|

市場調查報告書

商品編碼

2064385

義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)Italy Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

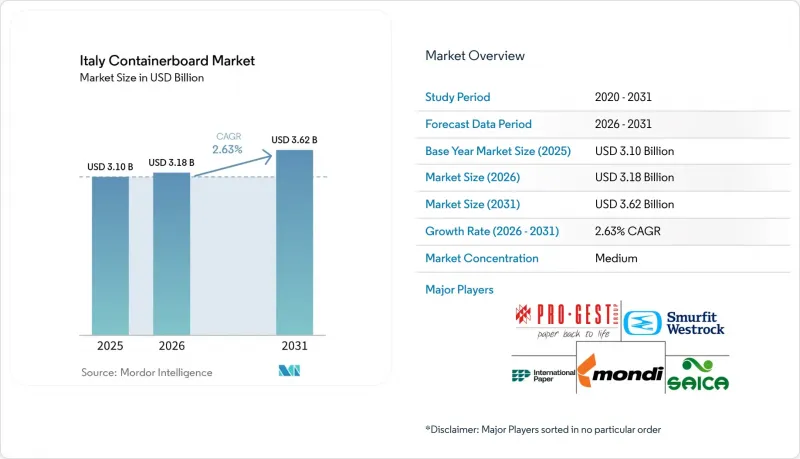

根據 Mordor Intelligence 預測,義大利瓦楞紙板市場預計將從 2025 年的 31 億美元成長到 2026 年的 31.8 億美元,到 2031 年達到 36.2 億美元,2026 年至 2031 年的複合年成長率為 2.63%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶行業(食品飲料、消費品、工業及其他)進行細分。市場預測以美元計價。

義大利箱板紙市場趨勢與洞察

電子商務和全通路策略推動了紙板需求成長。

隨著B2C電子商務在2025年持續擴張,以及所有產品類型的線上滲透率不斷提高,義大利瓦楞紙板市場正受益於小包裹的成長而穩步發展。預計到2025年,義大利B2C電子商務產品市場規模將達到400億歐元(451億美元),零售產品銷售的線上滲透率預計將從上一年的10.7%上升至11.2%。與托盤運輸相比,單件包裹的紙板用量每件增加30%至50%,導致紙板需求成長速度超過了產品基數本身的成長速度。此外,需求也在地理上不斷擴展,預計到2026年,義大利南部地區和島嶼成年人的線上使用率將達到60.6%,從而縮小與北部地區長期存在的數位落差。根據 2026 年初發布的一項調查,75% 的義大利消費者認為小包裹接收是他們與瓦楞紙板的主要實體接觸,這表明紙質配送在最後一公里零售中仍然發揮著核心作用。

二級包裝中以紙板取代塑膠

義大利箱板紙市場也受惠於二次包裝和運輸包裝領域塑膠用量普遍減少的趨勢。在那些對回收便利性和簡化逆向物流要求較高的地區,這一趨勢尤其顯著。根據2026年1月發布的一項調查,51%的義大利用戶企業已用瓦楞紙板取代了軟質塑膠,55%的消費者表示,在收到的包裹中,瓦楞紙板比氣泡膜或硬質塑膠組件更為常見。這項變更並非完全出於法規要求,因為瓦楞紙板包裝減輕了分類負擔,並且更容易融入廢紙回收流程。替代二次包裝通常需要更厚更堅固的紙板等級,這提高了測試襯墊和其他能夠承受更高負載的規格的價值。此外,政策環境也不斷改善,歐盟委員會的PPWR指南建立了一個建議易於回收包裝的框架,該指南將於2026年8月起在義大利實施。

電力和天然氣成本負擔加重

義大利箱板紙市場持續面臨能源成本帶來的結構性負擔,且壓力比其他歐洲主要造紙國更為嚴峻。義大利工業家聯合會(Confindustria)的報告預測,到2025年,義大利的工業用電價格將比歐盟平均高出約30%,高於德國、法國和西班牙。這對造紙廠而言是一個至關重要的問題,因為能源成本歷來佔義大利造紙生產營運成本的40%以上。此外,由於該產業95%以上的供熱需求依賴天然氣,生產商難以承受國內電力和燃料價格之間的巨大差距。業內相關人員在2025年初就警告稱,這種價格差距將威脅到整個供應鏈的競爭力,該供應鏈僱用了70萬名工人,並強調問題並非僅限於個別造紙廠。

