|

市場調查報告書

商品編碼

2064395

印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)India Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

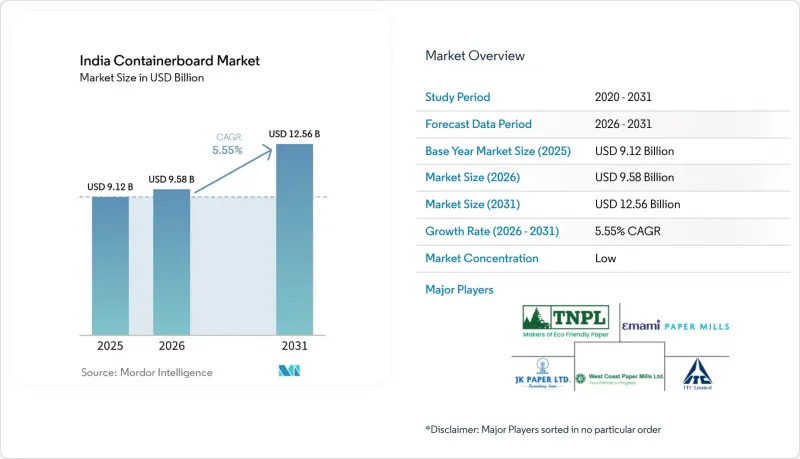

據 Mordor Intelligence 稱,印度瓦楞紙板原紙市場預計將從 2025 年的 91.2 億美元成長到 2026 年的 95.8 億美元,到 2031 年達到 125.6 億美元,2026 年至 2031 年的複合年成長率為 5.55%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業等)進行細分。市場預測以美元計價。

印度箱板紙市場趨勢與洞察

電子商務和快速交易帶動了對瓦楞紙板的需求增加。

印度快速商業領域的商品交易總額(GMV)預計將在2024年達到33.5億美元,並在2028年以27.42%的複合年成長率成長至88.3億美元,這將徹底改變都市區履約網路中的包裝需求格局。到2025年,Blinkit將在100多個城市營運超過1500家「暗店」(dark store),Zepto和Swiggy Instamart也拓展至人口密集的「暗店」網路。這擴大了短期瓦楞紙板消費的潛在市場。這些網路不僅需要大量的紙箱,還需要緊湊、尺寸合適的瓦楞紙包裝,以承受從揀貨到出貨過程中反覆的橫向搬運。這項需求促使買家不再僅僅依賴爆破係數閾閾值,而是開始測試能夠更穩定地滿足其短期抗壓和抗壓邊需求的襯紙和瓦楞等級。造紙商目前仍主要與低成本的再生紙產品競爭,但由於自動化、快速的配送系統比傳統零售通路能更快地暴露紙張的結構缺陷和壓縮性能差異,他們被迫加強對紙張規格的控制。這種轉變對印度箱板紙市場影響重大,因為即使是對於大規模生產且價格敏感的包裝產品,市場需求也轉向技術可靠的工業級紙張。

食品飲料包裝的優質化

在印度的食品加工和飲料價值鏈中,隨著有組織的零售、食品安全要求以及對可回收包裝的推廣,包裝規範正日趨嚴格。可口可樂、百事可樂和Pearl Agro等品牌所有者正在調整其包裝組合,轉向可回收包裝,從而在有組織的經銷管道中增加了單一材料和纖維基二次包裝的使用。食品加工商也在努力減輕包裝重量,將內襯紙的紙張重量從150克/平方米降低到120克/平方米,同時透過更強韌的纖維設計和更優異的紙板工程來保持包裝的可壓縮性。 2026年4月,印度食品安全標準局(FSSAI)發布了一份草案通知,提案在麵包香料和菸草包裝中使用紙張、紙板、纖維素或其他天然衍生材料。這進一步加大了對纖維基材料的監管壓力,即使在長期以來依賴多層塑膠結構的品類中也是如此。這項變革意義重大,因為印度南部和西部地區對這些產品類型的需求已經很高,這意味著包裝類型的轉變可能會迅速蔓延至該地區對襯紙和牛皮紙的需求。在印度箱板紙市場,這種優質化趨勢提高了消費者對食品相關瓦楞紙包裝的印刷品質、抗壓強度均勻性和可回收性的基本期望。

