15 Ojitex (Vietnam) Company Limited

- 6.4.16 Song Lam Trading & Packaging Production Co., Ltd.

- 6.4.17 Khang Thanh Manufacturing Co., Ltd.

- 6.4.18 HC Packaging Vietnam Company Limited

- 6.4.19 Starprint Vietnam Joint Stock Company

- 6.4.20 United Packaging Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)