細分市場分析

到2025年,再生纖維將佔義大利瓦楞紙板原紙市場佔有率的61.13%,這反映的是基礎設施的發展水平,而不僅僅是價格偏好。在義大利,再生紙佔造紙纖維成分的63%,使其成為繼德國之後歐洲第二大再生纖維消費國。這項供應基礎使義大利瓦楞紙板原紙市場在國內再生紙等級中保持強勁地位。這是因為義大利擁有成熟的國內收集和分類系統,可以取得充足的原料。蒙迪公司位於杜伊諾的工廠耗資2億歐元(約2.14億美元)的維修已於2025年4月竣工(將其年再生瓦楞紙板產能提升至42萬噸),這表明主要製造商認為義大利的再生纖維供應鏈足夠可靠,足以開展旗艦項目。

預計2026年至2031年間,原生紙漿的複合年成長率將達到2.94%,雖然起步較小,但將成為成長最快的原料基礎。在義大利瓦楞紙板市場,生鮮食品和高階消費品的出口商對瓦楞紙板的耐破強度、印刷性能和表面品質均勻性提出了更高的要求,而再生紙漿由於重量較輕,無法始終如一地滿足這些需求。此外,義大利仍然高度依賴進口原生牛皮紙,這表明該供應鏈環節的供不應求。認證標準似乎已經相當完善。到2024年,義大利造紙廠使用的原生纖維中,90%將獲得FSC或PEFC認證,將提高大規模買家採購流程的透明度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務和全通路策略推動了紙板需求成長。

- 二級包裝中以紙板取代塑膠

- 義大利再生纖維產量高、回收率高

- 食品飲料出口及對生鮮食品的物流需求

- PPWR 的發展正在促進可回收單一材料包裝的採用。

- 新回收生產能力運作後,減重的經濟可行性

- 市場限制因素

- 電力和天然氣成本負擔加重

- 再生紙價格和品質的波動

- 小規模轉換器中的PPWR合規性和文件成本

- 高性能進口牛皮紙襯墊的壓力

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 按最終用戶行業分類

- 食品/飲料

- 消費品

- 產業

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pro-Gest SpA

- Smurfit Westrock plc

- Mondi plc

- International Paper Italia Srl

- Sociedad Anonima Industrias Celulosa Aragonesa, SA

- VPK Group NV

- Progroup Board Srl

- Ghelfi Ondulati SpA

- Ondulati Santerno SpA

- LIC Packaging SpA

- Ondapack Sud SpA

- Box Marche SpA

- Sada SpA

- Antonio Sada & Figli SpA

- Burgo Group SpA

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy containerboard market size is expected to increase from USD 3.10 billion in 2025 to USD 3.18 billion in 2026 and reach USD 3.62 billion by 2031, growing at a CAGR of 2.63% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Containerboard Market Trends and Insights

E-Commerce and Omnichannel Corrugated Demand

The Italian containerboard market is receiving steady support from parcel growth, as B2C e-commerce continued to expand in 2025 and online penetration rose across product categories. Italy's B2C e-commerce product segment reached EUR 40 billion (USD 45.1 billion) in 2025, while online penetration of retail product sales rose to 11.2% from 10.7% in the prior year. Single-item shipment formats use 30% to 50% more board per unit than consolidated pallet formats, allowing board demand to rise faster than the merchandise base itself. Demand is also spreading geographically, as daily online use in southern regions and the islands reached 60.6% of adults in 2026, narrowing the long-standing digital divide with the north. Research presented in early 2026 also showed that 75% of Italian consumers viewed the parcel receipt as their primary physical point of contact with corrugated cardboard, keeping paper-based shipping formats central to last-mile retail.

Plastic-to-Paperboard Substitution in Secondary Packaging

The Italy containerboard market is also benefiting from a broader switch away from plastic in secondary and transit packaging, especially where easier recycling and simpler reverse logistics matter to buyers. Research released in January 2026 showed that 51% of Italian user companies had replaced flexible plastics with corrugated cardboard, while 55% of consumers said corrugated had become more common than bubble wrap and rigid plastic components in delivered packages. This change is not tied solely to regulation, because corrugated packaging also reduces sorting friction and fits more easily into the paper recycling stream after use. Secondary packaging substitution often requires heavier, stronger board grades that support value growth in testliner and other specifications that can handle higher stacking loads. The policy backdrop is becoming more favorable as well, as the European Commission's PPWR guidance establishes a framework that favors easily recyclable packaging and will apply in Italy from August 2026.

