|

市場調查報告書

商品編碼

2063779

中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

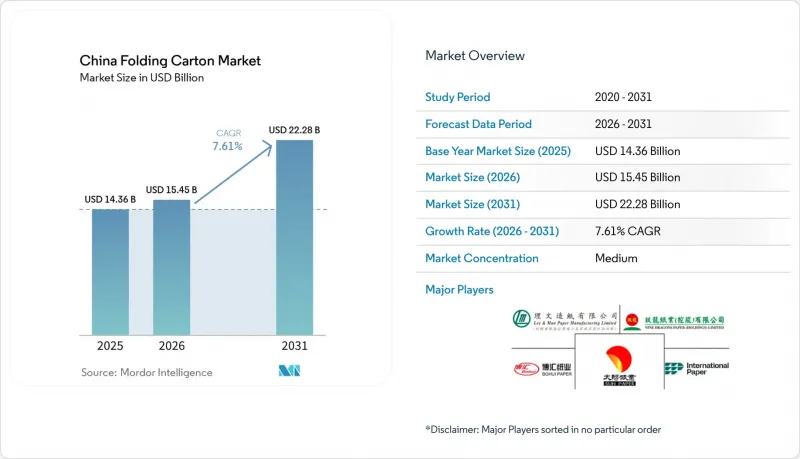

根據 Mordor Intelligence 預測,中國折疊式紙盒市場規模預計到 2025 年將達到 143.6 億美元,到 2026 年將達到 154.5 億美元,到 2031 年將達到 222.8 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 7.61%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、塗佈未漂白牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷、凹版印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)進行細分。市場預測以美元計價。

中國折疊式紙盒市場趨勢與洞察

對可回收紡織包裝材料的需求日益成長

到2025年,小包裹處理量將超過1,200億件。目前宅配包裝的綠色轉型計畫要求95%的材料可回收利用,促使托運人轉向使用折疊式紙箱。品牌商開始採用牛皮紙的美觀設計,這種紙張可以減少油墨用量並簡化回收流程。同時,像九龍紙業這樣的綜合性造紙企業已將其漂白紙板的年產能擴大到120萬噸,以確保認證供應。儘管目前已有重複使用試驗計畫,但由於衛生和逆向物流的挑戰,一次性紙箱仍然佔據主導地位。

電子商務的加速發展正在推動對小批量紙箱的需求。

在中國,受限時搶購和網紅行銷主導的銷售模式影響,訂單通路佔據了折疊式紙盒市場約55%的佔有率。 HP Indigo和EFI數位印刷機能夠實現97%的PANTONE色彩精度、QR碼嵌入,即使是500個小批量生產也能實現盈利。深圳的電子品牌對防靜電襯紙和客製化模切的需求日益成長,迫使加工商投資於與數位化工作流程整合的線上塗佈設備,以實現7天的前置作業時間。

紙漿和能源價格波動

2025年,針葉木漿價格下跌11.98%,至每噸5,633元人民幣(約790美元),預計2026年也將進一步下跌8.81%。雖然加工商歡迎原物料價格下跌,但像山東博匯這樣在紙漿生產大規模擴張方面投入巨資的綜合性造紙企業,如今正面臨利潤壓力。能源成本佔造紙乾燥成本的70%,而沿海省份天然氣價格的波動進一步加劇了利潤率的不穩定。

細分市場分析

折疊式紙板表面光滑、剛性穩定,適用於高速折疊糊盒機,可用於零食、乳製品和藥品包裝,預計到2025年將佔中國折疊紙盒市場佔有率的37.21%。這一細分市場受益於綜合造紙廠新增的原生紙漿生產線,這些生產線能夠可靠地滿足GB 4806關於重金屬遷移的標準。未漂白塗佈牛皮紙預計將以8.23%的複合年成長率超越中國折疊瓦楞紙板市場,這主要得益於有機食品和精釀飲料標籤因其天然棕色而追求真實性的需求。固體漂白硫酸鹽紙仍然是高階化妝品的主要基材,其亮白度、壓紋性和箔片黏合性使其價格合理,但由於硬木漿供應的限制,其市場佔有率的擴張受到限制。 White Line 塑合板用於清潔劑和乾貨的包裝,但其再生材料含量限制了印刷保真度和防潮性,導致其在冷凍和冷藏食品行業的應用有限。

投資者對原生紙漿產能日益成長的興趣在九龍紙業東莞工廠的設備升級中可見一斑。該公司計劃用一條年產62萬噸的牛皮紙襯紙生產線取代兩台老舊設備,這表明其生產方向正轉向食品級紙漿。奈米纖維素增強特種紙板正在興起,初步試驗顯示其重量減輕了15%。這可望降低多通路電商配送的物流成本。擁有內部實驗室以檢驗是否符合GB 4806標準的造紙企業正在擴大與尋求透明採購的全球品牌所有者的合作,這使得大型生產商在中國折疊式紙盒市場相對於現貨市場貿易商具有一定的競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對可再生纖維包裝材料的需求日益成長

- 電子商務的加速發展正在推動小批量瓦楞紙箱出貨量的成長。

- 化妝品和個人護理市場優質化的推進

- 政府的塑膠減量政策促進了紙板市場的發展。

- 透過投資自動化降低轉換成本

- 數位印刷技術的廣泛應用使得大規模個人化定製成為可能。

- 市場限制因素

- 紙漿和能源價格波動

- 與軟質塑膠包裝的競爭

- 由於造紙廠產能快速擴張,導致供應過剩。

- 食品接觸材料的嚴格合規成本

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nine Dragons Paper Holdings Limited

- Lee & Man Paper Manufacturing Limited

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Shandong Bohui Paper Industry Co., Ltd.

