|

市場調查報告書

商品編碼

2063922

南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)South America Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

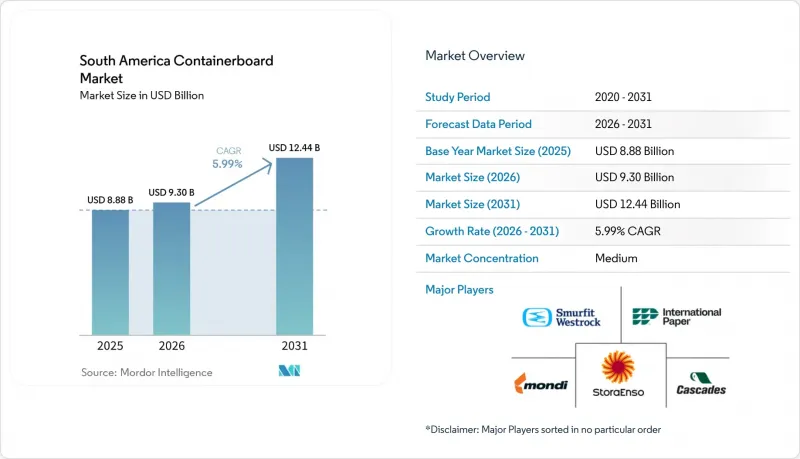

據 Mordor Intelligence 稱,2025 年南美箱板紙市值為 88.8 億美元,預計到 2031 年將達到 124.4 億美元,2026 年至 2031 年的複合年成長率為 5.99%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)、最終用戶(食品飲料、消費品、工業等)和地區(巴西、阿根廷、哥倫比亞、智利、秘魯及其他南美國家)進行細分。市場預測以美元計價。

南美瓦楞紙板原紙市場趨勢與洞察

電子商務的快速發展帶動了對瓦楞紙板包裝的需求。

在南美箱板紙市場,電子商務的興起正在縮小線上零售成長與包裝材料投資之間傳統的差距。 2026年1月,巴西瓦楞紙板出貨量達到創紀錄的34.3萬噸,較去年同期成長2.3%,顯示自年初以來紙箱需求強勁。動物性蛋白質和消費品佔巴西瓦楞紙板總需求的30%,與零售和履約通路相關的生產商訂單依然活躍。退貨物流也在改變設計重點,因為托運人要求使用更輕的瓦楞紙箱,同時提高二次包裝的品質以適應重複搬運。投資於輕質瓦楞和可印刷面的製造商能夠獲得小批量、高利潤的訂單,而傳統的牛皮紙工廠在訂單時間方面無法滿足這些訂單的需求。 Fastmarkets先前已預測,2024年巴西瓦楞紙箱出貨量將成長5%。因此,南美洲貨櫃紙板市場在2026年開始就擁有穩固的業務基礎,而非經歷疲軟的復甦週期。

農產品出口激增,對結實的瓦楞紙箱需求量大。

南美洲的箱板紙市場正受惠於農產品出口,因為這些價值鏈需要更堅固、防潮且適用於低溫運輸運輸的瓦楞紙板。預計到2025年,巴西的農產品出口將達到創紀錄的1,692億美元,其中牛肉出口額將增加39.9%,出口量將增加20.4%。這進一步推動了長途蛋白質貿易中對重型瓦楞紙箱的需求。通往中國、歐盟和中東的貿易路線增加了運輸距離和裝卸負擔,從而提高了每批貨物的包裝要求。預計秘魯將在2025年創下農產品出口新紀錄,向115個市場出口540種產品,其中包括767,230噸酪梨和343,537噸藍莓,這將使生鮮食品盒的需求持續成長。預計智利2025年新鮮蔬果出口量也將創歷史新高,包裝在多模態低溫運輸運輸中日益成為北美和歐洲零售商的競爭利器。由於出口計畫與長期貿易流和認證要求密切相關,南美箱板紙市場主要依靠農業部門而非國內消費品需求來獲得更穩定的支撐。

再生紙價格波動給利潤率帶來了壓力。

再生紙價格波動仍然是南美箱板紙市場最明顯的成本風險之一,尤其對於那些依賴再生纖維且無法改用原生原料的生產商而言更是如此。 2024年第三季度,隨著加工商為水果出口季確保供應,全部區域恢復了舊報紙(OCC)的進口,加上該地貨幣對美元貶值,價格指數飆升。該地區大部分地區的國內回收率仍處於結構性低位,因此本地再生纖維供應無法迅速滿足加工商不斷成長的需求。在巴西的軟塑膠產業,再生材料的使用量僅為2026年目標的5%,這顯示回收和再利用系統存在普遍的脆弱性,並減少了供應給造紙業的清潔原料數量。因此,再生纖維生產商面臨雙重壓力:進口再生紙(OCC)價格飆升,而國內回收的品質也在下降。在南美瓦楞紙板市場,這種成本壓力對測試襯紙和再生瓦楞纖維的供應商來說是一個嚴重的問題,因為瓦楞紙板製造商要求即使在纖維原料供應不穩定的情況下,價格也要保持穩定。

