|

市場調查報告書

商品編碼

2063761

歐洲折疊式紙盒:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

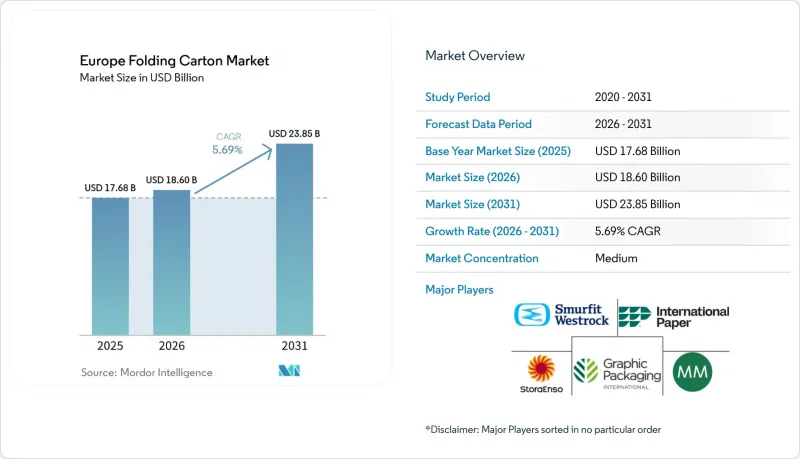

根據 Mordor Intelligence 預測,歐洲折疊式紙匣生產規模預計將在 2025 年達到 176.8 億美元,2026 年達到 186 億美元,到 2031 年達到 238.5 億美元,2026 年至 2031 年的複合年成長率為 5.69%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、塗佈未漂白牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷等)、終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)以及地區進行細分。市場預測以美元(USD)為單位。

歐洲折疊式紙盒市場趨勢與洞察

歐盟正在加速推動快速消費品品牌向可回收包裝轉型。

大型食品和個人護理公司在確保纖維原料供應和降低成本方面,行動速度超過了相關法規的實施速度。貝爾集團(Groupe Bel)於2025年承諾,到2027年將所有起司獨立包裝更換為折疊式紙盒,目標是每年減少4,200噸塑膠用量。費列羅(Ferrero)已實現其目標,到2025年僅採購FSC認證的紙板,而億滋國際(Mondelez)則已改用低致敏性油墨,這些油墨在標準造紙廠仍可回收利用。先行者可以按標準價格獲得認證纖維,但從2028年起,後後進企業可能被迫支付15%至25%的溢價。各國機構正在根據聯合研究中心(JRC)的協議監督可回收性檢驗,這使得先行企業能夠確保合規並更順利地進入市場。

電子商務的快速成長帶動了對輕型保護紙箱的需求。

預計到2025年,線上零售市場規模將達到8,990億歐元(1.01兆美元),這將改變我們設計包裝結構的方式。目前,250-350克/平方公尺的瓦楞紙箱是自動化履約中心的主流選擇。這是因為這種紙箱可以減輕12-18%的運輸重量,同時在最後一公里配送過程中具有很高的抗壓性。 2026年3月,DS Smith對其位於丹麥格倫納的工廠進行了升級改造,引進了伺服驅動的旋轉式模切機。這將使其年產能增加1500萬平方米,旨在為時尚和電子產品零售商提供機器人可直接使用的模切產品。亞馬遜和Zalando計劃在2027年前要求使用無應力、無黏合劑的包裝形式,這將加速自鎖結構的普及,從而減少生產線換線次數和膠帶用量。

硬木紙漿價格波動給加工商的利潤率帶來了壓力。

2024年至2025年間,NBSK紙漿價格在每噸950美元至1,180美元之間波動,而BEK紙漿價格則維持在每噸720美元至920美元之間。這給息稅折舊EBITDA獲利率在8%至12%之間的加工商帶來了壓力。 Mayr-Melnhof指出,2025年成本上漲的60%是由於紙漿價格飆升造成的,而成本轉嫁需要3至6個月的延遲時間。受年度價格合約約束的中小型加工商難以回收成本,往往不得不接受利潤率下降200至300個基點。再生紙漿的緩解作用有限,因為出於安全考慮,藥品和化妝品瓦楞紙箱仍然需要使用原生纖維SBS。

