|

市場調查報告書

商品編碼

2061732

亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

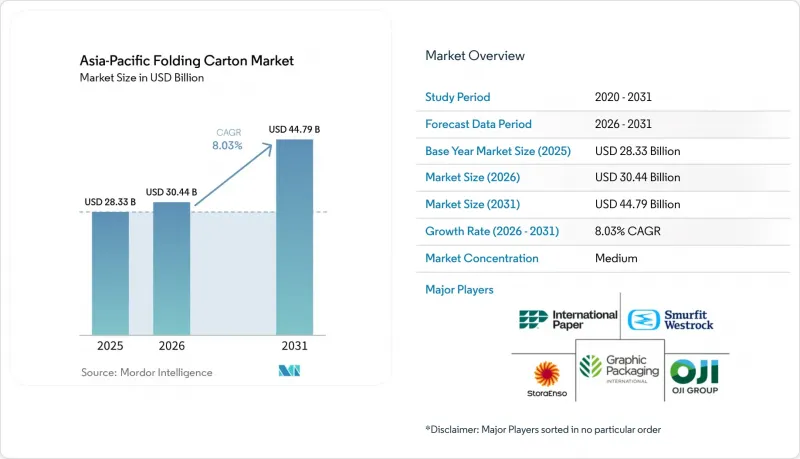

根據 Mordor Intelligence 預測,亞太地區折疊式紙盒市場規模將從 2025 年的 283.4 億美元成長到 2026 年的 304.3 億美元,然後在 2031 年達到 447.9 億美元,2026 年至 2031 年的複合年成長率為 8.03%。

本報告按材料類型(固態漂白硫酸紙漿、折疊紙盒用紙板、未漂白塗佈牛皮紙、白線塑合板等)、印刷技術(膠印、凹版印刷、數位印刷等)、終端用戶行業(個人護理和化妝品、電氣和電子設備等)以及地區進行細分。市場預測以美元(USD)為單位。

亞太地區折疊式紙盒市場趨勢及洞察。

亞洲新興國家食品和飲料消費的成長

亞太地區折疊式紙盒市場最主要的需求仍然是食品和飲料。這主要是因為現代零售、出口通路和調理食品等產品的二次包裝需求日益成長。最大的變化不僅在於消費量的成長,還在於消費者對包裝產品的需求不斷提高,他們希望包裝產品擁有更高的印刷品質、更強的展示效果以及與食品接觸的兼容性,這不僅適用於國內銷售,也適用於出口銷售。越南和印尼的加工商尤其突出,他們擴大滿足國內需求和出口生產相關的加工食品分銷需求。這推動了對更高性能紙板和更可靠加工能力的需求。單份包裝、冷藏包裝和便利包裝的應用範圍也在擴大,尤其是在都市區地區,消費者更傾向於小包裝和頻繁補貨,而不是大量購買。

過渡到永續和可回收的包裝材料

永續性正透過採購決策影響著亞太地區的折疊式紙盒市場,品牌所有者對包裝方案的可回收性、纖維含量以及與自身既定環境目標的契合度都進行了更嚴格的審查。這項轉變意義重大,因為與難以回收或與品牌永續聲明不符的塑膠包裝相比,折疊式紙盒通常更容易滿足這些要求。因此,加工商和品牌所有者之間的對話日益增多,尤其是在高階食品、個人護理和出口型消費品領域。在這些領域,合規性和聲譽在包裝選擇中扮演越來越重要的角色。 Graphic Packaging 透過其「2030願景」計畫強化了這一趨勢,該計畫旨在實現90%的可再生燃料使用和100%採購永續管理的森林產品,這表明永續性績效正成為供應商在包裝領域定位的重要組成部分。隨著這些採購標準在區域供應鏈中的推廣,亞太地區的折疊式紙盒市場正受益於其與可回收、可印刷以及日益優質化的纖維性包裝解決方案的緊密聯繫。

紙板原料價格波動

原物料價格波動仍是亞太地區折疊式紙盒市場最明顯的短期阻礙因素。這是因為,當紙板和紙漿成本的波動速度超過其與主要消費品製造商簽訂的合約價格時,獨立加工商就會受到影響。這種壓力在全部區域分佈不均。依賴進口的市場和缺乏後向整合的加工商,與能夠掌控大部分紙板供應的造紙廠相比,更難控制成本波動。這會對投資行為產生重大影響,因為即使在終端需求強勁的市場,利潤率前景的惡化也會延緩產能擴張。 Smurfit Westrock 發布的 2026 年第一季財報顯示,由於能源成本上漲和需求復甦,該地區箱板紙價格在 2026 年 3 月和 4 月有所上漲,這證實了價格環境依然波動,包裝行業仍然處於成本敏感的環境中。因此,能夠在整個經濟週期中保持利潤率的綜合供應商與面臨標準等級和合約量激烈競爭的中小型加工商之間的差距可能會進一步擴大。

