|

市場調查報告書

商品編碼

2063884

美國紙箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

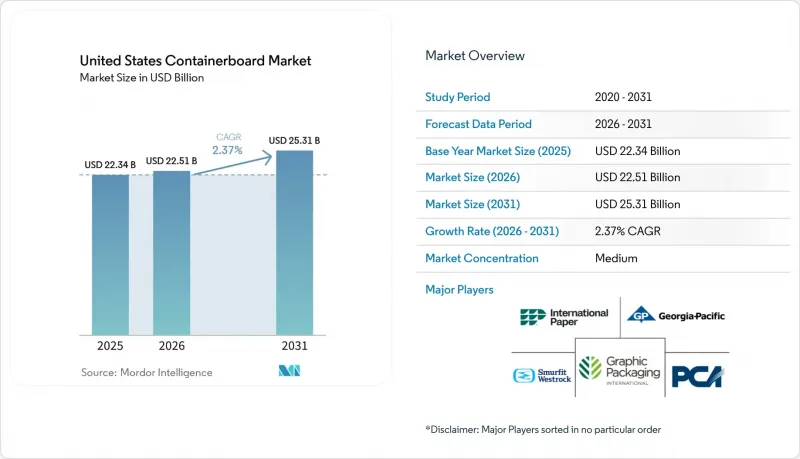

據 Mordor Intelligence 稱,2025 年美國瓦楞紙板市場價值為 223.4 億美元,預計到 2031 年將達到 253.1 億美元,而 2026 年為 225.1 億美元,2026 年至 2031 年預測期內的複合成長率為 2.37%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶(食品飲料、消費品、工業等)進行細分。市場預測以美元計價。

美國箱板紙市場趨勢與洞察

電子商務和全通路應用對瓦楞紙箱的需求不斷成長。

雖然小包裹的成長不再直接轉化為紙箱需求的等量成長,但線上零售仍然是美國箱板紙市場整體需求的支撐。瓦楞紙箱仍占美國國內運輸貨物的90%以上,纖維基運輸包裝在國內商業中持續扮演核心角色。履約網路的組成正在發生變化,模切成型、單層層級構造和微型瓦楞設計逐漸取代了更簡單的規格。這種轉變有利於那些能夠提供強度更高、重量更輕的紙箱(而不僅僅是通用紙芯)的製造商。荷蘭合作銀行在2026年初指出,由於電子商務的成長將被小包裹重量的減輕部分抵消,因此到2027年底,需求將基本保持穩定。在美國箱板紙市場,這意味著雖然全通路需求支撐了工廠的運轉率,但產品組合的變化在提高利潤率方面發揮更大的作用。

提高強制性回收率和降低成本

品牌所有者日益將包裝規格轉向紙質形式,這推動了美國箱板紙市場的需求。亞馬遜已在其北美履約中心移除了95%的塑膠氣枕,取而代之的是100%由回收材料製成的紙質填充材,每年可避免使用150億個塑膠氣枕。此舉表明,一家大型物流公司的包裝重新設計如何能夠改變整個供應鏈的紡織品需求。這也支撐了對再生纖維的需求,因為來自廢棄產品的再生材料的價值日益凸顯,不僅被視為一種品牌選擇,也成為採購要求的一部分。美國箱板紙市場正受益於此轉變,因為瓦楞紙包裝符合現有的回收系統,並且比許多競爭材料更容易滿足可回收性要求。由此產生的另一個影響是,更多的紙質包裝最終將回歸舊瓦楞紙板(OCC)的回收流程,從而有助於補充再生原料,同時對再生纖維的需求也在不斷成長。

靈活的郵寄方式和「自有貨櫃運輸」的替代方案

彈性包裝袋和自有貨櫃運輸 (SIOC) 計劃正在減少對瓦楞紙箱的部分需求,而這些需求原本會支撐美國箱板紙市場。據亞馬遜稱,出貨中瓦楞紙箱的比例從 43% 下降到 40%,而 SIOC 參與率則從 8% 上升到 11%。這種影響在小包裹電商領域最為顯著,因為使用氣泡信封和產品包裝可以省去額外的瓦楞紙箱。這並沒有完全消除對小包裹的需求,但減少了每次出貨使用的瓦楞紙面積。同時,剩餘的瓦楞紙箱出貨通常需要更堅固、更專業的紙板,這在一定程度上抵消了因成分變化而導致的用量減少。然而,如果主要平台繼續將合適的商品轉向不使用瓦楞紙箱或不使用外包裝的形式,美國箱板紙市場的成長將面臨巨大的瓶頸。