細分市場分析

預計固態漂白硫酸漿 (SBS) 將以 6.69% 的複合年成長率成長,高於歐洲折疊式紙盒市場的平均水平,這反映出醫藥和高階化妝品包裝領域嚴格的轉型限制。歐洲 SBS折疊式紙盒市場受益固態的「Fusion TopScreen」和 Stora Enso 的「PerformaBARRIER」技術,這兩款技術均符合 CEPI 的 2025 年可回收性標準,且無需使用塑膠薄膜即可實現阻隔性能。折疊式紙板仍保持最大的市場佔有率,預計到 2025 年將佔歐洲折疊式紙盒市場佔有率的 38.12%。它適用於乾貨和煙草等對適中硬度要求的應用領域。

「塗佈未漂白牛皮紙」憑藉其天然的棕色美感,在有機食品領域不斷擴張;而「白線塑合板」則在價格敏感的金屬製品和家居用品領域極具競爭力。 Mondi於2025年收購了Schumacher Packaging,進一步增強了其SBS產品組合,新增了在棕色基材上使用白色油墨進行六色數位印刷的能力。這使得化妝品品牌能夠以較低的成本進行小批量、季節性促銷活動。在歐盟指令2011/62/EU監管的藥品序列化過程中,原生紙漿材料仍然佔據主導地位,因為印刷均勻性和壓紋深度對於防篡改完整性至關重要。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟正在加快快速消費品品牌向可回收包裝的過渡。

- 強制性生產者延伸責任制(EPR)費用增加了成本壓力。

- 電子商務的快速發展帶動了對輕便防護瓦楞紙箱。

- 採用高阻隔塗層取代塑膠層壓。

- 零售商對「現貨包裝」的需求以及物流最佳化

- 利用人工智慧色彩管理系統減少列印廢棄物。

- 市場限制因素

- 硬木漿價格波動給造紙企業的利潤率帶來了壓力。

- 能源成本上漲正在削弱中小規模轉換器的盈利。

- 塑膠產業的遊說活動正在延緩特定立法禁令的實施。

- 缺乏收集多材質瓦楞紙箱的基礎設施

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 國家

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Stora Enso Oyj

- Smurfit Westrock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging Holding Company

- International Paper Company

- Mondi plc

- Huhtamaki Oyj

- Sonoco Products Company

- Metsa Board Corporation

- Essentra plc

- Rondo Ganahl AG

- BBP Packaging Ltd.

- Autajon Group

- GPA Global Ltd.

- AR Lithos Carton Ltd.

- Scatolificio del Garda SpA

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe folding cartons market size is expected to be USD 17.68 billion in 2025, USD 18.60 billion in 2026, and reach USD 23.85 billion by 2031, growing at a CAGR of 5.69% from 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Folding Carton Market Trends and Insights

Accelerated Shift Toward Recyclable Packaging Among EU FMCG Brands

Major food and personal-care companies are moving faster than regulation to secure fiber supply and cost relief. Groupe Bel committed in 2025 to migrate all cheese-portion packs to folding cartons by 2027, removing 4,200 tonnes of plastic annually. Ferrero met its 2025 goal of sourcing only FSC-certified paperboard, while Mondelez switched to low-migration inks that stay recyclable in standard mills. Early adopters access certified fiber at baseline pricing, whereas late movers could face a 15-25% premium after 2028. National agencies oversee recyclability verification against Joint Research Centre protocols, giving first movers compliance certainty and smoother market access.

E-commerce Boom Driving Demand for Lightweight Protective Cartons

Online retail reached EUR 899 billion (USD 1.01 trillion) in 2025 and is reshaping the design of structures. Cartons between 250-350 gsm now dominate automated fulfillment centers because they reduce shipping weight by 12-18% while resisting crush during last-mile handling. DS Smith upgraded its Grenaa, Denmark, plant in March 2026 with a servo-driven rotary die-cutter that adds 15 million m2 of annual capacity, targeting robotics-compatible die-cuts for fashion and electronics shippers. Amazon and Zalando will require frustration-free, glue-free formats by 2027, accelerating uptake of self-locking structures that cut line changeovers and tape usage.

