|

市場調查報告書

商品編碼

2063776

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Singapore Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

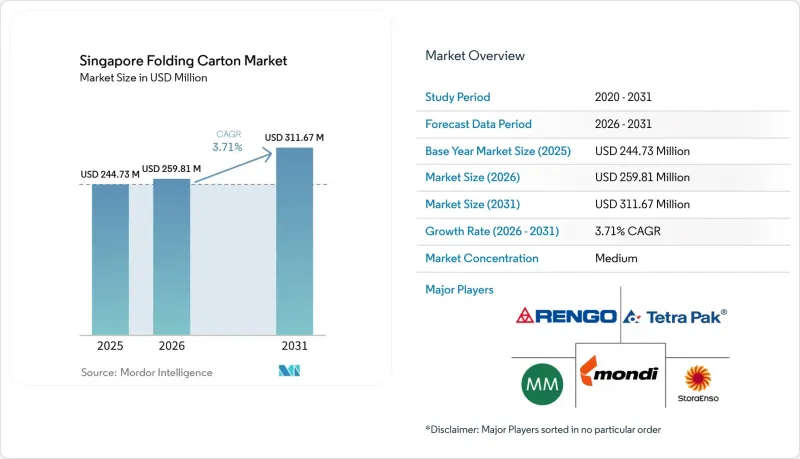

根據 Mordor Intelligence 預測,新加坡可折疊瓦楞紙板市場規模預計到 2025 年將達到 2.4473 億美元,到 2026 年將達到 2.5981 億美元,到 2031 年將達到 3.1167 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 3.71%。

本報告按材料類型(固態漂白硫酸漿、折疊紙盒用紙板、未漂白塗佈牛皮紙、白線塑合板等)、印刷技術(膠印、凹版印刷、數位印刷等)和終端用戶行業(食品飲料、電子電氣設備、個人護理和化妝品等)進行細分。市場預測以美元計價。

新加坡折疊紙盒市場趨勢及洞察

電子商務包裝需求激增

由於新加坡作為區域履約中心,數位零售商可以將庫存集中存放於保稅倉庫,重新貼標產品,並在48小時內出貨給東協地區的買家。跨國小包裹通常至少使用一層瓦楞紙箱,因此交易量的成長直接帶動了新加坡瓦楞紙箱市場的需求成長。為了最大限度地降低退貨成本,電商企業要求紙箱具備防篡改設計、嵌入式QR碼和堅固的邊角保護。配備自動化CAD庫和數位印刷機的加工商能夠在幾天內完成3000至15000個瓦楞紙箱的交貨、校對和交付,從而確保訂單的順利完成。

政府推廣永續包裝和“2030年綠色計劃”

包裝報告要求以及2026年將掩埋量減少20%的暫定目標,正在加速企業向可回收材料的轉型。能夠證明其產品擁有FSC產銷監管鏈(CoC)認證並達到最低再生纖維使用量的折疊紙盒製造商,如今已成為在新加坡運營的全球快速消費品買家的首選供應商。許多飲料品牌也開始使用紙盒取代聚對苯二甲酸乙二醇酯(PET)多包裝環,利用了紙盒免繳飲料容器押金的監管漏洞。

高昂的地租和人事費用限制了當地的生產能力。

儘管工業租金持續上漲,但勞工改革導致最低工資和稅收增加,推高了加工商的固定成本。因此,新加坡龐大的折疊式紙盒市場需要兩條供應路線:一是從馬來西亞和印尼採購通用紙盒,二是本地工廠專注於小批量生產、高階產品或涉及智慧財產權的項目。對機器人模切和人工智慧視覺系統的自動化投資旨在彌合成本差距,但這需要大量的初始投資。

