|

市場調查報告書

商品編碼

2063810

菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Philippines Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

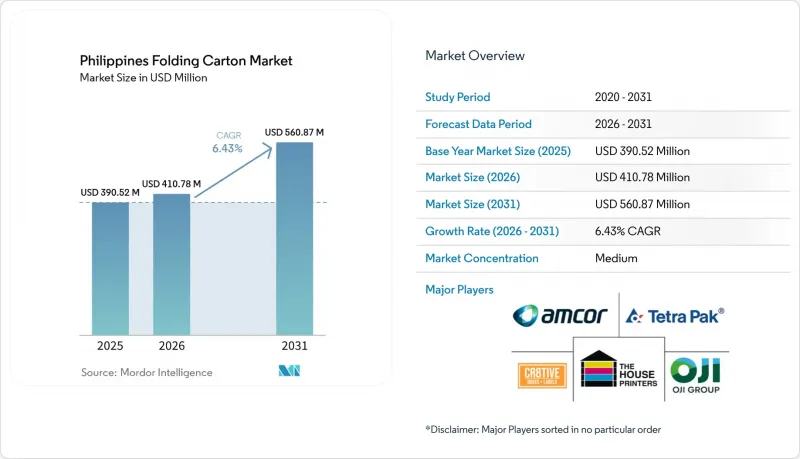

根據 Mordor Intelligence 預測,菲律賓折疊式紙盒市場規模將從 2026 年的 4.1078 億美元成長到 2031 年的 5.6087 億美元,2026 年至 2031 年的複合年成長率為 6.43%。

本報告按材料類型(固態漂白硫酸紙漿、折疊式紙板、塗佈未漂白牛皮紙、白線塑合板等)、印刷技術(膠印、凹版印刷、數位印刷等)和終端用戶行業(食品飲料、個人護理及化妝品、電氣電子設備等)進行細分。市場預測以美元計價。

菲律賓折疊式紙盒市場趨勢及洞察

電子商務包裝需求不斷成長

線上生鮮服務和D2C(直接面對消費者)品牌要求使用防篡改封條和可變數據印刷技術,以創造個人化的開箱體驗。雲端連鎖餐廳正在加大投資,並依賴可在數日內而非數週內採購的快速配送瓦楞紙箱。菲律賓貿易和工業部的報告顯示,78%的菲律賓消費者在線網路購物時永續性,這促使履約中心指定使用可回收紙板而非塑膠袋。物流供應商強調,纖維基瓦楞紙板可以降低體積重量費用,並且在成熟市場中可透過79%的家庭垃圾回收系統進行回收。考慮到國內燃料價格的波動,這無疑是一個令人信服的論點。

食品和飲料加工產業的擴張

2024年至2026年間,超過200億披索(約3.52億美元)的投資用於擴大冷凍食品、餅乾、椰子製品和調味品的國內產能。這些項目主要集中在呂宋島的低溫運輸基礎設施建設上,以確保對符合FDA標準的塗層未漂白牛皮紙板(帶防潮層)的穩定需求。隨著加工商加強審核流程,擁有食品接觸基材認證的加工商作為供應商的優先順序正在提升。 2025年10月推出的產品註冊證書(ECTA)提高了人們對產品可追溯性的期望,這將有利於已實施數位批號編碼的工廠。

紙板價格波動

2026年2月,基準紙漿價格上漲至每噸740美元,六個月內漲幅達15%。這擠壓了加工商的利潤空間,觸發了季度價格調整條款。菲律賓加工商幾乎全部依賴進口原生紙漿,因此極易受到運費上漲和外匯波動的影響。儘管目前庫存水準較高,但過剩的庫存正在加劇營運資金緊張,這對信貸額度有限的中小型印刷企業而言尤其嚴峻。這種情況使得加工商難以提供固定價格契約,而固定價格合約正是許多消費品公司所青睞的。在區域紙漿供應穩定之前,成本轉嫁不均的情況可能會持續存在。

細分市場分析

到2025年,未漂白塗佈牛皮紙將佔據菲律賓折疊式紙盒市場32.83%的佔有率,這主要得益於其可回收性和適用於食品接觸環境的特性。預計未漂白塗佈牛皮紙的複合年成長率將達到7.76%,超過所有其他材料,這主要得益於高階化妝品和藥品市場的發展,這些產品需要高亮度基材和防篡改密封。隨著冷凍食品和快餐店(QSR)的成長,菲律賓未漂白塗佈牛皮紙折疊式紙盒的市場規模也將擴大。為口服固態採購紙匣的製藥企業已經開始指定兒童安全設計,而這種設計往往傾向於使用高檔漂白紙板。

未漂白硫酸鹽紙漿板也受益於高階飾面(例如壓紋和金屬裝飾)在百貨公司和電商平台銷售的護膚品系列中日益成長的需求。折疊式紙板為乾貨和中等價位的家居用品提供了一種經濟實惠的選擇,而白色襯裡的塑合板仍然用於鞋盒和工業包裝,在這些領域,價格比美觀更重要。由於生產者延伸責任制 (EPR) 的要求,品牌所有者越來越需要在包裝正面的圖形上標註可回收性評分,因此,採用含再生材料的等級正在逐步推進。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 食品飲料加工部門的擴張

- 電子商務包裝需求不斷成長

- 對永續包裝解決方案的需求日益成長

- 擴大數位印刷在小批量瓦楞紙箱中的應用。

- 政府對塑膠包裝徵收銷售稅,這促使包裝材料轉向紙板。

- 雲端廚房和食材自煮包新創公司的快速發展,推動了對小批量紙盒包裝的需求成長。

- 市場限制因素

- 紙板價格波動

- 來自軟性包裝替代品的競爭

- 國內紙漿產量有限,導致對進口的依賴性日益增強。

- 停電增加了轉換器的生產成本。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tetra Pak(Philippines), Inc.