Volatile Hardwood Pulp Prices Compressing Converter Margins

NBSK pulp bounced between USD 950-1,180 per tonne in 2024-2025, while BEK ranged USD 720-920 per tonne, squeezing converters that operate on 8-12% EBITDA margins. Mayr-Melnhof noted that pulp inflation drove 60% of its COGS hike in 2025, with the pass-through delayed by 3 to 6 months. Smaller converters locked into annual price contracts struggle to recover costs and often accept margin erosion of 200-300 bps. Recycled grades offer only limited relief, as pharmaceutical and cosmetic cartons still require virgin-fiber SBS for migration-safety reasons.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Extended Producer Responsibility Fees Increasing Cost Pressure

- Adoption of High-Barrier Coatings Replacing Plastic Lamination

- Rising Energy Costs Undermining Small Converters' Profitability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate is projected to outgrow the European folding cartons market average at 6.69% CAGR, reflecting stringent migration limits for medicinal and luxury-cosmetic packs. The European folding cartons market for SBS benefits from Sappi Fusion TopScreen and Stora Enso PerformaBARRIER, both of which cleared CEPI's recyclability protocol in 2025, enabling barrier performance without plastic film. Folding Boxboard maintains the largest base, with 38.12% of the Europe folding cartons market share in 2025, favored for dry grocery and tobacco applications where moderate stiffness suffices.

Coated Unbleached Kraft expands in organic food lines that leverage its natural brown aesthetic, while White Line Chipboard competes in price-sensitive hardware and household goods. Mondi's 2025 buyout of Schumacher Packaging deepened its SBS portfolio and added six-color digital capability with white ink on brown substrates, letting cosmetics brands run short, seasonal promotions without litho plate costs. Virgin-fiber dominance persists in pharmaceutical serializations regulated under EU Directive 2011/62/EU, because print uniformity and emboss depth remain critical for anti-tamper integrity.

List of Companies Covered in this Report:

- Stora Enso Oyj

- Smurfit Westrock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging Holding Company

- International Paper Company

- Mondi plc

- Huhtamaki Oyj

- Sonoco Products Company

- Metsa Board Corporation

- Essentra plc

- Rondo Ganahl AG

- BBP Packaging Ltd.

- Autajon Group

- GPA Global Ltd.

- AR Lithos Carton Ltd.

- Scatolificio del Garda SpA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Shift Toward Recyclable Packaging Among EU FMCG Brands

- 4.2.2 Mandatory Extended Producer Responsibility Fees Increasing Cost Pressure

- 4.2.3 E-commerce Boom Driving Demand for Lightweight Protective Cartons

- 4.2.4 Adoption of High-Barrier Coatings Replacing Plastic Lamination

- 4.2.5 Retailer Demand for Shelf-Ready Packaging Optimizing Logistics

- 4.2.6 AI-Enabled Color Management Systems Reducing Print Waste

- 4.3 Market Restraints

- 4.3.1 Volatile Hardwood Pulp Prices Compressing Converter Margins

- 4.3.2 Rising Energy Costs Undermining Small Converters' Profitability

- 4.3.3 Plastic Lobby Campaigns Delaying Certain Legislative Bans

- 4.3.4 Limited Recovery Infrastructure for Multimaterial Cartons

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stora Enso Oyj

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Graphic Packaging Holding Company

- 6.4.5 International Paper Company

- 6.4.6 Mondi plc

- 6.4.7 Huhtamaki Oyj

- 6.4.8 Sonoco Products Company

- 6.4.9 Metsa Board Corporation

- 6.4.10 Essentra plc

- 6.4.11 Rondo Ganahl AG

- 6.4.12 BBP Packaging Ltd.

- 6.4.13 Autajon Group

- 6.4.14 GPA Global Ltd.

- 6.4.15 AR Lithos Carton Ltd.

- 6.4.16 Scatolificio del Garda SpA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)