|

市場調查報告書

商品編碼

2063878

中東和非洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East And Africa Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

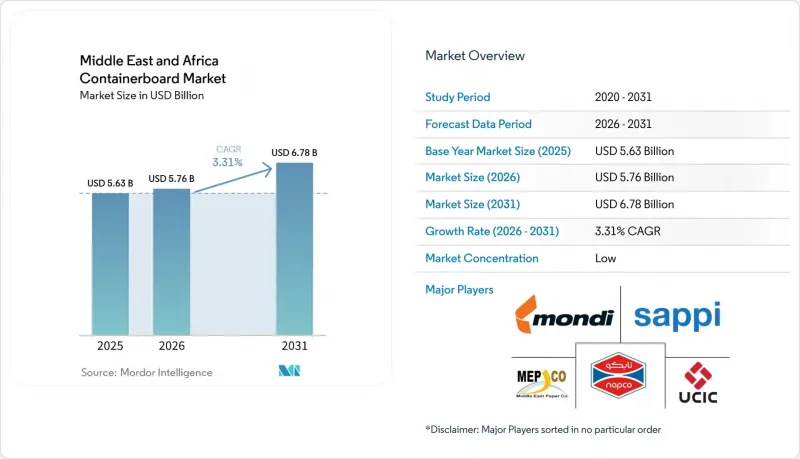

根據 Mordor Intelligence 預測,中東和非洲瓦楞紙板原紙市場規模將從 2025 年的 56.3 億美元和 2026 年的 57.6 億美元成長到 2031 年的 67.8 億美元,2026 年至 2031 年的複合年成長率為 3.31%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯紙、測試襯紙、瓦楞紙)、最終用戶(食品飲料、消費品、工業等)和地區(沙烏地阿拉伯、阿拉伯聯合大公國、土耳其、其他中東國家、南非、埃及、奈及利亞和其他非洲國家)進行細分。市場預測以美元計價。

中東和非洲箱板紙市場趨勢與洞察

電子商務和全通路小包裹的成長

線上零售正以遠超一般生產指標的速度改變海灣合作理事會(GCC)國家的瓦楞紙板需求,中東和非洲的箱板紙市場正明顯轉向以履約為主導的包裝需求。沙烏地阿拉伯非石油私部門採購經理人指數(PMI)預計在2025年的大部分時間裡將保持在53以上,顯示商業和物流行業持續活躍,而這些行業通常會消耗大量的瓦楞紙板包裝。小包裹設計方面的變化更為顯著,沙烏地阿拉伯和阿拉伯聯合大公國的電商營運商需要尺寸合適的模切瓦楞紙板,以減少最後一公里配送的體積重量。這項需求同時也推動了對輕質瓦楞材料和高強度測試襯紙的需求,這也是中東和非洲箱板紙市場對瓦楞材料的需求成長速度快於成熟等級瓦楞紙板的原因之一。由於瓦楞紙板生產商的營運資金緊張,小包裹需求轉化為實際紙板採購的速度可能會放緩。因此,能夠在服務、柔軟性和信用條款方面為客戶提供支援的造紙企業,更有利於維持其市場佔有率。

食品宅配及生鮮食品出口活性化

生鮮食品的出口對高性能瓦楞紙板托盤和紙箱的需求集中且持續,使農業包裝成為中東和非洲瓦楞紙板市場需求最強勁的領域之一。南非柑橘和核果的出口高峰期在2月至7月,這帶動了對包裝材料的穩定需求,這些包裝材料既能保護農產品在長途運輸過程中不受損壞,又能滿足歐盟的植物檢疫和食品接觸要求。 Sappi公司報告稱,2025年包裝紙和特種紙的銷售量將年增8%,其中箱板紙需求的成長主要得益於柑橘豐收。 MPact公司也報告稱,箱板紙和農業包裝材料的銷售額強勁成長,並指出由於出口導向成長,農業領域具有結構性吸引力。由於這些造紙廠的生產週期與北半球的零售和收穫日曆以及國內週期相一致,中東和非洲的箱板紙市場受益於與出口相關的食品包裝,而這種包裝需求並不完全依賴於當地消費者的意願。

進口OCC、紙漿和牛皮紙襯裡的價格波動。

在中東和非洲的箱板紙市場,原料風險仍是最明顯的阻礙因素。這是因為該地區國內原生木漿供應有限,仍然嚴重依賴進口的再生紙(OCC)和牛皮紙襯紙。 2025年,隨著主要區域公司出貨量的增加,這項風險變得更加明顯,但不斷上漲的再生紙成本擠壓了利潤運作。根據MPact的數據顯示,儘管2025年上半年瓦楞紙板銷量成長了20.3%,但由於再生紙價格大幅上漲,導致息稅折舊攤提前利潤(EBITDA)下降了14.5%。這種反饋循環至關重要,因為雖然新建再生紙生產設施將改善當地的紙板供應,但對同一再生紙(OCC)來源的競爭將加劇,這可能會再次推高原料價格。簡而言之,中東和非洲的瓦楞紙板原紙市場正受惠於國內規模的擴大,但仍在努力將這種規模轉化為穩定的利潤成長。