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Amcor plc

- Printwell Inc.

- VJ7 Printing and Packaging Inc.

- Papercon Philippines Inc.

- The House Printers Corporation

- Majestic Press Inc.

- Apo International Marketing Corporation

- Grand C Graphics Inc.

- Starkson Packaging Inc.

- Fortune Packaging Corporation

- Megaprint Offset and Packaging Corp.

- Cr8tive Boxes & Labels Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the philippines folding carton market size is projected to expand from USD 410.78 million in 2026 to USD 560.87 million by 2031, registering a 6.43% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Gravure Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Philippines Folding Carton Market Trends and Insights

Growth of E-commerce Packaging Demand

Online grocery services and direct-to-consumer brands request tamper-evident seals and variable-data printing that personalize unboxing experiences. Cloud-based restaurant chains have secured fresh investment and rely on short-run cartons that can be sourced within days rather than weeks. The Department of Trade and Industry reports that 78% of Filipino consumers value sustainability when shopping online, encouraging fulfillment centers to specify recyclable paperboard in place of plastic pouches. Logistics providers highlight that fiber-based cartons lower dimensional-weight charges and offer 79% curbside recycling access in mature markets, a persuasive argument as domestic fuel costs remain volatile.

Expansion of Food and Beverage Processing Sector

More than PHP 20 billion (USD 352 million) has been deployed between 2024 and 2026 to enlarge domestic capacity for frozen foods, biscuits, coconut products, and seasonings. These projects cluster around cold-chain infrastructure in Luzon, locking in steady volumes of FDA-compliant, coated, unbleached kraft cartons with moisture barriers. Converters that certify substrates for food contact gain preferred-supplier status as processors tighten audit protocols. Adoption of electronic Certificates of Product Registration starting October 2025 increases traceability expectations, benefitting plants equipped with digital lot-coding.

Volatility in Paperboard Prices

Benchmark pulp climbed to USD 740 per ton in February 2026, a 15% jump in six months, tightening converter margins and triggering quarterly price-adjustment clauses. Philippine converters import nearly all virgin fiber, leaving them exposed to freight spikes and foreign-exchange swings. Inventories now run higher, but carrying extra stock strains working capital, especially for small printers whose credit lines are capped. Those conditions complicate converters' ability to offer fixed-price contracts, which many consumer-goods companies prefer. Until regional pulp supply stabilizes, cost pass-through will remain uneven.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Sustainable Packaging Solutions

- Increased Adoption of Digital Printing

- Limited Domestic Pulp Production Increasing Import Dependence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated unbleached kraft captured 32.83% of the Philippines folding carton market share in 2025 on the strength of its recyclability and suitability for food-contact applications. Solid bleached sulfate is forecast to outpace all other materials at a 7.76% CAGR, buoyed by premium cosmetics and pharmaceutical launches that require high-brightness substrates and tamper-evident seals. The Philippines folding carton market size attributed to coated unbleached kraft will rise in parallel with frozen food and quick-service restaurant growth. Pharmaceutical producers sourcing cartons for oral solids already specify child-resistant designs that favor premium bleached board.

Solid bleached sulfate benefits further from rising demand for deluxe finishes such as embossing and metallic accents in skin-care lines distributed through department stores and e-commerce platforms. Folding boxboard provides a cost-effective option for dry groceries and mid-tier household goods, while white-lined chipboard persists in shoe boxes and industrial packs where aesthetics rank below price. Recycled-content grades make incremental headway as EPR compliance drives brand owners to publish recyclability scores on front-of-pack graphics.

List of Companies Covered in this Report:

- Tetra Pak (Philippines), Inc.

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Amcor plc

- Printwell Inc.

- VJ7 Printing and Packaging Inc.

- Papercon Philippines Inc.

- The House Printers Corporation

- Majestic Press Inc.

- Apo International Marketing Corporation

- Grand C Graphics Inc.

- Starkson Packaging Inc.

- Fortune Packaging Corporation

- Megaprint Offset and Packaging Corp.

- Cr8tive Boxes & Labels Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Food and Beverage Processing Sector

- 4.2.2 Growth of E-commerce Packaging Demand

- 4.2.3 Rising Demand for Sustainable Packaging Solutions

- 4.2.4 Increased Adoption of Digital Printing for Short-Run Cartons

- 4.2.5 Government Excise Tax on Plastic Packaging Spurring Shift Toward Paperboard

- 4.2.6 Rapid Growth of Cloud Kitchen and Meal-Kit Start-ups Requiring Small-Batch Cartons

- 4.3 Market Restraints

- 4.3.1 Volatility in Paperboard Prices

- 4.3.2 Competition From Flexible Packaging Alternatives

- 4.3.3 Limited Domestic Pulp Production Increasing Import Dependence

- 4.3.4 Power Supply Interruptions Elevating Production Costs for Converters

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Tetra Pak (Philippines), Inc.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Stora Enso Oyj

- 6.4.4 Rengo Co., Ltd.

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Amcor plc

- 6.4.7 Printwell Inc.

- 6.4.8 VJ7 Printing and Packaging Inc.

- 6.4.9 Papercon Philippines Inc.

- 6.4.10 The House Printers Corporation

- 6.4.11 Majestic Press Inc.

- 6.4.12 Apo International Marketing Corporation

- 6.4.13 Grand C Graphics Inc.

- 6.4.14 Starkson Packaging Inc.

- 6.4.15 Fortune Packaging Corporation

- 6.4.16 Megaprint Offset and Packaging Corp.

- 6.4.17 Cr8tive Boxes & Labels Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)