|

市場調查報告書

商品編碼

2063760

北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

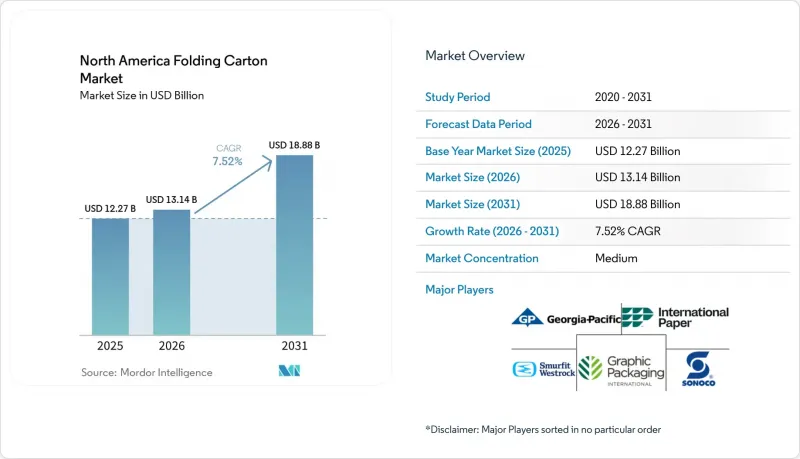

根據 Mordor Intelligence 預測,北美折疊式紙匣市場規模將從 2025 年的 122.7 億美元和 2026 年的 131.4 億美元成長到 2031 年的 188.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 7.52%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、未漂白塗佈牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷等)、終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣電子設備等)以及地區進行細分。市場預測以美元計價。

北美折疊式紙盒市場趨勢與洞察

電子商務出貨量的激增催生了對適合商店展示的包裝的需求。

電商零售商現在要求供應商交付折疊式紙盒,以便直接從收貨區搬運到商店貨架,無需二次搬運。亞馬遜、沃爾瑪和塔吉特已強制要求到2025年採用可掃描的預印刷瓦楞紙板規格。這迫使加工商投資於支援RFID標籤的高解析度數位印刷和膠印設備。當日交貨是一項關鍵的差異化優勢,在北美折疊式紙盒市場,那些在其履約中心附近配備自動化模切機的加工商正在不斷擴大市場佔有率。這種影響在墨西哥也日益顯著,蒙特雷和瓜達拉哈拉等地正在形成新的製造群,對本地生產的即用型包裝的需求也日益成長。

人們越來越偏好永續紡織材料來取代塑膠。

加州和加拿大的「生產者延伸責任法案」正迫使品牌商從塑膠轉向可回收紙板,從而推高了對經森林管理委員會 (FSC) 和永續林業計劃 (SFI) 認證的高品質纖維的需求。斯特拉勒恩索 (Strahler Enso) 的 Performa Lumi 紙板具有高印刷性和高再生材料含量,預計將在 2025 年前被化妝品行業廣泛採用。一體化製造商正在其所有產品系列中推行「塑膠換紙」計劃,進一步擴大了北美折疊式紙盒市場的規模。

再生纖維供應價格的波動

由於中國造紙廠關閉以及亞洲新的出口限制,廢紙供應減少,導致北美再生紙板價格連續幾季出現兩位數波動。擁有生活垃圾收集和紙漿廠的綜合生產商透過簽訂長期纖維合約來保護利潤率,這使得北美折疊式瓦楞紙板的市場佔有率集中在少數幾家大型企業手中。這種價格波動促使品牌擁有者調整籌資策略,優先選擇纖維來源穩定、價格透明的供應商。

細分市場分析

預計白紋紙板將以7.94%的複合年成長率成長,超過7.52%的整體市場成長率,這主要得益於電商零售商擴大採用其低光澤度,用於二次加工和商店展示。到2025年,固態漂白硫酸漿(SBS)仍將以34.21%的佔有率佔據北美折疊式紙盒市場的最大佔有率,這主要得益於藥品和化妝品對序列化包裝的需求。由於Smurfit Westrock關閉了位於魁北克的SBS生產線,導致供應緊張和價格管制收緊,加工商正轉向對印刷精度要求較低的塑合板。雖然食品飲料產業對折疊式紙盒的訂單依然強勁,但零食品牌為了方便攜帶,仍在繼續使用輕便的包裝袋。未漂白的塗佈牛皮紙則用於小眾有機食品的標籤,因為這些食品偏好天然的棕色。整體而言,材料選擇正從對傳統基材的執著轉向對總交付成本和可回收性認證的關注。隨著品牌所有者優先事項的改變,能夠快速切換材料等級的加工商可以在北美折疊式紙盒市場抓住新的商機。

