|

市場調查報告書

商品編碼

2063763

中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East And Africa Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

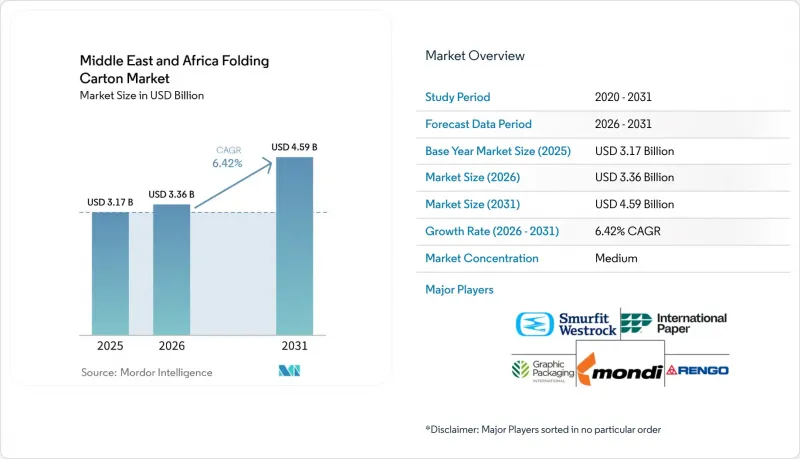

根據 Mordor Intelligence 預測,中東和非洲折疊式紙盒市場規模將從 2025 年的 31.7 億美元成長到 2026 年的 33.6 億美元,到 2031 年將達到 45.9 億美元,2026 年至 2031 年的複合年成長率為 6.42%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、塗佈未漂白牛皮紙等)、印刷技術(膠印、柔版印刷等)、終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)以及地區進行細分。市場預測以價值(美元)表示。

中東和非洲折疊式紙盒市場趨勢及洞察

快速的都市化正在推動加工食品的消費。

中東和非洲的城市人口正在不斷成長,現代化的雜貨店正在農村地區取代露天市場。奈及利亞、埃及和肯亞的連鎖超級市場優先使用折疊式紙盒包裝穀物、餅乾和粉狀飲料,因為這種紙盒可以整齊堆疊,提供充足的品牌展示空間,並且能夠承受潮濕的通路。隨著波灣合作理事會成員國城市中產階級收入的成長,消費者對折疊式紙盒所提供的優質圖案、可重複密封的封口以及經認證的永續材料的需求也日益成長。當地加工商正在升級印前工藝和膠印生產線,以滿足品牌所有者對色彩精準度的要求。同時,沙烏地阿拉伯正透過進口替代計劃促進瓦楞紙板原紙的國內採購。由於人口向都市區遷移導致購買力集中,消費者更傾向於選擇尺寸合適、衛生密封的包裝而非散裝商品,折疊式紙盒的出貨量成長速度超過了人口成長速度。

電子商務的擴張需要輕便的運輸包裝。

隨著線上零售滲透率的不斷提高,Noon、Jumia 和亞馬遜等平台正在利雅德、杜拜、拉各斯和內羅畢等城市擴展履約網路。品牌商傾向於選擇折疊式紙盒而非較重的瓦楞紙箱來包裝化妝品、電子配件和非處方藥,因為 250-350 克/平方米的普通漂白硫酸紙漿即可提供足夠的結構剛性。可變數據數位印刷機使加工商能夠按需印刷圖形、QR碼和季節性圖案,而無需承擔設置成本,從而最大限度地減少庫存積壓。美容和健康產品的訂閱盒正在採用膠印貼合加工折疊式紙盒,以最佳化體積重量課稅並降低最後一公里配送成本。海灣地區首都雲端廚房和快速生鮮雜貨應用程式的激增,推動了對耐油紙盒的需求,以確保食品在配送過程中保持品質和品牌形象。

紙漿價格波動給加工商的利潤率帶來了壓力。

斯堪地那維亞地區能源成本上漲和供應緊張已將北方漂白軟木牛皮紙(NBSK)的價格推高至每噸1710美元,預計到2026年初將達到這一價格。許多依賴進口原生紙漿的折疊式紙盒加工商面臨合約價格調整需要60至90天的滯後,這削弱了它們的營運資金緩衝。奈及利亞和埃及的貨幣貶值進一步加速了進口成本的上漲,對於沒有對沖手段的中小型加工商而言,利潤率面臨快速下降的風險。沙烏地阿拉伯的MEPCO公司計劃將產能翻倍至每年90萬噸,但其工廠主要生產衛生紙和特種紙,而非用於製造高清食品紙盒的塗佈紙板。由於零售商抵製成本上漲,對新的膠印生產線的投資正在放緩,加工商正轉向使用更輕的材料和數位化工作流程以減少基材的使用。

