|

市場調查報告書

商品編碼

2063883

德國瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Germany Containerboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

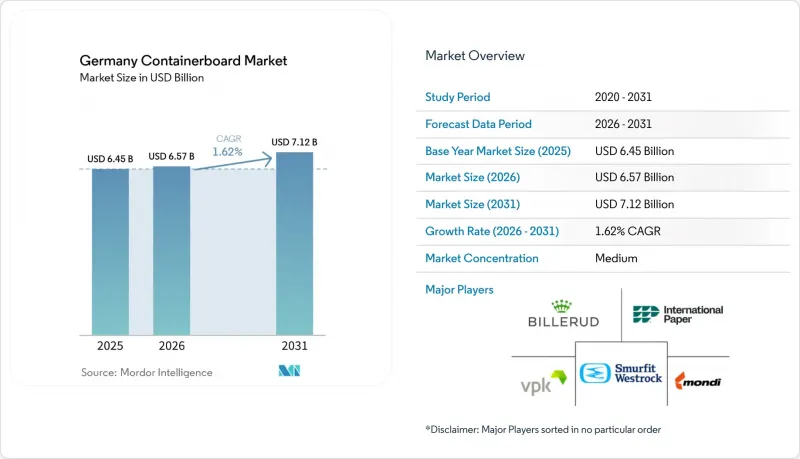

根據 Mordor Intelligence 預測,德國瓦楞紙板市場預計將從 2025 年的 64.5 億美元成長到 2026 年的 65.7 億美元,到 2031 年達到 71.2 億美元,2026 年至 2031 年的複合年成長率為 1.62%。

本報告按材料(原生纖維和再生纖維)、產品類型(工藝襯墊、測試襯墊、瓦楞紙板)和最終用戶(食品飲料、消費品、工業等)進行細分。市場預測以美元計價。

德國箱板紙市場趨勢與洞察

對電子商務和全通路履約。

預計到2025年,德國線上零售市場規模將達到924億歐元(1,000億美元),較2024年成長4%。電商平台是推動這一成長的主要力量,而非電商通路預計將平均下降5.4%。這一趨勢導致瓦楞紙板的需求集中在少數幾家大型物流運營商手中,從而提升了德國箱板紙市場中交貨週期短、結構緊湊輕便的瓦楞紙板的價值。由於瓦楞紙板具有優異的防護性能、可回收性和易於自動化生產的特點,預計到2024年,瓦楞紙板仍將佔據德國電商包裝市場90%的佔有率。 2024年,德國的電子商務滲透率將達到87%,人均小包裹遞送量為54件。預計到 2031 年,宅配、快遞和小包裹業務也將以 3.4% 的複合年成長率成長。因此,德國貨櫃紙板市場對尺寸合適的再生中型和測試襯裡紙板的需求增加,而對傳統運輸模式中以前使用的重型小包裹紙板的需求則有所下降。

在二級包裝和運輸包裝中用紙張取代塑膠

在德國,商業買家和監管機構都在推動從塑膠運輸容器轉向紙質替代品,因為他們優先考慮的是更便捷的回收和更低的合規成本。 2023年,歐洲紙張和瓦楞紙板的回收率達到了87%,而塑膠的回收率僅42.1%,這進一步鞏固了纖維包裝在生產者延伸責任制(EPR)下的經濟優勢。海德堡印刷機械股份公司(Heidelberger Druckmaschineen AG)和DHBW海爾布隆公司聯合開展的一項關於2030年包裝趨勢的調查預測,未來十年軟性紙包裝的年成長率將超過4.5%。在2026年德國國際包裝展(Interpack 2026)上,Hugo Beck和Mondi展示了他們的「Paper S」套筒包裝,該包裝使用70克牛皮紙代替塑膠收縮膜進行二次包裝,並展示了其實際應用。在德國箱板紙市場,這種轉變推動了對中等重量牛皮紙和特種瓦楞紙等級的需求增加,而對重型箱板紙的需求則有所下降,這主要體現在運輸應用方面。

能源、天然氣和OCC成本的波動

能源成本波動仍是德國箱板紙市場最明顯的結構性限制。這是因為德國再生紙的價格持續受到天然氣價格的嚴重影響。根據Fastmarkets的數據顯示,測試襯紙生產中68%的能源消耗依賴天然氣,而白襯紙塑合板的比例可能高達92%。 2025年第二季德國天然氣價格較2024年第二季上漲了18%,在能源價格飆升的情況下,生產商計劃在2026年初進一步提價。非一體化加工商和再生紙生產商在德國瓦楞紙板原紙市場受到的衝擊最大。這些公司幾乎沒有成本對沖空間,也難以消化能源和纖維原料價格同時上漲帶來的衝擊。

