|

市場調查報告書

商品編碼

2061699

非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Africa Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

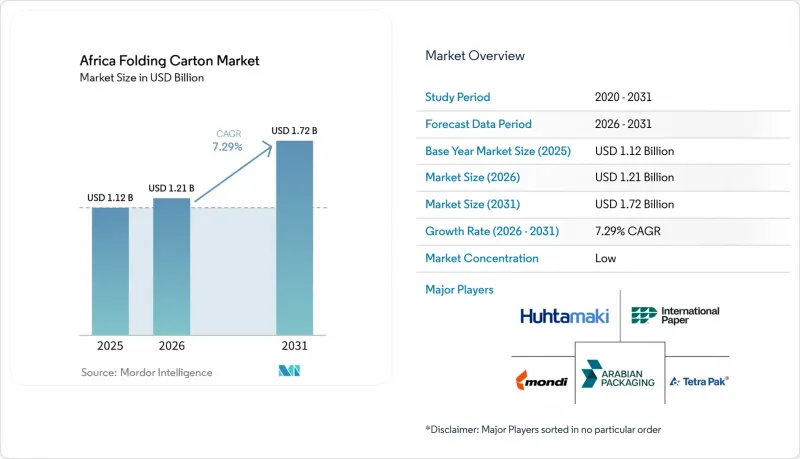

根據 Mordor Intelligence 預測,非洲折疊式紙匣市場規模將從 2025 年的 11.2 億美元成長到 2026 年的 12.1 億美元,到 2031 年將達到 17.2 億美元,2026 年至 2031 年的複合年成長率為 7.29%。

本報告按材料類型(固態漂白硫酸紙漿、折疊紙盒用紙板、塗佈未漂白牛皮紙、白線塑合板等)、印刷技術(膠印、凹版印刷、數位印刷等)、終端用戶行業(食品飲料、電子商務和零售包裝、煙草等)以及地區進行細分。市場預測以美元(USD)為單位。

非洲折疊式紙盒市場的趨勢與洞察

電子商務領域的需求不斷成長

智慧型手機的普及、末端物流的改進以及付款閘道的擴展,推動了奈及利亞、南非、埃及和肯亞等國線上零售業的兩位數成長。銷售時尚、電子產品和個人保養用品的品牌商如今需要既能提升開箱體驗又能經受嚴苛運輸考驗的保護性折疊式紙盒。非洲大陸自由貿易協定(AfCFTA)海關現代化計畫要求的QR碼追溯系統提高了印刷解析度的要求,並促使能夠整合安全功能的加工商更受青睞。數位印刷機縮短了設計週期,並能快速更新促銷密集型線上管道的圖案,而平均訂單量的下降則降低了長期膠印的經濟吸引力。因此,電子商務的結構性需求正在推動非洲折疊式紙盒市場的發展,透過擴大短週期、小批量生產,提高優質材料的利潤率。

食品和飲料行業的擴張

2024年,南非柑橘出口量超過1.645億箱(每箱15公斤),這支撐了對符合歐洲植物檢疫規定的防潮折疊式紙盒的穩定需求。在奈及利亞和肯亞,速食店正迅速採用耐油紙板包裝,以取代已停用的聚苯乙烯翻蓋式容器。都市區家庭可支配收入的成長加速了已調理食品的普及,並促進了SKU(庫存單位)的多樣化。這迫使加工商實施靈活的生產線,以在遵守食品接觸法規的同時控制成本。面向出口的水果、水產品和肉類加工商也在尋求能夠在低溫運輸中承受潮氣且不會分層的紙板。出口和國內消費的這些相互關聯的趨勢,進一步鞏固了食品和飲料在擴大非洲折疊式紙盒市場中的核心作用。

再生紙漿價格波動

2024年下半年,南非向亞洲出口再生紙的增加推高了國內價格,銷量也隨之成長,但Mpact紙製品的毛利率卻下降了2.7個百分點。都市區回收網路正引導廢棄紙纖維流向出口路線,而隨著當地造紙廠競相爭奪紙漿供應,加工商更容易受到現貨市場價格上漲的影響。埃及新近推出的生產者責任再利用(EPR)計畫強制要求標註再生材料含量,這進一步加劇了原料採購的壓力,儘管農村地區缺乏完善的回收基礎設施。雖然部分成本可以透過與回收商簽訂長期合約來規避,但中小加工商缺乏議價能力。除非像Polysmart投資6000萬美元在拉各斯建設的工廠那樣,產能的提升能夠穩定區域供應,否則紙漿價格的波動將繼續對非洲折疊式紙盒市場構成重大拖累。