細分市場分析

2025年,再生纖維在南美箱板紙市場佔有64.35%的佔有率。這得益於完善的回收網路以及測試襯紙和再生纖維瓦楞紙板在國內製作流程中的成本效益。南美箱板紙市場長期以來一直依賴來自工業和商業通路的再生紙。這一趨勢在聖保羅大都會圈和庫里蒂巴地區尤為顯著,這些地區的一體化供應鏈已經影響了採購和生產方式。南方共同市場第02/25號決議於2025年修訂了纖維素食品接觸材料的技術要求,要求在再生纖維產品中盡可能減少二異丙基萘(DIPN)的含量,從而在採購決策中更加重視食品安全問題。這項變更促使一些食品接觸包裝材料的採購商更加關注再生材料的含量,尤其是在出口認證和產品接觸法規日益嚴格的情況下。

原生纖維雖然仍是相對較小的材料類別,但卻是南美箱板紙市場成長最快的細分市場,預計到2031年複合年成長率將達到6.61%。在南美箱板紙產業,這一成長與對用於農產品出口包裝和紙箱的高品質牛皮紙襯紙的需求不斷成長密切相關,這些包裝和紙箱必須能夠承受潮濕和裝載壓力。 Cravin位於奧爾蒂蓋拉的工廠生產「Yuka Liner」襯紙,其27號和28號造紙機合計年產能超過90萬噸,在高性能襯紙領域佔據了穩固的地位。因此,南美瓦楞紙板原紙產業的材料選擇正從單純的成本競爭轉向對合規性、強度和表面品質要求的全面考量,優質原生纖維襯紙正成為某些終端應用的首選。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務的快速發展正在推動對瓦楞紙板包裝的需求。

- 農產品出口的快速成長需要堅固的包裝箱。

- 從塑膠包裝到纖維包裝的轉變正在推進。

- 國內主要造紙和紙漿生產企業擴大產能。

- 政府提高進口二手瓦楞紙箱關稅

- 數位印刷技術的引進使得小批量印刷獲得高利潤成為可能。

- 市場限制因素

- 再生紙價格波動劇烈,對利潤率帶來了壓力。

- 多式聯運物流基礎設施有限

- 貨幣貶值導致個人消費放緩

- 影響紙漿廠的用水限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 最終用戶

- 食品/飲料

- 消費品

- 產業

- 其他最終用戶

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- Klabin SA

- Mondi plc

- International Paper Company

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Stora Enso Oyj

- Sappi Limited

- Georgia-Pacific LLC

- Irani Papel e Embalagem SA

- Packaging Corporation of America

- Cascades Inc.

- Pratt Industries, Inc.

- Bio Pappel SAB de CV

- Empresa CMPC SA

- Celulosa Arauco y Constitucion SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america containerboard market was valued at USD 8.88 billion in 2025 and is projected to reach USD 12.44 billion by 2031, expanding at a CAGR of 5.99% during 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Containerboard Market Trends and Insights

E-Commerce Boom Fueling Corrugated Packaging Demand

The South America containerboard market is seeing e-commerce compress the old gap between online retail growth and packaging conversion investment. Brazil opened 2026 with record corrugated board shipments of 343,000 tonnes in January, up 2.3% year over year, which showed that box demand remained firm at the start of the year. Animal protein and fast-moving consumer goods accounted for 30% of total corrugated demand in Brazil, keeping order flow active for producers tied to retail and fulfillment channels. Returns logistics is also changing design priorities, because shippers now want lighter boxes while still upgrading secondary packaging quality for repeat handling. Producers that invested in lightweight fluting and printable liner surfaces have been better placed to capture short-run, higher-margin work that standard kraft-focused mills struggle to match on turnaround time. Fastmarkets had already projected 5% full-year growth in corrugated box shipments in Brazil for 2024, so the South America containerboard market entered 2026 on top of a firm operating base rather than a weak rebound cycle.

Surging Agricultural Exports Requiring Robust Boxes

The South America containerboard market is benefiting from export agriculture, as these supply chains require stronger, moisture-resistant, and cold-chain-ready corrugated formats. Brazil's agribusiness exports reached a record USD 169.2 billion in 2025, and beef export value rose 39.9% while volume increased 20.4%, which reinforced demand for heavyweight corrugated boxes in long-distance protein trade. Those trade corridors to China, the European Union, and the Middle East stretch transport distance and handling intensity, which raises packaging requirements per shipment. Peru set a historic agricultural export record in 2025, shipping 540 products to 115 markets, including 767,230 tonnes of avocados and 343,537 tonnes of blueberries, keeping fresh-produce box demand on an upward trajectory. Chile also posted record fresh fruit and vegetable export revenue in 2025, and packaging is increasingly being used as a competitive tool in multimodal cold-chain movement to North American and European retailers. This is why the South America containerboard market is drawing support from agriculture in a steadier way than domestic fast-moving consumer goods demand, because export programs are tied to long-running trade flows and certification requirements.