在美國,對白紋紙板的需求最為顯著,預計到2025年,電子商務在美國零售額的滲透率將超過15%。零售商對成本控制的關注促使品牌所有者轉向成本較低的基材,同時又不影響展示效果。在墨西哥,近岸外包技術的進步提高了人們對消費性電子產品瓦楞紙箱可以抵消不斷上漲的物流成本。在加拿大,雖然對用於受監管藥品的優質SBS紙板的需求依然強勁,但不斷上漲的運費和強勢的美元正促使人們考慮將塑合板作為替代方案。隨著供應鏈日益本地化,能夠從單一廠區供應多種等級紙板的造紙廠可以更快地調整產量,維持利潤率,並深化其在北美折疊式紙盒市場的參與度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務出貨量的激增催生了對可在商店展示的包裝的需求。

- 人們對以永續纖維為基礎的塑膠替代品越來越感興趣。

- 減輕紙板重量以降低物流成本

- 水性阻隔塗層技術的進步使得冷凍食品紙盒的生產成為可能。

- 高速模切和黏合生產線的自動化

- 零售商對可掃描且影像清晰的包裝的要求

- 市場限制因素

- 再生纖維供應價格的波動

- 零嘴零食領域與軟包裝袋形式的競爭

- 遵守 PFAS 法規需要大量資本投資

- 數位印刷在大規模印刷領域商業性擴張的限制。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 國家

- 美國

- 墨西哥

- 加拿大

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- International Paper Company

- Georgia-Pacific LLC

- Sonoco Products Company

- Huhtamaki Oyj

- Packaging Corporation of America

- Cascades Inc.

- Pratt Industries Inc.

- Rengo Co., Ltd.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Multi Packaging Solutions International LLC

- Caraustar Industries, Inc.(Greif, Inc.)

- Americraft Carton, Inc.

- Edelmann Group

- Great Little Box Company Ltd.

- Unicorr Packaging Group

- Bell Incorporated

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america folding cartons market size is projected to expand from USD 12.27 billion in 2025 and USD 13.14 billion in 2026 to USD 18.88 billion by 2031, registering a CAGR of 7.52% between 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Folding Carton Market Trends and Insights

Surge in E-Commerce Shipments Requiring Shelf-Ready Packaging

E-commerce retailers now ask suppliers to deliver folding cartons that move straight from inbound docks to store shelves, eliminating secondary handling. Amazon, Walmart, and Target introduced mandatory scannable, pre-printed carton specifications in 2025, prompting converters to invest in high-graphic digital and litho printing that supports RFID tagging. Same-day turnaround has become a decisive differentiator, and converters with automated die-cutters near fulfillment hubs are gaining a growing share of the North America folding cartons market. Mexico is feeling the pull as new manufacturing clusters in Monterrey and Guadalajara demand localized, shelf-ready packaging.

Growing Preference for Sustainable Fiber-Based Substitutes to Plastics

Extended producer responsibility laws in California and Canada compel brands to switch from plastic to recyclable paperboard, lifting demand for premium fiber grades certified by the Forest Stewardship Council and the Sustainable Forestry Initiative. Stora Enso's Performa Lumi paperboard achieved broad adoption in cosmetics by 2025 because it pairs high graphic fidelity with high recycled content. Integrated producers have responded with portfolio-wide "plastic-to-paper" programs, further enlarging the North America folding cartons market footprint.

Volatility in Recycled Fiber Supply Prices

Mill closures in China and new Asian export restrictions cut recovered-paper availability, pushing North American recycled-paperboard prices up or down by double digits in back-to-back quarters. Integrated producers that control curbside collection and possess pulp mills lock in long-term fiber contracts, shielding margins and concentrating North America's folding cartons market share among the top tier. This volatility is also prompting brand owners to diversify sourcing strategies and prioritize suppliers with stable fiber access and pricing visibility.

