|

市場調查報告書

商品編碼

2063919

歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Europe Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

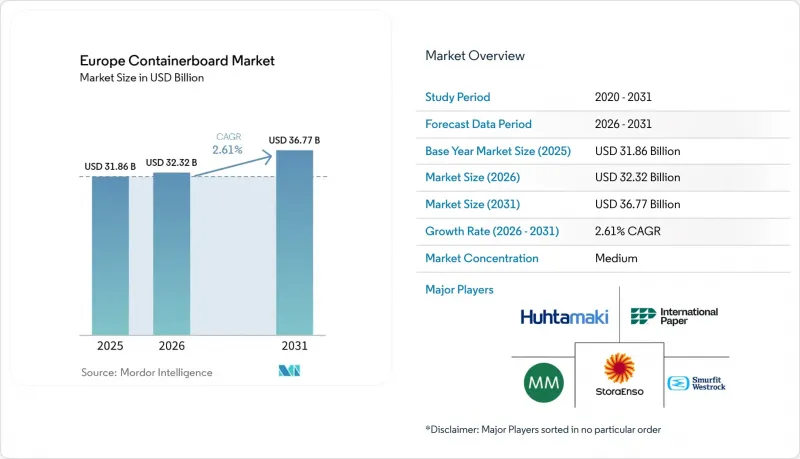

根據 Mordor Intelligence 預測,歐洲瓦楞紙板市場規模預計將在 2025 年達到 318.6 億美元,2026 年達到 323.2 億美元,2031 年達到 367.7 億美元,2026 年至 2031 年的複合年成長率為 2.61%。

本報告按材料(原生纖維和再生纖維)、類型(工藝襯墊、測試襯墊、瓦楞紙板)、最終用戶(食品飲料、消費品、工業等)和地區(德國、法國、義大利、西班牙、英國、俄羅斯及其他歐洲國家)進行細分。市場預測以美元計價。

歐洲瓦楞紙板原紙市場趨勢與洞察

電子商務和線上零售的成長

電子商務持續為歐洲箱板紙市場提供強勁支撐,反映出與先前的疫情高峰相比,物流週期更加穩定。隨著線上零售商對包裝盒的需求日益成長,不再局限於傳統的棕色紙箱,而是更加注重尺寸合適的包裝盒、更高的承載能力以及對數位印刷的適應性,市場需求模式也在改變。這項轉變意義重大,因為它不僅影響出貨量,還會影響纖維成分和紙板規格。在德國,這種影響已經顯現。儘管2024年運輸包裝僅佔瓦楞紙板銷售額的6.7%,但其對品質標準的影響遠不止於此。 2026年初,許多製造商的出貨量都優於預期,證實了主要市場庫存補充和包裝材料更新換代週期的活躍度。因此,歐洲箱板紙市場正經歷著對輕量高性能紙板組合的需求轉變,這種組合既能提高運輸效率,又能提升品牌形象。

嚴格的永續發展法規鼓勵使用可回收包裝。

法規是歐洲箱板紙市場需求最顯著的促進因素之一。這是因為《包裝和包裝材料法規》(PPWR)將於2025年2月11日生效,並於2026年8月12日廣泛實施。該法規要求到2030年,所有進入歐盟市場的包裝都必須可回收利用,並引入了一套可回收性框架,這將影響各個產品類型的包裝選擇。這將為纖維包裝形式帶來直接的商業性優勢,因為與許多混合材料包裝相比,纖維包裝更適合現有的收集和分類系統。義大利在這方面展現出了良好的準備,其瓦楞紙包裝的回收率在2024年達到了92.5%,已經超過了歐盟2030年85%的目標。德國的紙張回收率也持續維持在90%以上,進一步鞏固了再生瓦楞紙板在全部區域的結構性重要性。因此,歐洲瓦楞紙板市場不僅受益於永續發展訊息,也受惠於法規結構,這些框架越來越重視旨在實現高回收率和優異分揀效果的包裝形式。

紙張回收率和價格波動

再生紙價格的波動仍然是歐洲瓦楞紙板原紙市場面臨的最緊迫的商業風險,尤其是對於完全依賴再生纖維的造紙廠。 2025年4月,由於回收量下降和出口競爭導致供應緊張,歐洲1.04級和1.05級瓦楞紙板(OCC)的價格上漲了每噸20-30歐元(22-33美元)。這種壓力不容忽視,因為儘管相關法規正在推動對再生纖維的需求,但消費活動的放緩或出口需求的改善都可能加劇原料供應緊張。這種供需不匹配給再生瓦楞紙板生產商帶來了嚴峻的利潤挑戰,因為原料成本的上漲並不一定會直接轉嫁到紙板價格上。這也解釋了為什麼一些中型企業正在尋求收回資產並確保長期穩定的原料供應管道,而不是僅僅依賴從公開市場購買再生紙(OCC)。因此,歐洲瓦楞紙板市場面臨著一個反覆出現的矛盾:雖然循環經濟目標支撐了需求,但再生纖維的經濟可行性仍然限制了滿足這種需求的盈利。

