|

市場調查報告書

商品編碼

2063709

西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spain Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

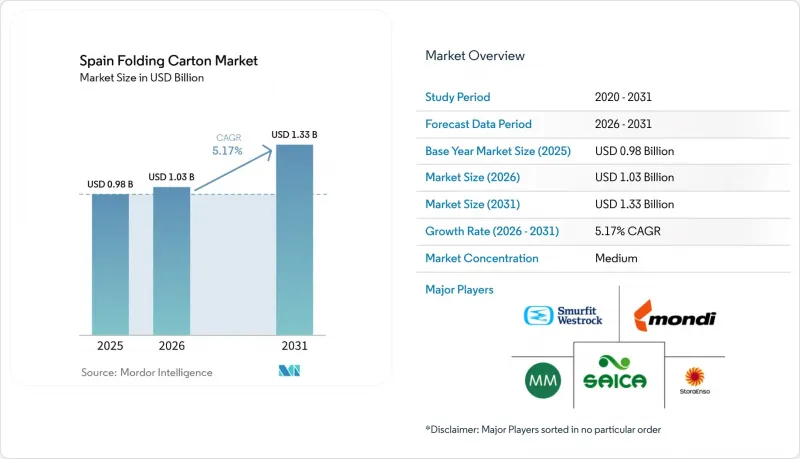

根據 Mordor Intelligence 預測,西班牙折疊式紙盒市場將從 2026 年的 10.3 億美元成長到 2031 年的 13.3 億美元,2026 年至 2031 年的複合年成長率為 5.17%。

本報告按材料類型(未漂白硫酸紙漿、折疊式紙板、塗佈未漂白牛皮紙、白線塑合板等)、印刷技術(膠印、柔版印刷、數位印刷等)和終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品等)進行細分。市場預測以價值(美元)表示。

西班牙折疊式紙盒市場的趨勢與洞察

對永續包裝的需求日益成長

消費者對可回收材料的偏好以及零售法規的推動,正在加速西班牙向纖維基初級和二級包裝的轉變。歐盟包裝和包裝廢棄物法規要求到2030年,包裝材料中再生材料的含量必須達到35%,這迫使品牌商重新設計折疊紙盒,以適應不同尺寸的貨物運輸,並消除混合材料帶來的障礙。諸如ALASKA SMART和ALASKA KRAFT等高品質原生紙漿產品,正以輕盈、點字和食品接觸相容等優勢進行市場推廣。上游工程,像Papkot這樣的塗層新創公司正在資金籌措,以實現無塑膠阻隔材料的商業化,這標誌著一個更深層的創新週期正在形成,進一步強化了西班牙折疊式紙盒市場對永續發展的承諾。

需要二次包裝的電子商務貨運量增加。

2025年,已調理食品出貨量成長7.6%,帶動了零售瓦楞紙箱的需求。其中,Mercadona的即食產品系列成長了24%,覆蓋了其40%的客戶。歐盟法規將紙箱空隙率限制在50%以內,迫使線上經銷商用緊湊型可折疊紙盒取代瓦楞紙運輸箱,從而提升了對整合緩衝設計的興趣。能夠透過數位化平台快速回應設計變更的加工商正在獲得多品種、小批量生產的契約,Saica Fresh於2025年9月推出的符合氣調包裝(MAP)標準的紙盒解決方案就是一個典型的例子。

再生紙板價格波動劇烈

2025年4月,再生紙(OCC)價格大幅上漲,每噸上漲20-30歐元(22-33美元),給加工商的息稅折舊攤銷前利潤(EBITDA)帶來壓力,使西班牙折疊紙盒市場更容易受到上游市場價格波動的影響。辦公用紙回收量的減少以及地緣政治因素導致的運輸中斷,使得短纖維紙漿(SOP)供應趨緊,迫使造紙商通過從斯堪地那維亞進口原生紙漿來規避風險,而進口費用卻很高。這種情況凸顯了在市場中維持成本效益所面臨的日益嚴峻的挑戰。

細分市場分析

2025年,固態漂白硫酸漿(SOP)佔據了西班牙折疊式紙盒市場34.78%的佔有率。其白度高、無異味且符合醫藥法規,鞏固了其市場地位。該細分市場佔據了化妝品、糖果甜點和吸塑包裝用折疊式紙盒的高階價格區間,使加工商免受OCC價格波動的影響。塗佈未漂白牛皮紙是成長最快的紙種,預計到2031年將以7.34%的複合年成長率成長,因為有機食品和手工烘焙品牌正在採用其天然的棕色美感和耐油性。儘管由於對再生材料含量的監管更加嚴格,脫墨工藝的投資有所增加,但折疊紙板和白紋塑合板仍然滿足了冷凍食品和穀物等大規模生產行業的需求,這些行業對成本效益要求極高。

大規模上游項目,例如斯特拉恩佐造紙廠(Strah Enzo)年產75萬噸的PM6重組,確保了西班牙加工商塗佈紙的穩定供應。特殊塗佈紙、微瓦楞紙板和鍍鋁紙板用於高檔烈酒和葡萄酒的包裝,但由於更嚴格的脫金屬要求,其成長速度正在放緩。在西班牙折疊紙盒市場,小眾基材的市場規模仍然小規模,但優質原生紙漿保持著穩固的優勢,尤其是在GLP-1療法包裝這一高成長領域,這主要得益於對防篡改瓶蓋和智慧標籤整合需求的不斷成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對永續包裝的需求日益成長