- International Paper Company

- Graphic Packaging International, LLC

- Huhtamaki Oyj

- Stora Enso Oyj

- Mayr-Melnhof Karton AG

- Mondi plc

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- Ningbo Zhonghua Paper Co., Ltd.

- Shanghai DE Printed Box

- Hangzhou Gerson Paper Co., Ltd.

- ITC Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the china folding carton market size is expected to be USD 14.36 billion in 2025, USD 15.45 billion in 2026, and reach USD 22.28 billion by 2031, growing at a CAGR of 7.61% from 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Folding Carton Market Trends and Insights

Growing Demand for Recyclable Fiber-Based Packaging

Parcel volumes surpassed 120 billion in 2025, and the express delivery packaging green transition plan now requires 95% of materials to be recyclable, steering shippers toward folding carton. Brands embrace Kraft aesthetics that cut ink coverage and simplify recycling, while integrated mills such as Nine Dragons expanded bleached boxboard capacity to 1.2 million t per year to secure a certified supply. Pilot reuse programs exist, yet hygiene and reverse-logistics hurdles keep single-use carton dominant.

E-Commerce Acceleration Driving Small-Run Carton Volumes

China's folding carton market orders placed through online channels reached an estimated 55% share in 2025, driven by flash sales and influencer-driven SKUs. Digital presses from HP Indigo and EFI enable profitable runs of 500 units with 97% PANTONE accuracy and embedded QR codes. Electronics brands in Shenzhen demand anti-static liners and custom die-cuts, pushing converters to invest in inline coating that integrates with digital workflows to achieve seven-day lead times.

Volatility in Pulp and Energy Prices

Softwood pulp fell 11.98% in 2025 to CNY 5,633 (USD 790) per tonne and is forecast to dip another 8.81% in 2026. Converters welcome cheaper inputs, but integrated mills such as Shandong Bohui financed sizable pulp expansions that now face compressed returns. Energy can represent 70% of drying costs in papermaking, and fluctuating natural gas tariffs in coastal provinces further destabilize margins

Other drivers and restraints analyzed in the detailed report include:

- Rising Premiumization in Cosmetics and Personal Care

- Government Plastic-Reduction Mandates Boosting Paperboard

- Competition from Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard captured 37.21% of the Chinese folding carton market share in 2025, supported by its smooth surface and consistent stiffness, which enable high-speed folder-gluers for snack, dairy, and pharmaceutical packaging. The segment benefits from integrated mills adding virgin fiber lines that ensure compliance with GB 4806 limits on heavy-metal migration. Coated Unbleached Kraft is forecast to outgrow the China folding carton market size at an 8.23% CAGR, propelled by organic food and craft beverage labels that showcase natural brown tones as an authenticity cue. Solid Bleached Sulfate remains the substrate of choice for prestige cosmetics where bright whiteness, embossability, and foil adhesion justify premium pricing, yet constrained hardwood pulp supply limits share gains. White Line Chipboard fills value tiers for detergents and dry goods, though its recycled content caps print fidelity and moisture resistance, limiting uptake in frozen and chilled foods.

Rising investor interest in virgin-fiber capacity is evident in Nine Dragons' Dongguan upgrade, which will replace two legacy machines with a 620,000 tonne-per-year kraft liner line, signaling a pivot toward food-safe grades. Specialty boards fortified with nanocellulose are emerging, with pilot trials documenting 15% weight reductions that can lower logistics costs for multichannel e-commerce distribution. Mills that embed in-house labs to verify GB 4806 compliance increasingly partner with global brand owners that demand transparent sourcing, giving scaled producers a margin edge over spot-market traders in the China folding carton market.

List of Companies Covered in this Report:

- Nine Dragons Paper Holdings Limited

- Lee & Man Paper Manufacturing Limited

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Shandong Bohui Paper Industry Co., Ltd.

- International Paper Company

- Graphic Packaging International, LLC

- Huhtamaki Oyj

- Stora Enso Oyj

- Mayr-Melnhof Karton AG

- Mondi plc

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- Ningbo Zhonghua Paper Co., Ltd.

- Shanghai DE Printed Box

- Hangzhou Gerson Paper Co., Ltd.

- ITC Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Recyclable Fiber-Based Packaging

- 4.2.2 E-Commerce Acceleration Driving Small-Run Carton Volumes

- 4.2.3 Rising Premiumization in Cosmetics and Personal Care

- 4.2.4 Government Plastic-Reduction Mandates Boosting Paperboard

- 4.2.5 Automation Investments Lowering Conversion Costs

- 4.2.6 Digital Printing Adoption Enabling Mass Personalization

- 4.3 Market Restraints

- 4.3.1 Volatility in Pulp and Energy Prices

- 4.3.2 Competition from Flexible Plastic Packaging

- 4.3.3 Supply Gluts from Rapid Mill Capacity Expansions

- 4.3.4 Stringent Food-Contact Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-Commerce and Retail-Ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nine Dragons Paper Holdings Limited

- 6.4.2 Lee & Man Paper Manufacturing Limited

- 6.4.3 Shandong Sun Paper Industry Joint Stock Co., Ltd.

- 6.4.4 Shandong Bohui Paper Industry Co., Ltd.

- 6.4.5 International Paper Company

- 6.4.6 Graphic Packaging International, LLC

- 6.4.7 Huhtamaki Oyj

- 6.4.8 Stora Enso Oyj

- 6.4.9 Mayr-Melnhof Karton AG

- 6.4.10 Mondi plc

- 6.4.11 Rengo Co., Ltd.

- 6.4.12 Oji Holdings Corporation

- 6.4.13 Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- 6.4.14 Ningbo Zhonghua Paper Co., Ltd.

- 6.4.15 Shanghai DE Printed Box

- 6.4.16 Hangzhou Gerson Paper Co., Ltd.

- 6.4.17 ITC Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)