細分市場分析

2025年,塗佈未漂白牛皮紙在新加坡折疊瓦楞紙板市場佔33.87%的佔有率。這主要歸功於其優異的濕強度和阻隔塗層,使其成為飲料容器、冷凍食品包裝套和油性零食包裝的理想選擇。此等級的牛皮紙符合市政回收系統的要求,並通過了FSC認證,符合品牌所有者在「2030綠色計畫」下的承諾。同時,預計到2031年,折疊瓦楞紙板的複合年成長率將達到5.53%,高於整體市場成長。其光滑的黏土塗層表面、優異的白度和高剛性使其能夠進行壓紋、燙金和清晰的膠印,這些工藝深受高階化妝品和營養補充劑品牌的青睞。同時儲備這兩種基材的加工商可以提案最佳的紙張重量、阻隔層壓和裝飾後處理方案,從而強化其諮詢服務,並隨著平均售價(ASP)的上漲,在新加坡折疊瓦楞紙箱市場獲得更大的佔有率。

在醫藥紙盒市場,由於嚴格的純度和光學要求限制了替代品的選擇,對固態漂白硫酸漿(SBS)的需求仍然強勁。白線塑合板則用於經濟實惠的家用產品,它利用回收材料,既能滿足企業永續發展指標,又能降低每噸成本。特殊等級的塑合板,例如帶有分散塗層和植物來源聚合物襯裡的紙板,適用於微波爐適用食品托盤和調節氣體包裝(MAP),但目前由於認證週期的限制,產量有限。隨著高階糖果甜點進口商更加重視產品開箱展示效果以支撐更高的價格,可折疊紙板的紋理表面和結構剛性正成為至關重要的因素。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電子商務包裝需求激增

- 政府關於永續包裝的計劃和“2030年綠色計劃”

- 人們對已調理食品宅配的需求日益成長,推動了可折疊紙箱的使用。

- 小批量印刷的數位印刷技術進步

- 人口老化推動了對高階醫療包裝日益成長的需求。

- 品牌所有者從塑膠轉向紙張

- 市場限制因素

- 高昂的土地和人事費用限制了當地的生產能力。

- 來自馬來西亞和中國的低成本進口商品的競爭。

- 日本再生纖維供不應求阻礙了再生紙板的廣泛應用。

- 原生紙板價格隨全球紙漿市場波動。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 未漂白工藝服

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Tetra Pak International SA

- Mayr-Melnhof Karton AG

- Rengo Co. Ltd

- Stora Enso Oyj

- Mondi plc

- Muda Packaging Industries Sdn Bhd

- Seow Khim Polythelene Pte Ltd.

- Toyo Ink Pte Ltd.

- LSY Packaging Pte Ltd.

- Paper Products Singapore(Pte)Ltd.

- Amcor plc

- International Paper Company

- Graphic Packaging International LLC

- Oji Holdings Corporation

- Smurfit Westrock plc

- Huhtamaki Oyj

第7章 市場機會與未來展望

According to Mordor Intelligence, the singapore folding carton market size is projected to be USD 244.73 million in 2025, USD 259.81 million in 2026, and reach USD 311.67 million by 2031, growing at a CAGR of 3.71% from 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Gravure Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Electrical and Electronics, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Folding Carton Market Trends and Insights

Surge in E-Commerce Packaging Demand

Singapore's position as a regional fulfillment nexus allows digital retailers to consolidate inventory in bonded warehouses, re-label products, and ship within 48 hours to ASEAN shoppers. Each cross-border parcel typically uses at least one secondary folding carton, so transaction growth directly translates into additional tonnage for the Singapore folding carton market. E-tailers insist on tamper-evident designs, embedded QR codes, and robust corner protection to minimize return costs. Converters with automated CAD libraries and digital presses win these orders because they can quote, proof, and deliver runs of 3,000-15,000 cartons within a few days.

Government Push for Sustainable Packaging and Green Plan 2030

Mandatory Packaging Reporting and the interim 20% landfill-reduction target for 2026 accelerate corporate moves toward recyclable substrates. Folding-carton producers able to document Forest Stewardship Council (FSC) chain-of-custody status and minimum recycled-fiber thresholds now enjoy preferred-supplier status with global FMCG buyers operating in Singapore. Many beverage brands also use folding cartons to replace polyethylene terephthalate (PET) multipack rings, taking advantage of a regulatory gap because cartons currently fall outside the beverage-container deposit scheme.