細分市場分析

可靠的統計數據支持了這一轉變的規模。截至2025年,可折疊紙板將在中東和非洲的可折疊紙盒市場佔據38.0%的佔有率,而固態漂白硫酸鹽紙漿(SBS)預計到2031年將以9.4%的複合年成長率成長。跨國糖果甜點和護膚品牌更傾向於使用後者,因為它具有高亮度、無異味且與水性分散劑相容性良好的優點。藥品泡殼包裝和營養補充品包裝袋正從PVC包裝轉向通過加速老化測試的SBS紙盒,這進一步加速了高檔基材的普及。

成長軌跡因價值鏈的不同而有所差異。在埃及,注重成本的家用清潔劑包裝仍然使用白色襯裡的塑合板,而沿岸地區的化妝品製造商則願意為採用經FSC認證的SBS紙板並塗覆紋理清漆的產品支付更高的價格。像RDM的「Vincicoat PLUS」這樣的再生紙板,其抗張強度可提高15-20%,使品牌商能夠在不影響圖形品質的前提下推廣使用再生材料。這種兩極化使得能夠同時採購低成本混合廢棄物板和高性能原生纖維的加工商佔據優勢,從而能夠為不同的客戶群提供廣泛的服務。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速的都市化正在推動加工食品的消費。

- 電子商務的擴張刺激了對輕型運輸包裝的需求。

- 政府的塑膠減量政策支持紙質包裝

- 隨著醫藥低溫運輸的發展,對阻隔塗佈紙盒的需求也增加。

- 投資高速數位印刷機,以縮短 SKU 的生產週期。

- 擴大海灣合作理事會國家清真認證食品出口

- 市場限制因素

- 紙漿價格波動給造紙企業的利潤率帶來了壓力。

- 缺乏完善的回收系統限制了再生纖維的供應。

- 無菌紙盒用塑膠阻隔膜的發展

- 非洲部分地區的政治不穩定影響資本投資決策。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 其他中東國家

- 非洲

- 埃及

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Graphic Packaging Holding Company

- Rengo Co., Ltd.

- Georgia-Pacific LLC

- Oji Holdings Corporation

- El-Sewedy Paper Industries Co.

- Nampak Ltd.

- AR Packaging Group AB

- Nada Manufacturing Co.

- Emirates Printing Press LLC

- Uniprint(Pty)Ltd.

- Offset Printing Industries LLC

- Hala Print Co.

- Primepak Industries Nigeria Ltd.

- Future Pack Group

- Caira International Paperboard

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa folding carton market size is expected to increase from USD 3.17 billion in 2025 to USD 3.36 billion in 2026 and reach USD 4.59 billion by 2031, growing at a CAGR of 6.42% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Folding Carton Market Trends and Insights

Rapid Urbanization Driving Packaged Food Consumption

Urban populations are swelling across the Middle East and Africa, prompting modern grocery formats to replace open-air markets in secondary cities. Supermarket chains in Nigeria, Egypt, and Kenya prioritize shelf-ready folding cartons for cereals, biscuits, and powdered beverages because the packs stack neatly, carry large branding areas, and withstand humid distribution corridors. Rising middle-class incomes in Gulf Cooperation Council cities are boosting demand for premium graphics, resealable closures, and certified sustainable substrates that folding cartons can deliver. Local converters are upgrading pre-press workflows and offset lines to meet brand owner requirements for color accuracy, while import substitution programs in Saudi Arabia encourage domestic sourcing of cartonboard grades. As migration concentrates purchasing power in urban hubs, folding-carton volumes grow faster than population because consumers favor portion-controlled, hygiene-sealed formats over loose goods.

E-commerce Expansion Requiring Lightweight Transit Packs

Online retail penetration is escalating, with platforms such as Noon, Jumia, and Amazon scaling fulfillment networks in Riyadh, Dubai, Lagos, and Nairobi. Brand owners choose folding cartons over heavier corrugated boxes for cosmetics, electronics accessories, and over-the-counter medicines, where structural rigidity is achievable with 250-350 gsm solid bleached sulfate. Variable-data digital presses allow converters to print order-specific graphics, QR codes, and seasonal artwork without makeready waste, minimizing inventory obsolescence. Subscription boxes for beauty and health products rely on litho-laminated folding cartons that optimize dimensional-weight tariffs, lowering last-mile costs. The surge of cloud kitchens and quick-commerce grocery apps in Gulf capitals drives demand for grease-resistant cartons that preserve food integrity and brand aesthetics during delivery.