細分市場分析

預計到2025年,再生纖維將占美國箱板紙市場佔有率的54.5%,並將保持最高的成長率,到2031年複合年成長率將達到3.4%。這一地位反映了美國再生紙(OCC)收集、分類和造紙系統的長期發展。美國箱板紙市場長期以來依賴此基礎設施,但近年來,品牌所有者對源自廢棄舊產品的消費後再生材料的需求不斷成長,進一步鞏固了其基礎。此外,老牌原生纖維廠產能的下降導致未漂白牛皮紙的供應緊張,提高了再生紙生產在整個系統中的相對重要性。 Cascades、Kruger、Pratt Industries和ND Paper等製造商正在投資生產高性能的再生箱板紙和中型,而不再局限於通用等級的產品。根據Cascades公司介紹,其超高性能箱板紙採用100%再生纖維製成(其中90%來自廢棄舊產品),專為輕量化、高速瓦楞紙板生產而設計。該產品的發展方向表明,美國箱板紙產業正積極推動在對性能要求極高的應用中採用再生材料。

在某些應用中,僅靠再生紙漿難以確保表面品質、耐破強度和食品接觸安全性,因此原生紙漿仍然至關重要。在高階牛皮紙襯紙、出口包裝和某些零售包裝中,功能性優於原生紙漿的產品依然備受青睞。美國箱板紙市場在對可靠性和品牌有嚴格要求的包裝領域仍然依賴原生紙漿生產。根據Mordor Intelligence的報告,2024年北美瓦楞紙板產量的89%已獲得產銷監管鏈(CoC)認證,高於2023年的76%。這表明企業將繼續投資於經認證的原生原料,並需要更全面的永續性文件。喬治亞太平洋公司也強調了對牛皮紙基產品的持續資本投資,並計劃於2025年投資8,300萬美元擴建其位於佛羅裡達州帕拉特卡的工廠。因此,儘管再生紙漿在規模和成長方面主導市場,但原生紙漿在高階產品領域仍佔據重要地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務和全通路對包裝盒的需求增加。

- 加強對再生材料含量和紙張生產的監管。

- 食品飲料出貨需求穩定

- 合理化生產能力並提高產業運轉率

- 環保EPR定價機制鼓勵生產可回收紙板產品。

- 透過輕質再生襯墊的創新來拓展替代方案

- 市場限制因素

- 靈活的郵寄方式和自有貨櫃運輸方案

- OCC和能源成本波動

- 食品應用中不含 PFAS 的阻隔材料的認證成本

- 各州EPR及合規性的複雜性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 最終用戶

- 食品/飲料

- 消費品

- 產業

- 其他最終用戶

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Paper Company

- Smurfit Westrock plc

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries, Inc.

- Cascades Inc.

- Graphic Packaging International LLC

- Hood Container Corporation

- Green Bay Packaging Inc.

- Atlantic Packaging, LLC

- Menasha Corporation

- Nine Dragons Paper Holdings

- New-Indy Containerboard LLC

- Kruger Inc.

- Saica Pack USA, LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states containerboard market size was valued at USD 22.34 billion in 2025 and estimated to grow from USD 22.51 billion in 2026 to reach USD 25.31 billion by 2031, at a CAGR of 2.37% during the forecast period 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Containerboard Market Trends and Insights

Rising E-Commerce and Omnichannel Box Demand

Online retail continues to support a broad demand floor for the United States containerboard market, even though parcel growth no longer converts into box demand on a one-to-one basis. Corrugated boxes still account for more than 90% of goods shipped in the country, keeping fiber-based transport packaging central to domestic commerce. The mix inside fulfillment networks is changing, with more die-cut formats, single-wall structures, and microflute designs replacing simpler runs. That shift favors producers who can supply stronger and lighter grades rather than just the commodity-grade medium. Rabobank noted in early 2026 that demand should remain broadly flat through late 2027, with e-commerce gains partly offset by parcel-level lightweighting. In the United States containerboard market, that means omnichannel demand is supporting plant utilization, while product mix is doing more of the work on margins.

Growing Recycled-Content and Pauperization Mandates

Brand owners are directing more packaging specifications toward paper-based formats, which is reinforcing demand for the United States containerboard market. Amazon removed 95% of plastic air pillows from North American fulfillment centers and replaced them with paper filler made from 100% recycled content, avoiding 15 billion plastic air pillows each year. That move shows how packaging redesign at one large shipper can alter fiber demand across broad supply chains. It also supports recycled-fiber grades, as post-consumer content is increasingly part of procurement requirements rather than a branding option. The United States containerboard market benefits from this shift because corrugated packaging already fits existing recovery systems and can more easily meet recyclability expectations than many competing materials. A related effect is that more paper-based packaging eventually returns to the OCC stream, which helps replenish recycled feedstock even as demand for recovered fiber rises.