細分市場分析

到2025年,折疊紙板將佔亞太地區折疊式紙盒市場53.78%的佔有率。這反映了該材料在大眾消費品領域中卓越的適用性,這些領域對紙板的剛性、表面品質和大規模生產的高效加工能力都有極高的要求。在亞太地區的大規模包裝項目中,折疊紙板仍然是食品、飲料、家居用品和一般消費品等眾多應用領域的主要基材選擇,因為它在外觀、結構性能和成本之間取得了良好的平衡。其他等級的折疊紙板也同樣重要,例如「塗佈未漂白牛皮紙板」在對撕裂強度要求極高的領域發揮著重要作用,「白襯塑合板」在需要大量使用再生材料的應用中仍然佔據著重要地位,這符合不斷發展的永續發展要求。總體而言,折疊紙板仍然是支撐市場需求的主要材料,尤其是在亞太地區折疊式紙盒市場,該市場依賴規模、印刷品質和成熟加工技術的熟練程度。

預計2026年至2031年間,漂白實心紙板的複合年成長率將達到10.23%,這一增速反映出醫藥、高階個人護理、營養保健品和嬰幼兒營養品等應用領域的需求不斷成長,而非大眾食品等主流市場的需求成長。漂白實心紙板的優勢不僅在於其潔白度和良好的印刷性能,還在於其更均勻的質地、更純淨的纖維結構,以及對安全性、產品形象和精細印刷效果要求極高的應用場景的適用性。因此,漂白實心紙板在亞太折疊式紙盒行業中扮演著重要角色,尤其是在高價值市場,買家願意為性能可靠且符合更嚴格法規的瓦楞紙板支付更高的價格。由此可見,漂白實心紙板的加速成長表明,市場正穩步轉向對法規和品牌價值日益提升的應用領域,而非走向大宗商品化。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務對永續二次包裝的需求日益成長

- 對可回收的硬質塑膠。

- 快餐店的擴張需要客製化印刷的瓦楞紙箱。

- 政府對一次性塑膠製品的監管正加速紙盒的普及。

- 水性阻隔塗層技術的進步提升了食品安全性

- 加工廠的自動化正在推動高產量、低成本的生產。

- 市場限制因素

- 木漿價格波動給造紙企業的利潤率帶來了壓力。

- 嚴格的VOC法規正在推高印刷技術的成本。

- 調理食品形式的彈性包裝競爭

- 新興東協國家缺乏回收基礎設施

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依材料類型

- 固態漂白硫酸漿

- 折疊盒用紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 按地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Graphic Packaging International, LLC

- International Paper Company

- Smurfit WestRock plc

- Stora Enso Oyj

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Nippon Paper Industries Co., Ltd.

- Toppan Holdings Inc.

- Amcor plc

- Huhtamaki Oyj

- Cheng Loong Corporation

- Jiangsu Zhongnan Packaging Co., Ltd.

- Greatview Aseptic Packaging Co., Ltd.

- TCPL Packaging Limited

- Lee and Man Paper Manufacturing Limited

- Siegwerk Druckfarben AG & Co. KGaA

- Parksons Packaging Limited

- SIG Group AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific folding carton market size is expected to grow from USD 28.34 billion in 2025 to USD 30.43 billion in 2026 and is forecast to reach USD 44.79 billion by 2031 at 8.03% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Gravure Printing, Digital Printing, and More), End-User Industry (Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Folding Carton Market Trends and Insights

Growing Food and Beverage Consumption in Emerging Asian Economies

Food and beverage demand remains the clearest volume base for the Asia-Pacific folding carton market because secondary packs for dairy, chilled foods, snacks, beverages, and ready meals are needed across modern retail, export channels, and convenience formats. The greatest change is not only higher consumption, but also a steady shift toward packaged products that require better print quality, stronger shelf impact, and food-contact suitability in both domestic and export sales. Vietnam and Indonesia stand out because converters are increasingly serving packaged food flows linked to both local demand and export manufacturing, which lifts the need for more capable board grades and more reliable finishing capacity. Single-serve, chilled, and convenience-oriented formats are also expanding the application base, especially where urban shopping patterns favor smaller packs and more frequent replenishment rather than larger household purchases.

Shift Toward Sustainable and Recyclable Packaging Materials

Sustainability is influencing the Asia-Pacific folding carton market through procurement decisions, because brand owners now screen packaging options more closely for recyclability, fiber content, and alignment with stated environmental targets. This shift matters because folding cartons often fit those requirements more easily than plastic-heavy formats that carry a more difficult recycling profile or a weaker fit with brand sustainability claims. The result is a broader conversation between converters and brand owners, especially in premium food, personal care, and export-oriented consumer goods, where packaging selection now carries a stronger compliance and reputation dimension. Graphic Packaging has reinforced this direction through its Vision 2030 program, which targets 90% renewable fuel use and 100% sustainably managed purchased forest products, showing how sustainability performance is becoming part of supplier positioning in packaging discussions. As these procurement filters spread across regional supply chains, the Asia-Pacific folding carton market benefits from its close association with recyclable, high-print, and increasingly premium fiber-based packaging solutions.