Elevated Electricity And Gas Cost Burden

The Italy containerboard market still faces a structural cost burden from energy, and that pressure is stronger than in the main competing paper-producing countries in Europe. Confindustria reported that Italian industrial electricity prices in 2025 were around 30% above the EU average and remained higher than those in Germany, France, and Spain. This matters deeply for paper mills because energy has historically accounted for more than 40% of operating costs in Italian paper production. The sector also depends on natural gas for more than 95% of its heat requirements, so producers cannot easily absorb wide differences in national power and fuel pricing. Industry representatives warned in early 2025 that this gap threatened competitiveness across a supply chain employing 700,000 workers, underscoring that the issue extends beyond individual mills.

Other drivers and restraints analyzed in the detailed report include:

- High Recovered Fiber Collection and Recovery Rates in Italy

- Food and Beverage Export and Fresh Produce Logistics Demand

- Recovered Paper Price And Quality Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 61.13% of Italy's containerboard market share in 2025, reflecting infrastructure depth more than simple price preference. Italy used recycled paper for 63% of its fiber mix in paper production, ranking second in Europe for total recovered fiber consumption after Germany. This supply base helps the Italy containerboard market keep a strong domestic position in recycled grades, because furnishes can be sourced through a mature national collection and sorting system. Mondi's EUR 200 million (USD 214 million) conversion of the Duino mill to 420,000 tonnes per year of recycled containerboard, completed in April 2025, showed that a major producer viewed the Italian recovered fiber chain as dependable enough for a flagship project.

Virgin fibers are forecast to grow at a CAGR of 2.94% between 2026 and 2031, which makes them the fastest-expanding material base, even from a smaller starting point. The Italy containerboard market is seeing this pull from exporters of fresh produce and premium consumer goods that need stronger burst performance, better printability, and a more uniform surface quality than recycled grades can consistently deliver at lighter weights. Italy also remained highly exposed to imported virgin kraft paper, indicating that this part of the supply chain still has a structural domestic gap. Certification standards already appear well established, because 90% of virgin fibers used in Italian mills carried FSC or PEFC certification in 2024, which supports procurement transparency for larger buyers.

List of Companies Covered in this Report:

- Pro-Gest S.p.A.

- Smurfit Westrock plc

- Mondi plc

- International Paper Italia S.r.l.

- Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- VPK Group NV

- Progroup Board S.r.l.

- Ghelfi Ondulati S.p.A.

- Ondulati Santerno S.p.A.

- LIC Packaging S.p.A.

- Ondapack Sud S.p.A.

- Box Marche S.p.A.

- Sada S.p.A.

- Antonio Sada & Figli S.p.A.

- Burgo Group S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce and Omnichannel Corrugated Demand

- 4.2.2 Plastic-to-Paperboard Substitution in Secondary Packaging

- 4.2.3 High Recovered Fiber Collection and Recovery Rates in Italy

- 4.2.4 Food and Beverage Export and Fresh Produce Logistics Demand

- 4.2.5 PPWR Readiness Favoring Recyclable Mono-Material Packs

- 4.2.6 Lightweighting Economics After New Recycled Capacity Start-Ups

- 4.3 Market Restraints

- 4.3.1 Elevated Electricity and Gas Cost Burden

- 4.3.2 Recovered Paper Price and Quality Volatility

- 4.3.3 PPWR Compliance and Documentation Costs for Smaller Converters

- 4.3.4 Imported Kraftliner Pressure in High-Performance Grades

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pro-Gest S.p.A.

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mondi plc

- 6.4.4 International Paper Italia S.r.l.

- 6.4.5 Sociedad Anonima Industrias Celulosa Aragonesa, S.A.

- 6.4.6 VPK Group NV

- 6.4.7 Progroup Board S.r.l.

- 6.4.8 Ghelfi Ondulati S.p.A.

- 6.4.9 Ondulati Santerno S.p.A.

- 6.4.10 LIC Packaging S.p.A.

- 6.4.11 Ondapack Sud S.p.A.

- 6.4.12 Box Marche S.p.A.

- 6.4.13 Sada S.p.A.

- 6.4.14 Antonio Sada & Figli S.p.A.

- 6.4.15 Burgo Group S.p.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)