細分市場分析

截至2025年,原生纖維佔德國瓦楞紙板原紙市場的62.5%,但預計到2031年,再生紙的年複合成長率將達到2.1%。再生材料成長最顯著的領域是消費品、零售物流和日常消費品(FMCG)產業,這些產業的採購部門正在積極採用高品質的再生纖維。德國的閉合迴路回收系統為這項轉型提供了支持,因為瓦楞紙板佔回收的商業運輸包裝材料(包括紙張、紙板和瓦楞紙板)重量的88%。這一趨勢在小包裹和商店展示包裝領域尤其明顯,自動化瓦楞紙板生產設備正致力於透過使用更清潔的再生紙(OCC)來提高原紙製備效率和尺寸一致性。

另一方面,原生紙漿紙板在藥品二級包裝、生鮮食品和重型工業瓦楞紙板領域仍然發揮著重要的結構性作用,這些領域對耐破強度、印刷適性和防潮性的要求依然很高。根據2024年德國從業人員的一項調查,80%的受訪者認為,他們使用的包裝材料中包含的原生紙漿是提高再生紙漿品質的一個因素。因此,德國箱板紙市場正朝著更均衡的原料組成方向發展,而不是完全過渡到100%再生紙漿。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對電子商務和全通路履約。

- 在二級包裝和運輸包裝中用紙張取代塑膠

- 食品飲料運輸和商店展示過程中的衛生管理需求。

- 德國包裝材料採購中對再生纖維的接受度很高

- 在全自動瓦楞紙板生產機中採用克重低於100克/平方米的輕質紙板。

- 用於白色上衣和特殊襯裡的創新替代纖維混合物

- 市場限制因素

- 能源、天然氣和OCC成本波動劇烈

- 工業生產下滑,訂單謹慎

- 再生纖維出口中斷正在扭曲國內供應鏈經濟。

- PPWR合規和文件成本(實現完全貨幣化)

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料

- 原生光纖

- 再生纖維

- 依產品類型

- Craftliner

- 測試線

- 凹槽

- 最終用戶

- 食品/飲料

- 消費品

- 產業

- 其他最終用戶

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Progroup AG

- Papierfabrik Palm GmbH & Co. KG

- Hamburger Rieger GmbH

- LEIPA Georg Leinfelder GmbH

- Klingele Paper & Packaging SE & Co. KG

- Papierfabrik Adolf Jass GmbH & Co. KG

- THIMM Group GmbH+Co. KG

- Dunapack Spremberg GmbH & Co. KG

- Mondi plc

- Smurfit Westrock plc

- Saica, SA

- VPK Group NV

- Model GmbH

- Rondo Ganahl AG

- Billerud AB

- Metsa Board Corporation

- Schumacher Packaging GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany containerboard market size is expected to increase from USD 6.45 billion in 2025 to USD 6.57 billion in 2026 and reach USD 7.12 billion by 2031, growing at a CAGR of 1.62% over 2026-2031.

This report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End User (Food and Beverage, Consumer Goods, Industrial, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Containerboard Market Trends and Insights

Rising E-Commerce and Omnichannel Fulfillment Demand

Germany's online retail sector rose to EUR 92.4 billion (USD 100 billion) in 2025, up 4% from 2024, with marketplace platforms driving growth while non-marketplace channels declined on average by 5.4%. This pattern is concentrating corrugated demand around a smaller set of large logistics operators, which raises the value of short lead times and tightly configured lightweight formats in the German containerboard market. Corrugated board held a 90% share of German e-commerce packaging in 2024 because it remained strong in protection, recyclability, and automation compatibility. Germany's e-commerce penetration reached 87% in 2024, average parcel deliveries were 54 per resident, and the courier, express, and parcel segment is projected to expand at a 3.4% CAGR through 2031. The German containerboard market is therefore seeing a stronger pull for right-size recycled medium and testliner formats than for heavier parcel grades used in earlier shipping models.

Plastic-to-Paper Substitution in Secondary and Transit Packaging

The move from plastic transport formats to paper-based alternatives is advancing in Germany as commercial buyers and regulators both push for easier recycling and lower compliance costs. Across Europe, paper and cardboard reached a 87% recycling rate in 2023, while plastics stood at 42.1%, strengthening the economic case for fiber-based packaging under EPR systems. The Heidelberger Druckmaschinen AG and DHBW Heilbronn study on packaging to 2030 projected that flexible paper packaging will grow by more than 4.5% annually through the decade. Hugo Beck and Mondi showcased a commercial example at Interpack 2026 featuring the Paper S sleeve wrapper, which uses 70 gsm kraft paper instead of plastic shrink film for secondary packaging. In the German containerboard market, this shift supports greater demand for medium-weight kraft and specialty fluting grades than for heavyweight linerboard in transit applications.