Volatile Recovered Paper Prices Pressuring Margins

Recovered paper volatility remains one of the clearest cost risks in the South America containerboard market, especially for producers that rely on recycled fiber and cannot switch their mix toward virgin inputs. OCC imports resumed across the region in the third quarter of 2024 as converters secured supply for fruit export seasons, and price indices rose sharply as local currencies weakened against the USD. Domestic collection rates remain structurally low across much of the region, so local recovered fiber supply does not respond quickly when converter demand rises. Brazil's flexible plastic packaging sector was operating with only 5% recycled content, against a 2026 target of 22%, indicating broader weaknesses in collection and recovery systems and leaving less clean material available for the paper circuit. That leaves recycled-fiber producers exposed to a two-sided squeeze, because imported OCC becomes more expensive while domestic recovery quality also weakens. In the South America containerboard market, this cost pressure matters most for testliner and recycled-fluting suppliers, who are being asked by box makers to hold pricing steady while fiber inputs remain unstable.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Substitution of Plastic with Fiber-Based Packaging

- Capacity Expansions by Domestic Pulp and Paper Majors

- Limited Intermodal Logistics Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 64.35% of the South America containerboard market share in 2025, supported by integrated recovery networks and the cost efficiency of testliner and recycled-fiber fluting in domestic conversion. The South America containerboard market has long depended on recovered paper from industrial and commercial generators, especially in the Greater Sao Paulo and Curitiba belts, where integrated circuits have shaped procurement and production routines. MERCOSUR Resolution No. 02/25 updated technical requirements for cellulosic food-contact materials in 2025 and called for recycled-fiber articles to keep diisopropylnaphthalene, or DIPN, as low as technically feasible, which added a stronger food-safety dimension to sourcing decisions. That change is prompting some food-contact packaging buyers to scrutinize recycled content, particularly as export certifications and product-contact rules tighten.

Virgin fibers remain the smaller material category, but they are the fastest-growing segment with a 6.61% CAGR through 2031 in the South America containerboard market. Within the South America containerboard industry, this growth is tied to rising demand for premium kraft-grade liners for agricultural export packaging and boxes that must withstand moisture and stacking stress. Klabin's Ortigueira unit produces Eukaliner and has installed capacity above 900,000 tonnes per year across Paper Machines 27 and 28, giving it a strong position in higher-performance liner grades. Material choice in the South America containerboard industry is therefore moving away from a simple cost debate and toward a mix of compliance, strength, and surface quality requirements that favor premium virgin grades in selected end uses.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Klabin S.A.

- Mondi plc

- International Paper Company

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Stora Enso Oyj

- Sappi Limited

- Georgia-Pacific LLC

- Irani Papel e Embalagem S.A.

- Packaging Corporation of America

- Cascades Inc.

- Pratt Industries, Inc.

- Bio Pappel S.A.B. de C.V.

- Empresa CMPC S.A.

- Celulosa Arauco y Constitucion S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Boom Fueling Corrugated Packaging Demand

- 4.2.2 Surging Agricultural Exports Requiring Robust Boxes

- 4.2.3 Increasing Substitution of Plastic with Fiber-Based Packaging

- 4.2.4 Capacity Expansions by Domestic Pulp and Paper Majors

- 4.2.5 Rising Government Tariffs on Imported Old Corrugated Containers

- 4.2.6 Digital Print Adoption Enabling High-Margin Short Runs

- 4.3 Market Restraints

- 4.3.1 Volatile Recovered Paper Prices Pressuring Margins

- 4.3.2 Limited Intermodal Logistics Infrastructure

- 4.3.3 Slowdown in Consumer Spending Amid Currency Depreciation

- 4.3.4 Water-Use Restrictions Affecting Pulp Mills

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Colombia

- 5.4.4 Chile

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Klabin S.A.

- 6.4.3 Mondi plc

- 6.4.4 International Paper Company

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Stora Enso Oyj

- 6.4.8 Sappi Limited

- 6.4.9 Georgia-Pacific LLC

- 6.4.10 Irani Papel e Embalagem S.A.

- 6.4.11 Packaging Corporation of America

- 6.4.12 Cascades Inc.

- 6.4.13 Pratt Industries, Inc.

- 6.4.14 Bio Pappel S.A.B. de C.V.

- 6.4.15 Empresa CMPC S.A.

- 6.4.16 Celulosa Arauco y Constitucion S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)