細分市場分析

到2025年,再生纖維將佔歐洲瓦楞紙板市場的62.83%。這反映了該地區成熟的有機瓦楞紙板(OCC)回收體系、循環經濟的政策激勵措施,以及在原料供應穩定的情況下維持再生等級的成本優勢。德國瓦楞紙板產業在2024年超過81.8%的紙張原料來自再生纖維,進一步鞏固了其主導地位。再生纖維基礎支撐著現有的回收基礎設施和品牌所有者的永續發展目標,並與歐盟包裝政策的方向高度契合。然而,各地區的情況並不相同,義大利仍然嚴重依賴高品質的原生等級瓦楞紙板用於食品接觸和出口應用。這種差異意義重大,因為它顯示歐洲箱板紙市場轉型為再生材料的速度並不相同,各國在性能權衡方面也存在差異。

原生纖維目前仍佔市場佔有率較小,但預計到2031年將以3.62%的複合年成長率成長,因為加工商和品牌所有者對潮濕敏感應用、出口應用和食品級應用的性能保證要求不斷提高。強度並非唯一考慮因素;純度、阻隔性相容性和加工一致性也至關重要,因為再生材料的品質往往因批次而異。正因如此,儘管法規持續支持循環利用材料,但在歐洲瓦楞紙板產業的某些領域,以再生材料取代再生材料仍存在實際限制。這也解釋了為什麼製造商即使產品缺陷成本超過不斷上漲的纖維成本,仍繼續投資於優質牛皮紙襯紙和混合解決方案。因此,雖然再生材料在歐洲瓦楞紙板市場將持續成長,但在那些優先考慮可靠性而非降低原料成本的領域,原生纖維等級和高性能等級預計也將持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務和線上零售的成長

- 嚴格的永續發展法規鼓勵使用可回收包裝。

- 零售連鎖店對預包裝商品的需求日益成長。

- 從塑膠包裝到紙質包裝的轉變正在推進。

- 不斷擴大的跨國水果出口路線需要防潮貨櫃紙板。

- 在貨櫃紙板上引入數位浮水印技術,以提高分類效率。

- 市場限制因素

- 廢紙的回收率和價格波動

- 歐洲造紙廠能源成本飆升

- 來自輕質微槽實心板的競爭日益激烈

- 妥爾油松香的潛在供應短缺可能會影響新船襯裡中使用強度添加劑。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 最終用戶

- 食品/飲料

- 消費品

- 產業

- 其他最終用戶

- 按地區

- 德國

- 法國

- 義大利

- 西班牙

- 英國

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- International Paper Company

- Mondi plc

- Stora Enso Oyj

- Holmen AB

- Svenska Cellulosa AB SCA

- Metsa Board Oyj

- Klingele Paper & Packaging Group

- Pro-Gest SpA

- Hamburger Containerboard

- VPK Packaging Group NV

- LEIPA Group GmbH

- SAICA Group

- Reno de Medici SpA

- Burgo Group SpA

- Cartiera del Chiese SpA

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the european containerboard market is projected to reach USD 31.86 billion in 2025, USD 32.32 billion in 2026, and USD 36.77 billion by 2031, growing at a CAGR of 2.61% from 2026 to 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Germany, France, Italy, Spain, United Kingdom, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe Containerboard Market Trends and Insights

Growth in E-Commerce and Online Retail

E-commerce continues to provide durable support for the Europe containerboard market, even though the pace now reflects a steadier logistics cycle rather than the earlier pandemic spike. The demand pattern is also changing because online retailers increasingly want right-sized boxes, stronger stacking performance, and better digital print-readiness rather than standard brown transit cases. That shift is important because it changes fiber mix and board specification, not only shipment volume. Germany already shows how this influence works in practice, with shipping packaging accounting for 6.7% of corrugated board revenue in 2024, even though its effect on quality standards extends well beyond that share. Early 2026 also opened with a better volume trend than many producers expected, which supports a more active restocking and packaging-conversion cycle in key markets. As a result, the Europe containerboard market is seeing demand shift toward lighter yet more capable board combinations that balance transport efficiency and brand presentation.

Stringent Sustainability Regulations Favoring Recyclable Packaging

Regulation is one of the clearest demand shapers for the Europe containerboard market, as the PPWR entered into force on February 11, 2025, and is scheduled to be broadly applied from August 12, 2026. The regulation requires all packaging placed on the EU market to be recyclable by 2030 and introduces a recyclability performance framework that will influence packaging choices across product categories. This creates a direct commercial advantage for fiber-based formats that already fit established collection and sorting systems better than many mixed-material packs. Italy provides a useful signal of readiness, as corrugated packaging recycling reached 92.5% in 2024, already above the EU's 2030 target of 85%. Germany also continued to report paper recovery rates above 90%, reinforcing the structural importance of recycled containerboard across the region. The Europe containerboard market therefore benefits not only from sustainability messaging, but also from a regulatory framework that increasingly rewards pack formats designed for high recovery and strong sorting outcomes.