- 需要二次包裝的電子商務貨運量增加。

- 歐盟和西班牙對一次性塑膠製品有嚴格的規定

- 輕質板材在物流的成本優勢

- 西班牙冷藏調理食品市場快速擴張

- 供應鏈數位化實現了小批量印刷。

- 市場限制因素

- 再生紙板價格波動劇烈

- 零食產業軟包裝的競爭

- 供不應求

- 品牌擁有者不願採用需要大量投資的數位印刷機。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 可折疊紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- Saica Pack SL

- Edelmann Group

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Autajon Group

- Fedrigoni Group

- Hinojosa Packaging Group

- Cartonajes VIR

- Mondi plc

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain folding carton market size is projected to expand from USD 1.03 billion in 2026 to USD 1.33 billion by 2031, registering a 5.17% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Folding Carton Market Trends and Insights

Growing Demand for Sustainable Packaging

Consumer preference for recyclable materials and retailer mandates are accelerating Spain's shift toward fiber-based primary and secondary packs. The EU Packaging and Packaging Waste Regulation requires 35% post-consumer recycled content by 2030, pushing brand owners to redesign folding cartons for right-sized deliveries and to eliminate mixed-material barriers. Premium virgin-fiber grades such as ALASKA SMART and ALASKA KRAFT are marketed as lighter yet Braille-ready options that keep food-contact approvals intact. Upstream, coating start-ups like Papkot are securing capital to commercialize plastic-free barriers, signaling a deeper innovation cycle that reinforces the Spanish folding carton market's sustainability narrative.

Rising E-commerce Shipments Requiring Secondary Packaging

Prepared-food volumes grew 7.6% in 2025, driving up retail-ready carton demand, particularly from Mercadona, whose ready-to-eat range expanded 24% and now reaches 40% shopper penetration. The EU regulation capping void space at 50% forces online merchants to replace corrugated shippers with compact folding cartons, spurring interest in integrated cushioning designs. Converters that can deliver rapid artwork changes through digital platforms are winning high-mix, low-volume contracts, as exemplified by Saica Fresh's MAP-compatible carton solution launched in September 2025.

Volatile Recycled Paperboard Prices

April 2025 OCC spikes of EUR 20-30 per metric ton (USD 22-33 per metric ton) squeezed converter EBITDA, exposing the Spain folding carton market to upstream volatility. Declining office paper collection and geopolitical freight disruptions have tightened SOP supply, compelling mills to hedge by importing Scandinavian virgin fiber at higher freight premiums. This situation underscores the growing challenges in maintaining cost efficiency within the market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent EU and Spanish Regulations on Single-Use Plastics

- Cost Advantages of Lightweight Board for Logistics

- Competition from Flexible Packaging in Snack Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate held 34.78% of the Spain folding carton market share in 2025, a position secured by its white optics, odor neutrality, and pharmaceutical compliance credentials. The segment captures premium price points in cosmetics, confectionery, and blister folding cartons, cushioning converters against OCC price swings. Coated Unbleached Kraft is scaling fastest at a 7.34% CAGR through 2031, as organic food and artisan bakery brands adopt its natural-brown aesthetics and grease resistance. Folding Boxboard and White Line Chipboard satisfy high-volume frozen-food and cereal categories where cost efficiency prevails, even as regulatory recycled-content thresholds raise de-inking investments.

Large upstream projects, such as Stora Enso's 750,000-metric ton PM6 rebuild, ensure a stable supply of coated grade for Spanish converters. Coated specialty grades, micro-flute corrugated, and metalized boards serve luxury spirits and wine but face stricter demetallization requirements, slowing their momentum. The Spain folding carton market size for niche substrates remains modest, yet heightened demand for tamper-evident closures and smart-label integration is giving premium virgin fibers a defensible edge, particularly in high-growth GLP-1 therapy packaging.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- Saica Pack SL

- Edelmann Group

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Autajon Group

- Fedrigoni Group

- Hinojosa Packaging Group

- Cartonajes VIR

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Sustainable Packaging

- 4.2.2 Rising E-commerce Shipments Requiring Secondary Packaging

- 4.2.3 Stringent EU and Spanish Regulations on Single-Use Plastics

- 4.2.4 Cost Advantages of Lightweight Board for Logistics

- 4.2.5 Rapid Expansion of Spain's Chilled Ready-Meals Segment

- 4.2.6 Digitization of Supply Chains Enabling Short Print Runs

- 4.3 Market Restraints

- 4.3.1 Volatile Recycled Paperboard Prices

- 4.3.2 Competition from Flexible Packaging in Snack Formats

- 4.3.3 Limited Domestic Hardwood Pulp Availability

- 4.3.4 Brand Owner Reluctance Toward High-CapEx Digital Presses

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International LLC

- 6.4.4 International Paper Company

- 6.4.5 Saica Pack SL

- 6.4.6 Edelmann Group

- 6.4.7 Mayr-Melnhof Karton AG

- 6.4.8 Stora Enso Oyj

- 6.4.9 Autajon Group

- 6.4.10 Fedrigoni Group

- 6.4.11 Hinojosa Packaging Group

- 6.4.12 Cartonajes VIR

- 6.4.13 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)