High Land and Labor Costs Limiting Local Production Capacity

Industrial rents keep trending higher while labor reforms raise minimum salaries and levies, inflating fixed costs for converters. The larger Singapore folding carton market must therefore be served through a two-track supply chain: regionally produced commodity cartons flow in from Malaysia and Indonesia, while local plants concentrate on short-run, premium, or IP-sensitive jobs. Automation investments in robotic die-cutting and AI vision systems aim to close the cost gap but require significant upfront capital.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Ready-to-Eat Meal Deliveries Boosting Folding Carton Usage

- Technological Advancements in Digital Printing for Short Runs

- Competition From Lower-Cost Imports From Malaysia and China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated Unbleached Kraft captured 33.87% of the Singapore folding carton market share in 2025 as beverage carriers, frozen-food sleeves, and greasy snack packs favor its wet strength and barrier coatings. The grade fits within municipal recycling streams and carries FSC tags, aligning with brand-owner pledges under the Green Plan 2030. Folding Boxboard, however, is pegged to outpace overall market growth at a 5.53% CAGR to 2031. Its smooth, clay-coated surface, superior brightness, and high stiffness support embossing, foil stamping, and crisp offset graphics demanded by premium cosmetics and nutraceutical brands. Converters that stock both substrates can recommend optimal grammage, barrier lamination, and post-press embellishment, strengthening their consultative role and capturing a larger share of the Singapore folding carton market as ASPs rise.

Demand for Solid Bleached Sulfate remains sticky in pharmaceutical cartons where stringent purity and optical requirements limit substitution. White Line Chipboard serves low-budget household goods, leveraging recycled content to satisfy corporate sustainability metrics at a lower cost per ton. Specialty grades, including dispersion-coated and plant-based polymer-lined boards, address microwave-safe food trays and modified-atmosphere packs, though volumes are currently limited by qualification cycles. As importers of luxury confectionery lean on unboxing theatrics to justify premium price tags, Folding Boxboard's tactile finish and structural rigidity become decisive.

List of Companies Covered in this Report:

- Tetra Pak International S.A.

- Mayr-Melnhof Karton AG

- Rengo Co. Ltd

- Stora Enso Oyj

- Mondi plc

- Muda Packaging Industries Sdn Bhd

- Seow Khim Polythelene Pte Ltd.

- Toyo Ink Pte Ltd.

- LSY Packaging Pte Ltd.

- Paper Products Singapore (Pte) Ltd.

- Amcor plc

- International Paper Company

- Graphic Packaging International LLC

- Oji Holdings Corporation

- Smurfit Westrock plc

- Huhtamaki Oyj

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in E-Commerce Packaging Demand

- 4.2.2 Government Push for Sustainable Packaging and Green Plan 2030

- 4.2.3 Growth of Ready-to-Eat Meal Deliveries Boosting Folding Carton Usage

- 4.2.4 Technological Advancements in Digital Printing for Short Runs

- 4.2.5 Rising Demand for Premium Healthcare Packaging Amid Aging Population

- 4.2.6 Brand-Owner Shift Toward Plastic-to-Paper Substitution

- 4.3 Market Restraints

- 4.3.1 High Land and Labor Costs Limiting Local Production Capacity

- 4.3.2 Competition From Lower-Cost Imports From Malaysia and China

- 4.3.3 Limited Domestic Recovered Fiber Constraining Recycled Board Adoption

- 4.3.4 Volatility in Virgin Paperboard Prices Linked to Global Pulp Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Tetra Pak International S.A.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Rengo Co. Ltd

- 6.4.4 Stora Enso Oyj

- 6.4.5 Mondi plc

- 6.4.6 Muda Packaging Industries Sdn Bhd

- 6.4.7 Seow Khim Polythelene Pte Ltd.

- 6.4.8 Toyo Ink Pte Ltd.

- 6.4.9 LSY Packaging Pte Ltd.

- 6.4.10 Paper Products Singapore (Pte) Ltd.

- 6.4.11 Amcor plc

- 6.4.12 International Paper Company

- 6.4.13 Graphic Packaging International LLC

- 6.4.14 Oji Holdings Corporation

- 6.4.15 Smurfit Westrock plc

- 6.4.16 Huhtamaki Oyj

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

印尼折疊式紙盒包裝:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)可折疊瓦楞紙板包裝:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)