細分市場分析

到2025年,折疊紙板將佔據折疊式紙盒市場38.43%的佔有率。這主要歸功於其多層結構,兼具剛性和輕盈性。預計實心漂白紙板(SBS)的複合年成長率將達到8.06%,這反映了化妝品和製藥品牌偏好純白衛生纖維的趨勢。未漂白塗佈牛皮紙板因其追求天然美感,在有機和公平貿易食品生產商中越來越受歡迎,而白襯塑合板仍然是成本績效利潤乾貨紙盒的經濟之選。

蒙迪在南非擁有25.3萬公頃經FSC認證的森林,確保了原生紙漿的穩定供應,印證了SBS關於供應能力和可追溯性的說法。同時,南非的再生材料含量目標正推動對脫墨和分散系統的投資,以提高再生紙漿在食品級應用方面的性能,從而加強非洲折疊式紙盒行業回收基礎設施與材料成分演變之間的聯繫。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對高檔食品和飲料包裝盒的需求正在增加。

- 電子商務履約網路的擴展

- 政府在可回收包裝材料方面的永續性義務

- 擴大數位印刷在小批量印刷中的應用。

- 杜拜製藥製造群的成長

- 免稅零售額的激增帶動了紙箱出貨量的上升。

- 市場限制因素

- 原生紙漿和再生紙價格的波動

- 國內紙板生產能力受限

- 中小企業遵守嚴格的食品接觸法規的成本。

- 軟包裝帶來的替代品威脅

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依材料類型

- 固態漂白硫酸漿

- 折疊紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 按地區

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- International Paper Company

- Gulf Printing and Packaging FZ-LLC

- Arabian Packaging Ltd.

- Al Ghurair Printing and Publishing LLC

- Emirates Printing Press LLC

- Al Bayader International LLC

- Tetra Pak International SA

- SIG Combibloc Group AG

- Smurfit WestRock plc

- Mondi plc

- Huhtamaki Oyj

- Ittihad Paper Mill LLC

- Prism Packaging Industries LLC

- Hotpack Packaging Industries LLC

- Trost Creative Packaging GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the africa folding carton market size is expected to grow from USD 1.12 billion in 2025 to USD 1.21 billion in 2026 and is forecast to reach USD 1.72 billion by 2031 at a 7.29% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Gravure Printing, Digital Printing, and More), End-User Industry (Food and Beverage, E-Commerce and Retail-Ready Packaging, Tobacco and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Africa Folding Carton Market Trends and Insights

Growing Demand from the E-Commerce Sector

Smartphone adoption, improved last-mile logistics, and expanding payment gateways are fueling double-digit online retail growth in Nigeria, South Africa, Egypt, and Kenya. Brand owners shipping fashion, electronics, and personal-care items now require protective, visually distinct folding cartons that enhance unboxing experiences and withstand the rigors of parcel networks. QR-code traceability demanded by customs modernization programs under AfCFTA raises print-resolution requirements and favors converters able to integrate security features. Digital presses shorten design cycles, allowing rapid artwork refreshes for promotion-heavy online channels, while smaller average order quantities reduce the economic appeal of long offset runs. The structural pull from e-commerce therefore expands short-run volumes, supports higher margins on premium substrates, and bolsters the Africa folding carton market outlook.

Expansion of Food and Beverage Industry

Citrus exports from South Africa exceeded 164.5 million 15-kilogram-equivalent cartons in 2024, anchoring steady demand for moisture-resistant folding cartons that meet European phytosanitary rules. Nigeria and Kenya are witnessing rapid rollouts of quick-service restaurants that replace banned polystyrene clamshells with grease-resistant paperboard packaging. Rising disposable incomes across urban households accelerate packaged-meal adoption and diversify SKU counts, pushing converters toward flexible production lines that balance food-contact compliance with cost control. Export-oriented fruit, seafood, and meat processors also demand cartonboard that endures cold-chain humidity without delamination. These intertwined export and domestic consumption trends reinforce the central role of food and beverages in scaling the Africa folding carton market.