Flexible Mailers and Ships-In-Own-Container Substitution

Flexible mailers and ship-in-own-container programs are reducing part of the box demand that would otherwise support the United States containerboard market. Amazon reported that corrugated boxes fell from 43% to 40% of deliveries while ship-in-own-container participation increased from 8% to 11%. The effect is most visible in small-parcel e-commerce, where padded mailers and product-ready packs can bypass the need for an additional corrugated box. This does not remove parcel demand from the system, but it does reduce the square footage per shipment. At the same time, the remaining corrugated shipments often require stronger, more specialized board, which partly offsets the lost volumes from the mix. Even so, the United States containerboard market faces a real ceiling on growth if major platforms continue shifting more qualified items into non-box or no-overbox formats.

Other drivers and restraints analyzed in the detailed report include:

- Stable Food and Beverage Shipment Demand

- Capacity Rationalization Tightening Industry Utilization

- OCC and Energy Cost Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Recycled fibers held 54.5% of the United States containerboard market share in 2025 and are also projected to post the fastest CAGR of 3.4% through 2031. This position reflects the long build-out of OCC recovery, sorting, and mill systems across the country. The United States containerboard market has relied on that infrastructure for years, and recent brand-owner requirements for post-consumer content have further reinforced it. Capacity closures at older virgin-fiber assets also tightened the supply base for unbleached kraft grades and increased the relative weight of recycled production in the system. Producers such as Cascades, Kruger, Pratt Industries, and ND Paper have been investing in stronger recycled liner and medium offerings rather than staying confined to commodity grades. Cascades said its extra-high-performance linerboard uses 100% recycled fiber, including 90% post-consumer content, and is designed for lightweight, high-speed corrugating. That product direction shows how the United States containerboard industry is pushing recycled material deeper into performance-sensitive uses.

Virgin fibers still matter in applications where surface quality, burst strength, and food-contact assurance remain harder to meet with recycled furnish alone. Premium kraftliner, export packaging, and some retail-ready formats continue to support a functional premium for virgin grades. The United States containerboard market still relies on virgin output for parts of the packaging mix where reliability and branding requirements are strict. Mordor Intelligence noted that 89% of North American corrugated output carried chain-of-custody certifications in 2024, up from 76% in 2023, which points to continued investment in certified virgin inputs as well as broader sustainability documentation. Georgia-Pacific also announced an USD 83 million expansion at its Palatka, Florida mill in 2025, which underlined ongoing capital support for kraft-based paper output. The result is a market where recycled fiber leads on scale and growth, while virgin fiber remains important in the premium end of the grade spectrum.

List of Companies Covered in this Report:

- International Paper Company

- Smurfit Westrock plc

- Packaging Corporation of America

- Georgia-Pacific LLC

- Pratt Industries, Inc.

- Cascades Inc.

- Graphic Packaging International LLC

- Hood Container Corporation

- Green Bay Packaging Inc.

- Atlantic Packaging, LLC

- Menasha Corporation

- Nine Dragons Paper Holdings

- New-Indy Containerboard LLC

- Kruger Inc.

- Saica Pack USA, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-commerce and Omnichannel Box Demand

- 4.2.2 Growing Recycled-Content and Paperization Mandates

- 4.2.3 Stable Food and Beverage Shipment Demand

- 4.2.4 Capacity Rationalization Tightening Industry Utilization

- 4.2.5 Eco-Modulated EPR Fees Favoring Recyclable Corrugated Formats

- 4.2.6 Lightweight Recycled Liner Innovation Expanding Substitution

- 4.3 Market Restraints

- 4.3.1 Flexible Mailers and Ships-in-Own-Container Substitution

- 4.3.2 OCC and Energy Cost Volatility

- 4.3.3 PFAS-Free Barrier Qualification Costs in Food Applications

- 4.3.4 State-by-State EPR and Compliance Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Packaging Corporation of America

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Pratt Industries, Inc.

- 6.4.6 Cascades Inc.

- 6.4.7 Graphic Packaging International LLC

- 6.4.8 Hood Container Corporation

- 6.4.9 Green Bay Packaging Inc.

- 6.4.10 Atlantic Packaging, LLC

- 6.4.11 Menasha Corporation

- 6.4.12 Nine Dragons Paper Holdings

- 6.4.13 New-Indy Containerboard LLC

- 6.4.14 Kruger Inc.

- 6.4.15 Saica Pack USA, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)