Other drivers and restraints analyzed in the detailed report include:

- Advances in Water-Based Barrier Coatings Enabling Frozen Food Cartons

- Automation of High-Speed Die-Cutting and Gluing Lines

- Capital-Intensive Compliance With PFAS Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White Line Chipboard is projected to grow at a 7.94% CAGR, outpacing the overall 7.52% expansion, as e-commerce retailers accept its lower brightness for secondary and shelf-ready applications. Solid Bleached Sulfate retained the largest 34.21% share of the North America folding cartons market in 2025, a position secured by pharmaceutical and cosmetic serialization demands. Supply tightened when Smurfit WestRock shuttered its Quebec SBS machine, lifting price discipline and nudging converters toward chipboard when print fidelity is less critical. Folding Boxboard maintains steady food and beverage orders, yet snack brands continue to migrate to lightweight pouches for on-the-go convenience. Coated Unbleached Kraft serves niche organic food labels that value the natural brown appearance. Overall, material decisions now pivot more on total delivered cost and recyclability certification than on historical substrate loyalties. Converters that can switch grades quickly capture incremental opportunities in the North America folding carton market as brand-owner priorities evolve.

Demand for White Line Chipboard is most visible in the United States, where e-commerce penetration breached 15% of retail sales in 2025. Retailers' focus on cost control encourages brand owners to trade down to a lower-cost substrate without sacrificing shelf impact. In Mexico, nearshoring has sparked interest in chipboard for consumer electronics cartons, as a low-cost substrate offsets higher logistics overhead. Canada continues to support premium SBS for regulated pharmaceuticals, but rising freight costs and a strong U.S. dollar are opening conversations about chipboard substitution. As supply chains regionalize, mills able to furnish multiple grades from a single complex can rebalance output faster, protecting margins and deepening engagement across the North America folding cartons market.

List of Companies Covered in this Report:

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- International Paper Company

- Georgia-Pacific LLC

- Sonoco Products Company

- Huhtamaki Oyj

- Packaging Corporation of America

- Cascades Inc.

- Pratt Industries Inc.

- Rengo Co., Ltd.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Multi Packaging Solutions International LLC

- Caraustar Industries, Inc. (Greif, Inc.)

- Americraft Carton, Inc.

- Edelmann Group

- Great Little Box Company Ltd.

- Unicorr Packaging Group

- Bell Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-commerce Shipments Requiring Shelf-Ready Packaging

- 4.2.2 Growing Preference for Sustainable Fiber-Based Substitutes to Plastics

- 4.2.3 Lightweighting of Paperboard to Cut Logistics Costs

- 4.2.4 Advances in Water-Based Barrier Coatings Enabling Frozen Food Cartons

- 4.2.5 Automation of High-Speed Die-Cutting and Gluing Lines

- 4.2.6 Retailer Mandates for Scannable, High-Graphic Packaging

- 4.3 Market Restraints

- 4.3.1 Volatility in Recycled Fiber Supply Prices

- 4.3.2 Competition From Flexible Pouch Formats in Snacks

- 4.3.3 Capital-Intensive Compliance With PFAS Regulations

- 4.3.4 Limited Commercial Scaling of Digital Print for Long Runs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Mexico

- 5.4.3 Canada

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Graphic Packaging Holding Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 International Paper Company

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Sonoco Products Company

- 6.4.6 Huhtamaki Oyj

- 6.4.7 Packaging Corporation of America

- 6.4.8 Cascades Inc.

- 6.4.9 Pratt Industries Inc.

- 6.4.10 Rengo Co., Ltd.

- 6.4.11 Mayr-Melnhof Karton AG

- 6.4.12 AR Packaging Group AB

- 6.4.13 Multi Packaging Solutions International LLC

- 6.4.14 Caraustar Industries, Inc. (Greif, Inc.)

- 6.4.15 Americraft Carton, Inc.

- 6.4.16 Edelmann Group

- 6.4.17 Great Little Box Company Ltd.

- 6.4.18 Unicorr Packaging Group

- 6.4.19 Bell Incorporated

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)