Volatile Pulp Prices Compressing Converter Margins

Northern Bleached Softwood Kraft prices climbed to USD 1,710 per tonne in early 2026 after energy-cost spikes and Scandinavian supply constraints. Folding-carton converters, many of which are reliant on imported virgin fiber, endure 60-90-day lags before contract price adjustments, eroding working-capital buffers. Currency depreciation in Nigeria and Egypt amplifies landed-cost inflation, while smaller converters lacking hedging facilities risk rapid margin compression. Although Saudi Arabia's MEPCO is doubling capacity to 900,000 tonnes per year, the mill targets tissue and specialty grades rather than the coated boxboard essential for high-graphics food cartons. Cost pass-through resistance from retailers dampens investment appetite for new litho lines, nudging converters toward lightweighting and digital workflows that cut substrate usage.

Other drivers and restraints analyzed in the detailed report include:

- Government Plastic-Reduction Policies Favoring Paper-Based Packaging

- Pharmaceutical Cold-Chain Growth Requiring Barrier-Coated Cartons

- Under-Developed Collection Systems Limiting Recycled Fiber Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid statistics underscore the scale of this shift. Folding Boxboard held a 38.0% slice of the Middle East and Africa folding carton market in 2025, while Solid Bleached Sulfate is set to grow at a 9.4% CAGR through 2031. Multinational confectionery and skincare brands prefer the latter for its brightness, odor neutrality, and compatibility with aqueous dispersion barriers. Pharmaceutical blisters and nutraceutical sachets are migrating from PVC wallets to SBS cartons that pass accelerated-aging tests, reinforcing premium substrate adoption.

Growth trajectories diverge across value chains. Cost-sensitive household detergent packs in Egypt retain white-lined chipboard, yet Gulf cosmetics marketers pay premiums for FSC-certified SBS paired with tactile varnishes. Recycled grades, such as RDM's Vincicoat PLUS, which deliver 15-20% higher tensile strength, enable brand owners to claim recycled content without downgrading graphics. This bifurcation rewards converters that can source both low-cost mixed-waste boards and high-performance virgin fiber, sustaining service breadth for diverse customer tiers.

List of Companies Covered in this Report:

- International Paper Company

- Smurfit Westrock plc

- Mondi plc

- Graphic Packaging Holding Company

- Rengo Co., Ltd.

- Georgia-Pacific LLC

- Oji Holdings Corporation

- El-Sewedy Paper Industries Co.

- Nampak Ltd.

- AR Packaging Group AB

- Nada Manufacturing Co.

- Emirates Printing Press LLC

- Uniprint (Pty) Ltd.

- Offset Printing Industries LLC

- Hala Print Co.

- Primepak Industries Nigeria Ltd.

- Future Pack Group

- Caira International Paperboard

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanization Driving Packaged Food Consumption

- 4.2.2 E-commerce Expansion Requiring Lightweight Transit Packs

- 4.2.3 Government Plastic-Reduction Policies Favoring Paper-Based Packaging

- 4.2.4 Pharmaceutical Cold-Chain Growth Requiring Barrier Coated Cartons

- 4.2.5 Investment in High-Speed Digital Presses Enabling Short-Run SKUs

- 4.2.6 Rise of Halal-Certified Food Exports from GCC

- 4.3 Market Restraints

- 4.3.1 Volatile Pulp Prices Compressing Converter Margins

- 4.3.2 Under-developed Collection Systems Limiting Recycled Fiber Availability

- 4.3.3 Growing Plastic Barrier Films in Aseptic Cartons

- 4.3.4 Political Instability Affecting Cap-Ex Decisions in Parts of Africa

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of Substitutes

- 4.8.4 Threat of New Entrants

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 Middle East

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Qatar

- 5.4.1.4 Turkey

- 5.4.1.5 Rest of Middle East

- 5.4.2 Africa

- 5.4.2.1 Egypt

- 5.4.2.2 South Africa

- 5.4.2.3 Nigeria

- 5.4.2.4 Kenya

- 5.4.2.5 Rest of Africa

- 5.4.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mondi plc

- 6.4.4 Graphic Packaging Holding Company

- 6.4.5 Rengo Co., Ltd.

- 6.4.6 Georgia-Pacific LLC

- 6.4.7 Oji Holdings Corporation

- 6.4.8 El-Sewedy Paper Industries Co.

- 6.4.9 Nampak Ltd.

- 6.4.10 AR Packaging Group AB

- 6.4.11 Nada Manufacturing Co.

- 6.4.12 Emirates Printing Press LLC

- 6.4.13 Uniprint (Pty) Ltd.

- 6.4.14 Offset Printing Industries LLC

- 6.4.15 Hala Print Co.

- 6.4.16 Primepak Industries Nigeria Ltd.

- 6.4.17 Future Pack Group

- 6.4.18 Caira International Paperboard

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)