細分市場分析

預計到2025年,再生纖維將佔中東和非洲箱板紙市場佔有率的53.7%,這反映出在纖維短缺的環境下,該地區對以OCC為基礎的測試襯紙和瓦楞紙板的依賴程度很高。沙烏地阿拉伯、阿拉伯聯合大公國和科威特的生產結構進一步強化了再生紙的主導地位,這些國家的箱板紙產能主要集中在再生纖維而非原生紙漿上。成本控制和永續性要求共同推動了這一趨勢,使得買家通常認為再生紙在供應和經濟性方面是最現實的選擇。這也解釋了為什麼即使進口OCC的價格波動性增加,中東和非洲箱板紙市場仍依賴再生纖維。

預計到2031年,原生紙漿的年複合成長率將達到4.4%,而這加速成長反映的是品質溢價,而非對再生紙漿的普遍摒棄。蒙迪位於義大利杜伊諾的工廠已將其再生瓦楞紙板的年產能提高了42萬噸。此舉旨在供應歐洲客戶和國際市場,特別是中東和非洲的瓦楞紙板市場,顯示來自資金雄厚的出口商的競爭壓力仍然存在。由於再生材料無法在大規模生產中保持穩定的性能,原生紙漿基箱板紙仍然是食品接觸應用、對耐破強度要求較高應用以及藥品包裝的首選。此外,跨國客戶越來越重視監管鍊和認證標準,這導致一些區域性再生纖維供應商面臨規格方面的挑戰。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務和全通路小包裹市場的成長

- 生鮮食品的配送和出口強度

- EPR作為塑膠替代品在包裝領域的進展

- 輕質低紙張重量板材的升級

- 非洲大陸自由貿易區對加強運輸包裝的需求

- 數位印刷技術的引進使得小批量印刷獲得高利潤成為可能。

- 市場限制因素

- 進口再生紙(OCC)、紙漿和牛皮紙襯裡的價格波動。

- 水資源短缺及工廠廢水排放限制

- 紅海和波斯灣航運中斷造成的成本衝擊

- 影響紙漿廠的用水限制

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 最終用戶

- 食品/飲料

- 消費品

- 產業

- 其他最終用戶

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Mondi plc

- Mpact Limited

- Middle East Paper Company

- Arab Paper Manufacturing Company

- Sappi Limited

- United Carton Industries Company

- Arabian Packaging Co. LLC

- Industrial Development Company sal

- Napco National CJSC

- Obeikan Investment Group

- Gulf Paper Manufacturing Company KSC

- Omani Packaging Company SAOG

- Queenex Corrugated Carton Factory

- RAK Packaging Company Ltd.

- UNIPAKNILE Ltd.

- Cairo Egyptian Packaging and Containers

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa containerboard market size is projected to expand from USD 5.63 billion in 2025 and USD 5.76 billion in 2026 to USD 6.78 billion by 2031, registering a CAGR of 3.31% between 2026 and 2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), End User (Food and Beverage, Consumer Goods, Industrial, and More), and Geography (Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East, South Africa, Egypt, Nigeria, and Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Containerboard Market Trends and Insights

E-Commerce and Omnichannel Parcel Growth

Online retail is changing corrugated demand in the GCC faster than broader output indicators would usually suggest, and the Middle East and Africa containerboard market is now seeing a clearer shift toward fulfillment-driven packaging demand. Saudi Arabia's non-oil private sector PMI remained above 53 for most of 2025, indicating sustained activity in commerce and logistics, which typically consume large volumes of corrugated packaging. The more meaningful change is in parcel design, because e-commerce operators in Saudi Arabia and the UAE are requesting right-sized, die-cut corrugated formats that reduce cubic weight for last-mile deliveries. That requirement is lifting demand for lightweight fluting media and stronger testliners simultaneously, which is one reason the Middle East and Africa containerboard market is showing faster momentum in flutings than in more mature grades. Working capital pressure among corrugators has at times slowed the conversion of parcel demand into actual board offtake, so mills that can support customers on service, flexibility, and credit terms are in a better position to hold share.

Food Delivery and Fresh-Produce Export Intensity

Agricultural packaging remains one of the most resilient demand pools in the Middle East and Africa containerboard market, as fresh-produce exports create concentrated, recurring demand for high-performance corrugated trays and boxes. South Africa's citrus and pome fruit export cycle, which peaks from February to July, drives predictable demand for packaging that meets EU phytosanitary and food-contact requirements while also protecting produce during long transit. Sappi reported that packaging and specialty paper sales volumes rose 8% year on year in FY2025, with improved containerboard demand driven mainly by a strong citrus season. MPact also reported strong volume growth in containerboard and agricultural packaging, and described the agricultural segment as structurally attractive due to export-oriented growth. Because these mills plan around Northern Hemisphere retail and harvest calendars as much as domestic cycles, the Middle East and Africa containerboard market benefits from export-linked food packaging that is not fully tied to local consumer sentiment.