再生紙和進口紙漿的價格波動

在印度,很大一部分再生紙板原料仍依賴海運的再生纖維。這種高度依賴性使得許多生產商極易受到進口再生紙(OCC)和其他原物料價格劇烈波動的影響。外匯波動加劇了這種風險,因為即使以美元計價的國際纖維價格看似穩定,印度盧比貶值也可能導致接收成本上升。這進一步擴大了擁有自有紙漿和種植園支持的一體化企業與高度依賴進口原料且採購週期短的再生纖維工廠之間的差距。中小型工廠尤其脆弱,因為它們缺乏足夠的財務柔軟性來應對進口狀況惡化時建立庫存緩衝,這可能迫使它們突然減產或提高本地價格。這種壓力也改變了採購行為,因為尋求高純度再生材料的工廠將更直接地競爭優質材料,而不是依賴國內混合廢料。在印度瓦楞紙板市場,纖維價格波動仍然是缺乏一體化系統或規模的生產商面臨的最緊迫的盈利風險。

細分市場分析

截至2025年,再生纖維佔印度瓦楞紙板原紙市場的64.53%。這反映了那些仍然高度依賴再生纖維以維持競爭力的製造地的成本結構。雖然印度廢紙和瓦楞紙板的回收率僅50%,但已開發國家的回收率高達85%,顯示印度國內的回收效率遠未達到完全滿足造紙廠原料需求的水準。這種差距影響了供應量和品質。回收系統的脆弱性導致國內再生纖維供應不穩定,迫使許多造紙廠依賴進口再生紙板(OCC)。原生纖維目前仍佔市場佔有率小規模,但在優質化和進口替代投資的推動下,預計到2031年將以6.02%的複合年成長率成長,從而支撐對高性能牛皮紙襯紙的需求。因此,印度箱板紙市場的材料轉型呈現兩極化的趨勢。雖然再生鋼材在數量上仍然佔據主導地位,但原生鋼材在需要更高抗壓強度、更光滑的表面和更高均勻性的應用中變得越來越有吸引力。

貿易措施也使原生紙受益,因為國際貿易救濟總局建議對中國原生紙板徵收每噸152.27美元的反傾銷稅,對智利原生紙板徵收每噸123.18美元的反傾銷稅。如果這些措施得以維持,將有助於提高國內造紙企業的盈利。 FSC認證和生產者延伸責任制(EPR)的合規性正逐漸成為印度箱板紙行業的市場准入要求,尤其對於日常消費品(FMCG)和藥品出口商而言更是如此。這些公司現在更加嚴格地審查包裝供應商的可追溯性和永續性記錄。 Paswala Papers公司就體現了該領域平衡的重要性。該公司正在將其牛皮紙與牛皮襯紙的比例從60:40調整為以襯紙主導的生產組合,同時優先從美國進口高品質的脫氧短纖維紙漿(DSOCC),而不是混合等級的再生紙漿。這一趨勢表明,即使是中型製造商也開始區分通用再生產品和高檔產品,這表明即使國內低檔紙漿的收集情況僅呈現漸進式改善,對高品質進口再生紙漿的需求也可能保持強勁。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 由於電子商務和快速交易的擴張,對瓦楞紙箱的需求增加。

- 食品飲料包裝的高階化

- 可再生纖維包裝法規帶來的推動作用

- 製造業和出口物流的擴張

- 輕巧而堅固的設計,適用於自動化瓦楞紙板生產

- 高品質工藝襯墊的進口替代品

- 市場限制因素

- 再生紙和進口紙漿的價格波動

- 電力、燃料和貨運成本上漲

- 國內再生纖維流的品質差異

- 因應歐盟自2027年起實施的廢棄物轉移法規

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ITC Limited

- JK Paper Limited

- West Coast Paper Mills Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- B&B Triplewall Containers