Volatility in Recycled Paper Pulp Prices

Recovered-paper exports from South Africa to Asia lifted domestic prices in late 2024, trimming Mpact's paper gross margin by 2.7% points despite volume gains. Urban collection networks funnel post-consumer fiber into export channels, leaving converters exposed to spot-market spikes when local mills compete for supply.Egypt's early-stage EPR program magnifies feedstock pressure by stipulating recycled-content labeling without parallel rural collection infrastructure. Long-term contracts with aggregators partly hedge costs, but smaller converters lack bargaining power. Until incremental capacity from initiatives such as Polysmart's USD 60 million Lagos plant stabilizes regional supply, pulp price swings will remain a material drag on the Africa folding carton market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Sustainable Packaging Regulations

- Rapid Growth of Quick-Commerce Dark Stores in Urban Hubs

- Skilled Technician Shortage Limiting Automation Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard captured 38.43% of the African folding carton market in 2025, owing to its multi-ply architecture that balances rigidity and lightweighting. Solid Bleached Board is forecast to rise at an 8.06% CAGR, reflecting cosmetics and pharmaceutical brands' preference for pristine whiteness and hygienic fiber. Coated Unbleached Kraftboard is gaining traction among organic and fair-trade food producers eager to showcase natural aesthetics, while White-lined Chipboard remains the value option for dry-goods cartons despite narrower margin buffers.

Mondi's 253,000 hectares of FSC-certified forestry in South Africa secure a virgin fiber supply, supporting SBS availability and traceability claims. Concurrently, South Africa's recycled-content targets are stimulating investment in de-inking and dispersion systems that upgrade recovered fiber for food-grade applications, tightening the linkage between recycling infrastructure and material-mix evolution in the Africa folding carton industry.

List of Companies Covered in this Report:

- International Paper Company

- Gulf Printing and Packaging FZ-LLC

- Arabian Packaging Ltd.

- Al Ghurair Printing and Publishing LLC

- Emirates Printing Press LLC

- Al Bayader International LLC

- Tetra Pak International SA

- SIG Combibloc Group AG

- Smurfit WestRock plc

- Mondi plc

- Huhtamaki Oyj

- Ittihad Paper Mill LLC

- Prism Packaging Industries LLC

- Hotpack Packaging Industries LLC

- Trost Creative Packaging GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of Food and Beverage Carton Demand

- 4.2.2 Expansion of E-commerce Fulfillment Networks

- 4.2.3 Government Sustainability Mandates for Recyclable Packaging

- 4.2.4 Rising Adoption of Digital Printing for Short-Run Jobs

- 4.2.5 Growth of Dubai Pharmaceutical Manufacturing Cluster

- 4.2.6 Surge in Duty-Free Retail Sales Boosting Carton Volumes

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Fiber and Recovered Paper Prices

- 4.3.2 Limited Domestic Paperboard Production Capacity

- 4.3.3 Stringent Food-Contact Compliance Costs for SMEs

- 4.3.4 Substitution Threat From Flexible Packaging Formats

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 South Africa

- 5.4.2 Nigeria

- 5.4.3 Egypt

- 5.4.4 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 International Paper Company

- 6.4.2 Gulf Printing and Packaging FZ-LLC

- 6.4.3 Arabian Packaging Ltd.

- 6.4.4 Al Ghurair Printing and Publishing LLC

- 6.4.5 Emirates Printing Press LLC

- 6.4.6 Al Bayader International LLC

- 6.4.7 Tetra Pak International SA

- 6.4.8 SIG Combibloc Group AG

- 6.4.9 Smurfit WestRock plc

- 6.4.10 Mondi plc

- 6.4.11 Huhtamaki Oyj

- 6.4.12 Ittihad Paper Mill LLC

- 6.4.13 Prism Packaging Industries LLC

- 6.4.14 Hotpack Packaging Industries LLC

- 6.4.15 Trost Creative Packaging GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)