Imported OCC, Pulp, And Kraft Liner Price Volatility

Raw material risk remains the clearest constraint on the Middle East and Africa containerboard market because the region has almost no domestic virgin wood fiber pulp base and still depends heavily on imported OCC bales and kraft liner. This exposure became more visible in 2025 when higher recovered paper costs hit margins even as shipment volumes improved for major regional players. MPact said recovered paper prices rose significantly in the first half of 2025, and that cost pressure contributed to a 14.5% decline in EBITDA even though containerboard sales volumes increased 20.3% in the same period. The feedback loop is important because new recycled machine capacity improves local availability of board, but it can also intensify competition for the same OCC pool and raise input prices again. That means the Middle East and Africa containerboard market can gain from domestic scale while still struggling to convert that scale into stable margin expansion.

Other drivers and restraints analyzed in the detailed report include:

- Plastic Substitution and Packaging EPR Momentum

- Lightweight Low-Basis-Weight Board Upgrades

- Red Sea and Gulf Shipping-Disruption Cost Shocks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 53.7% of the Middle East and Africa containerboard market share in 2025, which reflects the region's practical dependence on OCC-based testliner and fluting in a fiber-deficient environment. The dominance of recycled grades is reinforced by the production profile in Saudi Arabia, the UAE, and Kuwait, where domestic containerboard capacity is centered on recycled fiber rather than virgin pulp. Cost discipline and sustainability requirements are both supporting this pattern, so buyers often see recycled board as the most workable balance between availability and economics. That is why the Middle East and Africa containerboard market continues to rely on recovered fiber even when imported OCC costs become more volatile.

Virgin fibers are projected to grow at a 4.4% CAGR through 2031, and that faster pace reflects a quality premium rather than a broad shift away from recycled grades. Mondi's Duino mill in Italy added 420,000 tonnes per year of recycled containerboard capacity designed to serve European customers and international routes, including flows connected to the Middle East and Africa containerboard market, which underlines the continued competitive pressure from well-capitalized exporters. Food-contact applications, stronger burst-strength needs, and pharma-adjacent packaging still favor virgin-based linerboard, where recycled input cannot deliver consistent performance at scale. Multinational customers are also placing greater weight on chain-of-custody and certification standards, and that creates a specification gap for some regional recycled-fiber suppliers.

List of Companies Covered in this Report:

- Mondi plc

- Mpact Limited

- Middle East Paper Company

- Arab Paper Manufacturing Company

- Sappi Limited

- United Carton Industries Company

- Arabian Packaging Co. LLC

- Industrial Development Company s.a.l.

- Napco National CJSC

- Obeikan Investment Group

- Gulf Paper Manufacturing Company K.S.C.

- Omani Packaging Company SAOG

- Queenex Corrugated Carton Factory

- RAK Packaging Company Ltd.

- UNIPAKNILE Ltd.

- Cairo Egyptian Packaging and Containers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce and Omnichannel Parcel Growth

- 4.2.2 Food Delivery and Fresh-Produce Export Intensity

- 4.2.3 Plastic Substitution and Packaging EPR Momentum

- 4.2.4 Lightweight Low-Basis-Weight Board Upgrades

- 4.2.5 AFCFTA-Led Need for Stronger Transit Packaging

- 4.2.6 Digital Print Adoption Enabling High-Margin Short Runs

- 4.3 Market Restraints

- 4.3.1 Imported OCC, Pulp, and Kraft Liner Price Volatility

- 4.3.2 Water Scarcity and Mill-Effluent Constraints

- 4.3.3 Red Sea and Gulf Shipping-Disruption Cost Shocks

- 4.3.4 Water-Use Restrictions Affecting Pulp Mills

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 Middle East

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Turkey

- 5.4.1.4 Rest of Middle East

- 5.4.2 Africa

- 5.4.2.1 South Africa

- 5.4.2.2 Egypt

- 5.4.2.3 Nigeria

- 5.4.2.4 Rest of Africa

- 5.4.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mondi plc

- 6.4.2 Mpact Limited

- 6.4.3 Middle East Paper Company

- 6.4.4 Arab Paper Manufacturing Company

- 6.4.5 Sappi Limited

- 6.4.6 United Carton Industries Company

- 6.4.7 Arabian Packaging Co. LLC

- 6.4.8 Industrial Development Company s.a.l.

- 6.4.9 Napco National CJSC

- 6.4.10 Obeikan Investment Group

- 6.4.11 Gulf Paper Manufacturing Company K.S.C.

- 6.4.12 Omani Packaging Company SAOG

- 6.4.13 Queenex Corrugated Carton Factory

- 6.4.14 RAK Packaging Company Ltd.

- 6.4.15 UNIPAKNILE Ltd.

- 6.4.16 Cairo Egyptian Packaging and Containers

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)亞太地區箱板市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)南美洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)北美貨櫃紙板:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)