- Pakka Limited

- NR Agarwal Industries Limited

- Khanna Paper Mills Limited

- Paswara Papers Limited

- Bell Multi Kraft Private Limited

- Laxmi Board and Paper Mills Private Limited

- Apollo Papers LLP

- Venkraft Paper Mills Private Limited

- Aryan Paper Mills Private Limited

- Ruchira Papers Limited

- Star Paper Mills Limited

- Shree Ajit Pulp and Paper Limited

- Caliber Papers LLP

- Gauranga Papers LLP

第7章 市場機會與未來展望

According to Mordor Intelligence, the india containerboard market size is expected to increase from USD 9.12 billion in 2025 to USD 9.58 billion in 2026 and reach USD 12.56 billion by 2031, growing at a CAGR of 5.55% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

India Containerboard Market Trends and Insights

Rising E-Commerce And Quick-Commerce Corrugated Demand

India's quick-commerce sector reached USD 3.35 billion in gross merchandise value in 2024 and is projected to grow to USD 8.83 billion by 2028 at a 27.42% CAGR, which is reshaping packaging demand across urban fulfillment networks. Blinkit operated more than 1,500 dark stores across more than 100 cities in 2025, while Zepto and Swiggy Instamart had also scaled to dense dark-store networks, which widened the addressable base for short-cycle corrugated consumption. These networks do not just need more boxes; they need compact and right-sized corrugated packs that can withstand repeated lateral handling from picking to dispatch. That requirement is pushing buyers toward testliner and fluting grades that meet short-span compression and edge-crush needs with greater consistency, rather than relying only on burst-factor thresholds. Mills that still compete mainly on low-cost recycled output are under pressure to upgrade their specification control, because automated, fast-turn delivery systems are exposing weak formations and uneven compression performance more quickly than traditional retail channels did. This change is important for the India containerboard market because it is shifting demand toward technically dependable grades even within high-volume, price-sensitive packaging formats.

Food And Beverage Packaging Premiumization

India's food processing and beverage value chains are steadily tightening packaging specifications as organized retail, food safety requirements, and commitments to recyclable formats all move in the same direction. Brand owners such as Coca-Cola, PepsiCo, and Parle Agro have been aligning their packaging portfolios toward recyclable formats, thereby increasing the use of mono-material and fiber-based secondary packaging in organized distribution channels. Food processors are also reducing pack weights by moving liner grammages from 150 GSM toward 120 GSM while still trying to preserve compression performance through stronger fiber design and better board engineering. In April 2026, the Food Safety and Standards Authority of India issued a draft notification proposing paper, paperboard, cellulose, or other naturally derived materials for pan masala and tobacco packaging, extending the regulatory push for fiber-based formats into a category that had long relied on multi-layer plastic structures. That change matters because southern and western India already has high demand density for these product categories, so that any format migration can flow quickly into regional requirements for testliner and kraft grades. For the India containerboard market, this premiumization trend is raising the baseline expectation for print quality, compression consistency, and recyclability across food-linked corrugated packaging.

Wastepaper And Imported Fiber Price Volatility

India still relies on seaborne recovered fiber for a meaningful share of recycled-board furnish, and that dependence leaves many producers exposed to sudden cost swings in imported OCC and other feedstock streams. The risk is amplified by currency movement, because INR weakness can push landed costs higher even when dollar-denominated international fiber prices appear stable. This creates a widening gap between integrated players with captive pulp or plantation support and recycled-fiber mills that depend heavily on imported furnish and short procurement cycles. Smaller mills are especially vulnerable because they lack the financial flexibility to build inventory buffers when import conditions turn unfavorable, which can force abrupt production cuts or local price increases. The pressure also changes sourcing behavior, as mills seeking higher-purity recovered inputs compete more directly for premium grades rather than relying on mixed domestic scrap streams. For the India containerboard market, fiber volatility remains the most immediate profitability risk for producers that lack integration and scale.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push Toward Recyclable Fiber-Based Packaging

- Manufacturing And Export Logistics Expansion

- Power, Fuel, And Freight Cost Inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers accounted for 64.53% of the India containerboard market in 2025, reflecting the cost logic of a manufacturing base that still depends heavily on recovered fiber to remain competitive. India recycled 50% of used paper and boards, compared with 85% in developed economies, which shows that domestic recovery efficiency is still far below the level needed to fully support mill furnish needs. That gap affects both availability and quality, because weaker collection systems produce a more uneven domestic recovered-fiber stream and keep many mills dependent on imported OCC. Virgin fiber grades remained the smaller material segment, but they are projected to grow at a 6.02% CAGR through 2031, as brand premiumization and investment in import substitution support higher-performance kraftliner demand. The India containerboard market is therefore seeing a two-speed material transition, where recycled grades still dominate volume while virgin grades are becoming more attractive for applications that require higher compression strength, smoother surfaces, and greater consistency.