Volatile Energy, Gas, and OCC Costs

Energy cost volatility is still the clearest structural restraint on the Germany containerboard market because German recycled grades remain highly exposed to natural gas costs. Fastmarkets reported that testliner production draws 68% of its energy from natural gas, while white-lined chipboard can reach 92%. German natural gas prices rose 18% in Q2 2025 versus Q2 2024, and producers were still pursuing further hikes in early 2026 as energy pressure persisted. The German containerboard market feels this most sharply at non-integrated converters and recycled-grade mills, as they have less room to hedge costs or absorb concurrent spikes in energy and fiber input prices.

Other drivers and restraints analyzed in the detailed report include:

- Food and Beverage Shipment Hygiene and Shelf-Ready Needs

- High Recycled-Fiber Acceptance in German Packaging Procurement

- Weak Industrial Production and Cautious Ordering

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Virgin fibers held 62.5% of the Germany containerboard market share in 2025, while recycled grades are projected to grow at a 2.1% CAGR through 2031. Recycled-furnish growth is strongest in consumer goods, retail logistics, and FMCG applications where procurement teams are comfortable with high-quality recovered fiber. Germany's closed-loop collection structure supports this shift because corrugated board makes up 88% by mass of commercial transport packaging collected as paper, paperboard, and cardboard. The move is especially visible in parcel and shelf-ready formats where automated corrugators favor improved dimensional consistency from better stock preparation and cleaner OCC streams.

Virgin-fiber board still keeps a structural role in pharmaceutical secondary packaging, fresh produce, and heavy-wall industrial corrugated because those uses still value burst strength, print surface, and moisture resistance. The 2024 German practitioner survey showed that 80% of respondents see virgin fiber in incoming packaging as a positive input to recycled pulp quality. That is why the German containerboard market is moving toward a more balanced raw-material mix rather than a full shift to mono-recycled fiber.

List of Companies Covered in this Report:

- Progroup AG

- Papierfabrik Palm GmbH & Co. KG

- Hamburger Rieger GmbH

- LEIPA Georg Leinfelder GmbH

- Klingele Paper & Packaging SE & Co. KG

- Papierfabrik Adolf Jass GmbH & Co. KG

- THIMM Group GmbH + Co. KG

- Dunapack Spremberg GmbH & Co. KG

- Mondi plc

- Smurfit Westrock plc

- Saica, S.A.

- VPK Group NV

- Model GmbH

- Rondo Ganahl AG

- Billerud AB

- Metsa Board Corporation

- Schumacher Packaging GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-Commerce and Omnichannel Fulfillment Demand

- 4.2.2 Plastic-to-Paper Substitution in Secondary and Transit Packaging

- 4.2.3 Food and Beverage Shipment Hygiene and Shelf-Ready Needs

- 4.2.4 High Recycled-Fiber Acceptance in German Packaging Procurement

- 4.2.5 Lightweight Sub-100 gsm Grade Adoption on Automated Corrugators

- 4.2.6 Alternative-Fiber Blending for White-Top and Specialty Liner Innovation

- 4.3 Market Restraints

- 4.3.1 Volatile Energy, Gas, and OCC Costs

- 4.3.2 Weak Industrial Production and Cautious Ordering

- 4.3.3 Recovered-Fiber Export Disruptions Distorting Domestic Supply Economics

- 4.3.4 PPWR Compliance and Documentation Costs Ahead of Full Monetization

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material

- 5.1.1 Virgin Fibers

- 5.1.2 Recycled Fibers

- 5.2 By Product Type

- 5.2.1 Kraftliners

- 5.2.2 Testliners

- 5.2.3 Flutings

- 5.3 By End User

- 5.3.1 Food and Beverage

- 5.3.2 Consumer Goods

- 5.3.3 Industrial

- 5.3.4 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Progroup AG

- 6.4.2 Papierfabrik Palm GmbH & Co. KG

- 6.4.3 Hamburger Rieger GmbH

- 6.4.4 LEIPA Georg Leinfelder GmbH

- 6.4.5 Klingele Paper & Packaging SE & Co. KG

- 6.4.6 Papierfabrik Adolf Jass GmbH & Co. KG

- 6.4.7 THIMM Group GmbH + Co. KG

- 6.4.8 Dunapack Spremberg GmbH & Co. KG

- 6.4.9 Mondi plc

- 6.4.10 Smurfit Westrock plc

- 6.4.11 Saica, S.A.

- 6.4.12 VPK Group NV

- 6.4.13 Model GmbH

- 6.4.14 Rondo Ganahl AG

- 6.4.15 Billerud AB

- 6.4.16 Metsa Board Corporation

- 6.4.17 Schumacher Packaging GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

菲律賓貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)越南貨櫃板材:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞箱板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國瓦楞紙板原紙:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)新加坡瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031)印度貨櫃紙板市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)日本瓦楞紙板原紙:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)法國貨櫃紙板:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利貨櫃紙板:市場佔有率分析、產業趨勢與統計數據、成長預測(2026-2031)西班牙瓦楞紙板原紙:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)