Volatility In Paperboard Raw Material Prices

Raw material volatility remains the clearest near-term constraint on the Asia-Pacific folding carton market because independent converters are exposed whenever paperboard and pulp costs move faster than contract pricing with large consumer goods customers. The pressure is not evenly distributed across the region, since import-dependent markets and converters without backward integration have less room to manage cost swings than mills that control a greater share of their own board supply. This matters for investment behavior because capacity upgrades can be delayed when margin visibility weakens, even in markets where end demand remains healthy. Smurfit WestRock's first-quarter 2026 results pointed to higher containerboard prices in the region during March and April 2026 due to energy costs and improving demand, confirming that pricing conditions are still moving and that packaging players are operating in a cost environment that remains sensitive. The likely consequence is more differentiation between integrated suppliers that can hold margins through the cycle and smaller converters that compete heavily on standard grades and contract-driven volumes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of E-Commerce and Omni-Channel Retail

- Increasing Pharmaceutical Production and Healthcare Spending

- Competition from Flexible Packaging Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held a 53.78% share of the Asia-Pacific folding carton market in 2025, reflecting the material's strong fit with mass-market consumer goods that need stiffness, surface quality, and efficient conversion across large production runs. It remains the preferred volume substrate in many food, beverage, household, and general consumer applications because it offers a practical balance between appearance, structural performance, and cost across the region's largest packaging programs. Other grades still matter, with Coated Unbleached Kraftboard retaining a role where tear strength is important and White-lined Chipboard staying relevant in more recycled-content-oriented applications that align with evolving sustainability requirements. The broad result is a material mix in which Folding Boxboard continues to anchor mainstream demand, especially in the parts of the Asia-Pacific folding carton market that depend on scale, print quality, and established converting familiarity.

Solid Bleached Board is forecast to grow at a 10.23% CAGR from 2026 to 2031, and that pace reflects rising demand in pharmaceutical, premium personal care, nutraceutical, and infant nutrition applications rather than in the high-volume food mainstream. The appeal of this grade is not only its brightness or print appearance, but also its tighter consistency, cleaner fiber profile, and stronger fit for sensitive end uses where safety, product image, and detailed print performance all matter. This makes Solid Bleached Board especially important in the higher-value layers of the Asia-Pacific folding carton industry, where buyers are willing to pay more for dependable carton performance and stronger compliance alignment. Its faster growth therefore says less about broad commoditized expansion and more about the market's steady movement toward premium substrates in applications where regulation and brand value are both rising.

List of Companies Covered in this Report:

- Graphic Packaging International, LLC

- International Paper Company

- Smurfit WestRock plc

- Stora Enso Oyj

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Nippon Paper Industries Co., Ltd.

- Toppan Holdings Inc.

- Amcor plc

- Huhtamaki Oyj

- Cheng Loong Corporation

- Jiangsu Zhongnan Packaging Co., Ltd.

- Greatview Aseptic Packaging Co., Ltd.

- TCPL Packaging Limited

- Lee and Man Paper Manufacturing Limited

- Siegwerk Druckfarben AG & Co. KGaA

- Parksons Packaging Limited

- SIG Group AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-commerce Demand for Sustainable Secondary Packaging

- 4.2.2 Growing Preference for Recyclable Substitutes to Rigid Plastics

- 4.2.3 Expansion of Quick-Service Restaurants Requiring Custom Printed Cartons

- 4.2.4 Government Bans on Single-Use Plastics Accelerating Carton Adoption

- 4.2.5 Advancements in Water-Based Barrier Coatings Enhancing Food Safety

- 4.2.6 Converting Plant Automation Driving High-Volume, Cost-Effective Output

- 4.3 Market Restraints

- 4.3.1 Volatility in Wood Pulp Prices Compressing Converters' Margins

- 4.3.2 Stringent VOC Regulations Raising Printing Technology Costs

- 4.3.3 Competition From Flexible Packaging in Ready-Meal Formats

- 4.3.4 Limited Recycling Infrastructure in Emerging ASEAN Nations

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia and New Zealand

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Graphic Packaging International, LLC

- 6.4.2 International Paper Company

- 6.4.3 Smurfit WestRock plc

- 6.4.4 Stora Enso Oyj

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Nippon Paper Industries Co., Ltd.

- 6.4.8 Toppan Holdings Inc.

- 6.4.9 Amcor plc

- 6.4.10 Huhtamaki Oyj

- 6.4.11 Cheng Loong Corporation

- 6.4.12 Jiangsu Zhongnan Packaging Co., Ltd.

- 6.4.13 Greatview Aseptic Packaging Co., Ltd.

- 6.4.14 TCPL Packaging Limited

- 6.4.15 Lee and Man Paper Manufacturing Limited

- 6.4.16 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.17 Parksons Packaging Limited

- 6.4.18 SIG Group AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)