Virgin grades are also benefiting from trade action, as the Directorate General of Trade Remedies recommended anti-dumping duties of USD 152.27 per metric ton on Chinese virgin paperboard and USD 123.18 per metric ton on Chilean virgin paperboard, which could improve the economics for domestic mills if those measures hold. FSC certification and EPR compliance are becoming commercial entry requirements in the Indian containerboard industry, especially for FMCG and pharmaceutical exporters, who are now screening packaging suppliers more closely for traceability and sustainability credentials. Paswara Papers illustrates the balancing act within the segment, as it has shifted from a 60:40 kraft-to-kraftliner mix toward a more liner-led output profile while prioritizing high-quality DSOCC imports from the United States over mixed-grade recovered fiber. That move shows how even mid-tier producers are separating commodity recycled output from higher-specification grades, and it also suggests that demand for premium imported recovered fiber can remain firm even if there is only a slow improvement in lower-grade domestic collection.

List of Companies Covered in this Report:

- ITC Limited

- JK Paper Limited

- West Coast Paper Mills Limited

- Tamil Nadu Newsprint and Papers Limited

- Emami Paper Mills Limited

- B&B Triplewall Containers

- Pakka Limited

- N R Agarwal Industries Limited

- Khanna Paper Mills Limited

- Paswara Papers Limited

- Bell Multi Kraft Private Limited

- Laxmi Board and Paper Mills Private Limited

- Apollo Papers LLP

- Venkraft Paper Mills Private Limited

- Aryan Paper Mills Private Limited

- Ruchira Papers Limited

- Star Paper Mills Limited

- Shree Ajit Pulp and Paper Limited

- Caliber Papers LLP

- Gauranga Papers LLP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce and Quick-Commerce Corrugated Demand

- 4.2.2 Food and Beverage Packaging Premiumization

- 4.2.3 Regulatory Push Toward Recyclable Fiber-Based Packaging

- 4.2.4 Manufacturing and Export Logistics Expansion

- 4.2.5 Lightweighting and Strength Engineering for Automated Corrugation

- 4.2.6 Premium Kraftliner Import Substitution

- 4.3 Market Restraints

- 4.3.1 Wastepaper and Imported Fiber Price Volatility

- 4.3.2 Power, Fuel, and Freight Cost Inflation

- 4.3.3 Quality Variability in Domestic Recovered Fiber Streams

- 4.3.4 Post-2027 EU Waste Shipment Regulation Exposure

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ITC Limited

- 6.4.2 JK Paper Limited

- 6.4.3 West Coast Paper Mills Limited

- 6.4.4 Tamil Nadu Newsprint and Papers Limited

- 6.4.5 Emami Paper Mills Limited

- 6.4.6 B&B Triplewall Containers

- 6.4.7 Pakka Limited

- 6.4.8 N R Agarwal Industries Limited

- 6.4.9 Khanna Paper Mills Limited

- 6.4.10 Paswara Papers Limited

- 6.4.11 Bell Multi Kraft Private Limited

- 6.4.12 Laxmi Board and Paper Mills Private Limited

- 6.4.13 Apollo Papers LLP

- 6.4.14 Venkraft Paper Mills Private Limited

- 6.4.15 Aryan Paper Mills Private Limited

- 6.4.16 Ruchira Papers Limited

- 6.4.17 Star Paper Mills Limited

- 6.4.18 Shree Ajit Pulp and Paper Limited

- 6.4.19 Caliber Papers LLP

- 6.4.20 Gauranga Papers LLP

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)