Volatility in Wastepaper Collection Rates and Prices

Recovered-paper volatility remains the most immediate operating risk for the Europe containerboard market, especially for mills that rely fully on recycled fiber. In April 2025, OCC grades 1.04 and 1.05 rose by EUR 20-30 per ton (USD 22-33 per ton) across Europe as collection volumes weakened and export competition tightened supply. This pressure matters because recycled-fiber demand is being lifted by regulation at the same time that the feedstock base can tighten when consumer activity softens, or export demand improves. That mismatch creates a difficult margin structure for recycled containerboard producers, as higher raw-material costs do not always cleanly pass through to board pricing. It also explains why some mid-tier groups are seeking to secure asset collections and long-term feedstock channels rather than relying solely on open-market OCC purchases. The Europe containerboard market, therefore, faces a recurring tension in which circular-economy targets support demand, but the economics of collected fiber can still limit how profitably that demand is served.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Shelf-Ready Packaging in Retail Chains

- Increasing Substitution of Plastic with Paper-Based Packaging

- High Energy Costs in Europe's Paper Mills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 62.83% of the Europe containerboard market share in 2025, reflecting the region's mature OCC collection systems, the policy premium on circularity, and the cost advantage recycled grades can retain when input conditions are stable. This leadership position is reinforced by the fact that Germany's corrugated board sector sourced more than 81.8% of its paper input from recycled fiber in 2024. The recycled-fiber base also aligns well with the direction of EU packaging policy, as it supports established recovery infrastructure and brand-owner sustainability targets. At the same time, the regional picture is not uniform, as Italy still relies heavily on higher-quality virgin grades for food-contact and export-oriented applications. That unevenness is important because it shows that the Europe containerboard market is not moving toward recycled content at the same pace or with the same performance trade-offs in every country.

Virgin fibers remain the smaller material segment, but they are forecast to grow at a 3.62% CAGR through 2031, as converters and brand owners still need performance certainty in moisture-sensitive, export, and food-grade applications. The issue is not only strength, because purity, barrier compatibility, and process consistency also matter where recycled input quality can vary from batch to batch. This creates a practical ceiling for recycled substitution in parts of the Europe containerboard industry, even as regulation continues to favor circular content. It also explains why producers continue to invest in premium kraftliner and hybrid solutions, even when product failure is more costly than a higher fiber bill. The Europe containerboard market will therefore keep a large recycled base, but growth in virgin-backed and performance-led grades will continue where reliability matters more than the lowest possible raw-material cost.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- International Paper Company

- Mondi plc

- Stora Enso Oyj

- Holmen AB

- Svenska Cellulosa AB SCA

- Metsa Board Oyj

- Klingele Paper & Packaging Group

- Pro-Gest S.p.A.

- Hamburger Containerboard

- VPK Packaging Group NV

- LEIPA Group GmbH

- SAICA Group

- Reno de Medici S.p.A.

- Burgo Group S.p.A.

- Cartiera del Chiese S.p.A.

- Huhtamaki Oyj

- Mayr-Melnhof Karton AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in E-Commerce and Online Retail

- 4.2.2 Stringent Sustainability Regulations Favoring Recyclable Packaging

- 4.2.3 Rising Demand for Shelf-Ready Packaging in Retail Chains

- 4.2.4 Increasing Substitution of Plastic with Paper-Based Packaging

- 4.2.5 Expanding Cross-Border Fruit Export Corridors Requiring Humidity-Resistant Containerboard

- 4.2.6 Adoption of Digital Watermarking in Containerboard for Enhanced Sortation

- 4.3 Market Restraints

- 4.3.1 Volatility in Waste Paper Collection Rates and Prices

- 4.3.2 High Energy Costs in Europe's Paper Mills

- 4.3.3 Growing Competition from Lightweight Microflute Solid Board

- 4.3.4 Potential Supply Squeeze of Tall Oil Rosin Affecting Virgin Kraftliner Strength Additives

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 Italy

- 5.4.4 Spain

- 5.4.5 United Kingdom

- 5.4.6 Russia

- 5.4.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 International Paper Company

- 6.4.3 Mondi plc

- 6.4.4 Stora Enso Oyj

- 6.4.5 Holmen AB

- 6.4.6 Svenska Cellulosa AB SCA

- 6.4.7 Metsa Board Oyj

- 6.4.8 Klingele Paper & Packaging Group

- 6.4.9 Pro-Gest S.p.A.

- 6.4.10 Hamburger Containerboard

- 6.4.11 VPK Packaging Group NV

- 6.4.12 LEIPA Group GmbH

- 6.4.13 SAICA Group

- 6.4.14 Reno de Medici S.p.A.

- 6.4.15 Burgo Group S.p.A.

- 6.4.16 Cartiera del Chiese S.p.A.

- 6.4.17 Huhtamaki Oyj

- 6.4.18 Mayr-Melnhof Karton AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)